Ten Tools Managers Can Use to Get Long-Term Committed Shareholders

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

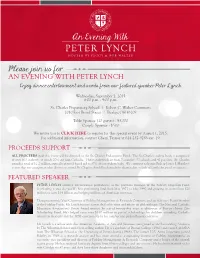

Please Join Us for an EVENING with PETER LYNCH Enjoy Dinner, Entertainment and Words from Our Featured Speaker, Peter Lynch

Please join us for AN EVENING WITH PETER LYNCH Enjoy dinner, entertainment and words from our featured speaker, Peter Lynch. Wednesday, September 2, 2015 6:00 p.m. - 9:00 p.m. St. Charles Preparatory School | Robert C. Walter Commons 2010 East Broad Street | Bexley, OH 43209 Table Sponsor (10 guests) - $5,000 Couple Sponsor - $500 We invite you to CLICK HERE to register for this special event by August 1, 2015. For additional information, contact Cherri Taynor at 614-252-9288 ext. 19. PROCEEDS SUPPORT ALL PROCEEDS from this event will be directed to the St. Charles Endowment Fund. The St. Charles student body is comprised of over 600 students, of which 20% are non-Catholic. These students draw from 7 counties, 53 schools and 42 parishes. St. Charles awards a total of $1.2 million annually in need-based aid to 37% of our student body. We continue to honor Bishop James J. Hartley’s vision that no young man who desires to attend St. Charles should be denied the chance due to lack of family financial resources. FEATURED SPEAKER PETER LYNCH attained international prominence as the portfolio manager of the Fidelity Magellan Fund, developing it into the world’s best performing fund from May 1977 to May 1990 and growing its assets from $20 million to over $14 billion and helping millions of American investors. Though currently Vice Chairman of Fidelity Management & Research Company and an Advisory Board Member of the Fidelity Funds, Mr. Lynch focuses a great deal of his time and efforts on philanthropy. The National Catholic Education Association’s Seton Award winner, he served twenty-five years as chairman of Boston’s Inner City Scholarship Fund. -

Liberty Media Corporation Owns Interests in a Broad Range of Media, Communications and Entertainment Businesses

2021 PROXY STATEMENT 2020 ANNUAL REPORT YEARS OF LIBERTY 2021 PROXY STATEMENT 2020 ANNUAL REPORT LETTER TO SHAREHOLDERS STOCK PERFORMANCE INVESTMENT SUMMARY PROXY STATEMENT FINANCIAL INFORMATION CORPORATE DATA ENVIRONMENTAL STATEMENT FORWARD-LOOKING STATEMENTS Certain statements in this Annual Report constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding business, product and marketing plans, strategies and initiatives; future financial performance; demand for live events; new service offerings; renewal of licenses and authorizations; revenue growth and subscriber trends at Sirius XM Holdings Inc. (Sirius XM Holdings); our ownership interest in Sirius XM Holdings; the recoverability of goodwill and other long- lived assets; the performance of our equity affiliates; projected sources and uses of cash; the payment of dividends by Sirius XM Holdings; the impacts of the novel coronavirus (COVID-19); the anticipated non-material impact of certain contingent liabilities related to legal and tax proceedings; and other matters arising in the ordinary course of business. In particular, statements in our “Letter to Shareholders” and under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Quantitative and Qualitative Disclosures About Market Risk” contain forward looking statements. Where, in any forward-looking statement, we express an expectation or belief as to future results or events, such expectation or belief -

Testimony of Gene Kimmelman, Senior Director for Advocacy and Public Policy, Consumers Union

