Equity Valuation Dissertation Walt Disney Company

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Simonetta Cattaneo Vespucci: Beauty. Politics, Literature and Art in Early Renaissance Florence

! ! ! ! ! ! ! SIMONETTA CATTANEO VESPUCCI: BEAUTY, POLITICS, LITERATURE AND ART IN EARLY RENAISSANCE FLORENCE ! by ! JUDITH RACHEL ALLAN ! ! ! ! ! ! ! A thesis submitted to the University of Birmingham for the degree of DOCTOR OF PHILOSOPHY! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! Department of Modern Languages School of Languages, Cultures, Art History and Music College of Arts and Law University of Birmingham September 2014 University of Birmingham Research Archive e-theses repository This unpublished thesis/dissertation is copyright of the author and/or third parties. The intellectual property rights of the author or third parties in respect of this work are as defined by The Copyright Designs and Patents Act 1988 or as modified by any successor legislation. Any use made of information contained in this thesis/dissertation must be in accordance with that legislation and must be properly acknowledged. Further distribution or reproduction in any format is prohibited without the permission of the copyright holder. ABSTRACT ! My thesis offers the first full exploration of the literature and art associated with the Genoese noblewoman Simonetta Cattaneo Vespucci (1453-1476). Simonetta has gone down in legend as a model of Sandro Botticelli, and most scholarly discussions of her significance are principally concerned with either proving or disproving this theory. My point of departure, rather, is the series of vernacular poems that were written about Simonetta just before and shortly after her early death. I use them to tell a new story, that of the transformation of the historical monna Simonetta into a cultural icon, a literary and visual construct who served the political, aesthetic and pecuniary agendas of her poets and artists. -

Cla Ss Schedu Le

USM Osher Lifelong Learning Institute Fall 2017 Sept. 11 through Nov. 3 CLASS SCHEDULE General Information If you are 50 or older, with a curious mind and an interest in learning just for the joy of it, you are invited to SPECIAL ACCOMMODATIONS OLLI at USM has purchased a portable assistive- join 2,000 like-minded older learners who are members listening device that can be used in any Wishcamper of the Osher Lifelong Learning Institute (OLLI) on the classroom. Students using the device will be able to hear Portland campus of the University of Southern Maine. the instructor. Any OLLI at USM student with hearing OLLI at USM is committed to providing its members difficulties may request the use of this system. Contact the with a wide variety of stimulating courses, lectures, OLLI at USM office at 780-4406 as soon as you register for workshops, and complementary activities in a creative class. and inclusive learning community. If you need other special accommodations to participate As a member of OLLI at USM, you’ll choose from an in OLLI at USM because of disability, please call the USM extensive array of peer-taught courses in the liberal Office of Support for Students with Disabilities at arts and sciences. There are no entrance requirements, 780-4706 as soon as you register but at least two grades, or tests. Your experience and love of learning are what count. Some OLLI at USM classes involve weeks before classes begin. homework — usually reading or honing skills taught in class. Homework is not mandatory, but it can enhance your learning experience; what you put in is what you’ll SCHOLARSHIPS get out of the course. -

