Report Name:Korea Seafood Market Update 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bibliography Database of Living/Fossil Sharks, Rays and Chimaeras (Chondrichthyes: Elasmobranchii, Holocephali) Papers of the Year 2016

www.shark-references.com Version 13.01.2017 Bibliography database of living/fossil sharks, rays and chimaeras (Chondrichthyes: Elasmobranchii, Holocephali) Papers of the year 2016 published by Jürgen Pollerspöck, Benediktinerring 34, 94569 Stephansposching, Germany and Nicolas Straube, Munich, Germany ISSN: 2195-6499 copyright by the authors 1 please inform us about missing papers: [email protected] www.shark-references.com Version 13.01.2017 Abstract: This paper contains a collection of 803 citations (no conference abstracts) on topics related to extant and extinct Chondrichthyes (sharks, rays, and chimaeras) as well as a list of Chondrichthyan species and hosted parasites newly described in 2016. The list is the result of regular queries in numerous journals, books and online publications. It provides a complete list of publication citations as well as a database report containing rearranged subsets of the list sorted by the keyword statistics, extant and extinct genera and species descriptions from the years 2000 to 2016, list of descriptions of extinct and extant species from 2016, parasitology, reproduction, distribution, diet, conservation, and taxonomy. The paper is intended to be consulted for information. In addition, we provide information on the geographic and depth distribution of newly described species, i.e. the type specimens from the year 1990- 2016 in a hot spot analysis. Please note that the content of this paper has been compiled to the best of our abilities based on current knowledge and practice, however, -

Does Climate Change Bolster the Case for Fishery Reform in Asia? Christopher Costello∗

Does Climate Change Bolster the Case for Fishery Reform in Asia? Christopher Costello∗ I examine the estimated economic, ecological, and food security effects of future fishery management reform in Asia. Without climate change, most Asian fisheries stand to gain substantially from reforms. Optimizing fishery management could increase catch by 24% and profit by 34% over business- as-usual management. These benefits arise from fishing some stocks more conservatively and others more aggressively. Although climate change is expected to reduce carrying capacity in 55% of Asian fisheries, I find that under climate change large benefits from fishery management reform are maintained, though these benefits are heterogeneous. The case for reform remains strong for both catch and profit, though these numbers are slightly lower than in the no-climate change case. These results suggest that, to maximize economic output and food security, Asian fisheries will benefit substantially from the transition to catch shares or other economically rational fishery management institutions, despite the looming effects of climate change. Keywords: Asia, climate change, fisheries, rights-based management JEL codes: Q22, Q28 I. Introduction Global fisheries have diverged sharply over recent decades. High governance, wealthy economies have largely adopted output controls or various forms of catch shares, which has helped fisheries in these economies overcome inefficiencies arising from overfishing (Worm et al. 2009) and capital stuffing (Homans and Wilen 1997), and allowed them to turn the corner toward sustainability (Costello, Gaines, and Lynham 2008) and profitability (Costello et al. 2016). But the world’s largest fishing region, Asia, has instead largely pursued open access and input controls, achieving less long-run fishery management success (World Bank 2017). -

Delivery Menu

Delivery Menu. Stuck between binge-watching your favourite show and a delicious meal? Well, debate no more! Our burgers and lobsters are now available for take-out from our Raffles restaurant and delivery, right to your doorstep. Please note that our delivery menu prices are lower than our usual a la carte prices. The following prices are only valid whilst our restaurants are temporarily closed. Key Worker Discount. We will be offering a 15% discount on take-outs to all frontline workers. This includes health workers, police officers, immigration officers, laboratory staff and more. To claim this, simply flash your ID card to any of our team members. Starters. Pan-Fried King Prawns. Salted Egg Yolk Cuttlefish. King Prawns served with our sweet and sour sauce and garnished Crispy baby cuttlefish flavoured with home-made with spring onion. salted egg yolk spice mix. 3 pieces $12.84 / 6 pieces $23.54 $10.70 Lobster Mac & Cheese. Kale & Quinoa Salad. Succulent lobster meat and macaroni folded in Quinoa, avocado and kale leaves with fig, cranberry a lobster bisque and creamy four cheese sauce. and roasted walnuts. Tossed in a balsamic dressing $16.05 served with succulent lobster meat and shavings of radish. Marinated Octopus. $18.19 Octopus tentacle marinated with lemon, parsley, garlic and olive oil. Served either chilled or grilled and served with fresh lime. Lobster Nuggets. $16.05 Crispy lobster claw ‘nuggets’ in a spicy batter served with a cooling lemon mayo. $17.12 Combos. We’ve made your life a little bit easier, get the best of both worlds! Minimum 2 people Main Course Options: Mayfair Burger, Smoked BBQ Burger, The Impossible Burger, Original Roll, Seven Samurai Roll, California Roll or Surf & Turf Roll.* Side Options: Sautéed Mushrooms, Garlic Spinach, Truffle Fries, Sweet Potato Fries or Salted Egg Yolk Fries. -