Testimony of Gene Kimmelman, Senior Director for Advocacy and Public Policy, Consumers Union Before the Antitrust, Competition Policy and Consumer Rights Subcommittee of the Senate Judiciary Committee On News Corp./DirecTV Merger June 18, 2003 Washington Office 1666 Connecticut Avenue, N.W. Suite 310 • Washington, D.C. 20009-1039 (202) 462-6262 • fax (202) 265-9548 • http://www.consumersunion.org SUMMARY Consumers Union1 welcomes this opportunity to testify before the Senate Antitrust, Competition Policy and Consumer Rights Subcommittee regarding the proposed merger between the News Corporation (“News Corp.”) and Hughes Electronics Corporation’s satellite television unit DIRECTV (“DirecTV”). Given the current concentration in the media marketplace, as well as the further concentration that will result from the Federal Communications Commission’s (FCC’s) recent relaxation of media ownership rules, we believe that the proposed merger between network and cable giant News Corp. and DirecTV, the largest direct broadcast satellite (DBS) service provider, will further increase prices for consumers and decrease the diversity of voices in the media marketplace. Today, consumers are not receiving the fruits that a competitive cable and satellite marketplace should deliver, and consumers are likely to suffer further harm if antitrust officials do not impose substantial conditions on the proposed deal between News Corp. and DirecTV. Since passage of the 1996 Telecommunications Act, cable rates have risen over 50%,2 and FCC data show that satellite competition is not creating downward pressure on cable rates. Despite the promise for more diversity from new technologies such as the Internet and satellite, a mere five media companies control nearly the same prime time audience shares as the Big Three networks did 40 years ago.3 Unfortunately, the market for news production and distribution is becoming more concentrated. -

Banking, Securities, and Insurance

UC Berkeley UC Berkeley Electronic Theses and Dissertations Title Inside the Castle Gates: How Foreign Corporations Nagivate Japan's Policymaking Processes Permalink https://escholarship.org/uc/item/3q9796r6 Author Kushida, Kenji Erik Publication Date 2010 Peer reviewed|Thesis/dissertation eScholarship.org Powered by the California Digital Library University of California Inside the Castle Gates: How Foreign Companies Navigate Japan‘s Policymaking Processes By Kenji Erik Kushida A dissertation submitted in partial satisfaction of the requirements for the degree of Doctor of Philosophy in Political Science in the Graduate Division of the University of California, Berkeley Committee in charge: Professor Steven K. Vogel, Chair Professor John Zysman Professor T.J. Pempel Professor Stephen Cohen Fall 2010 Abstract Inside the Castle Gates: How Foreign Companies Navigate Japan‘s Policymaking Processes by Kenji Erik Kushida Doctor of Philosophy in Political Science University of California, Berkeley Professor Steven K. Vogel, Chair Multinational corporations (MNCs) are at the heart of today‘s global economy, but their effects on the politics of advanced industrialized countries have not been studied systematically. This dissertation analyzes the case of Japan, a country most likely to reveal foreign MNCs‘ influence. Japan developed for most of its history with an extremely low presence of foreign MNCs, but it experienced a dramatic influx from the mid-1990s, particularly in long-protected sectors at the core of its postwar development model of capitalism. The dissertation explains an observed divergence in the political strategies of foreign MNCs in Japan—disruptive challenges to existing policymaking processes and norms of government-business interactions, versus insider strategies, in which MNCs worked within established organizations and prevailing modes of policymaking. -

2020 Investor Day

2020 Investor Day November 19, 2020 Disclaimers Forward-Looking Statements This presentation includes certain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements about business strategies including Formula 1’s sustainability strategy, the impact of COVID-19, market potential, new service and product launches, Formula 1 tax considerations, anticipated benefits from the new Concorde Agreement, future financial performance (including Formula 1 free cash flow), capital allocation, stock repurchases, Sirius XM Holdings Inc.’s (“SIRI”) realization of benefits from its acquisition of Pandora Media, Inc., the Atlanta Braves mixed-use facility, continuation of our stock repurchase program, the special purpose acquisition company and its initial public offering and other matters that are not historical facts. These forward-looking statements involve many risks and uncertainties that could cause actual results to differ materially from those expressed or implied by such statements, including, without limitation, possible changes in market acceptance of new products or services, competitive issues, regulatory matters, continued access to capital on terms acceptable to Liberty Media or its subsidiaries, the impact of COVID-19, including on general market conditions and the ability of Formula 1, the Braves and Live Nation to hold live events and fan attendance at such events, and market conditions conducive to stock repurchases. These forward-looking statements speak only as of the date of this presentation, and Liberty Media expressly disclaims any obligation or undertaking to disseminate any updates or revisions to any forward-looking statement contained herein to reflect any change in Liberty Media’s expectations with regard thereto or any change in events, conditions or circumstances on which any such statement is based. -

