AMHERST ISLAND July 2014

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Regulars Features

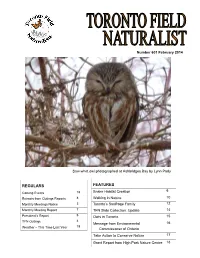

Number 601 February 2014 Saw-whet owl photographed at Ashbridges Bay by Lynn Pady FEATURES REGULARS 9 Coming Events 19 Snake Habitat Creation Extracts from Outings Reports 8 Walking in Nature 10 Monthly Meetings Notice 3 Toronto’s Saxifrage Family 12 Monthly Meeting Report 7 TFN Slide Collection: Update 14 President’s Report 6 Owls in Toronto 15 TFN Outings 4 Message from Environmental 16 19 Weather – This Time Last Year Commissioner of Ontario Take Action to Conserve Nature 17 Grant Report from High Park Nature Centre 18 TFN 601-2 Toronto Field Naturalist February 2014 Toronto Field Naturalist is published by the Toronto Field BOARD OF DIRECTORS Naturalists, a charitable, non-profit organization, the aims of President & Outings Margaret McRae which are to stimulate public interest in natural history and Past President Bob Kortright to encourage the preservation of our natural heritage. Issued Vice President & monthly September to December and February to May. Monthly Lectures Nancy Dengler Views expressed in the Newsletter are not necessarily those Secretary-Treasurer Charles Crawford of the editor or Toronto Field Naturalists. The Newsletter is printed on 100% recycled paper. Communications Alexander Cappell Membership & Newsletter Judy Marshall ISSN 0820-636X Newsletter Vivienne Denton Monthly Lectures Lavinia Mohr IT’S YOUR NEWSLETTER! Nature Reserves & Outings Charles Bruce- We welcome contributions of original writing of observa- Thompson tions on nature in and around Toronto (up to 500 words). Outreach Stephen Kamnitzer We also welcome reports, reviews, poems, sketches, paint- Webmaster Lynn Miller ings and digital photographs. Please include “Newsletter” Anne Powell in the subject line when sending by email, or on the enve- lope if sent by mail. -

The Owl Invasion of Amherst Island, Ontario, January-April 1979

DISTRIBUTION The owl invasion of Amherst Island, Ontario, January-April 1979 A report from the owl capital of the world of the parliament of winter, 19 79 Gary P. Bell, Frank J. S. Phelan and Ron C. P. Wypkema. Photographsby the authors. LTHOUGHNORTHERN OWLS moved into easternNorth America in large Short-eared Owl on Amherst Island. Photo/ numbers in the winter of 1978-79, the Frank J. S. Phelan. invasionof owls in the Kingston, Ontar- io, Canada area was unique. Over the course of the winter, thousands of bird- watchers from across Canada and the United States visited Amherst Island. 3 miles southwestof Kingston. to view an unusualassemblage of owl species. Amherst Island is an isolated rural community lying 2 miles south of the north shore of Lake Ontario, at 44ø10'N, 76ø40'W.The 25-squaremile islandpro- vides a variety of habitats including active farmland, old field pasture, woods and marsh. During the latter part of 1978the pop- ulation densityof meadowvoles (Micro- tus penns.vlvanicus) became very high. Great Gray Owl on Amherst Island. Photo/ The isolation of the island, and the lack Gary P. Be!!. of terrestrial predators such as foxes intensifiesthe natural population cycles Saw-whet Owl on Amherst Island. Photo/ of small mammals. Extreme population Frank J..S. Phelan. "outbreaks", then, are regular occur- rences.Large incursionsof raptorshave long been associatedwith such out- breaks of voles, and periodically raptor densities on Amherst Island and Wolfe Island, 2 miles to the east, increase dramatically in responseto abundances of meadow voles (Phelan. 1976; Phelan and Robertson,1978). These raptor den- sity increasesare easily predicted, but along with this increasein numbers of raptors, comes a highly unpredictable increasein the numbers and diversity of raptor species. -