Southwest Guide: Your Use to Word

BEST CHOICES GOOD ALTERNATIVES AVOID How to Use This Guide Arctic Char (farmed) Clams (US & Canada wild) Bass: Striped (US gillnet, pound net) Bass (US farmed) Cod: Pacific (Canada & US) Basa/Pangasius/Swai Most of our recommendations, Catfish (US) Crab: Southern King (Argentina) Branzino (Mediterranean farmed) including all eco-certifications, Clams (farmed) Lobster: Spiny (US) Cod: Atlantic (gillnet, longline, trawl) aren’t on this guide. Be sure to Cockles Mahi Mahi (Costa Rica, Ecuador, Cod: Pacific (Japan & Russia) Cod: Pacific (AK) Panama & US longlines) Crab (Asia & Russia) check out SeafoodWatch.org Crab: King, Snow & Tanner (AK) Oysters (US wild) Halibut: Atlantic (wild) for the full list. Lobster: Spiny (Belize, Brazil, Lionfish (US) Sablefish/Black Cod (Canada wild) Honduras & Nicaragua) Lobster: Spiny (Mexico) Salmon: Atlantic (BC & ME farmed) Best Choices Mahi Mahi (Peru & Taiwan) Mussels (farmed) Salmon (CA, OR & WA) Octopus Buy first; they’re well managed Oysters (farmed) Shrimp (Canada & US wild, Ecuador, Orange Roughy and caught or farmed responsibly. Rockfish (AK, CA, OR & WA) Honduras & Thailand farmed) Salmon (Canada Atlantic, Chile, Sablefish/Black Cod (AK) Squid (Chile & Peru) Norway & Scotland) Good Alternatives Salmon (New Zealand) Squid: Jumbo (China) Sharks Buy, but be aware there are Scallops (farmed) Swordfish (US, trolls) Shrimp (other imported sources) Seaweed (farmed) Tilapia (Colombia, Honduras Squid (Argentina, China, India, concerns with how they’re Shrimp (US farmed) Indonesia, Mexico & Taiwan) Indonesia, -

A Review of the Biology for Pacific Saury, Cololabis Saira in the North

North Pacific Fisheries Commission NPFC-2019-SSC PSSA05-WP13 (Rev. 1) A review of the biology for Pacific saury, Cololabis saira in the North Pacific Ocean Taiki Fuji1*, Satoshi Suyama2, Shin-ichiro Nakayama3, Midori Hashimoto1, Kazuhiro Oshima1 1National Research Institute of Far Seas Fisheries, Japan Fisheries Research and Education Agency 2Tohoku national Fisheries Research Institute, Japan Fisheries Research and Education Agency 3National Research Institute of Fisheries Science, Fisheries Research and Education Agency *Corresponding author’s email address: [email protected] Contents 1. Introduction…………………………………………………………………………………………2 2. Stock identity……………………………………………………………………………………….2 3. Early life history……………………………………………………………………………………2 3-1. Spawning ground………………………………………………………………………………2 3-2. Larval transportation……………………………………………………………………………3 3-3. Recruitment variability………………………………………………………………………….4 4. Feeding habits and predators…………………………………………………………………………4 5. Growth………………………………………………………………………………………………..5 6. Maturation…………………………………………………………………………………………….5 6-1. Spawning pattern, fecundity and spawning duration…………………………………………….5 6-2. Seasonal change of maturity size………………………………...................................................6 6-3. Maturation schedule for each seasonal cohort considering growth and maturation size…………6 6-4. Maturation and environmental factors……………………………………………………………7 6-5. Percentage of matured fish………………………………………………………………………..7 7. Distribution and migration…………………………………………………………………………….7 8. Natural mortality………………………………………………………………………………………9 -

FDA: "Glowing" Seafood?

