Cathay Opens Doors to Opportunity

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Retail Banking Announcement

Frequently asked questions 26 May 2021 What the repositioning of the HSBC USA Wealth and Personal Banking business means for our customers, here and abroad Why did HSBC take this action? In February 2020, we set out a plan to shift our business strategy in the United States to maximize the connection between our clients and our world-class international network. Our primary business will be a wholesale bank focused on the international needs of clients. We are renewing our emphasis on the US$5 trillion international wealth management opportunity from globally mobile and affluent individuals in the United States. Is HSBC exiting the United States? No, HSBC is not exiting its US business. We aim to be the leading international bank in the United States and are focused on what we do best – connecting Americans to a world of opportunity and bringing cross-border business and investment to the United States. We will continue to provide banking services not only to our wholesale banking clients, but also to our Premier, Jade and Private Banking customers. I have personal accounts at HSBC and I’m in the United States. How will these agreements affect me? Upon completion of the transactions, the accounts of in-scope customers will be transferred to Citizens or Cathay Bank. We thank those customers for their business and will ensure the transfer occurs with as minimum disruption as possible. Premier, Jade, Private Banking and other clients who will remain HSBC customers are in the process of being transitioned to one of our new 20-25 Wealth Centers. -

Pft Pittsburgh Picks! Aft Convention 2018

Pittsburgh Federation of Teachers PFT PITTSBURGH PICKS! AFT CONVENTION 2018 Welcome to Pittsburgh! The “Front Door” you see above is just a glimpse of what awaits you in the Steel City during our national convention! Here are some of our members’ absolute favorites – from restaurants and tours, to the best views, shopping, sights, and places to see, and be seen! Sightseeing, Tours & Seeing The City Double Decker Bus Just Ducky Tours Online booking only Land and Water Tour of the ‘Burgh Neighborhood and City Points of Interest Tours 125 W. Station Square Drive (15219) Taste of Pittsburgh Tours Gateway Clipper Tours Online booking only Tour the Beautiful Three Rivers Walking & Tasting Tours of City Neighborhoods 350 W. Station Square Drive (15219) Pittsburgh Party Pedaler Rivers of Steel Pedal Pittsburgh – Drink and Don’t Drive! Classic Boat Tour 2524 Penn Avenue (15222) Rivers of Steel Dock (15212) City Brew Tours Beer Lovers: Drink and Don’t Drive! 112 Washington Place (15219) Culture, Museums, and Theatres Andy Warhol Museum Pittsburgh Zoo 117 Sandusky Street (15212) 7370 Baker Street (15206) Mattress Factory The Frick Museum 500 Sampsonia Way (15212) 7227 Reynolds Street (15208) Randyland Fallingwater 1501 Arch Street (15212) Mill Run, PA (15464) National Aviary Flight 93 National Memorial 700 Arch Street (15212) 6424 Lincoln Highway (15563) Phipps Conservatory Pgh CLO (Civic Light Opera) 1 Schenley Drive (15213) 719 Liberty Avenue 6th Fl (15222) Carnegie Museum Arcade Comedy Theater 4400 Forbes Avenue (15213) 943 Penn Avenue (15222) -

Cathay General Bancorp Contact: Heng W

FOR IMMEDIATE RELEASE For: Cathay General Bancorp Contact: Heng W. Chen 777 N. Broadway (626) 279-3652 Los Angeles, CA 90012 CATHAY GENERAL BANCORP AND ASIA BANCSHARES INC. COMPLETE MERGER LOS ANGELES – August 3, 2015 – Cathay General Bancorp (NASDAQ: CATY), the holding company for Cathay Bank, announced today that it completed its merger with Asia Bancshares, Inc. at the end of the day on July 31, 2015. As a result of the transaction, Asia Bancshares, Inc. has been merged with and into Cathay General Bancorp, and Asia Bank has been merged with and into Cathay Bank. The completion of the merger results in a combined financial institution with total assets of approximately $12.4 billion and deposits of approximately $9.8 billion, 57 branches operating in nine states, and a presence in three overseas locations. Under the terms of the merger, Cathay General Bancorp is issuing 2.58 million shares of its common stock and paying $57.0 million in cash for all of the issued and outstanding shares of Asia Bancshares stock, valuing the merger at approximately $139.9 million, based on Cathay General Bancorp’s closing price on July 31, 2015. Based on properly and timely submitted and accepted elections, the stock consideration of 3.2134 shares of Cathay common stock per share of Asia Bancshares was over-subscribed by Asia Bancshares shareholders and subject to proration. As a result, approximately 36% of the shares of Asia Bancshares that were subject to stock elections will receive cash consideration of $86.76 per share of Asia Bancshares. Asia Bancshares shareholders who elected cash and those shareholders who failed to submit elections on a timely basis will receive cash consideration of $86.76 per share of Asia Bancshares. -