UNITED STATES DISTRICT COURT NORTHERN DISTRICT of ILLINOIS EASTERN DIVISION LEONARD SOKOLOW, Individually and on Behalf of All O

Case: 1:18-cv-01039 Document #: 209 Filed: 11/13/19 Page 1 of 25 PageID #:3098 UNITED STATES DISTRICT COURT NORTHERN DISTRICT OF ILLINOIS EASTERN DIVISION LEONARD SOKOLOW, Individually and on ) Case No. 1:18-cv-01039 Behalf of All Others Similarly Situated, ) ) Hon. Judge Robert M. Dow, Jr. Plaintiff, ) ) vs. ) ) LJM FUNDS MANAGEMENT, LTD., et al., ) ) Defendants. ) ) DECLARATION OF JAMES W. JOHNSON IN SUPPORT OF (I) LEAD PLAINTIFFS’ MOTION FOR FINAL APPROVAL OF PARTIAL CLASS ACTION SETTLEMENT AND PLAN OF ALLOCATION AND (II) LEAD COUNSEL’S MOTION FOR AWARD OF ATTORNEYS’ FEES AND PAYMENT OF LITIGATION EXPENSES I, JAMES W. JOHNSON, declare as follows pursuant to 28 U.S.C. §1746: 1. I am a partner of the law firm of Labaton Sucharow LLP (“Labaton Sucharow”). Labaton Sucharow and Robbins Geller Rudman & Dowd LLP (“Robbins Geller”) serve as Court-appointed Lead Counsel for Lead Plaintiffs Justin and Jenny Kaufman, Joseph N. Wilson, Dr. Larry and Marilyn Cohen, Tradition Capital Management LLC (“Tradition”), and SRS Capital Advisors, Inc. (“SRS”) (collectively, “Lead Plaintiffs”), and the proposed Settlement Class in the Action.1 I have been actively involved in prosecuting and resolving the Action, am 1 All capitalized terms used herein that are not otherwise defined shall have the meanings provided in the Stipulation and Agreement of Partial Settlement, dated as of August 19, 2019 (ECF No. 192) (the “Stipulation”), which was entered into by and among (a) Lead Plaintiffs, on behalf of themselves and the Settlement Class; and (b) defendants Two Roads Shared Trust (the “Trust”), Northern Lights Distributors, LLC (“NLD”), NorthStar Financial Services Group, LLC (“NorthStar”), and Mark D. -

Liberty Media Corporation Owns Interests in a Broad Range of Media, Communications and Entertainment Businesses

Annual REPORT Proxy STATEMENT 2019 2018 Annual REPORT Proxy STATEMENT LETTER TO SHAREHOLDERS STOCK PERFORMANCE INVESTMENT SUMMARY PROXY STATEMENT FINANCIAL INFORMATION CORPORATE DATA ENVIRONMENTAL STATEMENT Certain statements in this Annual Report constitute forward-looking • changes in the nature of key strategic relationships with partners, statements within the meaning of the Private Securities Litigation Reform vendors and joint venturers; Act of 1995, including statements regarding our business, product and • general economic and business conditions and industry trends; marketing strategies and initiatives; new service offerings; revenue and subscriber growth at Sirius XM Holdings Inc. (“SIRIUS XM”); the • consumer spending levels, including the availability and amount of recoverability of our goodwill and other long-lived assets; the performance individual consumer debt; of our equity affiliates; our projected sources and uses of cash; the • rapid technological changes; payment of dividends by SIRIUS XM; the expected benefits of SIRIUS XM’s acquisition of Pandora; the continuation of our stock repurchase program; • impairments of third-party intellectual property rights; monetization of sports media rights; plans for the Battery Atlanta; the • our indebtedness could adversely affect operations and could limit the anticipated non-material impact of certain contingent liabilities related to ability of our subsidiaries to react to changes in the economy or our legal and tax proceedings; and other matters arising in the ordinary course industry; of business. In particular, statements in our “Letter to Shareholders” and under “Management’s Discussion and Analysis of Financial Condition • failure to protect the security of personal information about our and Results of Operations” and “Quantitative and Qualitative Disclosures businesses’ customers, subjecting our businesses to potentially costly About Market Risk” contain forward looking statements. -

