Biofuels - at What Cost ?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Physicochemical, Pasting and Sensory Properties of Yam/Plantain Flour Enriched with Soybean Flour

GSJ: Volume 7, Issue 12, December 2019 ISSN 2320-9186 681 GSJ: Volume 7, Issue 12, December 2019, Online: ISSN 2320-9186 www.globalscientificjournal.com PHYSICOCHEMICAL, PASTING AND SENSORY PROPERTIES OF YAM/PLANTAIN FLOUR ENRICHED WITH SOYBEAN FLOUR 1Oloye, D.A*., 2Udeh Charles, 3Olawale-Olakunle, O. E., 1Orungbemi, O.O 1Department of Food Science and Technology, Rufus Giwa Polytechnic, Owo, Ondo State 2 Department of Food Science and Technology, Delta State Polytechnic, Ozoro 3 Department of Hospitality Management Technology, Rufus Giwa Polytechnic, Owo *corresponding author: [email protected] ABSTRACT This study was aimed at producing a high nutritious food that will meet nutritional requirements of consumers. The blend of yam, Plantain, Soybean Flour were processed and the resulting flour were formulated at ratio 100:00, 95:5, 80:10:10 and 60:25:15 (Yam, Plantain and Soybean flour). The resulting products were subjected to proximate composition, physicochemical, pasting and sensory evaluation. The result show that addition of soybean and plantain increased the moisture, fibre, fat and protein contents of the blend by about 6.12%, 6.47%, 9.8%, and 10.15%, the bulk density of the blends range from 0.83 (100% yam flour) to 1.56g/m (60% of yam, 25% of plantain and 5% of soybean flour). The least gelation of the diet range from 1.00% to 8.00%. The study also show the pasting properties of the diet. The organoleptic evaluation shows that there was a significant difference among the blend. The addition of soybean flour to yam and plantain flour to form blends successfully produce a high protein energy food. -

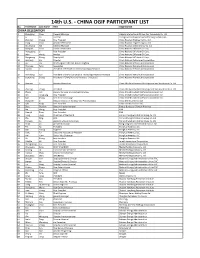

14TH OGIF Participant List.Xlsx

14th U.S. ‐ CHINA OGIF PARTICIPANT LIST No. First Name Last Name Title Organization CHINA DELEGATION 1 Zhangxing Chen General Manager Calgary International Oil and Gas Technology Co. Ltd 2 Li He Director Cheng Du Development and Reforming Commission 3 Zhaohui Cheng Vice President China Huadian Engineering Co. Ltd 4 Yong Zhao Assistant President China Huadian Engineering Co. Ltd 5 Chunwang Xie General Manager China Huadian Green Energy Co. Ltd 6 Xiaojuan Chen Liason Coordinator China National Offshore Oil Corp. 7 Rongguang Li Vice President China National Offshore Oil Corp. 8 Wen Wang Analyst China National Offshore Oil Corp. 9 Rongwang Zhang Deputy GM China National Offshore Oil Corp. 10 Weijiang Liu Director China National Petroleum Cooperation 11 Bo Cai Chief Engineer of CNPC RIPED‐Langfang China National Petroleum Corporation 12 Chenyue Feng researcher China National Petroleum Corporation 13 Shaolin Li President of PetroChina International (America) Inc. China National Petroleum Corporation 14 Xiansheng Sun President of CNPC Economics & Technology Research Institute China National Petroleum Corporation 15 Guozheng Zhang President of CNPC Research Institute(Houston) China National Petroleum Corporation 16 Xiaquan Li Assistant President China Shenhua Overseas Development and Investment Co. Ltd 17 Zhiming Zhang President China Shenhua Overseas Development and Investment Co. Ltd 18 Zhang Jian deputy manager of unconventional gas China United Coalbed Methane Corporation Ltd 19 Wu Jianguang Vice President China United Coalbed Methane Corporation Ltd 20 Jian Zhang Vice General Manager China United Coalbed Methane Corporation Ltd 21 Dongmei Li Deputy Director of Strategy and Planning Dept. China Zhenhua Oil Co. Ltd 22 Qifa Kang Vice President China Zhenhua Oil Co. -