3A Expanded Small Business Lending

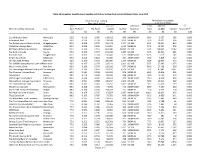

Table 3A Expanded. Small Business Lending Institutions in New York Using Call Report Data, June 2012 Small Business Lending Micro Business Lending (less than $ million) (less than $ 100k) Total Amount Institution Total Amount CC Name of Lending Institution City Rank TA Ratio1 TBL Ratio1 (1,000) Number Asset Size Rank (1,000) Number Amount/TA1 (1) (2) (3) (4) (5) (6) (7) (8) (9) (10) Catskill Hudson Bank Monticello 92.5 0.419 1.000 148,102 686 100M-500M 80.0 8,557 289 0.000 Adirondack Bank Utica 90.0 0.220 0.704 128,588 1,029 500M-1B 95.0 19,322 594 0.000 The Bridgehampton National Bank Bridgehampton 87.5 0.169 0.570 236,278 1,377 1B-10B 92.5 35,912 864 0.000 Watertown Savings Bank Watertown 85.0 0.208 0.690 105,854 1,012 500M-1B 87.5 14,901 596 0.000 NBT Bank, National Association Norwich 85.0 0.139 0.512 823,680 10,927 1B-10B 92.5 128,045 7,142 0.000 The Bank of Castile Castile 85.0 0.150 0.574 151,215 1,385 1B-10B 92.5 23,521 821 0.000 Riverside Bank Poughkeepsie 85.0 0.495 0.704 100,441 627 100M-500M 82.5 7,279 282 0.000 Empire State Bank Newburgh 85.0 0.414 0.864 66,385 431 100M-500M 70.0 3,038 237 0.000 Shinhan Bank America New York 82.5 0.197 0.307 189,889 1,175 500M-1B 82.5 18,025 494 0.001 The Suffolk County National Bank of RRiverhead 82.5 0.137 0.379 213,111 2,161 1B-10B 87.5 27,695 1,375 0.000 Woori America Bank New York 82.5 0.199 0.379 195,042 977 500M-1B 80.0 17,498 390 0.004 The Canandaigua National Bank and TCanandaigua 82.5 0.143 0.418 259,182 4,294 1B-10B 92.5 47,842 3,347 0.000 The Mahopac National Bank Brewster 82.5 -

The Chinese in Hawaii: an Annotated Bibliography

The Chinese in Hawaii AN ANNOTATED BIBLIOGRAPHY by NANCY FOON YOUNG Social Science Research Institute University of Hawaii Hawaii Series No. 4 THE CHINESE IN HAWAII HAWAII SERIES No. 4 Other publications in the HAWAII SERIES No. 1 The Japanese in Hawaii: 1868-1967 A Bibliography of the First Hundred Years by Mitsugu Matsuda [out of print] No. 2 The Koreans in Hawaii An Annotated Bibliography by Arthur L. Gardner No. 3 Culture and Behavior in Hawaii An Annotated Bibliography by Judith Rubano No. 5 The Japanese in Hawaii by Mitsugu Matsuda A Bibliography of Japanese Americans, revised by Dennis M. O g a w a with Jerry Y. Fujioka [forthcoming] T H E CHINESE IN HAWAII An Annotated Bibliography by N A N C Y F O O N Y O U N G supported by the HAWAII CHINESE HISTORY CENTER Social Science Research Institute • University of Hawaii • Honolulu • Hawaii Cover design by Bruce T. Erickson Kuan Yin Temple, 170 N. Vineyard Boulevard, Honolulu Distributed by: The University Press of Hawaii 535 Ward Avenue Honolulu, Hawaii 96814 International Standard Book Number: 0-8248-0265-9 Library of Congress Catalog Card Number: 73-620231 Social Science Research Institute University of Hawaii, Honolulu, Hawaii 96822 Copyright 1973 by the Social Science Research Institute All rights reserved. Published 1973 Printed in the United States of America TABLE OF CONTENTS FOREWORD vii PREFACE ix ACKNOWLEDGMENTS xi ABBREVIATIONS xii ANNOTATED BIBLIOGRAPHY 1 GLOSSARY 135 INDEX 139 v FOREWORD Hawaiians of Chinese ancestry have made and are continuing to make a rich contribution to every aspect of life in the islands. -

