Hearing Committee on Oversight and Government

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

82Nd Leg Members

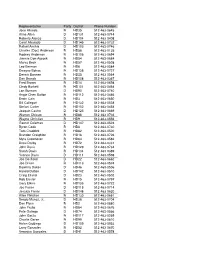

Representative Party District Phone Number Jose Aliseda R HD35 512-463-0645 Alma Allen D HD131 512-463-0744 Roberto Alonzo D HD104 512-463-0408 Carol Alvarado D HD145 512-463-0732 Rafael Anchia D HD103 512-463-0746 Charles (Doc) Anderson R HD56 512-463-0135 Rodney Anderson R HD106 512-463-0694 Jimmie Don Aycock R HD54 512-463-0684 Marva Beck R HD57 512-463-0508 Leo Berman R HD6 512-463-0584 Dwayne Bohac R HD138 512-463-0727 Dennis Bonnen R HD25 512-463-0564 Dan Branch R HD108 512-463-0367 Fred Brown R HD14 512-463-0698 Cindy Burkett R HD101 512-463-0464 Lon Burnam D HD90 512-463-0740 Angie Chen Button R HD112 512-463-0486 Erwin Cain R HD3 512-463-0650 Bill Callegari R HD132 512-463-0528 Stefani Carter R HD102 512-463-0454 Joaquin Castro D HD125 512-463-0669 Warren Chisum R HD88 512-463-0736 Wayne Christian R HD9 512-463-0556 Garnet Coleman D HD147 512-463-0524 Byron Cook R HD8 512-463-0730 Tom Craddick R HD82 512-463-0500 Brandon Creighton R HD16 512-463-0726 Myra Crownover R HD64 512-463-0582 Drew Darby R HD72 512-463-0331 John Davis R HD129 512-463-0734 Sarah Davis R HD134 512-463-0389 Yvonne Davis D HD111 512-463-0598 Joe Deshotel D HD22 512-463-0662 Joe Driver R HD113 512-463-0574 Dawnna Dukes D HD46 512-463-0506 Harold Dutton D HD142 512-463-0510 Craig Eiland D HD23 512-463-0502 Rob Eissler R HD15 512-463-0797 Gary Elkins R HD135 512-463-0722 Joe Farias D HD118 512-463-0714 Jessica Farrar D HD148 512-463-0620 Allen Fletcher R HD130 512-463-0661 Sergio Munoz, Jr. -

District 16 District 142 Brandon Creighton Harold Dutton Room EXT E1.412 Room CAP 3N.5 P.O

Elected Officials in District E Texas House District 16 District 142 Brandon Creighton Harold Dutton Room EXT E1.412 Room CAP 3N.5 P.O. Box 2910 P.O. Box 2910 Austin, TX 78768 Austin, TX 78768 (512) 463-0726 (512) 463-0510 (512) 463-8428 Fax (512) 463-8333 Fax 326 ½ N. Main St. 8799 N. Loop East Suite 110 Suite 305 Conroe, TX 77301 Houston, TX 77029 (936) 539-0028 (713) 692-9192 (936) 539-0068 Fax (713) 692-6791 Fax District 127 District 143 Joe Crab Ana Hernandez Room 1W.5, Capitol Building Room E1.220, Capitol Extension Austin, TX 78701 Austin, TX 78701 (512) 463-0520 (512) 463-0614 (512) 463-5896 Fax 1233 Mercury Drive 1110 Kingwood Drive, #200 Houston, TX 77029 Kingwood, TX 77339 (713) 675-8596 (281) 359-1270 (713) 675-8599 Fax (281) 359-1272 Fax District 144 District 129 Ken Legler John Davis Room E2.304, Capitol Extension Room 4S.4, Capitol Building Austin, TX 78701 Austin, TX 78701 (512) 463-0460 (512) 463-0734 (512) 463-0763 Fax (512) 479-6955 Fax 1109 Fairmont Parkway 1350 NASA Pkwy, #212 Pasadena, 77504 Houston, TX 77058 (281) 487-8818 (281) 333-1350 (713) 944-1084 (281) 335-9101 Fax District 145 District 141 Carol Alvarado Senfronia Thompson Room EXT E2.820 Room CAP 3S.06 P.O. Box 2910 P.O. Box 2910 Austin, TX 78768 Austin, TX 78768 (512) 463-0732 (512) 463-0720 (512) 463-4781 Fax (512) 463-6306 Fax 8145 Park Place, Suite 100 10527 Homestead Road Houston, TX 77017 Houston, TX (713) 633-3390 (713) 649-6563 (713) 649-6454 Fax Elected Officials in District E Texas Senate District 147 2205 Clinton Dr. -