The Great Telecom Meltdown for a Listing of Recent Titles in the Artech House Telecommunications Library, Turn to the Back of This Book

The Great Telecom Meltdown For a listing of recent titles in the Artech House Telecommunications Library, turn to the back of this book. The Great Telecom Meltdown Fred R. Goldstein a r techhouse. com Library of Congress Cataloging-in-Publication Data A catalog record for this book is available from the U.S. Library of Congress. British Library Cataloguing in Publication Data Goldstein, Fred R. The great telecom meltdown.—(Artech House telecommunications Library) 1. Telecommunication—History 2. Telecommunciation—Technological innovations— History 3. Telecommunication—Finance—History I. Title 384’.09 ISBN 1-58053-939-4 Cover design by Leslie Genser © 2005 ARTECH HOUSE, INC. 685 Canton Street Norwood, MA 02062 All rights reserved. Printed and bound in the United States of America. No part of this book may be reproduced or utilized in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without permission in writing from the publisher. All terms mentioned in this book that are known to be trademarks or service marks have been appropriately capitalized. Artech House cannot attest to the accuracy of this information. Use of a term in this book should not be regarded as affecting the validity of any trademark or service mark. International Standard Book Number: 1-58053-939-4 10987654321 Contents ix Hybrid Fiber-Coax (HFC) Gave Cable Providers an Advantage on “Triple Play” 122 RBOCs Took the Threat Seriously 123 Hybrid Fiber-Coax Is Developed 123 Cable Modems -

Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16

Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16:57:32 Desc Main Document Page 1 of 137 Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16:57:32 Desc Main Document Page 2 of 137 Exhibit A Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16:57:32 Desc Main Document Page 3 of 137 Exhibit A1 Served via Overnight Mail Name Attention Address 1 Address 2 City State Zip Country Aastha Broadcasting Network Limited Attn: Legal Unit213 MezzanineFl Morya LandMark1 Off Link Road, Andheri (West) Mumbai 400053 IN Abs Global LTD Attn: Legal O'Hara House 3 Bermudiana Road Hamilton HM08 BM Abs-Cbn Global Limited Attn: Legal Mother Ignacia Quezon City Manila PH Aditya Jain S/O Sudhir Kumar Jain Attn: Legal 12, Printing Press Area behind Punjab Kesari Wazirpur Delhi 110035 IN AdminNacinl TelecomunicacionUruguay Complejo Torre De Telecomuniciones Guatemala 1075. Nivel 22 HojaDeEntrada 1000007292 5000009660 Montevideo CP 11800 UY Advert Bereau Company Limited Attn: Legal East Legon Ars Obojo Road Asafoatse Accra GH Africa Digital Network Limited c/o Nation Media Group Nation Centre 7th Floor Kimathi St PO Box 28753-00100 Nairobi KE Africa Media Group Limited Attn: Legal Jamhuri/Zaramo Streets Dar Es Salaam TZ Africa Mobile Network Communication Attn: Legal 2 Jide Close, Idimu Council Alimosho Lagos NG Africa Mobile Networks Cameroon Attn: Legal 131Rue1221 Entree Des Hydrocarbures Derriere Star Land Hotel Bonapriso-Douala Douala CM Africa Mobile Networks Cameroon Attn: Legal BP12153 Bonapriso Douala CM Africa Mobile Networks Gb, -