FY 19 4Th Quarter & FYE Lender Ranking

LOS ANGELES DISTRICT OFFICE 7(a) and 504 Lender Ranking Report Fiscal Year 2019 - Q4 (10/1/18 - 9/30/19) 7(a) Loan Program 504 Loan Program 1 U.S. Bank, National Association 184 $23,757,600 67 Mega Bank 5 $1,672,000 1 CDC Small Business Finance Corporation* 94 $98,783,000 2 JPMorgan Chase Bank, National Association 174 $44,541,500 68 PCR Small Business Development*++ 5 $821,000 2 Business Finance Capital*++ 92 $109,382,000 3 Bank of Hope++ 167 $60,333,000 69 Poppy Bank 4 $8,690,000 3 California Statewide Certified Development* 84 $67,087,000 4 Wells Fargo Bank, National Association 155 $36,193,900 70 Wallis Bank 4 $7,542,000 4 Mortgage Capital Development Corporation 38 $39,865,000 5 First Home Bank 104 $22,494,000 71 BBVA USA 4 $5,926,300 5 Advantage Certified Development Corporation 15 $17,387,000 6 East West Bank++ 61 $33,406,500 72 Pacific Mercantile Bank 4 $4,927,000 6 Southland Economic Development Corporation 14 $14,297,000 7 Pacific City Bank++ 60 $50,311,500 73 Pacific Western Bank++ 4 $4,165,000 7 So Cal CDC++ 11 $22,780,000 8 CDC Small Business Finance Corporation* 55 $8,763,500 74 OneWest Bank, A Division of 4 $4,013,000 8 AMPAC Tri-State CDC, Inc. 10 $7,235,000 9 MUFG Union Bank, National Association 50 $75,482,600 75 IncredibleBank 4 $2,123,600 9 Coastal Business Finance++ 6 $3,666,000 10 Hanmi Bank++ 50 $30,864,000 76 Kinecta FCU++ 4 $862,000 10 Enterprise Funding Corporation 2 $2,980,000 11 Commonwealth Business Bank++ 47 $38,305,000 77 Montecito Bank & Trust++ 4 $503,900 11 San Fernando Valley Small Business Development++ 2 $1,046,000 12 Celtic Bank Corporation 44 $14,667,300 78 Meadows Bank 3 $5,091,000 12 Superior California Economic Development 1 $2,111,000 13 Independence Bank 40 $5,725,000 79 Banner Bank 3 $2,175,000 13 Capital Access Group, Inc. -

Minority Banks in New York City: Is the Community Reinvestment Act Relevant?

Journal of Civil Rights and Economic Development Volume 25 Issue 3 Volume 25, Spring 2011, Issue 3 Article 4 Minority Banks in New York City: Is the Community Reinvestment Act Relevant? Tarry Hum Follow this and additional works at: https://scholarship.law.stjohns.edu/jcred This Article is brought to you for free and open access by the Journals at St. John's Law Scholarship Repository. It has been accepted for inclusion in Journal of Civil Rights and Economic Development by an authorized editor of St. John's Law Scholarship Repository. For more information, please contact [email protected]. MINORITY BANKS IN NEW YORK CITY: IS THE COMMUNITY REINVESTMENT ACT RELEVANT? TARRY HUM, PH.D.* INTRODUCTION The United States has a long history of minority banks formed to meet the credit needs of populations excluded from mainstream financial institutions. Minority banks continue to be a prominent part of locally- based economic landscapes, but their record in individual asset building (e.g., homeownership) and community economic development is uneven at best. A recent example is Massachusetts-based OneUnited Bank, established by African Americans to underwrite the revitalization of urban poor neighborhoods. A long time advocate of minority banks, Congresswoman Maxine Waters is now a focus of a Congressional ethics committee inquiry on charges that she used her influence to arrange a meeting between OneUnited Bank representatives and US Treasury Department officials. While the media has covered extensively Congresswoman Waters' close personal ties to OneUnited Bank, what may be of greater consequence for African American communities is the nominal number of bank loans for community improvement.' In addition to an uneven role in community development, the demographic composition of minority banks has transformed in the past decades. -

