Bank 2019-Bnk24

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

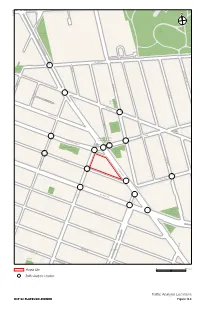

Draft EIS ECF 80 Flatbush Avenue Part 4

WILLOUGHBY STFLEET PL 2/5/2018 FLEET ST Fort Greene University Park Place FLATBUSH AVE EXTENSION DE KALB AVE HUDSON AVE Albee Square SOUTH PORTLAND AVE ASHLAND PL BOND ST SOUTH ELLIOTT PL HANOVER PL GROVE PL 230 Ashland Place POPS FULTON ST LIVINGSTON ST ST FELIX ST ROCKWELL PL Theatre for a New Audience Fowler Square VE TTE A FAYE Rockwell Place Bears LA SCHERMERHORN ST Community Garden Seating Sixteen Sycamores Area 2 Playground 300 Ashland Place Plaza FT GREENE PL STATE ST NEVINS ST FLATBUSH AVE HANSON PL North Pacific Plgd ATLANTIC AVE 3 AVE Atlantic PACIFIC ST Terminal Mall Plaza Barclay's Center DEAN ST Plaza 4 AVE E V A 5 BERGEN ST WYCKOFF ST Greenstreet Wykoff ST MARK'S PL Gardens Open Space Project Site 0 400 FEET Traffic Analysis Location Traffic Analysis Locations ECF 80 FLATBUSH AVENUE Figure 11-4 Chapter 11: Transportation Table 11-8 Traffic Level 2 Screening Analysis Results—Analysis Locations Incremental Vehicle Trips (Weekday) Intersection AM Midday PM Analysis Locations Fulton Street and DeKalb Avenue 0 0 0 Livingston Street and Bond Street 4 1 4 Schermerhorn Street and Bond Street 35 9 23 Flatbush Avenue and DeKalb Avenue 57 14 57 ✓ Flatbush Avenue and Fulton Street 72 19 92 ✓ Flatbush Avenue and Nevins Street 37 9 52 Livingston Street and Nevins Street 30 6 32 Schermerhorn Street and Nevins Street 61 13 51 ✓ State Street and Nevins Street 51 8 49 ✓ Atlantic Avenue and Nevins Street 32 7 36 Pacific Street and Nevins Street 10 0 7 DeKalb Avenue and Hudson Avenue 6 0 1 Hudson Avenue and Fulton Street 35 13 58 Flatbush -

USA | Canada Reference Projects

USA | Canada Reference Projects One Vanderbilt. New York. KPF Architects 1 Tvitec in the USA & Canada | Projects 2020 Contents United States & Canada MIDTOWN CENTER. 4 BROOKFIELD PLACE CALGARY 34 Reference Projects 2020 ONE MANHATTAN WEST 8 ONE SOUTH FIRST 37 VIRGIN HOTEL NEW YORK 12 ROCKEFELLER UNIVERSITY 38 Tvitec System Glass is an international glass manufacturer which after ten years of activity has become the first Spanish architectural glass HUNTER’S POINT 13 SURF CLUB. MIAMI FOUR SEASONS 40 transformer. The company and its 500 employees have developed into the world’s technology an innovation leader for insulating, safety and digital RESTON STATION 14 55 BLOOR. MANULIFE CENTER 41 printed glass. ONE MANHATTAN SQUARE 16 ONE DALTON ST. FOUR SEASONS 42 Tvitec was founded in 2008. Its main manufacturing center is located in Cubillos del Sil - León (Spain). Its organizational structure an investment 2000 ROSS STRET DALLAS 18 CAPITOL ONE. BLOCK C 45 plans are focused on turning Tvitec into one of the world’s largest hi- gh-performance architectural glass manufacturers for projects specia- 160 LEROY STREET 20 NATIONAL AIR MUSEUM . 45 lized in façade and building envelope on a global scale. Tvitec invoiced in 2017 over 100 Million Euros with an important increase in its turnover 2000 K STREET 22 LCBO TOWER. 46 with respect to the pevious year. The major part of these sales were generated in the international market. 50 WEST STREET 24 1441 L STREET 47 The Spanish high-performance glass manufacturer supplies its products CAPITOL CROSSING & OTHERS 26 NORSTROM FLAGSHIP NYC 48 for a large number of singular constructions in the United States and Canada. -