Fool Law Hearing Tonight No'4-1 T R ' Law L Nveiling Delayed

IVINDSOR-HIGHTS HERALD VOL. NO. HIGHTSTOWN, NEW JERSEY, THURSDAY, AUG. 1967 Newsstand IOC jyer copy Fool Law T R ’ Law Hearing l nveiling Tonight Delayed Permits, Fences Planning Board V* ouId Be Needed: ^ ants "I il Aug. I $200 t ine Limit To Rework Rill In a five-minute meeting Tues- Publlr hearing on a proposed law- i day night, the East WindsorTown- that would require "durable, 4-6- j ship planning board announced thal fee' nigh fencing around every per i Us revised planned unit develop manent or portable private pool In ment ordinance would not lie un~ F ast Windsor deeper that two feet NTHONY r P AN ' DONALD SCHULTZ | veiled until Thursday, Aug. 17 at : s scheduled for 7:30 tonight before 8 p. m. •he township committee. a O t l g Acting halrman William E. Hightstown of 1910; s Urt«*. Hiirh Sh 0 < * > . I r a i n The lav. designed to cut ac Harvey said the board already had This is the first in a series cidental drowning potential and Main Street across from the his photograph shows a shoes on boys on the station Franzo vs. Schultz gone beyond the recommendation in of nine glimpses at the Hights- tighten pool health standards, Is present location of the Baptist wooden passenger station lo p la if o r d a te the photo in the township committee's resolution town of the turn of the century. - used on one In use In nearby Wash Church, Information on the pho cated at the corner of Railroad vicinity of 1900. -

Preview – the Gallery Guide | November 2011

w w w .p re vi ew -a rt .c om THE GALLERY GUIDE ALBERTA I BRITISH COLUMBIA I OREGON I WASHINGTON Nov/Dec/Jan 2011-2012 Michael Nicoll Yahgulanaas SOLO TWO November 5 – 26, 2011 1 1 0 2 , s e h c n i 0 4 X 6 2 , r e p a p n o a i d e m d e x i m , 6 2 . 5 . 1 1 0 2 r e g g i B , s a a n a l u g h a Y l l o c i N l e a h c i M Opening reception: November 5, 2-4pm DOUGLAS UDELL GALLERY 1566 West 6 th Ave Vancouver, BC V6J 1R2 www.douglasudellgallery.com • 604-736-8900 Serving the visual arts community since 1986 Celebrating 25 years www.preview-art.com 8 PREVIEW I NOVEMBER/DECEMBER/JANUARY 2011/12 Nov/Dec/Jan 2011/2012 previews Vol. 25 No.5 12 Lesley Dill’s Poetic Visions ALBERTA Whatcom Museum 10 Black Diamond, Calgary 20 Edmonton 14 Douglas Coupland: Twelve Slogans 21 Lethbridge 8 TrépanierBaer Gallery 38 2 22 Medicine Hat 16 Norman Lundin: Inside/Outside BRITISH COLUMBIA Hallie Ford Museum of Art 23 Abbotsford, Burnaby 18 Group Exhibition/Emotional Blackmail 24 Campbell River, Castlegar, Southern Alberta Art Gallery 25 Chemainus, Chilliwack, 22 Painting Seattle: Tokita & Nomura Coquitlam Seattle Asian Art Museum 27 Courtenay, Fort Langley, Gibsons, Grand Forks 28 24 Robert Orchardson: Endless façade 30 Kamloops , Kaslo Contemporary Art Gallery 31 Kelowna, Maple Ridge 30 Nature, Knowledge and the Knower 32 Nanaimo, Nelson, Satellite Gallery New Westminster , North Vancou ver 36 Kate Scoones: Wish You Were Here 34 Osoyoos, Penticton, Port Moody, Polychrome Fine Arts Prince George, Prince Rupert 38 Ray Mead (1921-1998) 35 Qualicum Beach, -

Zombie-Loan: V. 2 PDF Book

ZOMBIE-LOAN: V. 2 PDF, EPUB, EBOOK Peach-Pit | 192 pages | 13 Feb 2008 | Little, Brown & Company | 9780759528369 | English | New York, United States Zombie-Loan: v. 2 PDF Book TV Asahi , Animax. Retrieved 16 June They eventually find their determination and renew their will to compete, to save their company. The series ends in a new time line with Michiru witnessing Chika and Shito's accident on television and Bekko announcing the reopening of Zombie Loan. Help Learn to edit Community portal Recent changes Upload file. Both started as doujinshi manga artists, but not as Peach-Pit. Shito saves the girl golem, but she ends up dying when Nogi shoots her in the head as part of "cleaning up". Chika finds Shito and they reunite to fight the twisted doctor Yoshizumi, who is absorbed into his ultimate golem creation. See terms. The Zombie-Loan group ends up going to a hot spring. Later, another old acquaintance of Chika's show up and decide to help him in his search. It contained a total of eleven episodes, with the final broadcast on September 11, As they progress through the world of the Ferryman, they become involved in the affairs of a Ferryman who attempts to use records to destroy the world. And once they learn about Michiru's "Shinigami Eyes," they drag her into their crazy world. To see what your friends thought of this book, please sign up. Want to Read Currently Reading Read. Lee rated it really liked it May 22, Otherwise there don't seem to be to many advances in the illegal zombie front story. -