FDA: "Glowing" Seafood? http://web.archive.org/web/20080225162926/http://vm.cfsan.fda.gov/~ea... U.S. Food and Drug Administration Seafood Products Research Center July 1998 "GLOWING" SEAFOOD? by Patricia N. Sado* Introduction Seafood that produces a bright, blue-green light in the dark could be a meal from outer space or haute cuisine in a science fiction novel. The U. S. Food and Drug Administration (FDA) has received many consumer complaints about various seafood products "glowing" in the dark. Some of these consumers called their local health departments, poison control centers, and their U.S. Senator because they thought they had been poisoned by radiation. These consumers said they had trouble convincing people that their seafood was emitting light. One consumer took his imitation crabmeat to a local television station. Unfortunately his seafood had dried out and did not glow for the television reporters. Several consumers said that it took them many weeks before they found phone numbers for various government agencies to make inquiries. Several consumers thought their "glowing" seafood was due to phosphorescing phytoplankton, or even fluorescence. The consumers' seafood products "glowing" in the dark were not due to radiation or to fluorescence, which requires an ultraviolet light to trigger the reaction. These seafood products exhibited luminescence due to the presence of certain bacteria that are capable of emitting light. Luminescence by bacteria is due to a chemical reaction catalyzed by luciferase, a protein similar to that found in fireflies. The reaction involves oxidation of a reduced flavin mononucleotide and a long chain aliphatic aldehyde by molecular oxygen to produce oxidized flavin plus fatty acid and light (5, 12). -

Spiny Lobster and Prawn (Shrimp) Regulations, 1973 Article 1

Spiny Lobster and Prawn (Shrimp) Regulations, 1973 Article 1. - These regulations may be cited as the Spiny Lobster and Prawn (Shrimp) Regulations, 1973. Article 2. - No person shall fish for, take, or land from any vessel any spiny lobster the carapace length of which is less than eight centimetres (3.15 inches) or the tail length of which is less than eleven and one half centimetres (4.50 inches). Article 3. - No person shall purchase or have in his possession any spiny lobster the carapace length of which is less than eight centimetres (3.15 inches) or the tail length of which is less than eleven and one half centimetres (4...50 inches). Article 4. - (1) No person shall fish for, or take any spiny lobster that is in the soft-shell stage. (2) No person shall sell, purchase or have in his possession any spiny lobster which is in the soft-shell stage. Article 5. - No person shall land from any vessel or sell or have in his possession any spiny lobster tail which: (a) is in such a condition that it cannot be measured; or (b) has the calcified bar of the tergum of the first abdominal segment fractured. Article 6. - (1) Every person who takes any spiny lobster that is carrying external eggs shall immediately return it alive with as little injury as possi~le into the water from which it was taken (2) No person shall remove the external eggs from any female lobster or from any spiny lobster tail. (3) No person shall buy, sell or expose for sale, or have in his possession any female spiny lobster or any spiny lobster tail from which any of the erteYnal eggs have been removed. -

A Preliminary Study on ABC Estimation Approach for Ecosystem-Based TAC T Management

Ocean and Coastal Management 157 (2018) 9–22 Contents lists available at ScienceDirect Ocean and Coastal Management journal homepage: www.elsevier.com/locate/ocecoaman A preliminary study on ABC estimation approach for ecosystem-based TAC T management ∗ Hee Joong Kanga, Young Il Seoa, Chang Ik Zhangb, a National Institute of Fisheries Science, 216, Gijanghaean-ro, Gijang-eup, Gijang-gun, Busan, Republic of Korea b Pukyong National University, 45, Yongso-ro, Nam-gu, Busan, Republic of Korea ARTICLE INFO ABSTRACT Keywords: Korea's acceptable biological catch (ABC) for total allowable catch (TAC) management has been estimated by a Ecosystem-based fisheries assessment five-tier system that relies on population-based stock assessment models according to available ecological in- Acceptable biological catch formation for pelagic or demersal species. To overcome the limitations of the current ABC estimation system Total allowable catch based on population dynamic models, this study attempted to integrate the ecosystem-based fisheries assessment Species risk index (EBFA) approach into Korea's current ABC estimation system, and has developed an ABC estimation approach for Sustainability ecosystem-based TAC management. To estimate an ecosystem-based ABC, ABC estimated by the current ABC estimation system was adjusted depending on the species risk index (SRI) that was derived from risk analysis of EBFA. During the process, the SRI-F relationship which generalizes the relationship between SRI and fishing mortality (F) was devised, and was used to estimate an ecosystem-based ABC. Also, the SRI projection as a function of the F scenario was conducted to estimate the regression coefficient of a relationship of SRI and F. -

