GAO-20-21, Black Lung Benefits Program: Improved Oversight of Coal Mine Operator Insurance Is Needed

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hot Topics in Coal Company Bankruptcies

Hot Topics in Coal Company Bankruptcies David M. Hillman, Karen S. Park and Lucy F. Kweskin Table of Contents Hot Topics in Coal Company Bankruptcies Legacy Obligations: Union and Retiree Benefits and Obligations Under the Coal Act and Black Lung Act 2 Reclamation Obligations 9 Conclusion 12 Endnotes 13 About SRZ 17 The recent “fracking revolution” has allowed U.S. energy companies to tap into abundant supplies of shale gas.1 Previously thought inaccessible, this form of natural gas has been found throughout the United States in deep underground shale formations.2 The shale gas boom has created a spike in natural gas supplies, causing prices to decline to their lowest level since 1999,3 and this has been cause for concern for coal-based energy producers, as well as their suppliers, as declining natural gas prices have made competing gas-fired plants far more cost- effective alternatives to coal-burning plants.4 Indeed, coal-based electricity Resources LP (2009) and Consol- generation in the United States idated Energy (2007) provide has dipped from half to about only evidence of the rapidly deteriorating one-third since 2007, and profits market for U.S. coal companies. from the nation’s coal-fired power In addition, a 2013 Fitch Ratings plants selling electricity in the report identified several coal mining open market have plummeted from companies as “distressed” and $20 billion in 2008 to $4 billion “near distressed” given their bond in 2011.5 Consequently, plans for spreads over U.S. Treasuries. Fitch more than 150 new coal-fired Ratings -

BLBA BULLETIN NO. 16-01 Issue Date

US. DEPARTMENT' OF LABOR Office ofW~rs· Compensation Programs Division of Coal Mine Worl<ers' Compensation Washington, DC 20210 BLBA BULLETIN NO. 16-01 Issue Date: November 12, 2015 Expiration Date: Indefinite Subject: Patriot Coal Corporation Bankruptcy. Background: On May 12, 2015, Patriot Coal Corporation and its subsidiaries filed for bankruptcy protection under Chapter 11. On October 9, 2015, Patriot received approval from the Bankruptcy Court to complete the sale of all its coal-mining operations. Patriot sold those operations to Blackhawk Mining and ERP Compliant Fuel, LLC (an affiliate of the Virginia Conservation Legacy Fund). Neither Blackhawk nor ERP is liable for federal black lung liabilities, except for those miners who continue to work for these companies after the sale. Patriot was authorized to self-insure its federal black lung liabilities as well as the liabilities of its subsidiaries in the States of KY, WV, n.,, IN, MO and PA. Some of Patriot's liabilities, however, are covered by commercial insurance policies. The Division of Coal Mine Workers' Compensation (DCMWC) has been notified that Patriot will no longer administer, defend, or pay claims after October 31, 2015. Applicability: Appropriate DCMWC Personnel Purpose: To provide guidance for district office staff in adjudicating claims in which the miner's last coal mine employment of at least one year was with one of the 50 subsidiary companies that have been affected by the Patriot Coal Corporation bankruptcy. Action: 1. Ensure no interruption of benefits for claims currently in approved/accepted status. For claims in approved/accepted status, claims examiners (CEs) will immediately place these claims into the Federal Black Lung Disability Trust Fund (BLDTF) by completing a Form CM-1261. -