THE SPRING STAFFORD SALE Important Pioneer, Vintage, Classic

THE SPRING STAFFORD SALE Important Pioneer, Vintage, Classic & Collectors’ Motorcycles and Related Memorabilia Sunday 26 April 2015 The International Classic MotorCycle Show Staffordshire County Showground ot THE SPRING STAFFORD SALE I P R S Sunday 26 April 2015 at 1000 and 1200 The International Classic MotorCycle Show Sandylands Centre Staffordshire County Showground IEING Please note that bids should be ENIRIES STOER SERIES submitted no later than 1600 on Monday to riday 000 100 Saturday 25 April ames Stensel riday 2 April Thereafter bids 0 20 1000 to 100 0 20 6 21 should be sent directly to the 115 to 100 0 00 2 625 fa onhams ofce at the sale enue Please see page 2 for bidder amesstenselbonhamscom Sunday 26 April 0 00 20 0 fa or information including aftersale bidsbonhamscom collection and shipment from 000 ill To 0 20 6 222 e regret that we are unable to ease see ac o cataoe SALE TIES 0 00 2 625 fa accept telephone bids for lots with or imortant notice to idders billtobonhamscom Memorabilia 1000 a low estimate below 500 Motorcycles 1200 Absentee bids will be accepted dmission to he nternationa en aler ew bidders must also proide assic otorce ho 0 20 6 21 ATALOGE PP proof of identity when submitting is not incded in the 0 00 2 625 fa admits two bids ailure to do so may result rice o the cataoe icets benwalerbonhamscom in your bids not being processed can e rchased in adance IDS rom cassicieshos Motorcycle Administrator ASH LIIT AEPTANE co 0 20 Andy arrett 0 20 01 fa ollowing a reiew of its 0 20 6 21 IPORTANT -

Lamass, a Large-Motion Active Suspension System for Powered Wheelchairs

LAMASS: A LARGE-MOTION ACTIVE SUSPENSION SYSTEM FOR POWERED WHEELCHAIRS William W. Li B.A.Sc., Simon Fraser University, 1993 THESIS SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF APPLIED SCIENCES in the School of Engineering Science 0William W. Li 1997 SIMON FRASER UNIVERSITY December 1997 All rights reserved. This work may not be reproduced in whole or in part, by photocopy or other means, without permission of the author. National Library ' BlblioWque nationale of Canada du Canada d Acquisitions and Acquisitions et Bibliographic Services services bibliographiques 395 Wellington Street 395,rue Wellington ' Ottawa ON K 1 A ON4 OnawaON KIA ON4 CaMda. Canada The author has granted a non- L'auteur a accorde une licence non exclusive licence allowing the exclusive pennettant a la National Library of Canada to Bibliotheque nationale du Canada de reproduce, loan, distribute or sell reproduire, przter, distribuer ou copies of th~sthesis in microform, vendre des copies de cette thesesous paper or electronic formats. la forme de microfiche/film, de reproduction sur papier ou sur format electronique. The author retaus ownership -of the L'auteur conserve la proprietk du . copyright in hsthe& Neither the droit d'auteur qui protege cette these. thesis nor substantial extracts from it Ni la these ni des extraits substantiels may be printed or otherwise de celle-ci ne doivent Stre imprimes reproduced without the author's ou autrement reproduits sans son autorisation. Approval Name: William W. Li Degree: ~.A.sc. Title of thesis: LAMASS: A Large-Motion Active Suspension System for Po~,eredWheelchairs Examining Committee: Chair: Dr. -