Natural Gas and Israel's Energy Future

Environment, Energy, and Economic Development A RAND INFRASTRUCTURE, SAFETY, AND ENVIRONMENT PROGRAM THE ARTS This PDF document was made available CHILD POLICY from www.rand.org as a public service of CIVIL JUSTICE the RAND Corporation. EDUCATION ENERGY AND ENVIRONMENT Jump down to document6 HEALTH AND HEALTH CARE INTERNATIONAL AFFAIRS The RAND Corporation is a nonprofit NATIONAL SECURITY research organization providing POPULATION AND AGING PUBLIC SAFETY objective analysis and effective SCIENCE AND TECHNOLOGY solutions that address the challenges SUBSTANCE ABUSE facing the public and private sectors TERRORISM AND HOMELAND SECURITY around the world. TRANSPORTATION AND INFRASTRUCTURE Support RAND WORKFORCE AND WORKPLACE Purchase this document Browse Books & Publications Make a charitable contribution For More Information Visit RAND at www.rand.org Explore the RAND Environment, Energy, and Economic Development Program View document details Limited Electronic Distribution Rights This document and trademark(s) contained herein are protected by law as indicated in a notice appearing later in this work. This electronic representation of RAND intellectual property is provided for non-commercial use only. Unauthorized posting of RAND PDFs to a non-RAND Web site is prohibited. RAND PDFs are protected under copyright law. Permission is required from RAND to reproduce, or reuse in another form, any of our research documents for commercial use. For information on reprint and linking permissions, please see RAND Permissions. This product is part of the RAND Corporation monograph series. RAND monographs present major research findings that address the challenges facing the public and private sectors. All RAND mono- graphs undergo rigorous peer review to ensure high standards for research quality and objectivity. -

Giant Miscanthus Establishment

Giant Miscanthus Establishment Introduction Giant Miscanthus (Miscanthus x giganteus), a warm-season perennial grass originating in Southeast Asia from two ornamental grasses, M. sacchariflorus and M. sinensis, is a popular candidate crop for biomass production in the Midwestern United States. This sterile hybrid is high yielding with many benefits to the land including soil stabilization and carbon sequestration. Vegetative propagation methods are necessary since giant Miscanthus does not produce viable seed. Field Preparation A giant Miscanthus stand first begins with field seedbed preparation. To provide good soil to rhizome contact, Figure 1. Rhizome segments. Photo credit: Heaton Lab. the seedbed should be tilled to a 3- to 5-inch depth. Soil moisture is critical to proper establishment for early stage time after the first frost in the fall and before the last one in germination. If working with dry land, prepare your field just the spring. If not immediately replanted in a new field, they prior to planting for optimal soil moisture. Good soil contact should be kept moist and cool (37-40º F) in storage. Ideal is also critical, so conversely, don’t till when the land is wet rhizomes have two to three visible buds, are light colored, and clods will form. Nutrient (NPK) and lime applications and firm (Fig. 1). Smaller rhizomes or those that are soft to should be made to the field as necessary before planting, the touch will likely have lower emergence. following typical corn recommendations for the area. Giant Miscanthus does not have high nutrient requirements once RHIZOME PLANTING established, but fields last for 20-30 years, so it is important Specialized rhizome planters are becoming available that adequate nutrition be present at establishment. -

February 2019 Garden & Landscape Newsletter Sweet Potato Or Yam?

February 2019 Garden & Landscape Newsletter U of A Cooperative Extension, Pinal County 820 E. Cottonwood Lane, Bldg. C., Casa Grande, AZ 85122 (520) 836-5221 http://extension.arizona.edu/pinal Sweet Potato or Yam? Someone asked me the other day to describe the difference between a sweet potato and a yam. It really is an interesting story. The terms ‘sweet potato’ and ‘yam’ can be confusing because in both plants the section of the root that we eat, the tuber, look very similar. They look so much alike that sometimes people use the two names interchangeably, that is, they consider both a sweet potato and a yam the same thing. Actually, these two root crops are big time different, and botanically speaking that difference is like night and day. To really appreciate the difference between them, we have to take a short peek at the plant world. A basic rule of botany is that the plant kingdom is quite diverse. To make that diversity easier to understand, botanists have divided plants up into groups or divisions. Each member of a specific division has the same characteristics as the other members of that division. Some of the plant divisions are made up of simple plants, like algae and fungi. Others are more complex because they have tubes inside of them that carry water and energy throughout the plant. Almost all of our garden and landscape plants fit into this category. Of the several divisions of higher plants, the largest by far are those plants that produce flowers. Flowering plants are divided up into two major groups with the basic characteristic used by botanists to separate them being the number of energy storage structures in the seed. -