Amherst Island – Biodiversity Threatened

Amherst Island – Biodiversity Threatened Algonquin Power plans to build 31 to 37 (500 foot tall) Industrial Wind Turbines on Amherst Island. If these are erected, the adverse consequences to Amherst Island’s unique environment will be significant, perhaps irreversible. The project must be stopped! Amherst Island: § 32 Species at Risk § Located on the Atlantic Migratory Flyway § Important Bird Area (IBA) of Global Significance § Internationally recognized for concentrations of wintering hawks and owls / Owl Woods nd § Ranked 2 in biodiversity significance (Lake Ontario Islands - Northeast) For Additional Information go to: ProtectAmherst.yolasite.com 1 Why Algonquin Power cannot be allowed to build 31 to 37 industrial wind turbines on Amherst Island: Amherst Island is an Important Bird Area (IBA) of Global and Continental Significance § The Amherst Island IBA, which encompasses the entire island, is recognized as being a site of Global and Continental Significance for Congregatory Species. Sizeable spring congregations of Brant and Dunlin have been recorded. Between 1994 and 1997 the average number of Brant staging at this site during the spring migration was 3,550, representing just over 1% of the North American population. 1 A diversity of habitats has resulted in Amherst Island becoming a renowned site for a wide variety of other birds including shorebirds, raptors, and land-birds such as large concentrations of migrating swallows. Amherst Island is located on the Atlantic Migratory Flyway § Amherst Island, located on the Atlantic migratory flyway in Lake Ontario, is seasonally impaired by fog and other weather events. Migratory birds and those that inhabit the island often experience low visibility conditions, this may increase the potential number of turbine blade/bird collisions. -

MPAC Decision

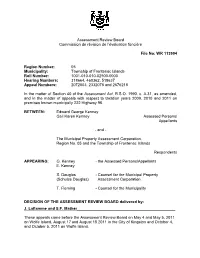

Assessment Review Board Commission de révision de l’évaluation foncière File No: WR 113994 Region Number: 05 Municipality: Township of Frontenac Islands Roll Number: 1001-010-010-02900-0000 Hearing Numbers: 318664, 460362, 518637 Appeal Numbers: 2072003, 2332078 and 2676218 In the matter of Section 40 of the Assessment Act, R.S.O. 1990, c. A.31, as amended, and in the matter of appeals with respect to taxation years 2009, 2010 and 2011 on premises known municipally 222 Highway 96. BETWEEN: Edward George Kenney Gail Karen Kenney Assessed Persons/ Appellants - and - The Municipal Property Assessment Corporation, Region No. 05 and the Township of Frontenac Islands Respondents APPEARING: G. Kenney - the Assessed Persons/Appellants E. Kenney S. Douglas - Counsel for the Municipal Property (Schulze Douglas) Assessment Corporation T. Fleming - Counsel for the Municipality DECISION OF THE ASSESSMENT REVIEW BOARD delivered by: J. Laflamme and S.F. Mather_____________________________________________ These appeals came before the Assessment Review Board on May 4 and May 5, 2011 on Wolfe Island, August 17 and August 18 2011 in the City of Kingston and October 4, and October 5, 2011 on Wolfe Island. 2 File No: WR 113994 INTRODUCTION The assessed persons/appellants’ (the Kenneys) home is located on a 0.72 acre waterfront lot on the west end of Wolfe Island in the Township of Frontenac Islands. The Kenneys built their 1,440 square foot single-family bungalow in 1965 and have resided there since 1966. For the taxation years under appeal, the water frontage for the property is 237 feet. A 396 square foot barn, and a 775 square foot detached garage are also situated on the property. -