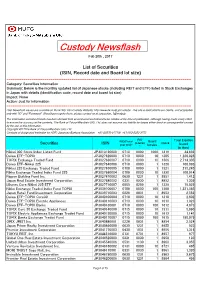

Mizuho BK Custody and Proxy Board Lot Size List JUN 15 , 2021

Mizuho BK Custody and Proxy Board Lot Size List JUN 15 , 2021 Board Lot Stock Name (in Alphabetical Order) ISIN Code QUICK Code Size 21LADY CO.,LTD. 100 JP3560550000 3346 3-D MATRIX,LTD. 100 JP3410730000 7777 4CS HOLDINGS CO.,LTD. 100 JP3163300001 3726 A-ONE SEIMITSU INC. 100 JP3160660001 6156 A.D.WORKS GROUP CO.,LTD. 100 JP3160560003 2982 A&A MATERIAL CORPORATION 100 JP3119800005 5391 A&D COMPANY,LIMITED 100 JP3160130005 7745 ABALANCE CORPORATION 100 JP3969530009 3856 ABC-MART,INC. 100 JP3152740001 2670 ABHOTEL CO.,LTD. 100 JP3160610006 6565 ABIST CO.,LTD. 100 JP3122480001 6087 ACCESS CO.,LTD. 100 JP3108060009 4813 ACCESS GROUP HOLDINGS CO.,LTD. 100 JP3108190004 7042 ACCRETE INC. 100 JP3108180005 4395 ACHILLES CORPORATION 100 JP3108000005 5142 ACMOS INC. 100 JP3108100003 6888 ACOM CO.,LTD. 100 JP3108600002 8572 ACRODEA,INC. 100 JP3108120001 3823 ACTIVIA PROPERTIES INC. 1 JP3047490002 3279 AD-SOL NISSIN CORPORATION 100 JP3122030004 3837 ADASTRIA CO.,LTD. 100 JP3856000009 2685 ADEKA CORPORATION 100 JP3114800000 4401 ADISH CO.,LTD. 100 JP3121500007 7093 ADJUVANT COSME JAPAN CO.,LTD. 100 JP3119620007 4929 ADTEC PLASMA TECHNOLOGY CO.,LTD. 100 JP3122010006 6668 ADVAN CO.,LTD. 100 JP3121950004 7463 ADVANCE CREATE CO.,LTD. 100 JP3122100005 8798 ADVANCE RESIDENCE INVESTMENT CORPORATION 1 JP3047160001 3269 ADVANCED MEDIA,INC. 100 JP3122150000 3773 ADVANEX INC. 100 JP3213400009 5998 ADVANTAGE RISK MANAGEMENT CO.,LTD. 100 JP3122410008 8769 ADVANTEST CORPORATION 100 JP3122400009 6857 ADVENTURE,INC. 100 JP3122380003 6030 ADWAYS INC. 100 JP3121970002 2489 AEON CO.,LTD. 100 JP3388200002 8267 AEON DELIGHT CO.,LTD. 100 JP3389700000 9787 AEON FANTASY CO.,LTD. 100 JP3131420006 4343 AEON FINANCIAL SERVICE CO.,LTD. -