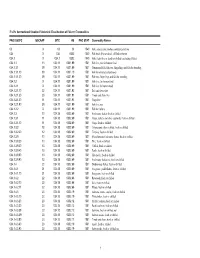

FAO's International Standard Statistical Classification of Fishery Commodities

FAO's International Standard Statistical Classification of Fishery Commodities FAO ISSCFC ISSCAAP SITC HS FAO STAT Commodity Names 03 X 03 03 1540 Fish, crustaceans, molluscs and preparations 034 X 034 0302 1540 Fish fresh (live or dead), chilled or frozen 034.1 X 034.1 0302 1540 Fish, fresh (live or dead) or chilled (excluding fillets) 034.1.1 13 034.11 0301.99 1501 Fish live, not for human food 034.1.1.1 39 034.11 0301.99 1501 Ornamental fish, fish ova, fingerlings and fish for breeding 034.1.1.1.10 39 034.11 0301.10 1501 Fish for ornamental purposes 034.1.1.1.20 39 034.11 0301.99 1501 Fish ova, fingerlings and fish for breeding 034.1.2 X 034.110301.99 1501 Fish live, for human food 034.1.2.1 X 034.110301.99 1501 Fish live for human food 034.1.2.1.10 22 034.11 0301.92 1501 Eels and elvers live 034.1.2.1.20 23 034.11 0301.91 1501 Trouts and chars live 034.1.2.1.30 11 034.11 0301.93 1501 Carps live 034.1.2.1.90 39 034.11 0301.99 1501 Fish live, nei 034.1.2.2 X 034.110301.99 1501 Fish for culture 034.1.3 10 034.18 0302.69 1501 Freshwater fishes, fresh or chilled 034.1.3.1 11 034.18 0302.69 1501 Carps, barbels and other cyprinids, fresh or chilled 034.1.3.1.10 11 034.18 0302.69 1501 Carps, fresh or chilled 034.1.3.2 12 034.18 0302.69 1501 Tilapias and other cichlids, fresh or chilled 034.1.3.2.20 12 034.18 0302.69 1501 Tilapias, fresh or chilled 034.1.3.9 10 034.18 0302.69 1501 Miscellaneous freshwater fishes, fresh or chilled 034.1.3.9.20 13 034.18 0302.69 1501 Pike, fresh or chilled 034.1.3.9.30 13 034.18 0302.69 1501 Catfish, fresh or -

Ocean Leader Co. Ltd. a Premium Seafood Exporter and Processor Key Milestones

Ocean Leader Co. Ltd. A Premium Seafood Exporter and Processor Key Milestones Founded in 1975, Ocean Leader Relocate our business focus on Ocean Leader Co. Ltd. became one of started as a loyal partner with the pacific fishery and became the biggest exporter of Mahi-mahi with multi Tai wanese seafood one of the leading exporter in other expertise in Wahoo, Mackerel, processer helping them selling Tai wan, exporting more than Blue Shark, Sword Fish, Sail Fish, King seafood to US 10,000 tons of fishery annually Fish, Tilapia...etc. 1975 1977 1990 1991-2018 Focused on shrimp business as Tai wan held Awarded ”Taiwan Excellent Exporter” for 30 the leading position in years consecutively global shrimp market Certified by HACCP, SQF, SGS and BRC, Ocean Leader Co. Ltd., demonstrated the pursuit in products sanitation and safety 2 Global Footprint Canada Europe USA Bahama UK Jamaica Dominica Puerto Rico Trinidad Mexico Ecuador 3 Products Overview Mahi Mahi Mackerel FRESH IQF Sword Fish Black Marlin King Fish Wahoo SEAFOOD Blue Shark Sail Fish CERTIFIED Golden Yellowfin Tuna Pompano Pacific Saury Oil Fish Mackerel Pike 4 Mahi Mahi Coryphaena Hippurus Product Specification: • Whole gutted • Fillet • Loin • Portion • Steak *All pictures are for illustration purpose only 5 Blue Shark Priunace Glauca Product Specification: • H+G (Headed & Gutted) • Fillet • Portion • Steak • Cube *All pictures are for illustration purpose only 6 Mackerel Scomber Japonicus Product Specification: • Whole round • Fillet *All pictures are for illustration purpose only 7 -

