Company Overview 2007 Table of Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

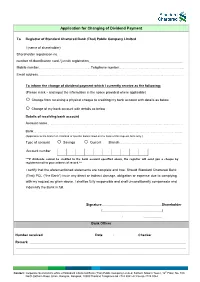

Application for Changing of Dividend Payment

Application for Changing of Dividend Payment To Registrar of Standard Chartered Bank (Thai) Public Company Limited I (name of shareholder) Shareholder registration no. number of identification card / juristic registration Mobile number………………………………………………….……….....Telephone number…………………..……………………………………….……………….. Email address……………………………………………………………………………………………………………….……………………………………………………………… To inform the change of dividend payment which I currently receive as the following: (Please mark and input the information in the space provided where applicable) Change from receiving a physical cheque to crediting my bank account with details as below Change of my bank account with details as below Details of receiving bank account Account name………………………………………………………………………………………………………………………………………………………..…….….. Bank………………………………………………………………………………………………………………………………………………………..……………………….... (Applicable to the branch in Thailand of specific banks listed on the back of this request form only.) Type of account Savings Current Branch…………………………………………………….……………………. Account number ***If dividends cannot be credited to the bank account specified above, the registrar will send you a cheque by registered mail to your address of record.*** I certify that the aforementioned statements are complete and true. Should Standard Chartered Bank (Thai) PCL (“the Bank”) incur any direct or indirect damage, obligation or expense due to complying with my request as given above. I shall be fully responsible and shall unconditionally compensate and indemnify the Bank in full. Signature Shareholder ( ) / / Bank Officer Number received Date / / Checker Remark Contact: Corporate Secretariat’s office of Standard Chartered Bank (Thai) Public Company Limited, Sathorn Nakorn Tower, 12th Floor, No. 100 North Sathorn Road, Silom, Bangrak, Bangkok, 10500 Thailand Telephone 66 2724 8041-42 Fax 66 2724 8044 Documents to be submitted for changing of dividend payment (All photocopies must be certified as true) For Individual Person 1. -

Gauging the Potential in Thai Banking* Introduction Overview

Financial Services Back on the investment radar: Gauging the potential in Thai banking* Introduction Overview The Thai banking sector is attracting increasing international • Economy set to rebound as confidence returns following interest as the market opens up to foreign investment and the return to democracy. the return to democracy helps to reinvigorate consumer • Banking sector recording steady growth. Strong confidence and demand. opportunities for the development of retail lending. Bad debt ratios have gradually declined and the balance • Foreign banks account for 12% of the market by assets and sheets of Thailand’s leading banks have strengthened 10% of lending by value.7 Strong presence in high-value considerably since the Asian financial crisis of 1997.1 niche segments including auto finance, mortgages and The moves to Basel II and IAS 39 are set to enhance credit cards. transparency and risk management within the sector, while accelerating the demand for foreign capital and expertise. • Organic entry strategies curtailed by licensing and branch opening restrictions. Reforms already in place include the ‘single presence’ rule, which by seeking to limit cross-ownership of the country’s • Acquisition of minority stakes in existing banks proving banks is leading to increased consolidation and the opening increasingly popular. Ceiling on foreign holdings set to be up of sizeable holdings for new investment. The Financial raised to 49%, though there are no firm plans to allow Sector Master Plan and forthcoming Financial Institution outright control. Business Act (2008), which will come into force in August • Demand for capital and foreign expertise is encouraging 2008, could ease restrictions on branch openings and the more domestic banks to seek foreign investment, especially size of foreign investment holdings. -

Siam City Bank Public Company Limited

Tender Offer for Securities Of Siam City Bank Public Company Limited By The Offeror Thanachart Bank Public Company Limited 17 September 2010 – 19 November 2010 (Business day only) 9.00 a.m. – 4.00 p.m. Tender Offer Preparer and Agent Thanachart Securities Public Company Limited -Translation- TNS_IB 098/2010 14 September 2010 Subject : The submission of the Tender Offer Form for securities of Siam City Bank Public Company Limited To : The Secretary –General of the Office of the Securities and Exchange Commission The President of the Stock Exchange of Thailand The Directors and Shareholders of Siam City Bank Public Company Limited Enclosed : The tender offer form for securities of Siam City Bank Public Company Limited (Form 247-4) Pursuant to Thanachart Bank Public Company Limited (“Tender Offeror”) offers to tender securities of Siam City Bank Public Company Limited (“SCIB” or “the Company”) from all minority shareholders at the offer price of 32.50 Baht per share for the purpose of delist SCIB shares from listed securities in the Stock Exchange of Thailand. In addition, the Shareholders’ Meeting of SCIB has resolved to approve the delisting of securities of SCIB from listed securities in the Stock Exchange of Thailand on 5 August 2010 and the SET has approved an application for voluntary delisting of SCIB shares on 27 August 2010. Thanachart Securities Public Company Limited, a tender offer preparer, is pleased to submit the Tender Offer Form (Form 247-4) for securities of the Company to the Securities and Exchange Commission, the Stock Exchange of Thailand, the Company, and the Shareholders of the Company as a supporting document for consideration. -