Monthly Accident Details: January - October 2019

Monthly Accident Details: January - October 2019 Incident Date Borough Address Number Street Fatalities Injuries EOC Final Description DOB Action ECB Violation Numbers DOB Violation Numbers Permit Permit No Incident Type Owner's Name Contractor Name 1/2/2019 Bronx 4215 PARK AVENUE 0 1 A DOB inspector reported that a worker in the cellar fell ECB Violation 35367408M 010319CE06WG01 Other Construction Related Incidents NOT ON FILE JOY CONSTRUCTION CORP approximately five feet from a ladder. The worker was sent to a hospital. An ECB Violation was issued for the improper use of a ladder. 1/2/2019 Queens 147-40 ARCHER AVENUE 0 1 The Site Safety Manager reported that an electrician No Dispatch NEW BUILDING 420654508 Other Construction Related Incidents HP JAMSTA HOUSING DEV. FUND CO CNY CONSTRUCTION LLC was preparing to pull wires through a pipe when he stepped backwards on the same floor and lost his balance. The electrician cut his left hand while trying to reach for something to grab to prevent himself from falling. The worker went to an urgent care center on his own to receive treatment. 1/3/2019 Brooklyn 1797 BROADWAY 0 1 A DOB inspector reported that a worker was guiding ECB Violation 35374959Y 010318CNEGS01 NB 32156883 Excavation/Soil Work 1797 REALTY ASSOCIATES W Developers Corp piles into place when a pile shifted and the worker suffered an injury to his right leg. The worker was in stable condition and was taken to an area hospital. The extent and severity of the worker's injuries were not known as of the time of inspection. -

480 Fulton Street Brooklyn, NY

480 Fulton Street Brooklyn, NY Confidential Offering Memorandum Champs Sports Financial summary 480 Fulton Street Brooklyn, NY Asset Summary Asking Price Cap Rate NOI Increases Term Remaining $16,980,220 5.01% $851,511 3% 12 years Investment Highlights Rent/Month $85,779 - Located on a prime retail corridor in Downtown Brooklyn Fulton Mall featuring hundreds of small and national businesses Gross Building SF 8,965 - Credit BB- tenant, subsidiary of Footlocker with long-term lease Rentable SF 6,740 - Proximity to three subway stations servicing all major subway lines First Floor 2,907 sf including 2 3 4 5 B D N Q R W Second Floor 926 sf - Champs is in the center of Citypoint surrounded by retailers such as Macy’s, Target, Express and Chase Bank Cellar Floor 3,067 sf Tenant Footlocker, Inc. Champs Sports Ownership Type Fee Simple Guarantor Parent Lease Commencement February 14, 2017 Rent Commencement June 14, 2017 Lease Expiration January 31, 2033 Avison Young | Confidential Offering Memorandum 2 Champs Sports Rent schedule 480 Fulton Street Brooklyn, NY Term Increases Annual Rent Monthly 7/1/2017 - 6/30/2018 - $942,000 $78,500 7/1/2018 - 6/30/2019 3.00% $970,260 $80,855 7/1/2019 - 6/30/2020 3.00% $999,368 $83,281 7/1/2020 - 6/30/2021 3.00% $1,029,349 $85,779 7/1/2021 - 6/30/2022 3.00% $1,060,229 $88,352 7/1/2022 - 6/30/2023 3.00% $1,092,036 $91,003 7/1/2023 - 6/30/2024 3.00% $1,124,797 $93,733 7/1/2024 - 6/30/2025 3.00% $1,158,541 $96,545 7/1/2025 - 6/30/2026 3.00% $1,193,297 $99,441 7/1/2026 -6/30/2027 3.00% $1,229,096 $102,425 7/1/2027 - 6/30/2028 3.00% $1,265,969 $105,497 7/1/2028 - 6/30/2029 3.00% $1,303,948 $108,662 7/1/2029 - 6/30/2030 3.00% $1,343,067 $111,922 7/1/2030 - 6/30/2031 3.00% $1,383,359 $115,280 7/1/2031 - 6/30/2032 3.00% $1,424,859 $118,738 7/1/2032 - 1/31/2033 3.00% $1,467,605 $122,300 Avison Young | Confidential Offering Memorandum 3 Champs Sports Tenant overview 480 Fulton Street Brooklyn, NY About Champs Sports Foot Locker, Inc. -