August 1, 2019 Texas Windstorm Insurance

August 1, 2019 Texas Windstorm Insurance Association, Board of Directors c/o John Polak, General Manager P.O. Box 99090 Austin, Texas 78709 Dear TWIA Board of Directors: We, the undersigned coastal members of the 86th Texas Legislature, respectfully request the Texas Windstorm Insurance Association (TWIA) board to postpone or reject consideration of any proposed rate increase on residential and commercial policyholders for the reasons outlined below. In early October, 2018, prior to the 86th Legislature convening, Governor Greg Abbott utilized his executive power in the aftermath of Hurricane Harvey to protect coastal homeowners and business owners from any unnecessary barrier that would impede recovery efforts post-disaster. He wrote a letter to the Texas Department of Insurance (TDI) Commissioner, Kent Sullivan, directing him to "delay any decision to approve or disapprove the proposed rate increase, and any deemed approval of the proposed rate increase, until the Legislature has had a full opportunity to address the matter." The Governor's order to suspend windstorm rates remained in effect until June 16, 2019. On May 24, 2019, the TWIA Board of Directors voted unanimously to withdraw the Association's annual rate filing made in August 2018. The Governor also emphasized the statutory timeframe within which the TWIA board and Commissioner of Insurance were required to consider rate adequacy: "strict compliance with this time frame would deprive the Legislature of the opportunity to address any actuarial deficiency in TWIA during the upcoming legislative session…". The 86th Legislature followed suit by passing significant legislation, Senate Bill 615 and House Bill 1900, addressing rate adequacy transparency and requiring two interim legislative committees, appointed by state leadership, to thoroughly inspect and review the current funding structure. -

April 29, 2020 the Honorable Greg Abbott Governor of Texas P.O. Box

April 29, 2020 The Honorable Greg Abbott Governor of Texas P.O. Box 12428 Austin, TX 78711 Delivered via Email Dear Governor Abbott: Long-term care facilities like nursing homes, state supported living centers, and group homes are now the epicenters of the COVID-19 pandemic. While media outlets have rightly focused on the deaths in nursing homes across the country, people with disabilities and older adults face increased risks in all institutional and congregate settings. Like nursing homes, there have been similar outbreaks and deaths in our state supported living centers, state hospitals, and group homes. Our state government can and must do more to protect our most vulnerable Texans. That is why we respectfully request the following critical measures to defend our elderly Texans, Texans with disabilities, and the Texans on the frontline serving these communities. • Immediate additional funding through an emergency Texas Medicaid rate increase for long-term and intermediate care facilities to help cover increased costs for direct-care staff wages and personal protective equipment (PPE); • Greater transparency in the reporting of COVID-19 deaths and cases in nursing home facilities, state supported living centers, state hospitals, and group homes; • Mandatory available COVID-19 testing for every employee and resident of a nursing home facility, state supported living centers, state hospitals, or group home in Texas. Thank you for your consideration of our request, and ensuring Texas protects our most vulnerable. Please do not hesitate -

Federal and State Elected Officials Representing Districts Within the UH System Service Area

Federal and State Elected Officials Representing Districts Within the UH System Service Area Name Area Represented Alumnus/a U.S. Senate John Cornyn Statewide Kay Bailey Hutchison Statewide U.S. House of Representatives Kevin Brady The Woodlands John Culberson Houston Al Green Houston Gene Green Houston UH, BBA, JD Sheila Jackson Lee Houston Pete Olson Sugar Land Michael McCaul Houston Ted Poe Houston UH, JD Texas Senate Rodney Ellis Houston Mario Gallegos Galena Park UHD, BA Glenn Hegar Katy Joan Huffman Houston Mike Jackson Pasadena Dan Patrick Houston John Whitmire Houston UH, BA Tommy Williams The Woodlands Texas House of Representatives Alma Allen Houston UH, EdD Carol Alvarado Houston BA, UH Dwayne Bohac Houston Dennis Bonnen Angleton Bill Callegari Houston UH, MS Ellen Cohen Bellaire Garnet Coleman Houston Joe Crabb Kingwood Brandon Creighton Conroe John Davis Houston UHCL, BA Harold Dutton Houston Al Edwards Houston Craig Eiland Galveston Rob Eissler The Woodlands Gary Elkins Houston Jessica Farrar Houston UH, BA Allen Fletcher Houston Patricia Harless Spring Ana Hernandez Houston UH, BA Scott Hochberg Houston Charlie Howard Sugar Land Lois Kolkhorst Brenham Ken Legler South Houston Geanie Morrison Victoria Dora Olivo Missouri City UH, MA, JD John Otto Dayton Debbie Riddle Houston Wayne Smith Baytown Larry Taylor League City Kristi Thibaut Houston Senfronia Thompson Houston UH, LLM Sylvester Turner Houston UH, BS Hubert Vo Houston Armando Walle Houston BS, UH Randy Weber Pearland BS, UHCL Beverly Woolley Houston UH, BA John Zerwas Houston UH, BS . -

