Onbiovc Trend Analysis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Tetraphase Pharmaceuticals, Inc

WBB Securities, LLC Steve Brozak, DMH [email protected] (908) 518-7610 Tetraphase Pharmaceuticals, Inc. (NasdaqGS: TTPH) Initiating Coverage Initiating Coverage with a Speculative Buy Rating February 22, 2018 and a 12-Month Price Target of $6.00 Tetraphase Prepares for Commercialization of a Needed Antibiotic Tetraphase Pharmaceuticals, Inc. (TTPH) is Current Price $2.20 a clinical stage pharmaceutical company, 12 Month Target Price $6.00 with eravacycline as its lead candidate. It is a novel tetracycline-derived antibiotic to 12-Month Trading Range $2.05-$9.93 treat resistant and multidrug-resistant Market Capitalization (Mil) $113.50 infections, including multidrug-resistant Shares Outstanding (Mil) 51.59 Gram-negative infections. Following Avg. Daily Volume 872,642 successful IGNITE1 and IGNITE4 Phase 3 L.T. Debt (Mil) 0.00 trials in complicated intra-abdominal infections (cIAI), a New Drug Application Dividend/Yield N/A (NDA) was filed with the FDA and a Book Value P/S $2.92 Marketing Authorisation Application (MAA) was submitted to the EMA for IV NASDAQ Composite 7,218.23 eravacycline. S&P 500 2,701.33 Historical Performance and Disclosures on Page 10 - 11 Two days ago, TTPH announced an exclusive Source: QUODD+ licensing agreement with Everest Medicines Limited, a C-bridge Capital-backed biopharmaceutical company based in China, to develop and commercialize eravacycline in mainland China, Taiwan, Hong Kong, Macau, South Korea, and Singapore (known as the Territories). Tetraphase will receive an initial upfront payment of $7.0 million and may receive clinical and regulatory milestones of up to $16.5 million as well as a maximum of $20.0 million via achieving annual sales milestones. -

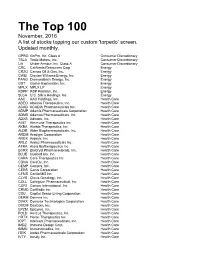

The Top 100 November, 2016 a List of Stocks Topping Our Custom 'Torpedo’ Screen

The Top 100 November, 2016 A list of stocks topping our custom 'torpedo’ screen. Updated monthly. GPRO GoPro, Inc. Class A Consumer Discretionary TSLA Tesla Motors, Inc. Consumer Discretionary UA Under Armour, Inc. Class A Consumer Discretionary CRC California Resources Corp Energy CRZO Carrizo Oil & Gas, Inc. Energy CWEI Clayton Williams Energy, Inc. Energy FANG Diamondback Energy, Inc. Energy GST Gastar Exploration, Inc. Energy MPLX MPLX LP Energy RSPP RSP Permian, Inc. Energy SLCA U.S. Silica Holdings, Inc. Energy AAC AAC Holdings, Inc. Health Care ABEO Abeona Therapeutics, Inc. Health Care ACAD ACADIA Pharmaceuticals Inc. Health Care ADMP Adamis Pharmaceuticals Corporation Health Care ADMS Adamas Pharmaceuticals, Inc. Health Care ADXS Advaxis, Inc. Health Care AIMT Aimmune Therapeutics Inc Health Care AKBA Akebia Therapeutics, Inc. Health Care ALDR Alder Biopharmaceuticals, Inc. Health Care ARDM Aradigm Corporation Health Care ARDX Ardelyx, Inc. Health Care ARLZ Aralez Pharmaceuticals Inc. Health Care ATRA Atara Biotherapeutics Inc Health Care BCRX BioCryst Pharmaceuticals, Inc. Health Care BLUE bluebird bio, Inc. Health Care CARA Cara Therapeutics Inc Health Care CDNA CareDx, Inc. Health Care CEMP Cempra, Inc. Health Care CERS Cerus Corporation Health Care CFMS ConforMIS Inc Health Care CLVS Clovis Oncology, Inc. Health Care COLL Collegium Pharmaceutical, Inc. Health Care CORI Corium International, Inc. Health Care CRMD CorMedix Inc. Health Care CSU Capital Senior Living Corporation Health Care DERM Dermira Inc Health Care DVAX Dynavax Technologies Corporation Health Care DXCM DexCom, Inc. Health Care EPZM Epizyme, Inc. Health Care FOLD Amicus Therapeutics, Inc. Health Care HRTX Heron Therapeutics Inc Health Care ICPT Intercept Pharmaceuticals, Inc. -