Custody Newsflash Feb 20Th , 2017

Custody Newsflash Feb 20th , 2017 List of Securities (ISIN, Record date and Board lot size) ======================================================================================== Category: Securities Information Summary: Below is the monthly updated list of Japanese stocks (including REIT and ETF) listed in Stock Exchanges in Japan with details (identification code, record date and board lot size) Impact: None Action: Just for information ======================================================================================== Past Newsflash issues are available on the BTMU Yen Custody Website; http://www.bk.mufg.jp/custody/. This site is dedicated to our clients, and accessible only with “ID” and “Password”. Should you require them, please contact us at [email protected]. The information contained herein has been derived from several sources believed to be reliable at the time of publication. Although having made every effort to ensure the accuracy of the contents, The Bank of Tokyo-Mitsubishi UFJ, Ltd. does not assume any liability for losses either direct or consequential caused by the use of this information. Copyright 2017The Bank of Tokyo-Mitsubishi UFJ, Ltd. Contacts of designated institution for ADR: Japanese Bankers Association +81-(0)570-017109 +81-(0)3-5252-3772 R/D R/D(Fiscal Board Total Equities Securities ISIN (Interim) Quick year end)* lot size Issued * (in thou) Nikkei 300 Stock Index Listed Fund JP3013190008 0710 0000 1000 1319 34,632 Daiwa ETF-TOPIX JP3027620008 0710 0000 10 1305 1,280,028 TOPIX Exchange Traded Fund JP3027630007 0710 0000 10 1306 2,714,335 Daiwa ETF-Nikkei 225 JP3027640006 0710 0000 1 1320 100,088 Nikkei 225 Exchange Traded Fund JP3027650005 0708 0000 1 1321 215,245 Nikko Exchange Traded Index Fund 225 JP3027660004 0708 0000 10 1330 108,914 Nippon Building Fund Inc. -

SCOREBOARD by RICK SANTOS a Anti-Bias Biii Manchester Herald Vehicle and Her to Children

24—MANCHESTER HERALD, Wednesday, July 25,1990 WhaVs News Summer Home Improvements...see page 9 Decibel level to be way down at the Patriots’ camp Thursday By The Associated Press players at those positions in camp. “Each coach is certainly allowed Staurovsky. $187,000 this season. He faced “It’s a cleaner operation if you of the regular two-a-days. to coach however he wants,” he At the team’s mini-camp last Veteran linebacker Steve DeOssie $ 1,500 per day fines for the holdout. Local news J can do it,” Rust said TUesday. “I added. “If they’re all quiet, then SMTTHFIELD, R.I. — Screaming May, Hansen beat out Feagles. reUmied to practice after suffering a Seahawks: Seattle agreed to coaches and scheming kickers are guess we’ll find out if it’s a mistake they’re quiet.” “It doesn’t bother me” to have terms with third-year comerback inside or not.” minor cramp Monday while tunning missing from New England’s train But he does want them to “coach just one punter and kicker. Rust Dwayne Harper and signed rookie Last year, when Raymond Berry on a wet field. ing camp. aggressively, coach in detail, correct said. “All we did is move the calen The Giants waived rookie Terry running back Chris Warren, reduc was head coach, the voices of defen every mistake and never do it in a dar up.” ing their holdouts to six. I Board revises Under new coach Rod Rust, the sive coaches Ed Khayat, Don Shin- Sanders when the 6-foot-6, 330- demeaning manner. -

Certain Integrated Repeaters, Switches, Transceivers and Products Containing Same