IDEOLOGY and PARTISANSHIP in the 87Th (2021) REGULAR SESSION of the TEXAS LEGISLATURE

IDEOLOGY AND PARTISANSHIP IN THE 87th (2021) REGULAR SESSION OF THE TEXAS LEGISLATURE Mark P. Jones, Ph.D. Fellow in Political Science, Rice University’s Baker Institute for Public Policy July 2021 © 2021 Rice University’s Baker Institute for Public Policy This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and the Baker Institute for Public Policy. Wherever feasible, papers are reviewed by outside experts before they are released. However, the research and views expressed in this paper are those of the individual researcher(s) and do not necessarily represent the views of the Baker Institute. Mark P. Jones, Ph.D. “Ideology and Partisanship in the 87th (2021) Regular Session of the Texas Legislature” https://doi.org/10.25613/HP57-BF70 Ideology and Partisanship in the 87th (2021) Regular Session of the Texas Legislature Executive Summary This report utilizes roll call vote data to improve our understanding of the ideological and partisan dynamics of the Texas Legislature’s 87th regular session. The first section examines the location of the members of the Texas Senate and of the Texas House on the liberal-conservative dimension along which legislative politics takes place in Austin. In both chambers, every Republican is more conservative than every Democrat and every Democrat is more liberal than every Republican. There does, however, exist substantial ideological diversity within the respective Democratic and Republican delegations in each chamber. The second section explores the extent to which each senator and each representative was on the winning side of the non-lopsided final passage votes (FPVs) on which they voted. -

Sunday, May 26, 2013 — 82Nd

HOUSE JOURNAL EIGHTY-THIRD LEGISLATURE, REGULAR SESSION PROCEEDINGS EIGHTY-SECOND DAY Ð SUNDAY, MAY 26, 2013 The house met at 2 p.m. and was called to order by the speaker. The roll of the house was called and a quorum was announced present (Recordi1286). Present Ð Mr. Speaker; Alonzo; Anderson; Ashby; Aycock; Bell; Bonnen, G.; Branch; Burkett; Burnam; Button; Callegari; Canales; Capriglione; Carter; Clardy; Collier; Cook; Cortez; Craddick; Creighton; Dale; Darby; Davis, J.; Davis, S.; Deshotel; Dukes; Dutton; Elkins; Fallon; Farias; Farney; Fletcher; Flynn; Frank; Frullo; Geren; Goldman; Gonzales; GonzaÂlez, M.; Gonzalez, N.; Gooden; Guerra; Gutierrez; Harper-Brown; Hilderbran; Howard; Huberty; Hughes; Hunter; Isaac; Johnson; Kacal; Keffer; King, K.; King, P.; King, S.; King, T.; Kleinschmidt; Klick; Kolkhorst; Krause; Kuempel; Larson; Lavender; Leach; Lewis; Lozano; MaÂrquez; Martinez; Martinez Fischer; McClendon; Miller, D.; Miller, R.; Morrison; Murphy; Naishtat; NevaÂrez; Oliveira; Orr; Otto; Paddie; Parker; Patrick; Perez; Perry; Phillips; Pickett; Pitts; Price; Raney; Ratliff; Raymond; Riddle; Ritter; Rodriguez, E.; Rose; Sanford; Schaefer; Sheffield, J.; Sheffield, R.; Simmons; Simpson; Smith; Springer; Stephenson; Stickland; Taylor; Thompson, E.; Thompson, S.; Toth; Turner, C.; Turner, E.S.; Turner, S.; Villalba; Villarreal; Vo; White; Workman; Wu; Zedler; Zerwas. Absent Ð Allen; Alvarado; Anchia; Bohac; Bonnen, D.; Coleman; Crownover; Davis, Y.; Eiland; Farrar; Giddings; Guillen; Harless; Hernandez Luna; Herrero; Laubenberg; -