NASDAQ Stock Market

Nasdaq Stock Market Friday, December 28, 2018 Name Symbol Close 1st Constitution Bancorp FCCY 19.75 1st Source SRCE 40.25 2U TWOU 48.31 21st Century Fox Cl A FOXA 47.97 21st Century Fox Cl B FOX 47.62 21Vianet Group ADR VNET 8.63 51job ADR JOBS 61.7 111 ADR YI 6.05 360 Finance ADR QFIN 15.74 1347 Property Insurance Holdings PIH 4.05 1-800-FLOWERS.COM Cl A FLWS 11.92 AAON AAON 34.85 Abiomed ABMD 318.17 Acacia Communications ACIA 37.69 Acacia Research - Acacia ACTG 3 Technologies Acadia Healthcare ACHC 25.56 ACADIA Pharmaceuticals ACAD 15.65 Acceleron Pharma XLRN 44.13 Access National ANCX 21.31 Accuray ARAY 3.45 AcelRx Pharmaceuticals ACRX 2.34 Aceto ACET 0.82 Achaogen AKAO 1.31 Achillion Pharmaceuticals ACHN 1.48 AC Immune ACIU 9.78 ACI Worldwide ACIW 27.25 Aclaris Therapeutics ACRS 7.31 ACM Research Cl A ACMR 10.47 Acorda Therapeutics ACOR 14.98 Activision Blizzard ATVI 46.8 Adamas Pharmaceuticals ADMS 8.45 Adaptimmune Therapeutics ADR ADAP 5.15 Addus HomeCare ADUS 67.27 ADDvantage Technologies Group AEY 1.43 Adobe ADBE 223.13 Adtran ADTN 10.82 Aduro Biotech ADRO 2.65 Advanced Emissions Solutions ADES 10.07 Advanced Energy Industries AEIS 42.71 Advanced Micro Devices AMD 17.82 Advaxis ADXS 0.19 Adverum Biotechnologies ADVM 3.2 Aegion AEGN 16.24 Aeglea BioTherapeutics AGLE 7.67 Aemetis AMTX 0.57 Aerie Pharmaceuticals AERI 35.52 AeroVironment AVAV 67.57 Aevi Genomic Medicine GNMX 0.67 Affimed AFMD 3.11 Agile Therapeutics AGRX 0.61 Agilysys AGYS 14.59 Agios Pharmaceuticals AGIO 45.3 AGNC Investment AGNC 17.73 AgroFresh Solutions AGFS 3.85 -