Monthly Accident Details: January - August 2018

Monthly Accident Details: January - August 2018 Incident Date Borough Address Number Street Fatalities Injuries EOC Final Description DOB Action ECB Violation Numbers DOB Violation Numbers Permit Permit No Incident Type Owner's Name Contractor Name 1/2/2018 Manhattan 13 EAST 7 STREET 0 1 The New York City Police Department reported that an ECB Violation 35309613X No Permit No Permit Worker Fell TRIAD CAPITAL, LLC No Permit exterminator fell into a six foot deep excavation in the basement. A DOB inspector reported that the worker suffered minor injuries and was taken to Bellevue Hospital and that there was unpermitted excavation work being performed in the basement. An Aggravated Level 2 ECB Violation was issued for a failure to safeguard and work without a permit. A full Stop Work Order was issued. 1/3/2018 Manhattan 269 0 1 The Site Safety Manager reported that a worker was ECB Violation 35285606Y, 35285607X, 35285608H, 35285609J Worker Fell RIVERVIEW OPERATING CO., LLC Leeding Builders Group LLC cleaning a platform from a multipoint scaffold when he slipped and fell five feet onto the ground, hitting his right elbow. An ambulance was on site. Four ECB Violations and a partial Stop Work Order were issued. 1/3/2018 Manhattan 430 EAST 58 STREET 0 1 The Site Safety Manager reported that a worker got his No Dispatch Other Construction Related Incidents SUTTON 58 HOLDING COMPANY LLC hand stuck between a steel plate and a frame and got two of his fingers crushed. The worker was sent to Bellevue Hospital. 1/4/2018 Manhattan 1681 3 AVENUE 0 1 The Site Safety Manager reported that a worker was No Dispatch Other Construction Related Incidents 95TH AND THIRD LLC loading garbage into a truck when he slipped on snow and hurt his arm. -

November 2018

Monthly Accident Details: January - November 2018 Incident Date Borough Address Number Street Fatalities Injuries EOC Final Description DOB Action ECB Violation Numbers DOB Violation Numbers Permit Permit No Incident Type Owner's Name Contractor Name 1/2/2018 Manhattan 13 EAST 7 STREET 0 1 The New York City Police Department reported that an ECB Violation 35309613X No Permit No Permit Worker Fell TRIAD CAPITAL, LLC No Permit exterminator fell into a six foot deep excavation in the basement. A DOB inspector reported that the worker suffered minor injuries and was taken to Bellevue Hospital and that there was unpermitted excavation work being performed in the basement. An Aggravated Level 2 ECB Violation was issued for a failure to safeguard and work without a permit. A full Stop Work Order was issued. 1/3/2018 Manhattan 269 0 1 The Site Safety Manager reported that a worker was ECB Violation 35285606Y, 35285607X, 35285608H, 35285609J Worker Fell RIVERVIEW OPERATING CO., LLC Leeding Builders Group LLC cleaning a platform from a multipoint scaffold when he slipped and fell five feet onto the ground, hitting his right elbow. An ambulance was on site. Four ECB Violations and a partial Stop Work Order were issued. 1/3/2018 Manhattan 430 EAST 58 STREET 0 1 The Site Safety Manager reported that a worker got his No Dispatch Other Construction Related Incidents SUTTON 58 HOLDING COMPANY LLC hand stuck between a steel plate and a frame and got two of his fingers crushed. The worker was sent to Bellevue Hospital. 1/4/2018 Manhattan 1681 3 AVENUE 0 1 The Site Safety Manager reported that a worker was No Dispatch Other Construction Related Incidents 95TH AND THIRD LLC loading garbage into a truck when he slipped on snow and hurt his arm. -