As Filed with the Securities and Exchange Commission on May 5

As filed with the Securities and Exchange Commission on May 5, 2020 UNITED STATES OF AMERICA BEFORE THE SECURITIES AND EXCHANGE COMMISSION FIRST AMENDED AND RESTATED APPLICATION FOR AN ORDER PURSUANT TO SECTION 3(b)(2) OF THE INVESTMENT COMPANY ACT OF 1940, AS AMENDED, DECLARING THAT ARCH COAL, INC. IS PRIMARILY ENGAGED IN A BUSINESS OTHER THAN THAT OF INVESTING, REINVESTING, OWNING, HOLDING, OR TRADING IN SECURITIES In the Matter of ARCH COAL, INC. File No. 812-15085 Please send all communications to: Robert G. Jones, Esq. Arch Coal, Inc. One CityPlace Drive, Suite 300 St. Louis, Missouri 63141 (314) 994-2700 Nabil Sabki, Esq. Latham & Watkins LLP 330 North Wabash Avenue, Suite 2800 Chicago, Illinois 60611 (312) 876-7700 This Application (including Exhibits) consists of 22 pages. 1 UNITED STATES OF AMERICA BEFORE THE SECURITIES AND EXCHANGE COMMISSION In the Matter of FIRST AMENDED AND RESTATED APPLICATION FOR AN ORDER PURSUANT TO SECTION 3(b)(2) OF THE INVESTMENT ARCH COAL, INC. COMPANY ACT OF 1940, AS AMENDED, DECLARING THAT One CityPlace Drive, Suite 300 ARCH COAL, INC. IS PRIMARILY ENGAGED IN A BUSINESS St. Louis, Missouri 63141 OTHER THAN THAT OF INVESTING, REINVESTING, OWNING, HOLDING, OR TRADING IN SECURITIES. File No. 812-15085 I. SUMMARY OF RELIEF REQUESTED Arch Coal, Inc. (“Arch Coal” or the “Company”),1 a Delaware corporation listed on the New York Stock Exchange (NYSE: ARCH) with its principal executive office in St. Louis, Missouri, is one of the world’s largest coal producers. Arch Coal hereby files this amended and restated application (this “Application”) and applies for an order (the “Requested Order”) of the U.S. -

Coal Mining Assignment

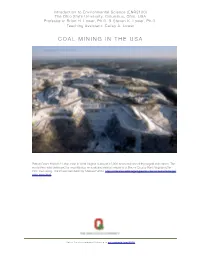

Introduction to Environmental Science (ENR2100) The Ohio State University, Columbus, Ohio, USA Professors: Brian H. Lower, Ph.D. & Steven K. Lower, Ph.D. Teaching Assistant: Cailey A. Lower COAL MINING IN THE USA Patriot Coal’s Horbet-21 strip mine in West Virginia is almost 12,000 acres and one of the largest strip mines. The ecosystem was destroyed by mountaintop removal and nearby residents of Boone County West Virginia suffer from the mining. The image was taken by Melissa Farlow. http://science.nationalgeographic.com/science/enlarge/ strip-mine.html ! Intro Environmental Science • go.osu.edu/enr2100 Coal Mining in the USA Coal-fired power plants generate approximately 30% of the electricity in the United States. Each year about 900-million tons of coal is mined in the USA, or almost 6,000 pounds for each U.S. citi- zen. Most of this coal is mined from Wyoming, West Virginia, and Kentucky. The mining process can pollute freshwater resources and destroy natural ecosystems. One type of mining that is par- ticularly destructive is called mountaintop removal (MTR). This is the process of extracting coal seams from a mountain using explosives to remove the summit of the mountain. The excess rock and debris is discarded in the valleys because it is less expensive than removing it completely from the area. MTR predominantly appears in West Virginia, Kentucky and Tennessee. The explo- sives destroy the vegetation on the mountain and by filling the valleys with the debris, wildlife and valley streams are destroyed. Nearby people and organisms suffer from pollution in the air and water (e.g., heavy metals, acid mine drainage). -