香港知識產權公報hong Kong Intellectual Property Journal

香港知識產權公報 Hong Kong Intellectual Property Journal 2007年7月27日 27 July 2007 公報編號 Journal No.: 225 公布日期 Publication Date: 27-07-2007 分項名稱 Section Name: 目錄 Contents * 目錄 Contents 根據專利條例第 20 條發表的指定專利申請記錄請求 Requests to Record Designated Patent Applications published under section 20 of the Patents Ordinance 1. 按國際專利分類排列 Arranged by International Patent Classification 2. 按發表編號排列 Arranged by Publication Number 3. 按申請編號排列 Arranged by Application Number 4. 按申請人姓名/名稱排列 Arranged by Name of Applicant 根據專利條例第 27 條發表批予標準專利 Granted Standard Patents published under section 27 of the Patents Ordinance 1. 按國際專利分類排列 Arranged by International Patent Classification 2. 按發表編號排列 Arranged by Publication Number 3. 按申請編號排列 Arranged by Application Number 4. 按專利所有人姓名/名稱排列 Arranged by Name of Proprietor 1/336 公報編號 Journal No.: 225 公布日期 Publication Date: 27-07-2007 分項名稱 Section Name: 目錄 Contents 根據專利條例第 118 條發表批予短期專利 Granted Short-term Patents published under section 118 of the Patents Ordinance 1. 按國際專利分類排列 Arranged by International Patent Classification 2. 按發表編號排列 Arranged by Publication Number 3. 按申請編號排列 Arranged by Application Number 4. 按專利所有人姓名/名稱排列 Arranged by Name of Proprietor 根據專利條例(第 514 章)公布的其他公告 Other Notices Published under the Patents Ordinance (Cap. 514) 根據專利條例第 20 條發表後撤回,當作已予撤回或被拒的申請 Applications Withdrawn, Deemed to have been Withdrawn, or Refused, after Publication under section 20 of the Patents Ordinance 根據專利條例第 39 條,標準專利因未繳續期費而停止有效 Standard Patents Ceased through Non-payment of Renewal Fees under section 39 of the Patents Ordinance 根據專利條例第 39(1)(b)條,標準專利 -

February 11-12, 2013 the Waldorf Astoria New York

February 11-12, 2013 The Waldorf Astoria New York 15th ANNU AL EVENT Now in its fifteenth year, the BIO CEO & Investor Conference is the largest independent investor conference focused on leading publicly-traded biotech companies. The meeting provides a neutral forum where institutional investors, industry analysts, and senior biotechnology executives have the opportunity to shape the future investment landscape of the biotechnology industry. Reasons Top 10 to attend 1 Present your company story to an audience of targeted investors. 2 Hear the Washington perspective on the Affordable Care Act, debt ceiling, and other timely policy developments affecting the industry. 3 Evaluate fresh investment opportunities including compatible, complementary and competitive companies. 4 Learn about the hottest clinical developments and industry catalysts by attending the conference’s therapeutic workshops and business roundtables. 5 Attend fireside chats with CEOs who will share their recent company successes, what keeps the C-suite up at night, and where the industry’s leading companies are headed in 2013. 6 Gain access to BIO’s 1x1 Partnering System for scouting potential deal partners and optimizing your time at the event. 7 Access presentations from more than 140 established public and private biotech companies and non-profit funding organizations, including many you won’t hear from at other investor conferences. 8 Get the pulse on the current and proposed investment trends in biotechnology. 9 Network with peers, investors and potential partners attending the conference. 10 It’s the first NYC biotech conference of the year, kicking off a week of key industry events that you don’t want to miss. -

Form 13F-HR Filed 2019-02-14

SECURITIES AND EXCHANGE COMMISSION FORM 13F-HR Initial quarterly Form 13F holdings report filed by institutional managers Filing Date: 2019-02-14 | Period of Report: 2018-12-31 SEC Accession No. 0001567619-19-004367 (HTML Version on secdatabase.com) FILER DEERFIELD MANAGEMENT COMPANY, L.P. (SERIES C) Mailing Address Business Address 780 THIRD AVENUE, 37TH 780 THIRD AVENUE CIK:1009258| IRS No.: 000000000 | State of Incorp.:DE FLOOR 37TH FLOOR Type: 13F-HR | Act: 34 | File No.: 028-05366 | Film No.: 19606038 NEW YORK NY 10017 NEW YORK NY 10017 2125511600 Copyright © 2019 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document OMB APPROVAL UNITED STATES SECURITIES AND EXCHANGE OMB Number: 3235-0006 COMMISSION Expires: July 31, 2015 Washington, D.C. 20549 Estimated average burden hours per response: 23.8 FORM 13F FORM 13F COVER PAGE Report for the Calendar Year or Quarter Ended: 12-31-2018 Check here if Amendment: ☐ Amendment Number: This Amendment (Check only one.): ☐ is a restatement. ☐ adds new holdings entries. Institutional Investment Manager Filing this Report: Name: DEERFIELD MANAGEMENT COMPANY, L.P. (SERIES C) Address: 780 THIRD AVENUE, 37TH FLOOR NEW YORK, NY 10017 Form 13F File Number: 028-05366 The institutional investment manager filing this report and the person by whom it is signed hereby represent that the person signing the report is authorized to submit it, that all information contained herein is true, correct and complete, and that it is understood that all required items, statements, schedules, lists, and tables, are considered integral parts of this form. Person Signing this Report on Behalf of Reporting Manager: Name: James E. -