Kingston Yacht Club Sailors' Handbook 2014

Kingston Yacht Club Sailors' Handbook 2014 2 Table of Contents Keelboat Racing Schedule _______________________ 4 Regattas at KYC _______________________________ 5 Other Important Sailing Events ___________________ 6 Cruising Schedule ______________________________7 Radio Controlled Schedule _______________________ 8 Women in Wind ________________________________9 Keelboat Racing - Sailing Instructions _____________10 Appendix A: Supplementary Instructions and Courses for Weekend Events ______________________________ 22 Appendix B: Season Awards _____________________ 34 Race Committee Guidelines______________________ 36 Cruising Fleet Program _________________________ 42 Cruising Awards ______________________________ 43 Radio Controlled Racing Season _________________ 44 A word from the shore… _______________________ 45 Contact the Kingston Yacht Club _________________ 51 Location of KYC racing marks ___________ Back Cover 3 Keelboat Racing Schedule April 26th Launch 27th Stepping of Masts 29 Practice Race May 1 Shark Racing Begins 1 PHRF Racing Begins 24th Pigeon Island Race June 7th Sailpast 8 Practice Sprints 14th Harbour Race 21 Single/Doublehanded Race 22 Practice Sprints July 4th Main Duck Island Race 19th Partridge Bowl August 9th Wolfe Island Race September 6th Carruthers Series 30th Weeknight Racing Ends October 4 Chase Race 29th Cradles - Trailer Unloading November 1 Mast De-Stepping 2 Haulout 8th KYC Awards Night 4 Regattas at KYC May 10 Kingston-Quinte Shark Team Race Challenge (Belleville) July 5-6 Eastern Ontario Shark Championship -

September & October Programs

Newsletter of the Northern Arizona Audubon Society ™ Volume XLIX • Number 6 • Sept. - Oct. 2021 September & October Programs Cruising for Seabirds Do your eyes glass over as you turn the pages of a field guide when Nests and Nestlings of the Mogollon Rim you come to the section containing pelagic birds? You know, those birds that require you In the spring and early summer of 2016, Katherine worked as to board a rocky boat and head out into the an ornithological field technician searching ocean, being in fear of tossing your cookies? for nests and measuring nestlings as part of Well, look no further-- Rich Armstrong will an ongoing research study of the life history make those birds easy for you. Come hear strategies of temperate and tropical songbirds. him give a fast-paced humorous presentation Ornithological research often requires long about going to sea to see seabirds in the sea. hours in the field, delicate hands, and an intense From a small boat to birding from a cruise passion for birds. Katherine will share a day in ship, you’ll learn about the 40 birds in North the life of a nest searcher and nestling measurer, America--albatrosses, shearwaters, storm the tools and work required for collecting petrels, and alcids; all of which require you to leave dry land. Both of field research, and a glimpse into the lives of these types of ships have advantages and disadvantages in seeing the many nesting bird species found along the Mogollon Rim. these wonderful birds, and don’t forget the whales and dolphins. -

A Birding Site Guide to Amherst and Wolfe Islands by Paul Mackenzie and Ron D

30 A Birding Site Guide to Amherst and Wolfe Islands by Paul MacKenzie and Ron D. Weir Amherst and Wolfe Islands lie in vole population is high and, as of the eastern end of Lake Ontario, early winter, there have been large near Kingston. Birding is good numbers of Rough-legged Hawks, year-round, especially during the harriers and at least two Boreal winter for hawks and owls, and Owls, as well as Long-eared, during spring and fall for migration Short-eared, Great Horned, of waterfowl and shorebirds. Both Northern Saw-whet, Snowy and islands consist of relatively flat Northern Hawk-Owl. farming country mixed with From Highway 401, take woodlots and surrounded by rocky Highway 133 south about 10 kIn shorelines, gravel beaches and to Highway 33 at Millhaven. Tum cattail marshes. They are right and the ferry dock is about accessible by public ferry, but a 0.3 kIn west along the Lake motor vehicle is essential for Ontario side of Highway 33. The birding the side roads as there is ferry leaves the nlainland hourly no public transport. Property is on the half hour, but the first one private and entry is by permission leaves at 0620 h, then 0730 h, etc. of the landowners, but much It costs $1.50 for car and driver birding can be done from the side plus 25 ¢ per passenger and carries roads and shorelines. Although it about 16 cars, so it is best to arrive is possible to visit both islands in a early. The ferry returns hourly, day, there is plenty of scope for a leaving Amherst I. -

Corporation of Loyalist Township Costing of 2019 Flood Related Damage to Municipal Infrastructure