Certain Integrated Repeaters, Switches, Transceivers and Products Containing Same Investigation No. 337-TA-435 Publication 3547 October 2002 - ~~ Washington. DC 20436 COMMISSIONERS Deanna Tanner Okun, Chairman Jennifer A. Hillman, Vice Chairman Lynn M. Bragg Marcia E. Miller Stephen Koplan Address all communications to Secretary to the Commission United States International Trade Commission Washington, DC 20436 U.S. International Tkade Commission Washington, DC 20436 www.usitc.gov Certain Integrated Repeaters, Switches, Transceivers and Products Containing Same Investigation No. 337-TA-435 Publication 3547 October 2002 UNITED STATES INTERNATIONAL TRADE COMMISSION Washington, D.C. In the Matter of G CERTAIN INTEGRATED REPEATERS, Inv. No. 337-T.4-4- SWITCHES, TRANSCEIVERS AND -4 PRODUCTS CONTAINING SAME 3 U . P' The Commission has determined that there is a violation of section 337 of L- the Tariff Act of 1930 (19 U.S.C. (i 1337) in the unlawfid importation and sale by respondent Altima Communications Inc. of (1) integrated repeaters that are covered by claims 1-7,or 9 of U.S.Letters Patent 5,742,603,and (2) integrated repeaters and switches in plastic ball grid array packages that are covered by claims 23, 24, 27, or 29 of U.S. Letters Patent 5,894,410. Having reviewed the record in this investigation, including the written submissions of the parties, the Commission has made its determination on the issues of remedy, the public interest, and bonding. The Commission has determined that the appropriate form of relief is a limited exclusion order. The Commission has also determined that the public interest factors enumerated in 19 U.S.C. -

Mizuho BK Custody and Proxy Board Lot Size List JAN 26 , 2021 21LADY

Mizuho BK Custody and Proxy Board Lot Size List JAN 26 , 2021 Board Lot Stock Name (in Alphabetical Order) ISIN Code QUICK Code Size 21LADY CO.,LTD. 100 JP3560550000 3346 3-D MATRIX,LTD. 100 JP3410730000 7777 4CS HOLDINGS CO.,LTD. 100 JP3163300001 3726 A DOT CO.,LTD 100 JP3160590000 7063 A-ONE SEIMITSU INC. 100 JP3160660001 6156 A.D.WORKS GROUP CO.,LTD. 100 JP3160560003 2982 A&A MATERIAL CORPORATION 100 JP3119800005 5391 A&D COMPANY,LIMITED 100 JP3160130005 7745 A&T CORPORATION 100 JP3160680009 6722 ABALANCE CORPORATION 100 JP3969530009 3856 ABC-MART,INC. 100 JP3152740001 2670 ABHOTEL CO.,LTD. 100 JP3160610006 6565 ABIST CO.,LTD. 100 JP3122480001 6087 ACCESS CO.,LTD. 100 JP3108060009 4813 ACCESS GROUP HOLDINGS CO.,LTD. 100 JP3108190004 7042 ACCRETE INC. 100 JP3108180005 4395 ACHILLES CORPORATION 100 JP3108000005 5142 ACMOS INC. 100 JP3108100003 6888 ACOM CO.,LTD. 100 JP3108600002 8572 ACRODEA,INC. 100 JP3108120001 3823 ACTCALL INC. 100 JP3108140009 6064 ACTIVIA PROPERTIES INC. 1 JP3047490002 3279 AD-SOL NISSIN CORPORATION 100 JP3122030004 3837 ADASTRIA CO.,LTD. 100 JP3856000009 2685 ADEKA CORPORATION 100 JP3114800000 4401 ADISH CO.,LTD. 100 JP3121500007 7093 ADJUVANT COSME JAPAN CO.,LTD. 100 JP3119620007 4929 ADTEC PLASMA TECHNOLOGY CO.,LTD. 100 JP3122010006 6668 ADVAN CO.,LTD. 100 JP3121950004 7463 ADVANCE CREATE CO.,LTD. 100 JP3122100005 8798 ADVANCE RESIDENCE INVESTMENT CORPORATION 1 JP3047160001 3269 ADVANCED MEDIA,INC. 100 JP3122150000 3773 ADVANEX INC. 100 JP3213400009 5998 ADVANTAGE RISK MANAGEMENT CO.,LTD. 100 JP3122410008 8769 ADVANTEST CORPORATION 100 JP3122400009 6857 ADVENTURE,INC. 100 JP3122380003 6030 ADWAYS INC. 100 JP3121970002 2489 AEON CO.,LTD. 100 JP3388200002 8267 AEON DELIGHT CO.,LTD.