Guidelines with Regard to the Composition, Calculation and Management of the Index

INDEX METHODOLOGY Solactive Pharma Breakthrough Value Index Version 2.1 dated September 03, 2020 Contents Important Information 1. Index specifications 1.1 Short Name and ISIN 1.2 Initial Value 1.3 Distribution 1.4 Prices and Calculation Frequency 1.5 Weighting 1.6 Index Committee 1.7 Publication 1.8 Historical Data 1.9 Licensing 2. Composition of the Index 2.1 Selection of the Index Components 2.2 Ordinary Adjustment 2.3 Extraordinary Adjustment 3. Calculation of the Index 3.1 Index Formula 3.2 Accuracy 3.3 Adjustments 3.4 Dividends and other Distributions 3.5 Corporate Actions 3.6 Correction Policy 3.7 Market Disruption 3.8 Consequences of an Extraordinary Event 4. Definitions 5. Appendix 5.1 Contact Details 5.2 Calculation of the Index – Change in Calculation Method 2 Important Information This document (“Index Methodology Document”) contains the underlying principles and regulations regarding the structure and the operating of the Solactive Pharma Breakthrough Value Index. Solactive AG shall make every effort to implement regulations. Solactive AG does not offer any explicit or tacit guarantee or assurance, neither pertaining to the results from the use of the Index nor the Index value at any certain point in time nor in any other respect. The Index is merely calculated and published by Solactive AG and it strives to the best of its ability to ensure the correctness of the calculation. There is no obligation for Solactive AG – irrespective of possible obligations to issuers – to advise third parties, including investors and/or financial intermediaries, of any errors in the Index. -

2016 Medicines in Development for Rare Diseases a LIST of ORPHAN DRUGS in the PIPELINE

2016 Medicines in Development for Rare Diseases A LIST OF ORPHAN DRUGS IN THE PIPELINE Autoimmune Diseases Product Name Sponsor Official FDA Designation* Development Status Actemra® Genentech treatment of systemic sclerosis Phase III tocilizumab South San Francisco, CA www.gene.com Adempas® Bayer HealthCare Pharmaceuticals treatment of systemic sclerosis Phase II riociguat Whippany, NJ www.pharma.bayer.com ARA 290 Araim Pharmaceuticals treatment of neuropathic pain in patients Phase II Tarrytown, NY with sarcoidosis www.ariampharma.com ARG201 arGentis Pharmaceuticals treatment of diffuse systemic sclerosis Phase II (type 1 native bovine skin Collierville, TN www.argentisrx.com collagen) BYM338 Novartis Pharmaceuticals treatment of inclusion body myositis Phase III (bimagrumab) East Hanover, NJ www.novartis.com CCX168 ChemoCentryx treatment of anti-neutrophil cytoplasmic Phase II (5a receptor antagonist) Mountain View, CA auto-antibodies associated vasculitides www.chemocentryx.com (granulomatosis with polyangitis or Wegener's granulomatosis), microscopic polyangitis, and Churg-Strauss syndrome * This designation is issued by the FDA's Office of Orphan Products Development while the drug is still in development. The designation makes the sponsor of the drug eligible for entitlements under the Orphan Drug Act of 1983. The entitlements include seven years of marketing exclusivity following FDA approval of the drug for the designated use. Medicines in Development: Rare Diseases | 2016 1 Autoimmune Diseases Product Name Sponsor Official FDA -