Pakdee Paknara Partner

Pakdee Paknara Partner Pakdee is a Partner at The Capital Law Office with over 20 years of experience in mergers and acquisitions, power and energy projects, real estate and construction, property funds, international trade, telecommunications, computer technology and software licensing, government bidding and tax-related transactions. He has advised domestic and international clients on a wide variety of matters, and is specialized in preparation of documentation for complex commercial transactions, including supply, purchase and sale, service, management agency and employment agreements. Education M.Sc. in Taxation, Prior to joining The Capital Law Office in 2017, Pakdee was a partner of a Golden Gate University, 1994 leading law firm in Bangkok as a head of the commercial and international trade and tax practice. LL.B. Chulalongkorn University, 1987 Selected Transactional Experience Languages Mergers & Acquisitions Thai, English • Representing Thailand’s Government Savings Bank (GSB) in the Accolades sale of its 25% interest in issued share capital of Thanachart Fund M&A Management Company Limited (TFUND), to Prudential Corporation Highly Regarded by Holdings Limited (Prudential), an affiliate of Eastspring Investments IFLR1000 (2019-2020) (Singapore) Limited. At closing, GSB sold its TFUND 25% interest, and Thanachart Bank Public Company Limited (TBANK) sold its TFUND Leading Lawyer by 25.1% interest; Prudential owned 50.1% of TFUND, and TBANK IFLR1000 (2010-2016) retained a 49% interest. Transaction value: approximately THB 2.1 Leading Lawyer by billion (approximately USD 69.1 million). Asialaw Profiles 2016 • Representing Thanachart Capital Public Company Limited and Recommended Lawyer by Thanachart Bank Public Company Limited in a business merger Legal 500 Asia Pacific with TMB Bank Public Company Limited (TMB Bank) to become the th (2009-2014) 6 largest bank in Thailand. -

KTB: Krung Thai Bank Public Company Limited | Annual Report

A N U L R E P O T 2 0 1 3 K r u n g h a i B k c l . TRANS FORMA TION 35 Sukhumvit Road, Klong Toey Nua Subdistrict, Wattana District, Bangkok 10110 Tel : +662 255-2222 Fax : +662 255-9391-3 KTB Call Center : 1551 Swift : KRTHTHBK http://www.ktb.co.th Annual Report 2013 K T B T r a n s f o r m a t i o n This annual report uses Green Read paper for low-eye strain and is printed with soybean ink that reduces carbon dioxide emission and has light weight for less energy consumed in delivery. Produced by : Business Risk Research Department Risk Management Sector Risk Management Group Krung Thai Bank Pcl. Designed by : Work Actually Co., Ltd. Printed by : Plan Printing Co., Ltd. Transformation…for a Sustainable Growth KTB has transformed its internal operation process and improve people capability for greater efficiency in customer services and business expansion under accurate and efficient risk management that will lead to enhanced competitiveness and readiness to make a sustainable leap together with customers, society, shareholders and stakeholders. K T B T r a n s f o r m a t i o n KTB e-Certificate ของ่าย ได้เร็ว ขอหนังสือรับรอง นิติบุคคล การประกอบธุรกิจ คนต่างด้าว สมาคมและหอการค้า 4 KTB สินเชื่อ SME เพื่อรับงานภาครัฐ หนังสือคํ้าประกันทันใจ แค่ 1 วัน Net Free Zero รับได้เลย จาก KTB netbank แบบอั้นๆ หลบไปเลย....Net Free Zero ค่าธรรมเนียม ฟรี ไม่มีอั้น ตัวจริง! มาแล้ว Annual Report 2013 Krung Thai Bank Pcl. สินเชื่อกรุงไทย 3 สบาย สินเชื่อบุคคล ที่ ให้ ชีวิต มีแต่เรื่อง สบายๆ บริการโอนเงินต่างประเทศ มุมไหนใน โลก ก็ โอนถึง ใน 1 วัน 5 สินเชื่ออเนกประสงค์ -