Amicus Brief of Former Speakers of the House

No. 21-0538 In the Supreme Court of Texas IN RE CHRIS TURNER, IN HIS CAPACITY AS A MEMBER OF THE TEXAS HOUSE OF REPRESENTATIVES AND HIS CAPACITY AS CHAIR OF THE HOUSE DEMOCRATIC CAUCUS; TEXAS AFL-CIO; HOUSE DEMOCRATIC CAUCUS; MEXICAN AMERICAN LEGISLATIVE CAUCUS; TEXAS LEGISLATIVE BLACK CAUCUS; LEGISLATIVE STUDY GROUP; THE FOLLOWING IN THEIR CAPACITIES AS MEMBERS OF THE TEXAS HOUSE OF REPRESENTATIVES: ALMA ALLEN, RAFAEL ANCHÍA, MICHELLE BECKLEY, DIEGO BERNAL, RHETTA BOWERS, JOHN BUCY, ELIZABETH CAMPOS, TERRY CANALES, SHERYL COLE, GARNET COLEMAN, NICOLE COLLIER, PHILIP CORTEZ, JASMINE CROCKETT, YVONNE DAVIS, JOE DESHOTEL, ALEX DOMINGUEZ, HAROLD DUTTON, JR., ART FIERRO, BARBARA GERVIN-HAWKINS, JESSICA GONZÁLEZ, MARY GONZÁLEZ, VIKKI GOODWIN, BOBBY GUERRA, RYAN GUILLEN, ANA HERNANDEZ, GINA HINOJOSA, DONNA HOWARD, CELIA ISRAEL, ANN JOHNSON, JARVIS JOHNSON, JULIE JOHNSON, TRACY KING, OSCAR LONGORIA, RAY LOPEZ, EDDIE LUCIO III, ARMANDO MARTINEZ, TREY MARTINEZ FISCHER, TERRY MEZA, INA MINJAREZ, JOE MOODY, CHRISTINA MORALES, EDDIE MORALES, PENNY MORALES SHAW, SERGIO MUÑOZ, JR., VICTORIA NEAVE, CLAUDIA ORDAZ PEREZ, EVELINA ORTEGA, LEO PACHECO, MARY ANN PEREZ, ANA-MARIA RAMOS, RICHARD RAYMOND, RON REYNOLDS, EDDIE RODRIGUEZ, RAMON ROMERO, JR., TONI ROSE, JON ROSENTHAL, CARL SHERMAN, SR., JAMES TALARICO, SHAWN THIERRY, SENFRONIA THOMPSON, JOHN TURNER, HUBERT VO, ARMANDO WALLE, GENE WU, AND ERIN ZWIENER; AND THE FOLLOWING IN THEIR CAPACITIES AS LEGISLATIVE EMPLOYEES: KIMBERLY PAIGE BUFKIN, MICHELLE CASTILLO, RACHEL PIOTRZKOWSKI, AND DONOVON RODRIGUEZ, Relators. Brief of Amici Curiae Former Speakers of the Texas House of Representatives and former Lieutenant Governor of the State of Texas in Support of Petition for Writ of Mandamus Jessica L. Ellsworth Blayne Thompson (pro hac vice application forthcoming) State Bar No. -