Corporation of Loyalist Township Costing of 2019 Flood Related Damage to Municipal Infrastructure October 15, 2019 BT Eng Project 19-027 Corporation of Loyalist Township Costing of Flood Related Damage to Municipal Infrastructure October 15, 2019 Table of Contents 1.0 Introduction ................................................................................................................... 1 2.0 Location of Flood Damaged Infrastructure ...................................................................... 1 3.0 Background Information ................................................................................................. 9 4.0 Site Inspections and Recommendations .......................................................................... 9 4.1 Site 1 - Front Road ................................................................................................................ 9 4.1.1 Site Inspection .................................................................................................................. 9 4.1.2 Recommendations ......................................................................................................... 10 4.2 Site 2 - Second Concession Road ........................................................................................ 11 4.2.1 Site Inspection ................................................................................................................ 11 4.2.2 Recommendations ........................................................................................................ -

Amherst Island Guide

Amherst Island is one of the best known spots in Ontario for wintering birding because the island regularly supports large populations of hawks, harriers, owls, shrikes and waterfowl. In spring and autumn Amherst Island can be a great place to see migrating waterfowl, shorebirds and passerines. During the summer months the island is home to a few notable breeding species like Wilson's Phalarope. Virtually all of the land on Amherst Island is privately owned, so most birding is done from the roadside. There are a few properties however, to which land owners kindly allow public access. Below is a list of some of the best birding spots on the island. Directions: To get to Amherst Island, drive about 20 km west of Kingston on Bath Road (aka Loyalist Parkway or Highway 33) to the town of Millhaven. Follow the signs to the Amherst Island ferry dock. At the time of this printing the ferry runs between 6:00 a.m. to 2:00 a.m. daily. It departs Millhaven on the half-hour and the island on the hour. At present there is a $9.00 fee for a round-trip crossing per vehicle. An up to date sailing times can be found on the Ministry of Transportation website (http://www.mto.gov.on.ca/english/traveller/ferry). A. Front Road Front Road runs the length of the island but it is the eastern end of the road between Stella (where the ferry docks) and Lower 40 Foot Road that is most heavily birded. Water views of Stella Bay, Preston Cove and the North Channel can provide views of good numbers of water birds throughout migration and winter. -

Appendix a Project Contact List

Appendix A Project Contact List IMPROVEMENTS TO THE AMHERST ISLAND FERRY DOCKS Stakeholder Mailing List Title First_Name Last_Name Job_Title Company_Name Address_Line_1 City Province Postal_Code MUNICIPAL Mr. Robert Maddocks CAO Loyalist Township 263 Main Street Box 70 Odessa Ontario K0H 2H0 Mr. David MacPherson Public Works Manager Loyalist Township 263 Main Street Box 70 Odessa Ontario K0H 2H0 Mr. Dave Thompson Director of Infrastructure Services Loyalist Township 263 Main Street Box 70 Odessa Ontario K0H 2H0 Mr. Larry Keech CAO/Clerk County of Lennox & Addington 97 Thomas Street East Napanee Ontario K7R 4B9 Mr. Chris Wager Manager, Roads and Bridges County of Lennox & Addington 97 Thomas Street East Napanee Ontario K7R 4B9 EMERGENCY SERVICES Ms. Leslie Jean A/Research Analyst, Business Management Bureau Ontario Provincial Police 777 Memorial Avenue 2nd Floor Orillia Ontario L3V 7V3 Madam/Sir Detachment Commander Ontario Provincial Police 1135 County Road 6 Odessa Ontario K0H 2H0 Chief Paul Charbonneau Director/Chief of Paramedic Services Frontenac Paramedic Services 2069 Battersea Road Glenburnie Ontario K0H 1S0 Director/Chief of Paramedic Services Lennox & Addington Emergency Services 97 Thomas Street East Napanee Ontario K7R 4B9 Chief Fred Stephenson Fire Chief/CEMC Loyalist Township Emergency Services 51 Main Street P.O. Box 70 Odessa Ontario K0H 2H0 FEDERAL GOVERNMENT Sir/Madam Warden Millhaven Institution, Corrections Canada Highway 33, P.O. Box 280 Bath Ontario K0H 1G0 Sir/Madam Warden Bath Institution, Corrections Canada 5775 Bath Road P.O. Box 1500 Bath Ontario K0H 1G0 Mr. Sunil Bajaj Manager, Lands & Economic Development, Environment Aboriginal Affairs and Northern Development Canada Ontario Region, 25 St. -