1 Pricewaterhousecoopers Thailand 2 AIA Company Limited 3 AIA

Certified Companies of Thailand's Private Sector Collective Action Coalition Against Corruption No. Membership Company 1 PricewaterhouseCoopers Thailand 2 AIA Company Limited 3 AIA Company Limited (Non-Life Insurance) Thailand Branch 4 Siemens Limited Thailand 5 Somboon Advance Technology Public Company Limited 6 S & P Syndicate Public Company Limited 7 Siam Cement Public Company Limited 8 KPMG Phoomchai Business Advisory Company Limited 9 Intouch Holdings Public Company Limited 10 KasikornBank Public Company Limited 11 Kasikorn Asset Management Company Limited 12 Kasikorn Securities Company Limited 13 Bangchak Petroluem Public Company Limited 14 TISCO Financial Group Public Company Limited 15 TISCO Bank Public Company Limited 16 TISCO Securities Company Limited 17 TISCO Asset Management Company Limited 18 Bank of Ayudhya Public Company Limited 19 KPMG Phoomchai Audit Limited 20 KPMG Phoomchai Tax Limited 21 The Erawan Group Public Company Limited 22 GlaxoSmithKline (Thailand) Company Limited 23 Phatra Capital Public Company Limited 24 Krungsri Asset Management Company Limited 25 Krungsri Factoring Company Limited Certified Companies of Thailand's Private Sector Collective Action Coalition Against Corruption No. Membership Company 26 Ayudhya Capital Auto Lease Public Company Limited 27 Krungsri Securities Public Company Limited 28 Siam Realty and Services Company Limited 29 Ayudhya Development Leasing Company Limited 30 Ayudhya Capital Services Company Limited 31 Krungsri Ayudhya AMC Limited 32 Krungsriayudhya Card Company Limited 33 -

1 Banpu Public Company Limited 2 Bualuang Securities Public

Signatory Companies of Thailand's Private Sector Collective Action Coalition Against Corruption's Declaration of Intent No. Company 1 Banpu Public Company Limited 2 Bualuang Securities Public Company Limited 3 Bangkok Bank Public Company Limited 4 BBL Asset Management Company Limited 5 BBV Systems Company Limited 6 The Bangchak Petroleum Public Company Limited 7 Bumrungrad Hospital Public Company Limited 8 Central Plaza Hotel Public Company Limited 9 CIMB Thai Bank Public Company Limited 10 Central Pattana Public Company Limited 11 Total Access Communication Public Company Limited 12 Eastern Water Resources Development and Management Public Company Limited 13 Electricity Generating Public Company Limited 14 Kasikornbank Public Company Limited 15 Kiatnakin Bank Public Company Limited 16 KPMG Phoomchai Business Advisory Company Limited 17 Krung Thai Bank Public Company Limited 18 Kang Yong Electric Public Company Limited 19 MBK Public Company Limited 20 MCOT Public Company Limited 21 MFEC Public Company Limited 22 Nation Multimedia Group Public Company Limited 23 Pfizer (Thailand) Limited 24 Phatra Capital Public Company Limited 25 Pranda Jewelry Public Company Limited Signatory Companies of Thailand's Private Sector Collective Action Coalition Against Corruption's Declaration of Intent No. Company 26 PTT Public Company Limited 27 PTT Exploration and Production Public Company Limited 28 PricewaterhouseCoopers Thailand 29 Sabina Public Company Limited 30 Somboon Advance Technology Public Company Limited 31 Siam Commercial Bank Public Company -