Biofuels in Africa Impacts on Ecosystem Services, Biodiversity and Human Well-Being

UNU-IAS Policy Report UNU-IAS Policy Report Biofuels in Africa Biofuels in Africa Impacts on Ecosystem Services, Impacts on Ecosystem Services, Biodiversity and Human Well-being Biodiversity and Human Well-being Alexandros Gasparatos Oxford University Lisa Y. Lee UNU-IAS Graham P. von Maltitz CSIR Manu V. Mathai UNU-IAS Jose A. Puppim de Oliveira UNU-IAS Katherine J. Willis Oxford University United National University Institute of Advanced Studies 6F, International Organizations Center Paci co-Yokohama, 1-1-1 Minato Mirai Nishi-ku, Yokohama 220-8520, Japan Tel +81 45 221 2300 Fax +81 45 221 2302 Email [email protected] URL http://www.ias.unu.edu printed on Forest Stewardship Council TM (FSC TM) certi ed paper using soy-based ink UNU-IAS Policy Report Biofuels in Africa Impacts on Ecosystem Services, Biodiversity and Human Well-being Alexandros Gasparatos Oxford University Lisa Y. Lee UNU-IAS Graham P. von Maltitz CSIR Manu V. Mathai UNU-IAS Jose A. Puppim de Oliveira UNU-IAS Katherine J. Willis Oxford University Copyright ©United Nations University, University of Oxford, and Council for Scientific and Industrial Research (CSIR) South Africa The views expressed in this publication are those of the authors and do not necessarily reflect the views of the United Nations University or the Institute of Advanced Studies, the University of Oxford, or the Council for Scientific and Industrial Research. United Nations University Institute of Advanced Studies 6F, International Organizations Center Pacifico-Yokohama 1-1-1 Minato Mirai Nishi-ku, -

Plant-Based Recipes

A collection of 100% PLANT-BASED RECIPES Breakfasts and smoothies p.02 Starters p.05 Mains p.06 Sweet treats p.12 Break- fasts and smooth- ies: Overnight Oats with Shiro Miso serves 1 The miso gives these oats their pleasant ‘umami’ taste (the ‘new’ fifth taste sensation). If you need to eat breakfast away from home, make this in an empty jam jar, and give your taste buds a treat! Nutrition Information: (Approximate nutrition information per serving with fresh fruit/ berries, nuts and maple syrup) Energy (kcals) 349 Fat (g) 12.6 Saturates (g) 1.3 Carbs (g) 47.1 Sugar (g) 5.5 Fibre (g) 6.7 Protein (g) 8.5 INGREDIENTS: METHOD: ½ cup (45 g) of porridge oats ¾ cup (180 mls) of Oatly Oat Drink 1. Mix all of the ingredients except the (preferably Whole/Barista Edition) topping in a bowl (or jam jar), cover and ½ tbsp white Shiro Miso paste leave in ‘fridge for at least 3 hours, but ideally overnight. Topping - your choice from maple 2. Remove from the ‘fridge and, if you syrup, fresh fruit/berries and wish, add more oat drink, until you get roasted nuts the desired consistency. 3. Top with your chosen toppings and enjoy! 02 Avocado & Strawberry smoothie INGREDIENTS: serves 2 This creamy smoothie is quick to make 300 ml Oatly Oat Drink and refreshing at any time of day. 150 g frozen strawberries ½ ripe avocado, peeled Nutrition Information: Juice of ½ lemon (Approximate nutrition information per serving) 1 tbsp maple or agave syrup 2 tsp chia seeds Energy (kcals) 182 Fat (g) 7.8 Saturates (g) 1.1 Carbs (g) 23.9 METHOD: Sugar (g) 13.6 Fibre (g) 4.9 1. -

Influence of Yam /Cassava Based Intercropping Systems with Legumes in Weed Suppression and Disease/Pest Incidence Reduction