Chinese Immigration and Its Implications on Urban Management in Los Angeles

Chen X. CHINESE IMMIGRATION AND ITS IMPLICATIONS ON URBAN MANAGEMENT IN LOS ANGELES CHINESE IMMIGRATION AND ITS IMPLICATIONS ON URBAN MANAGEMENT IN LOS ANGELES Xueming CHEN Virginia Commonwealth University ement 923 West Franklin Street, Richmond, VA 23284, United States of America [email protected] Abstract This paper reviews the Chinese immigration history in Los Angeles, with Chinatown representing its urbanization process and San Gabriel Valley representing its suburbanization process. These two processes are distinct and have different impacting factors. This empirical study also compares similarities and differences of the urban development patterns between the Chinese Americans and the mainstream white Americans. Furthermore, the paper examines the implications of Chinese immigration on local urban management from political, cultural, and socioeconomic aspects. Keywords: urbanization, suburbanization, Los Angeles, Chinatown, San Gabriel Valley. 1. Introduction Los Angeles County is the most populous, multi-ethnic county in the United States (U.S.) with an existing total population exceeding 10 million. Of all the U.S. counties, Los Angeles County has most Chinese American population. In the year 2000, the County’s total Chinese American population Number 4(13) / November 2009 amounted to 377,301, which was 33.6% and 15.6% of all Chinese American population living in California (1,122,187) and U.S. (2,422,970), respectively (Source: http://www.ameredia.com/resources/demographics/chinese.html). Therefore, examining Chinese Americans’ urban development patterns in Los Angeles clearly has its national significance. A good urban management requires a clear understanding about its population, including ethnic population. Theoretical Empirical and Researches in Urban Manag With the globalization trend and emergence of China, Chinese Americans will play an ever important role in future American urbanmanagement, economy and politics. -

Chinatown: a Taste of China in New York City

Chinatown: A Taste of China in New York City Historical Overview Chinatown in New York City was the second Chinatown created after the one made in San Francisco, California. Similar to the first one, Chinatown was originally a place for Chinese immigrants to come to after getting off their long journey on the ships. Originally the Chinese immigrants came to the West in hopes of getting a quick fortune from the Gold Rush or earning money from working on the Transcontinental Railroad. However, they soon realized that there was no potential to obtain wealth or to gain a job since the railroad was completed. They began to work for low wages at textile or cigarette making factories. However, since these immigrants were working at drastically lower prices, Americans were unable to get a job. This caused tension to grow and the Chinese faced increasing discrimination and violence (Waxman par.2-4). To escape these hardships, a majority of Chinese immigrants began to move towards the East Coast. These immigrants typically lived in the slums of the Five Points and the boundary of New York. By staying together, they would be able to support each other and separate themselves from the rest of society to live their own lives. As a result of not assimilating and stealing jobs, the U.S. government enacted the Chinese Exclusion Act of 1882. This diminished the number of Chinese immigrants who could come to the United States unless they had a special permit to enter. This caused the Chinese immigrants to become devastated because they could not bring their family relatives or friends to join them in the United States. -

Investor Presentation November 2017

Investor Presentation November 2017 NASDAQ: RBB Forward‐Looking Statements Certain matters set forth herein (including the exhibits hereto) constitute forward‐looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including forward‐looking statements relating to the Company’s current business plans and expectations and our future financial position and operating results. These forward‐looking statements are subject to risks and uncertainties that could cause actual results, performance and/or achievements to differ materially from those projected. These risks and uncertainties include, but are not limited to, local, regional, national and international economic and market conditions and events and the impact they may have on us, our customers and our assets and liabilities; our ability to attract deposits and other sources of funding or liquidity; supply and demand for real estate and periodic deterioration in real estate prices and/or values in California or other states where we lend, including both residential and commercial real estate; a prolonged slowdown or decline in real estate construction, sales or leasing activities; changes in the financial performance and/or condition of our borrowers, depositors or key vendors or counterparties; changes in our levels of delinquent loans, nonperforming assets, allowance for loan losses and charge‐offs; the costs or effects of acquisitions or dispositions we may make, whether we are able to obtain any required governmental approvals in connection with -