Mountaintop Removal Mining Companies Banks Should Avoid

Mountaintop Removal Mining Companies Banks Should Avoid Alpha Natural Resources LLC Alpha Natural Resources is the third-largest coal producer in the U.S., with production capacity of nearly 126 million tons. Alpha has approximately 150 active mines and 40 coal preparation plants located throughout Virginia, West Virginia, Kentucky, Pennsylvania and Wyoming. Alpha, with the takeover of Massey Energy, is now the single largest mountaintop removal company in the country, responsible for 22 percent of coal production from MTR mines. RepRisk named Alpha “The Most Controversial Mining Company of 2011,” identifying over 1000 citations from the U.S. Mining Safety and Health Administration since the infamous explosion at the Upper Big Branch coal mine that resulted in at least 25 miner fatalities. Alpha, Massey and its sunsidiary, Rawl Sales & Processing, were acused of contaminating drinking water supplies with coal slurry. More than 600 plaintiffs launched around 350 lawsuits. The companies have paid out in excess of $35 million in settlement fees. Patriot Coal Corporation Patriot Coal Corporation is based in St. Louis, Missouri. The company is a 2007 spin-off of most of the Eastern United States operations of Peabody Energy. Patriot has 14 mining complexes in Appalachia and the Illinois Basin, and it is responsible for eight percent of MTR coal mined in Appalachia. In 2010, 8.26 million of the 24.1 million tons of coal Patriot mined was from strip mining in Appalachia and the southern border of Illinois, the western border of Indiana, and the western tip of Kentucky. The company has approximately 1.9 billion tons of proven and probable coal reserves. -

12-12900-Scc Doc 4 Filed 07/09/12 Entered 07/09/12 20:56:15 Main Document Pg 1 of 122

12-12900-scc Doc 4 Filed 07/09/12 Entered 07/09/12 20:56:15 Main Document Pg 1 of 122 DAVIS POLK & WARDWELL LLP 450 Lexington Avenue New York, New York 10017 Telephone: (212) 450-4000 Facsimile: (212) 607-7983 Marshall S. Huebner Damian S. Schaible Brian M. Resnick Michelle M. McGreal Proposed Counsel to the Debtors and Debtors in Possession UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF NEW YORK In re: Chapter 11 PATRIOT COAL CORPORATION, et al., Case No. 12-[ ] (___) (Jointly Administered) Debtors. DECLARATION OF MARK N. SCHROEDER PURSUANT TO LOCAL BANKRUPTCY RULE 1007-2 Mark N. Schroeder declares and says: 1. I am the Senior Vice President and Chief Financial Officer of Patriot Coal Corporation (“Patriot Coal”). I have been employed in this position by Patriot Coal since Patriot Coal’s creation in October 2007. Prior to that, I held several management positions with Patriot Coal’s former parent company, Peabody Energy Corporation (“Peabody”), including President of Peabody China, LLC and Vice President of Materials Management, Vice President of Business Development and Vice President and Controller of Peabody. I am familiar with the day-to-day operations, business, and financial affairs of the Debtors (as defined below). 12-12900-scc Doc 4 Filed 07/09/12 Entered 07/09/12 20:56:15 Main Document Pg 2 of 122 2. I submit this declaration (i) in support of the petitions of the Debtors for relief under chapter 11 of title 11 of the United States Code (the “Bankruptcy Code”), (ii) pursuant to Local Bankruptcy Rule 1007-2 in support of the Debtors’ petitions and contemporaneously-filed requests for relief in the form of motions and applications (the “First Day Motions”), and (iii) to assist the Court and other interested parties in understanding the circumstances giving rise to the commencement of these chapter 11 cases. -