Journal of American Science, 3(1), 2007, Ibeawuchi, et al, Influence of Yam /Cassava Based Intercropping Systems Influence of Yam /Cassava Based Intercropping Systems with Legumes in Weed Suppression and Disease/Pest Incidence Reduction Ibeawuchi I.I., Dialoke S.A., Ogbede K.O., Ihejirika G.O., Nwokeji E.M., Chigbundu I.N., Adikuru N.C., Oyibo Patricia Obilo Department of Crop Science and Technology, Federal University of Technology ***P.M.B 1526 Owerri Nigeria, [email protected] Abstract: The research showed that intercropping significantly suppressed weeds, reduced pest/disease infestation and thereby can play a leading role in integrated pest management. However, no pests and diseases were observed in all plots at 4WAP while low incidence of termite and stem borers were observed at 8 and 12 WAP respectively. Although, there were heavy weed weights at 4 and 8 WAP, indicating weed troublesome nature and how it constitutes a major limiting factor to food production if not checked. Early canopy cover shading the land area on stakes and fast spread of the landrace legumes covering the ground reduced weed incidence at 12 WAP and beyond while timely weeding also reduced weed and host for pest and diseases syndrome prevalent in unweeded farms in rainforest zones. [The Journal of American Science. 2007;3(1):49-59]. Keywords: Weed suppression; diseased pest incidence; yam/cassava/legume; intercropping systems 1. Introduction through its diverse crop species and morphology, keep Intercropping plays a significant role in integrated low its attack and destructive tendencies since some of pest management. Intercropping with yam and or the intercrop species may be resistant to the pest and or cassava is vital in weed, pest and disease reduction disease. -

Clean Tech Handbook for Asia Pacific May 2010

Clean Tech Handbook for Asia Pacific May 2010 Asia Pacific Clean Tech Handbook 26-Apr-10 Table of Contents FOREWORD .................................................................................................................................................. 16 1 INTRODUCTION.................................................................................................................................... 19 1.1 WHAT IS CLEAN TECHNOLOGY? ........................................................................................................................ 19 1.2 WHY CLEAN TECHNOLOGY IN ASIA PACIFIC? .......................................................................................................19 1.3 FACTORS DRIVING THE CLEAN TECH MARKET IN ASIA PACIFIC .................................................................................20 1.4 KEY CHALLENGES FOR THE CLEAN TECH MARKET IN ASIA PACIFIC ............................................................................20 1.5 WHO WOULD BE INTERESTED IN THIS REPORT? ....................................................................................................21 1.6 STRUCTURE OF THE HANDBOOK ........................................................................................................................ 21 PART A – COUNTRY REVIEW.......................................................................................................................... 22 2 COUNTRY OVERVIEW.......................................................................................................................... -

Potato, Sweet Potato, Indigenous Potato, Cassava) in Southern Africa

South African Journal of Botany 2004, 70(1): 60–66 Copyright © NISC Pty Ltd Printed in South Africa — All rights reserved SOUTH AFRICAN JOURNAL OF BOTANY EISSN 1727–9321 Sustainable production of root and tuber crops (potato, sweet potato, indigenous potato, cassava) in southern Africa J Allemann1*, SM Laurie, S Thiart and HJ Vorster ARC–Roodeplaat Vegetable and Ornamental Plant Institute, Private Bag X239, Pretoria 0001, South Africa 1 Current address: Department of Soil, Crop and Climate Sciences, Faculty of Natural and Agricultural Sciences, University of the Free State, PO Box 339, Bloemfontein 9300, South Africa * Corresponding author, e-mail: [email protected] Received 15 October 2003, accepted 17 October 2003 Africa, including South Africa, is faced with a problem of of healthy planting material are the most important lim- increasing rural poverty that leads to increasing urban- iting factors in production. African Cassava Mosaic isation, joblessness, crime, food insecurity and malnu- Disease (CMD) caused by a virus, is a problem in grow- trition. Root and tuber crops such as sweet potato and ing cassava. Plant biotechnology applications offer a potato, as well as cassava and indigenous potato are number of sustainable solutions. Basic applications important crops for food security. The latter are also such as in vitro genebanking where large numbers of important due to their tolerance to marginal conditions. accessions can be maintained in a small space, meris- Potato and sweet potato are of great economic value in tem cultures to produce virus-free plants and mass South Africa, with well-organised marketing chains and, propagation of popular cultivars in order to make plant- for potato, a large processing industry. -