Amherst Island Ferry Terminals Study G.W.P. 4067

AMHERST ISLAND FERRY TERMINALS STUDY G.W.P. 4067-09-00 TRANSPORTATION ENVIRONMENTAL STUDY REPORT JANUARY 2014 Amherst Island Ferry Terminals Study (G.W.P. 4067-09-00) Preliminary Design and Class Environmental Assessment January 2014 TRANSPORTATION ENVIRONMENTAL STUDY REPORT PRELIMINARY DESIGN AND CLASS ENVIRONMENTAL ASSESSMENT GROUP ‘B’ G.W.P. 4067-09-00 Amherst Island Ferry Terminals Study Loyalist Township, County of Lennox and Addington Prepared by: Joanne Wang, MES Bob Bird Consultant Environmental Planner Consultant Senior Environmental Planner URS Canada Inc. URS Canada Inc. Ce document hautement spécialisé n’est disponible qu’en Anglais en vertu du règlement 671/92 qui en exempte l’application de la Loi sur les services en français. Pour de l’aide en français, veuillez communiquer avec Heather Edwardson, ministère des Transports, au (905) 704-2210. JANUARY 2013 i Amherst Island Ferry Terminals Study (G.W.P. 4067-09-00) Preliminary Design and Class Environmental Assessment January 2014 The Public Record To provide opportunities for public review, copies of this Report are available at the following locations: Ministry of Transportation Amherst Island Public School Eastern Region 5955 Front Road 1355 John Counter Boulevard Stella, ON K0H 2S0 Kingston, ON K7L 5A3 Loyalist Township Amherstview Public Library Clerk’s Office 322 Amherst Drive 263 Main Street Amherstview, ON K7N 1S9 Odessa, ON K0H 2H0 Interested persons are encouraged to review this document by the end of the public review period. If after consulting with the Project Team, you have unresolved concerns, you have the right to request of the Minister of the Environment (Ferguson Block, 11th Floor, 77 Wellesley Street West, Toronto, ON, M7A 2T5) a Part II Order (i.e. -

Short-Eared Owl (Asio Flammeus) Population Monitoring in Southern and Eastern Ontario Summer 2003

Short-eared Owl (Asio flammeus) Population Monitoring in Southern and Eastern Ontario Summer 2003 Leslie M. Hunt Project Director The Migration Research Foundation and Marcel A. Gahbauer Research Director The Migration Research Foundation November 2004 Short-eared Owl (Asio flammeus) Population Monitoring in Southern and Eastern Ontario Summer 2003 ABSTRACT The North American Short-eared Owl (Asio flammeus) population has been steadily declining since the mid 1960s. In southern Ontario, the Short-eared Owl was once the most frequently encountered owl, but has become very scarce and localized. It has recently been recommended for Special Concern status in Ontario. Little is known about the species’ breeding sites or movements, and there is debate as to whether the species deserves a higher conservation status. In order to accurately evaluate population status and effectively guide recovery efforts, The Migration Research Foundation (MRF) conducted a survey of the breeding population in southern and eastern Ontario. MRF, with the help of landowners and volunteers from the birding community, located and monitored nest sites, mapped nesting habitat, and set traps for the purpose of banding and blood-sampling adult owls. Approximately 40 historical or suitable nest sites were monitored, with evidence of Short-eared Owls being present found at only five. No owls were successfully trapped. 2 TABLE OF CONTENTS 1. INTRODUCTION……………………………………………………………….. 1 2. OBJECTIVES……………………………………………………………………. 3 3. METHODS………………………………………………………………………. 4 4. RESULTS………………………………………………………………………..