Liberty Braves Group

g.research, LLC August 20, 2018 One Corporate Center Rye, NY 10580-1422 g.research, LLC Tel (914) 921-5150 www.gabellisecurities.com Liberty Braves Group (BATRA - $26.41 - NASDAQ) 20 Year Old Ronald Acuna Jr. and 21 Year Old All-Star Ozzie Albies Source: Bleacher Report, research, LLC Playoff Push John Tinker g.research, LLC 2018 (914) 921-8348 -Please Refer To Important Disclosures On The Last Page Of This Report- g.research, LLC One Corporate Center g.research, LLC August 20, 2018 Rye, NY 10580-1422 Tel (914) 921-5150 www.gabellisecurities.com Liberty Braves Group (BATRA - $26.41 - NASDAQ) Playoff Push - Buy Year EBITDA EV/EBITDA PMV Dividend: None Current Return: Nil 2020P $90 20.9x $43 A Shares 10.2 million 2019P 88 21.5 42 B Shares 1.0 " 2018E 76 24.9 37 K Shares 48.8 " 2017A 7 NM 34 52-Week Range: $27.02 - $21.35 COMPANY OVERVIEW The Atlanta Braves were founded in 1871 and are the oldest continuously operating professional sports franchise in US. The Liberty Braves Group moved to the new 41.5K seat SunTrust Park, Cobb County from Atlanta in February 2017. Liberty Media Corporation recapitalized the Atlanta Braves as a tracking stock in April 2016 along with Liberty SiriusXM and Liberty Formula One. Assets include the Major League Baseball team, the Atlanta Braves, the Atlanta Braves' stadium and the Battery real estate project. The Battery Atlanta is a 46 acre mixed use development with residential and commercial property which feeds off the stadium (16 acres) on 82 acres with initial completion in 2018 and 20 acres to be completed by 2022. -

Our Firm and Fidelity. Working Together for You. Helping to Serve Your Best Interests

Our Firm and Fidelity. Working Together for You. Helping to serve your best interests. 31822.indd A 9/20/07 10:52:30 AM 331822.indd1822.indd B 99/12/07/12/07 11:56:14:56:14 PPMM A powerful combination As your financial advisor, we’re expected to make decisions about your money based on the highest degree of scrutiny. You can be assured that we use the same approach when choosing the service providers we employ to help meet your financial objectives. This is why we’ve selected Fidelity Investments as our custodian. What is a custodian? A custodian is a financial institution that has legal responsibility for a customer’s securities. Custodianship includes management as well as safekeeping, and this service incurs additional fees. Our firm, like all investment managers, is required to have a custodian. Investments that you entrust to our firm are placed in custody with Fidelity’s clearing firm, National Financial Services LLC (NFS) — one of the largest clearing providers in the industry. A clearing firm is an organization that works with financial exchanges to handle the confirmation, delivery, and settlement of transactions. When you’re selecting your financial advisor, it can be a critical factor to consider who your advisor uses to custody your investments, as this will help to determine the level of service, support, and protection that you can expect from your financial advisor. OUR FIRM AND FIDELITY 1 331822.indd1822.indd C 99/20/07/20/07 33:06:50:06:50 PPMM How does our relationship with Fidelity benefit you? An experienced, reputable firm helping to (SIPC). -

United States District Court District of South Carolina (Columbia Division)

3:17-cv-02616-MBS Date Filed 04/23/20 Entry Number 229 Page 1 of 57 UNITED STATES DISTRICT COURT DISTRICT OF SOUTH CAROLINA (COLUMBIA DIVISION) In re SCANA Corporation Securities Civil Action No. 3:17-CV-2616-MBS Litigation JOINT DECLARATION OF JOHN C. BROWNE AND JAMES W. JOHNSON IN SUPPORT OF (I) LEAD PLAINTIFFS’ MOTION FOR FINAL APPROVAL OF CLASS ACTION SETTLEMENT AND PLAN OF ALLOCATION; AND (II) LEAD COUNSEL’S MOTION FOR AN AWARD OF ATTORNEYS’ FEES AND PAYMENT OF LITIGATION EXPENSES 3:17-cv-02616-MBS Date Filed 04/23/20 Entry Number 229 Page 2 of 57 TABLE OF CONTENTS Page TABLE OF EXHIBITS TO DECLARATION.............................................................................. iii I. INTRODUCTION .............................................................................................................. 1 II. PROSECUTION OF THE ACTION .................................................................................. 6 A. Factual Background of the Claims .......................................................................... 6 B. Filing of the Initial Complaint and Appointment of Lead Plaintiffs and Lead Counsel .......................................................................................................... 8 C. Lead Counsel’s Investigation and the Consolidated Class Action Complaint ................................................................................................................ 9 D. Continued Informal Discovery Following Filing of Complaint ........................... 11 E. Defendants’ Motions to