Collateral Deposit & Payment by Bill Payment Service at the Bank No

Collateral Deposit & Payment by Bill Payment Service at the Bank For your convenience, the “Bill Payment of Goods and Services” currently available at 9 banks: Bangkok Bank, Krung Thai Bank, Krungsri, Kasikorn Bank, CIMB, Siam Commercial Bank, TMB, Thanachart Bank, and UOB can be used to deposit collateral and make payments to us. You can use it by (1) payment over the counter at a bank branch, (2) via their ATM, Auto Telephone Banking, or (3) their Internet or Mobile Banking. 1) Bill payment over the counter at a bank branch. Complete and submit a pay-in slip provided by us along with your payment at the bank. You can download the form from our website www.poems.in.th under: Download >> Form >> Pay-in Slip. For BBL, KTB, Krungsri, Kasikorn, SCB, TBank, and UOB you can also use the Bill Payment Slip provided by the bank. 2) Bill payment via ATM or Automatic Telephone Banking. In general, you need to look for the Bill Payment Service menu. Use the correct company code with your bank, payment reference 1, and 2 codes from the tables below. Please refer to or download the User’s Guide from each bank from our website www.poems.in.th under: Learning Center >> Investors Guide >> Bill Payment User Guide. Bill Payment Recipient Company Code for Payment at a Bank Branch, ATM, Internet, and Mobile Banking Bill Payment Channel (Service Code, Comp Code, BP Code) No. Banks Payment at a Bank Branch / Internet Banking & ATM Mobile Banking 1 TMB Bank Comp Code: 0914 Comp Code: 0504 2 Bangkok Bank Comp Code: 50234 / Service Code: PST 3 Kasikorn Bank Comp Code: 33826 4 Krung Thai Bank Comp Code: 5346 5 Krungsri Comp Code: 24155 6 CIMB Thai Comp Code: PST / Service Code: PST034 7 Siam Commercial Bank Comp Code: 0016 8 Thanachart Bank Com Code: C100 / Service Code : 3145 9 UOB BP Code: 3300 *For TMB, our Comp Code is different at the bank branch (0914) and at the ATM (0504) Payment Reference 1 is your 5 digit trading account number with us. -

BAY: Bank of Ayudhya Public Company Limited | Annual Report

ANNUAL REPORT 2013 GROWING IN STRENGTH WELCOMING MUFG/BTMU CONTENTS Message from the Chairman 4 Message from the Chief Executive 6 Officer 000 Our Organization Organizational Structure 11 Board of Directors 12 Senior Management 14 Financial Highlights 16 Awards and Recognition 18 Operating Environment 27 GOLDEN YEAR:18 KRUNGSRI HONORED WITH KEY AWARDS Competitive Capability 31 Risk Factors and Risk Management 73 Corporate Governance 85 Collective Action Coalition 99 Against Corruption (CAC) 000 Policy and Measures against 100 Insider Information 000 Internal Control and Internal 100 33 BANK SLATE: Audit System ASIA’S FIRST 000 FULLY-INTEGRATED BANKING APP A HIT Shareholding and Management 105 Structure 000 Corporate Social Responsibility 145 Financial Reporting and Financial 153 Statements 000 General Information 254 The Bank’s Securities 255 Group of Companies 259 Distribution Network Directory 261 SIMPLY46 BETTER: Summary of Specified Items per 271 452 NEW ATMS INSTALLED Form 56-2 NATIONWIDE MESSAGE FROM THE CHAIRMAN MESSAGE FROM THE CHAIRMAN its stake in Krungsri. The Ratanarak Group The acquisition of Krungsri will support BTMU’s understood the reasons behind GE’s decision strategy of expansion in Southeast Asia. and offered its full support. However, this Among MUFG/BTMU’s subsidiaries, Krungsri brought Krungsri to the crossroads once again, is the largest investment in Asia, and the requiring its core shareholder to consider second-largest stake globally after US-based a more permanent partnership. UnionBanCal Corporation. At this -