Consent Decree: United States Of

IN THE UNITED STATES DISTRICT COURT FOR THE SOUTHERN DISTRICT OF WEST VIRGINIA CHARLESTON DIVISION ________________________________________________ UNITED STATES OF AMERICA and the ) STATE OF WEST VIRGINIA by and through the ) WEST VIRGINIA DEPARTMENT OF ) ENVIRONMENTAL PROTECTION, ) ) Plaintiffs, ) ) v. ) )C ONSENTDECR EE PATRIOT COAL CORP.; MAGNUM COAL CO.; ) APOGEE COAL CO., LLC; CATENARY COAL CO., ) LLC; COYOTE COAL CO. LLC; DAKOTA LLC; ) HOBET MINING, LLC; JUPITER HOLDINGS LLC; ) LITTLE CREEK LLC; MIDLAND TRAIL ENERGY LLC;) PANTHER LLC; REMINGTON LLC; WILDCAT, LLC; ) BLACK STALLION COAL CO., LLC; BLACK ) WALNUT COAL CO.; COLONY BAY COAL CO.; ) EASTERN ASSOCIATED COAL, LLC; HILLSIDE ) MINING CO.; JARRELL’S BRANCH COAL CO.; ) KANAWHA EAGLE COAL, LLC; LOGAN FORK ) COAL CO.; MARTINKA COAL CO., LLC; MOUNTAIN ) VIEW COAL CO., LLC; PINE RIDGE COAL CO., LLC; ) RIVERS EDGE MINING, INC.; and WINIFREDE ) DOCKLLC, ) ) Defendants. ) ________________________________________________ ) TABLE OF CONTENTS I. BACKGROUND . 1 II. JURISDICTION AND VENUE . 3 III. APPLICABILITY .. 3 IV. DEFINITIONS . 4 V. CIVIL PENALTY . 8 VI. COMPLIANCE REQUIREMENTS . 9 VII. INJUNCTIVE RELIEF . 12 VIII. ADDITIONAL INJUNCTIVE RELIEF . 28 IX. REPORTING REQUIREMENTS . 29 X. STIPULATED PENALTIES . 32 XI. FORCE MAJEURE . 35 XII. DISPUTE RESOLUTION . 37 XIII. INFORMATION COLLECTION AND RETENTION . 40 XIV. EFFECT OF SETTLEMENT/RESERVATION OF RIGHTS . 42 XV. COSTS . 44 XVI. NOTICES . 44 XVII. EFFECTIVE DATE . 46 XVIII. RETENTION OF JURISDICTION. 46 XIX. MODIFICATION . 46 XX. TERMINATION -

National Mine Rescue, First Aid Bench and Preshift Competition 2017

Index Welcome from the President of Holmes Mine Rescue Association ..........................................1 Acitivities Schedule...................................................................................................................3 2015 Champions ......................................................................................................................5 In Memory.................................................................................................................................9 Contest History .......................................................................................................................13 Exhibitor Displays ...................................................................................................................28 Major Awards and Donors ......................................................................................................29 State Awards ..........................................................................................................................33 Combination Teams ................................................................................................................35 Mine Rescue Teams ...............................................................................................................40 First Aid Teams .......................................................................................................................50 Bench - BG-4 Participants ......................................................................................................54 -

Macey & Salovaara

Stanford Law Review Volume 71 April 2019 ARTICLE Bankruptcy as Bailout: Coal Company Insolvency and the Erosion of Federal Law Joshua Macey & Jackson Salovaara* Abstract. Almost half of all the coal produced in the United States is mined by companies that have recently gone bankrupt. This Article explains how those bankruptcy proceedings have undermined federal environmental and labor laws. In particular, coal companies have used the Bankruptcy Code to evade congressionally imposed liabilities requiring that they pay lifetime health benefits to coal miners and restore land degraded by surface mining. Using financial information reported in filings to the Securities and Exchange Commission and in the companies’ reorganization agreements, we show that between 2012 and 2017, four of the largest coal companies in the United States succeeded in shedding almost $5.2 billion of environmental and retiree liabilities. Most of these liabilities were backed by federal mandates. Coal companies disposed of these regulatory obligations by placing them in underfunded subsidiaries that they later spun off. When the underfunded successor companies liquidated, the coal companies managed to get rid of their regulatory obligations without defaulting on the pecuniary debts they owed to their creditors. * Joshua C. Macey is Postdoctoral Associate, Cornell Law School. Jackson Salovaara works in the renewable energy industry. During the editorial process for this Article, Mr. Salovaara was employed by McKinsey & Company, a global consulting firm. McKinsey offers consulting services to coal companies, including on restructuring matters. Mr. Salovaara did not advise any coal companies while employed at McKinsey, nor did he have access to nonpublic information on any coal company. -