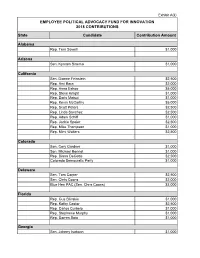

2018 BMS PAC Contributions

Exhibit A(ii) EMPLOYEE POLITICAL ADVOCACY FUND FOR INNOVATION 2018 CONTRIBUTIONS State Candidate Contribution Amount Alabama Rep. Terri Sewell $1,000 Arizona Sen. Kyrsten Sinema $1,000 California Sen. Dianne Feinstein $2,500 Rep. Ami Bera $2,000 Rep. Anna Eshoo $5,000 Rep. Steve Knight $1,000 Rep. Doris Matsui $1,000 Rep. Kevin McCarthy $5,000 Rep. Scott Peters $2,500 Rep. Linda Sanchez $2,500 Rep. Adam Schiff $1,000 Rep. Jackie Speier $2,500 Rep. Mike Thompson $1,000 Rep. Mimi Walters $2,500 Colorado Sen. Cory Gardner $1,000 Sen. Michael Bennet $1,000 Rep. Diana DeGette $2,500 Colorado Democratic Party $1,000 Delaware Sen. Tom Carper $2,500 Sen. Chris Coons $2,000 Blue Hen PAC (Sen. Chris Coons) $3,000 Florida Rep. Gus Bilirakis $1,000 Rep. Kathy Castor $2,500 Rep. Carlos Curbelo $1,000 Rep. Stephanie Murphy $1,000 Rep. Darren Soto $1,000 Georgia Sen. Johnny Isakson $1,000 Sen. David Perdue $2,000 Rep. Buddy Carter $2,500 Iowa Gov. Kim Reynolds $2,000 Sen. Chuck Grassley $2,500 State Sen. Charles Schneider $2,000 State Sen. Tom Shipley $500 Idaho Sen. Mike Crapo $5,000 Illinois Rep. Cheri Bustos $1,000 Rep. Bill Foster $1,000 Rep. Robin Kelly $1,000 Rep. Darin LaHood $1,000 Rep. Pete Roskam $1,000 Rep. Brad Schneider $1,000 Rep. John Shimkus $2,500 Indiana Sen. Mike Braun $1,000 Sen. Joe Donnelly $2,500 Rep. Larry Bucshon $2,500 Rep. Susan Brooks $2,000 Rep. Andre Carson $1,000 Rep. -

TSTA-PAC 2018 Endorsements Primary Winners / Runoffs / Friendly Incumbents

TSTA-PAC 2018 Endorsements Primary Winners / Runoffs / Friendly Incumbents Ryan Guillen - Rio Grande City HD 31** Republican Texas Senate Eric Johnson - Dallas HD 100** Kel Seliger - Amarillo SD 31** Jarvis Johnson - Houston HD 139 Julie Johnson - Dallas HD 115 Texas House of Representatives Ina Minjarez -San Antonio HD 124 Steve Allison – San Antonio HD 121* René O. Oliveira - Brownsville HD 37* Ernest Bailes - Shepherd HD 18 Ron Reynolds - Missouri City HD 27** Keith Bell - Forney HD 4 Shawn Thierry - Houston HD 146** Travis Clardy - Nacogdoches HD 11 John Turner - Dallas HD 114 Scott Cosper - Killeen HD 54* Dan Flynn - Van HD 2 State Board of Education Charlie Geren - Fort Worth HD 99 Ruben Cortez, Jr. - Brownsville SBOE 2 Cody Harris - Palestine HD 8 Marisa B. Perez - San Antonio SBOE 3 Dan Huberty - Houston HD 127** Ken King - Canadian HD 88 General Election Early Endorsement Chris Paddie - Marshall HD 9** Texas Senate Four Price - Amarillo HD 87** Democratic John Raney - Bryan HD 14 Kirk Watson - Austin SD 14 J.D. Sheffield - Gatesville HD 59** Royce West - Dallas SD 23 Hugh Shine - Temple HD 55** Reggie Smith - Sherman HD 62 Texas House of Representatives Lynn Stucky - Sanger HD 64 Democratic Alma Allen - Houston HD 131 Rafael Anchia - Dallas HD 103 Democratic Lt. Governor Nicole Collier - Fort Worth HD 95 Mike Collier - Houston Jessica Farrar - Houston HD 148 Abel Herrero - Robstown HD 34 Texas Senate Gina Hinojosa - Austin HD 49 Beverly Powell - Tarrant SD 10 Donna Howard - Austin HD 48 Nathan Johnson - Dallas SD 16 Victoria Neave - Dallas HD 107 John Whitmire - Houston SD 15 Mary Ann Perez - Houston HD 144 Joseph C. -