Chinatown Then and Now.Pdf

Bethany Y. Li Asian American Legal Defense and Education Fund (AALDEF) CHINATOWN 99 Hudson St, 12th Fl THEN AND NOW New York, NY 10013 tel: 212 966 5932 fax: 212 966 4303 email: [email protected] a snapshot of new york’s chinatown Chinatown: Then & Now A Snapshot of New York’s Chinatown Introduction The mention of “Chinatown” evokes many images. But for decades, Chinatown has meant home for immigrant families. Chinatown residents rely on networks of friends and relatives in the community and on affordable food and goods in nearby stores. Workers depend on jobs they find in the neighborhood and from employment agencies centered in these communities. Yet as land use struggles change downtown areas across the United States, Chinatowns are becoming increasingly destabilized as their future as sustainable low-income immigrant communities is threatened. The Asian American Legal Defense and Education Fund (AALDEF) embarked on a three-city study of Chinatowns in Boston, New York, and Philadelphia to determine the current state of Chinatowns. Whereas Chinatowns used to be disfavored places to live and dumping grounds for undesirable uses, luxury and institutional developers began targeting these previously shunned areas in the 1980s and 1990s for more luxury uses including high-end condominiums and stadiums. For decades, residents, workers, small business owners, and community organizations have fought against development that threatens to weaken immigrant networks and resources in these neighborhoods. In collaboration with these community partners, academic institutions, and hundreds of volunteers, AALDEF spent a year recording block by block and lot by lot the existing land uses in Boston, New York, and Philadelphia’s Chinatown and surrounding immigrant areas. -

A Comparison of Korean and Chinese American Banks in California*

한국지역지리학회지 제12 권 제 1 호 (2006) 154-171 The Financial Development of Korean Americans: A Comparison of Korean and Chinese American Banks in California* Hyeon-Hyo Ahn**, Yun-Sun Chung*** 미국에서의 한인 금융: 캘리포니아에서 한국계와 중국계 은행의 비교* 안현효**․ 정연선 *** 요약:본 논문은 캘리포니아의 중국계와 한국계의 양 소수민족은행을 비교하여 한국계 민족은행과 한국계 이민사회의 경제적 관계를 해명하고자 한다. 통상 미국 내 소수민족경제권의 경제적 성과 차이는 문화적 차이 또는 비공식금융의 기여로 설명되는 경우가 많으나 우리는 공식금융제도의 적극적 역할에 주목하여 금융제도와 소수민족경제의 관련성을 강조한다.,, 동시에 한국계 미국은행은 성장 수익성 은행전략 면에서 중국계 소수민족은행과 구분된다는 점을 중시하여, 은행전략 측면에서, 중국계와 한국계가 고객과의 장기적 거래를 중시하는 유사한 관계은행전략을 구사하지만, 은행의 대출분포와 예금분포는 서로 다르다는 점을 지적하였다. 이는 각 소수민족은행이 다른 경영성과를 낳는 이유가 된다. 한국계은행의 경우 대출구조가 사업대출 중심이며, 이자 낳지 않는 예금의 비중이 중국계 민족은행보다 상대적으로 높 은 사실이 한국계 소수민족은행이 높은 성장을 하게 된 배경이다. 따라서 관계은행전략이라는 개념만으로는 다수의 소 수민족은행의 차이를 설명할 수 없으므로, 본 연구는 한국계와 중국계의 이민사회 그 자체의 특수성에 주목하였다. 중 국계 미국인의 경우 인구구성의 이질성과 해외자본의 영향이, 한국계 미국인의 경우 동질적 인구 및 사업구성과 착 한 국계 미국인 금융기관의 경쟁력이 특징적이다. 주요어:소수민족은행, 한국계 미국은행 , 중국계 미국은행 , 관계은행 Abstract :By comparing to Chinese American banks, this research shows the uniqueness of Korean American banks. This article argues that instead of the cultural attributes and/or informal financial institutions, formal financial institutions, such as the ethnic banks studied here, are responsible for the business success of Asians abroad. However, ethnic banks have different development trajectories depending on their respective ethnic communities. Korean American banks are notably different from Chinese American banks in terms of growth, profitability, and banking strategies.