Mountain Top Removal Coal Mining United States

Mountain top removal coal mining United States Sectors: Coal Mining On record This profile is no longer actively maintained, with the information now possibly out of date Send feedback on this profile By: BankTrack Created before Nov 2016 Last update: Nov 30 2015 Project website Sectors Coal Mining Location About Mountain top removal coal mining Mountain top removal (MTR) mining is a form of strip mining in which coal companies use explosives to blast as much as 800 to 1,000 feet off the tops of mountains order to reach the coal seams that lie underneath. The resulting millions of tons of waste rock, dirt, and vegetation are then dumped into surrounding valleys, burying miles and miles of streams under piles of rubble hundreds of feet deep. Mountaintop removal mining harms not only aquatic ecosystem, and water quality, it also destroys hundreds of acres of healthy forests and fish and wildlife habitat, including habitat of threatened and endangered species, when the tops of mountains are blasted away. Throughout the Appalachian region of the Eastern United States, more than 500 mountains have been flattened, first by clear-cutting forests, then by blowing off the top layers of rock with powerful explosives. Giant cranes (draglines) expose buried coal by scraping billions of tons of dirt off the mountain. The debris is then dumped into neighboring valleys and streams. Rather than remove coal from the mountain, MTR removes the mountain from the coal. Latest developments Former Massey Energy executive found guilty of conspiracy Dec 3 2015 Patriot fasing out of coal, but Alpha and Arch not May 6 2014 What must happen We urge all private banks involved in commercial lending and investment banking services for the mining sector to end their relationships with companies who practice mountaintop removal coal mining in Appalachia. -

PEABODY ENERGY CORPORATION (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 _____________________________________________ FORM 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal Year Ended December 31, 2017 or TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Commission File Number 1-16463 ____________________________________________ PEABODY ENERGY CORPORATION (Exact name of registrant as specified in its charter) Delaware 13-4004153 (State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification No.) 701 Market Street, St. Louis, Missouri 63101 (Address of principal executive offices) (Zip Code) (314) 342-3400 Registrant’s telephone number, including area code Securities Registered Pursuant to Section 12(b) of the Act: Title of Each Class Name of Each Exchange on Which Registered Common Stock, par value $0.01 per share New York Stock Exchange Securities Registered Pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes No Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes No Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. -

USA Leveling Mountains, Demolishing Communities

IV. The “Hot Spots” USA Leveling Mountains, Demolishing Communities The United States has by far the world’s largest coal reserves, and is the sec- ond biggest coal producer after China. But, with 935 million tons produced 2012, U.S. coal production has fallen more than 10% from its 2008 peak, as strength- ened federal regulations on emissions, nationwide campaigns to shut down coal plants and falling natural gas prices have taken their toll on the industry. Five companies are responsible for 58% of U.S. coal production: Peabody Energy, Arch Coal, Alpha Natural Resources, Cloud Peak Energy and CONSOL Energy. Over 90% of US coal is consumed domestically. However, as domestic consumption falls, exports are growing rapidly, particularly to the EU. 147 U.S. coal production is witnessing a shift from underground to surface mining and an attendant shift from East to West. Production from underground mines has remained roughly constant since 1949 (and is lower today than in underground mining’s heyday in the 1920s). However, the amount of coal produced by surface mines has exploded, rising more than six-fold in the same period. This shift has been primarily driven by technological developments that make it Toxic coal feasible to mine the large, deep coal seams of the Powder River Basin. Ironically, it has also been caused in no small part by the passage of air pollution regula- slurry waste tions. 148 Western coal, on average, contains significantly less sulphur than Appala- chian coal. The restrictions placed on sulphur emissions under the Clean Air Act ponds have therefore contributed to a general shift towards large Western surface mines.