BE a UTRGV LEGISLATIVE INTERN at the TEXAS CAPITOL! Live

BE A UTRGV LEGISLATIVE INTERN AT THE TEXAS CAPITOL! Live & Work in Austin While Earning College Credit Earn SIX Credit Hours in Political Science or Academic Credit in certain Masters Programs. Gain ‘Real-World’ Experience – Receive an $8,000 Stipend!* Where will I Intern? Internships are available in the offices of State Legislators at the Texas Capitol in Austin, Texas. When? The 86th Texas Legislative Session begins Jan. 8, 2019. You will report to your Capitol office a few days before. An orientation at UTRGV will be provided prior to your report date. What Will I Do? You will put your academic knowledge into practice as you assist legislators & staff in administration, engage in research and writing assignments, steward legislation, participate in event organization and perform tasks at the Texas Capitol. How will I Benefit? You will acquire a greater understanding of the legislative process, receive training in a learning environment and increase professional skills while earning six upper-level credit hours in political science or Master’s program credit. Students selected for the Austin Legislative Internships will receive $8,000* each to help cover their expenses of living in Austin. How Do I Qualify? You must be currently enrolled at UTRGV, have completed 60 undergraduate hours, including 12 semester credit hours in political science, a 3.0 GPA in political science courses and a 2.5 cumulative GPA. Master’s students must have a minimum 3.0 GPA and enroll in the appropriate course(s) in the academic departments. Who Do I Contact? Contact Dr. Ruth Ann Ragland at [email protected] or Richard Sanchez at [email protected] Apply at: www.utrgv.edu/careercenter/_files/documents/vlip-internship-application.pdf Deadline to Apply: NOVEMBER 15, 2018 Legislative Internships at the Texas Capitol Spring 2019 State Legislative Offices Rio Grande Valley Texas House & Senate Members** TEXAS SENATORS TEXAS REPRESENTATIVES Senator Juan “Chuy” Hinojosa Representative Terry Canales Senator Eddie Lucio Jr. -

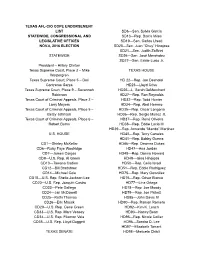

Texas Aflcio Cope Endorsement List Statewide, Congressional and Legislative Offices Nov.8, 2016

TEXAS AFLCIO COPE ENDORSEMENT LIST SD6—Sen. Sylvia Garcia STATEWIDE, CONGRESSIONAL AND SD13—Rep. Borris Miles LEGISLATIVE OFFICES SD19—Sen. Carlos Uresti NOV.8, 2016 ELECTION SD20—Sen. Juan “Chuy” Hinojosa SD21—Sen. Judith Zaffirini STATEWIDE SD26—Sen. José Menéndez SD27—Sen. Eddie Lucio Jr. President – Hillary Clinton Texas Supreme Court, Place 3 – Mike TEXAS HOUSE Westergren Texas Supreme Court, Place 5 – Dori HD 22—Rep. Joe Deshotel Contreras Garza HD23—Lloyd Criss Texas Supreme Court, Place 9 – Savannah HD26—L. Sarah DeMerchant Robinson HD27—Rep. Ron Reynolds Texas Court of Criminal Appeals, Place 2 – HD32—Rep. Todd Hunter Larry Meyers HD34—Rep. Abel Herrero Texas Court of Criminal Appeals, Place 5 – HD35—Rep. Oscar Longoria Betsy Johnson HD36—Rep. Sergio Munoz Jr. Texas Court of Criminal Appeals, Place 6 – HD37—Rep. René Oliveira Robert Burns HD38—Rep. Eddie Lucio III HD39—Rep. Armando “Mando” Martinez U.S. HOUSE HD40—Rep. Terry Canales HD41—Rep. Bobby Guerra CD1—Shirley McKellar HD46—Rep. Dawnna Dukes CD6—Ruby Faye Woolridge HD47—Ana Jordan CD7—James Cargas HD48—Rep. Donna Howard CD9—U.S. Rep. Al Green HD49—Gina Hinojosa CD10—Tawana Cadien HD50—Rep. Celia Israel CD12—Bill Bradshaw HD51—Rep. Eddie Rodriguez CD14—Michael Cole HD75—Rep. Mary González CD18—U.S. Rep. Sheila Jackson Lee HD76—Rep. César Blanco CD20—U.S. Rep. Joaquin Castro HD77—Lina Ortega CD23—Pete Gallego HD78—Rep. Joe Moody CD24—Jan McDowell HD79—Rep. Joe Pickett CD25—Kathi Thomas HD85—John Davis IV CD26—Eric Mauck HD90—Rep. Ramon Romero CD29—U.S.