2016 State Utility Commissioners Clean Energy Policy and Technology Leadership Mission to China

2016 STATE UTILITY COMMISSIONERS CLEAN ENERGY POLICY AND TECHNOLOGY LEADERSHIP MISSION TO CHINA SPONSORED BY OFFICE OF CLEAN COAL & CARBON MANAGEMENT US-CHINA CLEAN ENERGY RESEARCH CENTER US DEPARTMENT OF ENERGY BEIJING, HAIYANG, SHANGHAI, AND ORDOS TRIP REPORT ROBERT W. GEE, PRESIDENT SHERI S. GIVENS, SENIOR VICE PRESIDENT .... Gee Strategies 11111 Group,LLc WASHINGTON | AUSTIN WITH SPECIAL APPRECIATION TO: COMMISSIONER TRAVIS KAVULLA, MONTANA COMMISSIONER DAVID ZIEGNER, INDIANA COMMISSIONER LIBBY JACOBS, IOWA COMMISSIONER SANDY JONES, NEW MEXICO COMMISSIONER SHERINA MAYE EDWARDS, ILLINIOIS JOE GIOVE, US DEPARTMENT OF ENERGY a1J1 6e e Strategies Group,LLc 11111 December 1, 2016 Dr. Robert C. Marlay US Director US-China Clean Energy Research Center Office of International Affairs US Department of Energy Mr. David Mohler Deputy Assistant Secretary for Clean Coal and Carbon Management Office of Fossil Energy US Department of Energy Dear Dr. Marlay and Mr. Mohler: We are forwarding you the 2016 Trip Report for the State Utility Commissioners Clean Energy Policy and Technology Leadership Mission to China As the attached report outlines, each goal we set out to accomplish at the outset of the mission was achieved, and we believe that the lessons learned by the participating state utility commissioners will yield dividends to the US Government and Department of Energy. We extend my deep gratitude for your support for this mission. Sincerely, Robert W. Gee President Gee Strategies Group LLC Sheri S. Givens Sheri S. Givens Senior Vice President Gee Strategies Group LLC Attachment TABLE OF CONTENTS Background 1 Delegation Meetings 2 Beijing 3 Haiyang 33 Shanghai 38 Ordos 44 Major Mission Accomplishments 56 Recommendations 58 Appendices A. -

A Future Biorefinery for the Production of Propionic Acid, Ethanol, Biogas, Heat and Power – a Swedish Case Study

REPORT f3 2013:23 A FUTURE BIOREFINERY FOR THE PRODUCTION OF PROPIONIC ACID, ETHANOL, BIOGAS, HEAT AND POWER – A SWEDISH CASE STUDY Report from an f3 project Authors: Anna Ekman, Linda Tufvesson, Pål Börjesson and Serina Ahlgren PROJECT A FUTURE BIOREFINERY FOR THE PRODUCTION OF PROPIONIC ACID, ETHANOL, BIOGAS, HEAT AND POWER – A SWEDISH CASE STUDY PREFACE This report is the result of a cooperation project within the Swedish Knowledge Centre for Renewable Transportation Fuels (f3). The f3 Centre is a nationwide centre, which through cooperation and a systems approach contributes to the development of sustainable fossil free fuels for transportation. The centre is financed by the Swedish Energy Agency, the Region Västra Götaland and the f3 Partners, including universities, research institutes, and industry (see www.f3centre.se). The report is also based on ongoing research projects financed by the Swedish Energy Agency, which we hereby acknowledge. This report should be cited as: Ekman., et. al., (2013) A future biorefinery for the production of propionic acid, ethanol, biogas, heat and power – A Swedish case study. Report No 2013:23, f3 The Swedish Knowledge Centre for Renewable Transportation Fuels and Foundation, Sweden. Available at www.f3centre.se. f3 2013:23 2 PROJECT A FUTURE BIOREFINERY FOR THE PRODUCTION OF PROPIONIC ACID, ETHANOL, BIOGAS, HEAT AND POWER – A SWEDISH CASE STUDY SUMMARY The overall aim of this f3-project is to assess whether energy integration of bio-based industries will contribute to improved greenhouse gas (GHG) performance, compared to biorefineries between which there is no integration or exchange of energy. Comparisons will also be made against production systems based on fossil feedstock.