National Real Estate News Therealdeal.Com COLONY’S

SPECIALTHE HAMPTONS SECTION p39 May 2021 National Real Estate News TheRealDeal.com COLONY’S How MARC GANZI NEW bet the CRE giant’s future Will reform +ever come to WORLD New York co-ops? p30 NYC’s biggest general on the next-gen economy p70 contractors p59 The case of the vanishing RE attorney ORDER p74 Wait until you see the pool house. elliman.com © 2021 DOUGLAS ELLIMAN REAL ESTATE. EQUAL HOUSING OPPORTUNITY. 575 MADISON AVENUE, NY, NY 10022. 212.891.7000. Immediate Occupancy Now Available! studios from $695,000 1 bedrooms from $995,000 2 bedrooms from $1,425,000 3 bedrooms from $1,935,000 4 bedrooms from $3,400,000 Visualizations by binyan studios. tHE C oMPlEtE oFFERinG tERMs aRE in an oFFERinG P LAN aVAILABLE FR oM sPONSOR. F ilE no. C d18-0132. residence features More than 55,000 square › Two distinctive residence interior finish palettes — Classic and Heritage feet of unrivaled indoor and › Latch™ smart entry door locks outdoor amenities. › Smart wifi enabled thermostats › 10'-0" ceilings (typical) › Integrated USB outlets in select locations › In-residence washer/dryer Global design, rooted in Brooklyn. › 7" wide plank American White Oak flooring building features › Private driveway, motor court, and porte-cochere Architecture by Studio Gang. › Coffee bar and co-working lounge › Outdoor dog park Interiors by Michaelis Boyd. outdoor and park amenities › Fitness deck Landscape by Hollander Design. › Quiet lawn › Active lawn › Interactive children’s play area › Outdoor lounge › Private dining with barbecues › Sun deck › Hot tub › -

New York Business

ADVERTISING SUPPLEMENT TO CRAIN’S NEW YORK BUSINESS Honors New York City Leaders at Annual Banquet The year 2017 was an eventful one for New York City’s real estate market. Although rents have receded for Manhattan retail properties this year, leasing of commercial property in the borough was on the upswing toward the close of the year. On the residential front, closed sales in Manhattan remained stable from the previous year; and in Brooklyn, prices for townhouses hit a record $1.2 million in the third quarter. At the same time, there were new average price records set in sales of co-ops in Manhattan, Brooklyn and Queens; sales of condos in Queens; and sales of one-to-three family dwellings in Brooklyn, Queens and Staten Island. The Bronx, meanwhile, saw a boom in development. Construction starts for 2017 are A LEGACY OF SUCCESS expected to be greater than $2 billion, making it the third year in a row, according to the New York Building Congress. “The five boroughs are buzzing with excitement,” said John H. Banks, president of the Real Estate Board of New York (REBNY). But there are also ongoing challenges that call for smart public policy. Affordable housing, construction safety, sustainability, taxes and zoning issues are among the biggest issues facing New York City’s real estate community at the moment, said Banks. “New York’s affordable housing crisis can only be addressed by increasing our production of new housing,” said Banks. “It is important to maintain the quality COMMERCIAL | RESIDENTIAL | RETAIL | FINANCE of our existing inventory of affordable housing, but we will need approximately 200,000 additional affordable units if we are to close the gap between the number of households at median income and the number of existing units at rents they can afford.” Read on to learn how REBNY is working to make a difference and for a look at the seven movers and shakers being honored at REBNY’s 122nd Annual Banquet, who are NEW YORK CITY’S LARGEST OWNER OF COMMERCIAL REAL ESTATE shaping the city’s skyline and quality of life. -

Bankruptcy Sale

BANKRUPTCY SALE 13 BUILDING PORTFOLIO Williamsburg | Bushwick | Bed-Stuy | GreenwoodOffering MemorandumHts | 1 Brooklyn, NY INVESTMENT SALES TEAM INVESTMENT SALES TEAM Aaron Jungreis Founder and CEO Direct: 212-359-9901 Cell: 516-852-1342 [email protected] Greg Corbin President, Bankruptcy and Restructuring Direct: 212.359.9904 Cell: 917.406.0406 [email protected] Chaya Milworn Senior Director Direct: 212.359.9936 Cell: 917.804.7458 [email protected] Shaun Rose Director Direct: 212.359.9926 Cell: 917.523.7656 [email protected] Benjamin Sklar Associate Direct: 212.359.9925 Cell: 713.301.1576 [email protected] William Tavoulareas Head Analyst Direct: 212.359.9923 Cell: 561.212.5555 [email protected] Joel Nematzadeh Marketing Manager Direct: 212-359-9903 Cell: 516-884-5632 [email protected] Joshua Rashtian Analyst Direct: 212.359.9907 Cell: 516.606.0392 [email protected] Rosewood Realty Group 38 East 29th Street, 5th Floor New York, NY 10016 4 | 13 Building Portfolio, Brooklyn, NY Offering Memorandum | 5 TABLE OF CONTENTS PORTFOLIO OVERVIEW ....................8 THE PROPERTIES ............................17 Williamsburg Properties ........................... 21 92 South 4th Street .................................. 24 834 Metropolitan Avenue ......................... 28 Williamsburg New Contruction ................ 32 Williamsburg Retail ................................... 38 Bushwick Properties ................................. 40 1125-1133 Greene Avenue ...................... 44 53 Stanhope Street .................................. -