09-002 Phrma Heartdis09

201R1e port M EDICINES IN D EVELOPMENT FOR Heart Disease and Stroke PRESENTED BY AMERICA ’ S BIOPHARMACEUTICAL RESEARCH COMPANIES Biopharmaceutical Research Companies Are Developing Nearly 300 Medicines for Cardiovascular Disease iopharmaceutical research companies are MEDICINES IN DEVELOPMENT FOR HEART DISEASE AND STROKE * developing 299 new medicines for two of the Bleading causes of death of Americans—heart disease Acute Cor onary Syndrome 22 and stroke. The work continues the momentum of drug Adjunctive Therapies 5 Arrhythmia/Atrial Fibrillation 15 discovery that has helped cut deaths from these diseases Atherosclerosis 15 by 28 percent between 1997 and 2007. All of the medicines Coronary Artery Disease 9 are either in clinical trials or awaiting review by the Heart Attack 17 Food and Drug Administration. Heart Failure 36 Hypertension 27 According to the National Center for Health Statistics, Imaging Agents 11 heart disease has topped the list of killer diseases every Ischemic Disorders 23 43 year but one since 1900. (The exception was 1918, Lipid Disorders Peripheral Vascular Disease 20 when an influenza epidemic killed more than 450,000 Pulmonary Vascular Disease 17 Americans.) Stroke 27 Thrombosis 28 Thanks in large part to new drug treatments, death rates Other 35 from heart disease and stroke are falling. In 2008, stroke dropped to the fourth leading cause of death after being *S ome medicines are listed in more than one category. the third for over 50 years. According to the National Heart, Lung and Blood Institute (NHLBI), if death rates The medicines in development include 43 for lipid were the same as those of 30 years ago, 815,000 more disorders, such as high cholesterol, 36 for heart failure, Americans would die of heart disease annually and 27 for high blood pressure, 17 for heart attacks, and 250,000 more would die of stroke. -

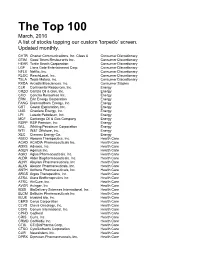

The Bottom 99

The Top 100 March, 2016 A list of stocks topping our custom 'torpedo’ screen. Updated monthly. CHTR Charter Communications, Inc. Class A Consumer Discretionary GTIM Good Times Restaurants Inc. Consumer Discretionary HEAR Turtle Beach Corporation Consumer Discretionary LGF Lions Gate Entertainment Corp. Consumer Discretionary NFLX Netflix, Inc. Consumer Discretionary RLOC ReachLocal, Inc. Consumer Discretionary TSLA Tesla Motors, Inc. Consumer Discretionary RKDA Arcadia Biosciences, Inc. Consumer Staples CLR Continental Resources, Inc. Energy CRZO Carrizo Oil & Gas, Inc. Energy CXO Concho Resources Inc. Energy ERN Erin Energy Corporation Energy FANG Diamondback Energy, Inc. Energy GST Gastar Exploration, Inc. Energy LNG Cheniere Energy, Inc. Energy LPI Laredo Petroleum, Inc. Energy MCF Contango Oil & Gas Company Energy RSPP RSP Permian, Inc. Energy WLL Whiting Petroleum Corporation Energy WTI W&T Offshore, Inc. Energy XEC Cimarex Energy Co. Energy ABEO Abeona Therapeutics, Inc. Health Care ACAD ACADIA Pharmaceuticals Inc. Health Care ADXS Advaxis, Inc. Health Care AGEN Agenus Inc. Health Care AGIO Agios Pharmaceuticals, Inc. Health Care ALDR Alder Biopharmaceuticals, Inc. Health Care ALNY Alnylam Pharmaceuticals, Inc Health Care ALXN Alexion Pharmaceuticals, Inc. Health Care ANTH Anthera Pharmaceuticals, Inc. Health Care ARGS Argos Therapeutics, Inc. Health Care ATRA Atara Biotherapeutics Inc Health Care ATRC AtriCure, Inc. Health Care AVGR Avinger, Inc. Health Care BDSI BioDelivery Sciences International, Inc. Health Care BLCM Bellicum Pharmaceuticals Inc Health Care BLUE bluebird bio, Inc. Health Care CERS Cerus Corporation Health Care CLVS Clovis Oncology, Inc. Health Care CORI Corium International, Inc. Health Care CPHD Cepheid Health Care CRIS Curis, Inc. Health Care CRMD CorMedix Inc. Health Care CTIC CTI BioPharma Corp. -