Tempering Large Tuna Prior to Thawing to Minimize Histamine Formation

PEER-REVIEWED ARTICLE John DeBeer,1* Fred Nolte,2 Food Protection Trends, Vol 41, No. 1, p. 36–45 3 4 Copyright© 2021, International Association for Food Protection Christopher W. Lord and Javier Colley 2900 100th Street, Suite 309, Des Moines, IA 50322-3855 1Retired, 1630 Burgundy Road, Encinitas, CA 92024, USA 2Principal at Fred Nolte Consulting, 2503 West 5th Ave., Vancouver BC, Canada V6K 1S9 3Principal at Pro-Tech International Consultants Co. Ltd., Bangkok, Thailand 4COS Georgia Canning, 129 North Commerce Drive, Lyons, GA 30436, USA Tempering Large Tuna Prior to Thawing to Minimize Histamine Formation ABSTRACT data. At the proposed ambient tempering temperatures The time and temperature controls for processing of −3 to −4°C, there is minimal risk of the growth of canned tuna to control histamine formation were first histamine-forming bacteria and the formation of histamine. published in the 1998 edition of the Fish & Fishery Products Hazards & Controls Guide from the U.S. INTRODUCTION Food and Drug Administration (FDA). The controls have Canned tuna processing is a global business that is been refined since then with validation studies and FDA regulated from catch (35) to can (69), and it provides a warning letters. To control histamine formation, the safe, sustainable high-protein food product for the world. latest precooking validation study allows a 12-h thawing Most tuna for canning is harvested and then frozen rapidly and butchering time limit, a critical limit of a minimum at sea (10). The raw frozen whole fish are delivered to precooking temperature of 60°C at the backbone of the canning factories either directly from the harvesting vessels fish, and a 12-h critical limit from the end of precooking or indirectly via container ships or bulk carriers following until the inhibitory temperatures is reached in the cold transshipment (17, 61). -

2016 Seafood Products Market Brief Korea

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 8/2/2016 GAIN Report Number: KS1624 Korea - Republic of Post: Seoul ATO 2016 Seafood Products Market Brief Report Categories: Fishery Products Approved By: Mark Myers, Acting Ag. Minister-Counselor Prepared By: Sun Young Yoo, Market Promotion Specialist Report Highlights: In 2015, total Korean imports of seafood were $4.24 billion, up 1.9 percent from 2014 due to rising prices. Imports of American seafood increased by 4.9 percent to $233 million, making the United States the fourth largest exporter with a market share of 5.5 percent. U.S. seafood is generally considered high quality and safe, but less price competitive when competing with other origins. By volume, Alaska Pollack Surimi, flatfish, frozen Alaskan Pollack, Cod, Alaskan Pollack roe, Monkfish, ray, Pacific salmon, Hagfish, Atka Mackerel, lobster, etc. are some of the major species imported in large quantities from the United States. By value, Alaskan Pollack Surimi, lobsters, flatfish, live Hagfish, Monkfish, frozen Alaskan Pollack, Cod, Alaskan Pollack roe, skate, and frozen Hagfish were the top ten imported species. Executive Summary: General Information: SECTION I: KOREAN SEAFOOD MARKET OVERVIEW In 2015, Korea’s seafood imports from all origins amounted to $4.24 billion, up 1.9 percent from $4.16 billion in 2014. The United States was the fourth largest exporter of seafood products to Korea. The largest seafood supplying country in 2015 was China at $1.1 billion, followed by Russia at $705 million, Vietnam at $574 million, USA at $233 million, Norway at $218 million, Thailand at $168 million, Japan at $116 million, Taiwan at $102 million, Peru at $99 million and Chile at $97 million.