CAMPAIGN for BIG MEMBERS 1. This “ June 2X Bonus Re

TERMS & CONDITIONS – “June 2X Bonus Regional All Banks Campaign” CAMPAIGN FOR BIG MEMBERS 1. This “June 2X Bonus Regional All Banks Campaign” [“Campaign”] is organised by BIGLIFE Sdn. Bhd. [“Organiser”]. 2. By participating in this Campaign, all participants [“Participants”] will be deemed to have read, understood and expressly agreed to be bound by the Terms & Conditions of this Campaign as stated herein and any additional terms and conditions stipulated by the Organiser (as may be applicable) including the decisions of the Organiser in all matters related thereto. 3. The Campaign is open to all BIG Members who hold valid credit cards and/or debit cards and/or trading accounts offered by the Organiser’s partners listed below (“Organiser’s Partners”):- (A) Malaysia (i) Affin Bank Berhad, (ii) Affin Islamic Bank Berhad, (iii) Alliance Bank Berhad, (iv) AmBank (M) Berhad, (v) AmBank Islamic Berhad, (vi) Bank Simpanan Nasional, (vii) CIMB Bank Berhad, (viii) Citibank Berhad, (ix) Hong Leong Bank Berhad, (x) HSBC Bank Malaysia Berhad, (xi) Malayan Banking Berhad, (xii) Public Bank Berhad, (xiii) Rakuten Trade Sdn Bhd, (xiv) RHB Bank Berhad, (xv) RHB Investment Bank, (xvi) Standard Chartered Bank Malaysia Berhad, and (xvii) UOB Bank Berhad. (B) Thailand (i) Ayudhya Capital Services Co. Ltd., (ii) Citibank N.A, (iii) Kasikronbank PLC., (iv) Krungsriayudhya Card Co., Ltd., (v) Krungthai Card PLC., (vi) Thanachart Bank PLC., (vii) TMB Bank PLC., (viii) Siam Commercial Bank PLC., (ix) Bangkok Bank PLC., (except AirAsia Bangkok Bank Credit Card, which is excluded from participating in this Campaign) (x) Industrial and Commercial Bank of China (Thai) PLC. -

Management Discussion and Analysis for the Year Ending 31 December 2010 (Audited Financial Statements)

Management Discussion and Analysis For the year ending 31 December 2010 (Audited Financial Statements) Thanachart Capital Public Company Limited Tel: 0 2217 8000, 0 2217 8444 Fax: 0 2217 8312 Website: www.thanachart.co.th Investor Relations Email: [email protected] Tel: 0 2613 6107 12 Thanachart Capital Public Company Limited Management Discussion and Analysis (Audited Financial Statements) Major Events 1. Thanachart Bank Public Company Limited purchased ordinary shares of Siam City Bank Public Company Limited in order to conduct an entire business transfer. On 9 April 2010, the share purchase from Financial Institution Development Fund (FIDF) has been successful. A tender offer was conducted for general public shareholders in June and November 2010 at a price of THB 32.50 per share (the same price that Thanachart Bank paid to FIDF). Consequently, Thanachart Bank’s shareholding was 99.95 percent of Siam City Bank’s total issued and paid up shares. Thanachart Bank, together with Siam City Bank, submitted the entire business transfer plan to the Bank of Thailand. The plan is currently under the review and evaluation of the Bank of Thailand. The entire business transfer is expected to be completed within the year 2011, after which the Bank will return banking license of Siam City Bank to the Bank of Thailand. 2. On 8 – 19 April 2010, Thanachart Bank has increased capital in the amount of 3,579,045,631 shares at a price of THB10 per share, an equivalent of THB 35,790 million, in proportion to the existing shareholding structure. As a result, Thanachart Bank has THB 55,136,649,030 of total issued and paid-up shares. -

Total Factor Productivity of Commercial Banks in Thailand

International Journal of Business and Society, Vol. 15 No. 2, 2014, 215 - 234 TOTAL FACTOR PRODUCTIVITY OF COMMERCIAL BANKS IN THAILAND Supachet Chansarn♣ Bangkok University ABSTRACT This study employed growth accounting equation to examine the total factor productivity of 14 commercial banks in Thailand during 2000 – 2009. The findings revealed that commercial banks in Thailand on average had low and very volatile total factor productivity with the average total factor productivity growth rate ranging from -13.35 – 10.06 percent per annum. In terms of individual bank, the findings revealed that most of commercial banks had the negative average total factor productivity growth rate during the study period, implying their lower productivity. In addition, the findings suggested that there were four factors which significantly determined the total factor productivity growth of commercial banks. They were credit risk as measured by the percentage of loan to total asset, management quality as measured by the percentage of non-interest expense to total asset, diversification as measured by the percentage of non-interest income to total asset and capital adequacy as measured by the percentage of owners’ equity to total asset. Furthermore, small commercial banks were found to have the highest total factor productivity growth whereas large banks were found to have the lowest one. Keywords: Total Factor Productivity; Commercial Bank; Banking Sector; Thailand. 1. INTRODUCTION Commercial banks have long been considered as the most important financial intermediaries in Thailand. In 2009, more than 7.1 trillion baht of deposits or deposits equivalent was accepted by Thailand’s commercial banks. This figure was approximately accounted for 79 percent of Thailand’s gross domestic product in 2009 (Bank of Thailand, 2010).