8Th Annual BIO Investor Forum

Monday Conrad Duke of Windsor Park South Basildon East Foyer Jade/Astor February 11, 2013 4th Floor 3rd Floor 7:00 – 7:55am Networking Breakfast: Grand Ballroom 8:00 – 8:45am Fireside Chat with Robert Hugin, Chairman and CEO, Celgene Corporation (Astor) Oxygen Proteon Therapeutics 9:00 – 9:25am Innovus Pharma Galena BioPharma GTx Biotherapeutics Tobira Therapeutics Show Me the Money: Reimbursement in an ACA World Transition Regado Biosciences 9:30 – 9:55am Verastem Advaxis ChemoCentryx (Jade) Therapeutics ALS TDI (PAG) CoLucid Pharmaceuticals ImmunoCellular 10:00 – 10:25am Advanced Cell Technology TBD Rigel Pharmaceuticals Actinium Pharmaceuticals Therapeutics Onconova Therapeutics Furiex 10:30 – 10:55am ReNeuron GENFIT NPS Pharmaceuticals Oncology: uniQure Pharmaceuticals Panning for Gold—Prospecting Fate Therapeutics Lexicon the Pancreatic Pipeline 11:00 – 11:25am Palatin Technologies CEL-SCI Corporation Repros Therapeutics Zafgen Pharmaceuticals (Jade) NovaBay Provectus LL Society (PAG) Tonix 11:30 – 11:55am Agenus Pharmaceuticals Pharmaceuticals Five Prime Therapeutics Pharmaceuticals 12:00 – 12:55pm Opening Plenary Session: Word on the Street – Buy-Side View for 2013 (Jade) – Box Lunch Catabasis Pharmaceuticals Fireside Chat with John Lechleiter, 1:00 – 1:25pm Anteo Diagnostics Atossa Genetics Targacept Synergy Pharmaceuticals Promedior Chairman, President & CEO, Eli Lilly KineMed (Astor; 1:00-1:45pm) 1:30 – 1:55pm ProMetic Life Sciences CytRx Corporation Biotie Therapies Cytokinetics TVAX Biomedical Good Start Genetics 2:00 – 2:25pm -

February 10-11, 2014 the Waldorf Astoria New York

February 10-11, 2014 The Waldorf Astoria New York Now in its sixteenth year, the BIO CEO & Investor Conference is the largest independent investor conference focused on leading publicly-traded biotech companies, with a special focus on select established private companies. The meeting provides a neutral forum where institutional investors, industry analysts, and senior biotechnology executives have the opportunity to shape the future investment landscape of the biotechnology industry. Reasons Top 10 to attend 1 35% of the biotechs who filed an IPO in 2013 will be presenting at this year’s BIO CEO & Investor Conference. 2 Hear the Washington perspective on the Affordable Care Act and other timely policy developments affecting the industry. 3 Evaluate fresh investment opportunities including compatible, complementary and competitive companies. 4 Learn about the hottest clinical developments and industry catalysts by attending the conference’s therapeutic workshops and business roundtables. 5 Attend fireside chats with CEOs who will share their recent company successes, what keeps the C-suite up at night, and where the industry’s leading companies are headed in 2014. 6 Gain access to BIO’s 1x1 Partnering SystemTM for scouting potential investments and deal partners, optimizing your time at the event. 7 Hear presentations from more than 150 established public and private biotech companies and non-profit funding organizations, including many you won’t hear from at other investor conferences. 8 Get the pulse of the current and proposed investment