New York Times

ADVERTISEMENT ADVERTISEMENT THE REAL ESTATE BOARD OF NEW YORK This special advertising feature is sponsored by participating advertisers. The material was written by Ron Derven and did not involve the reporting or editing staff of The New York Times. © 2018 The New York Times ADVERTISEMENT ADVERTISEMENT NEW YORK CITY’S COMMERCIAL REAL ESTATE MARKET As the New York real estate industry gathers for the Real Estate Board of New York’s (Rebny) 122nd Annual Banquet, the industry is hopeful that the vibrant economy experienced throughout the city and region in recent years will continue in 2018 and attract new jobs, residents and high numbers of tourists to the city. Rebny is pleased with its accomplishments at both the city and Housing Program (ANYHP), formerly known as 421a. The program state level over the past year. For example, Rebny was heartened provides fair wages for construction workers while producing sub- by the final passage of Midtown East rezoning, according to John stantially more affordable rental housing. H. Banks III, president of Rebny. “It will mean new private sector investment in modern offices, mass transit and new and enhanced public spaces. The rezoning will be a crucial tool for ensuring that Economic Incentives Program Extension East Midtown remains one of the world’s leading office districts.” The Greater East Midtown rezoning was enacted in August 2017, Equally important is making New York an affordable place for busi- establishing a plan to revitalize the district by increasing allowable nesses to function and grow. “The governor and state legislature floor area for the development of new office buildings. -

Above Standard Commissions and Incentives October 2019

Above Standard Commissions and Incentives October 2019 Developments with Rent-to-Own Programs 100 Barclay One Manhattan Square (252 South Street) Upper West Side / Upper East Side 207 West 79th Street – 4% 200 East 62nd Street – 4% 301 East 61st Street – Two years of common charges paid by sponsor 389 E 89 – $5,000 Saks Fifth Avenue Gift Card and VIP Personal Shopper on all contracts signed by December 31; three years of free common charges on all one bedroom contracts signed by December 31 Citizen360 (360 East 89th Street) – 4% and sedan parking space included with four bedroom purchase The Hayworth (1289 Lexington Avenue) – 4% One West End – 4% The Park Loggia (15 West 61st Street) – 4% Waterline Square (10 Riverside Boulevard, 30 Riverside Boulevard, 635 West 59th Street) – 4% Midtown 50 United Nations Plaza – 4%; sponsor funded carrying cost subsidy until June 2022 30E31 – 4% with 50% commission paid upon contract signing, sponsor to pay mansion and transfer taxes for all contracts signed 53W53 – 1% advanced commission paid upon contract signing 100 East 53rd Street – 3.5% The Bryant (16 West 40th Street) – 4% for all contracts signed through October 31 Charlie West (505 West 43rd Street) – 4%; sponsor paid city and state transfer taxes Fifty Third and Eight – 4% until October 31 One United Nations Park (695 First Avenue) – 4% on contracts signed by December 31 Manhattan View (460 West 42nd Street) – 4% until November 30 The Revere (400 East 54th Street) – Purchaser can choose between three year common charge -

6 Crucial Ways New York City's Landscape Will Change in 2019

6 crucial ways New York City’s landscape will change in 2019 What to expect from New York’s transit, parks, megaprojects and more in the coming year January 2, 2019 | By ZOE ROSENBERG 2018 was one heck of a year for New York: The beloved Riegelmann Boardwalk at Coney Island became a landmark, a wave of progressive politicians refocused the conversation around issues like housing and inequality, 520 Park Avenue unseated its neighbor at No. 432 to claim the city’s top residential sales, and—even though the news often felt crushing— good things did indeed happen in New York. Now, with 2018 in our collective rear view, it’s time look at what 2019 will bring. Rent stabilization will take center stage in June when the city’s laws are up for renewal, megaprojects throughout the five boroughs will make giant strides, the city’s new tallest residential tower will top out at 1,550 feet, and so much more. Megaprojects The construction of Amazon’s HQ2 in Long Island City will be a development a decade in the making. While local pols like the city comptroller and a handful of City Council members are still decrying the deal, it’s too soon to tell what will physically happen at the site this year. (Reps for Amazon and the New York City Economic Development Corporation were none too quick to share specifics.) Here’s what we do know what the year ahead holds for the manmade inlet of Anable Basin that will hold HQ2: A 14-month planning process will kick off in January, with members of the 45-person Community Advisory Committee holding four meetings throughout the year.