L Brands, Inc (LB) Memo Growth Potential Demonstrated by Solid Financial Data Great Management Team with Effective

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Copyrighted Material

15_787434 bindex.qxp 6/13/06 6:45 PM Page 314 INDEX A Alexander McQueen, 108, 140 Aaron Faber, 192–193 Alfred Dunhill, 199 Aaron’s, 289–290 Allan & Suzi, 87 ABC Carpet & Home, 12, 16, 21–22, American Express, 49 105, 108, 244, 249 American Girl Place, 93–94 Abercrombie & Fitch, 167 Amish Market, 173 About.com, 35 Amore Pacific, 117, 238–239 Accessories, 131–135 Amsterdam Avenue, 87 Accommodations, 67–77 Andy’s Chee-Pees, 216 chains, 76–77 An Earnest Cut & Sew, 189–190 dining deals, 57–58 Ann Ahn, 149 four-star, 73 Anna Sui, 137 luxury, 71–73 Anne Fontaine, 155 promotions, 53 The Annex/Hell’s Kitchen Flea Market, promotions and discounts, 69–71 267–268 tax, 70 Ann Taylor, 86, 167 unusual locations, 75–76 Ann Taylor LOFT, 90, 168 Active sportswear, 135–136 Anthropologie, 105, 117 Add, 131 Antiques, 275–278 Adidas, 21, 135 Anya Hindmarch, 184 Adrien Linford, 102, 255 AOL CityGuide New York, 35 Adriennes, 151 The Apartment, 255, 263 Aerosoles, 207 APC, 186–187 AfternoonCOPYRIGHTED tea, 18, 66–67 A Pea In The MATERIAL Pod, 198 Agatha Ruiz de la Prada, 255 Apple Core Hotels, 76 Airport duty-free stores, 55–56 Apple Store, 116, 264 Akris, 139 April Cornell, 22, 88 Alcone Company, 109–110, 224–225 Arcade Auctions, Sotheby’s, 275 314 15_787434 bindex.qxp 6/13/06 6:45 PM Page 315 Index 315 Armani Casa, 245 Barneys Co-Op, 12, 110, 159 Arriving in New York, 44–45 Barneys New York, 160, 198, 199, Ascot Chang, 85, 199 212, 256 A Second Chance, 307 cafe, 63 Atlantic Avenue (Brooklyn), antiques Barneys Warehouse Sale, 110 shops, 277 Barolo, 67 Au Chat Botte, 156–157 Bathroom accessories, 263 Auctions for art and antiques, 269–275 Bauman Rare Books, 147 Auto, 187, 255–256 Beacon’s Closet (Brooklyn), 128 Aveda, 100, 219–220 Beauty products, 218–240 Aveda Institute, 220, 239 bath and body stores, 228–230 Avon Salon & Spa, 220, 239 big names, 219–223 A. -

2020 Career Fair Organizations Organization Career Areas Position

2020 Career Fair Organizations Organization Career Areas Position Types Website 21st Century Home Healthcare LLC Health Fields Full-time, Part-time 21st Century Home Healthcare LLC 5B's Embroidery and Screen Print Customer Service, Manufacturing, Retail Full-time, Part-time http://5bs.com/employment/ Abercrombie & Fitch- Home Office Campus Stores Retail Part-time anfcareers.com Absolute Love Learning Center Education/Child Development Full-time, Part-time https://www.facebook.com/Absolute-Love- Learning-Center-162109230484126/ Acloche Customer Service, Health Fields, Management, Manufacturing, Full-time www.acloche.com Office Administration Acloche LLC Manufacturing Full-time Acloche LLC AFMETCAL (Dept of Defense; USAF) Computer Programing/Information Technology Full-time, Internship or Co-op https://www.wpafb.af.mil/afmetcal/ Air Force Primary Standards Laboratory Engineering/Architecture/Construction Full-time www.bionetics.com AK Steel Corporation Manufacturing Full-time aksteel.com Alene Candles Forensics/Laboratory, Manufacturing Full-time, Contract www.alene.com Allied Machine & Engineering Corp Engineering/Architecture/Construction Full-time www.alliedmachine.com Alps LTD Human Services/Social Work Full-time, Part-time www.alpsohio.com Amada Senior Care Health Fields Full-time, Part-time https://www.amadaseniorcare.com/columbus- senior-care/ American Electric Power Communication/Journalism/Digital Media, Computer Full- Time aep.com Programming/Information Technology, Customer Service, Engineering/Architecture/Construction, Human -

Spring 2017 • May 7, 2017 • 12 P.M

THE OHIO STATE UNIVERSITY 415TH COMMENCEMENT SPRING 2017 • MAY 7, 2017 • 12 P.M. • OHIO STADIUM Presiding Officer Commencement Address Conferring of Degrees in Course Michael V. Drake Abigail S. Wexner Colleges presented by President Bruce A. McPheron Student Speaker Executive Vice President and Provost Prelude—11:30 a.m. Gerard C. Basalla to 12 p.m. Class of 2017 Welcome to New Alumni The Ohio State University James E. Smith Wind Symphony Conferring of Senior Vice President of Alumni Relations Russel C. Mikkelson, Conductor Honorary Degrees President and CEO Recipients presented by The Ohio State University Alumni Association, Inc. Welcome Alex Shumate, Chair Javaune Adams-Gaston Board of Trustees Senior Vice President for Student Life Alma Mater—Carmen Ohio Charles F. Bolden Jr. Graduates and guests led by Doctor of Public Administration Processional Daina A. Robinson Abigail S. Wexner Oh! Come let’s sing Ohio’s praise, Doctor of Public Service National Anthem And songs to Alma Mater raise; Graduates and guests led by While our hearts rebounding thrill, Daina A. Robinson Conferring of Distinguished Class of 2017 Service Awards With joy which death alone can still. Recipients presented by Summer’s heat or winter’s cold, Invocation Alex Shumate The seasons pass, the years will roll; Imani Jones Lucy Shelton Caswell Time and change will surely show Manager How firm thy friendship—O-hi-o! Department of Chaplaincy and Clinical Richard S. Stoddard Pastoral Education Awarding of Diplomas Wexner Medical Center Excerpts from the commencement ceremony will be broadcast on WOSU-TV, Channel 34, on Monday, May 8, at 5:30 p.m. -

Black Magic NEW YORK — Carolina Herrera Is out to Prove That Men Can Be Every Bit As Stylish As Women with Chic for Men, Her Third Men’S Scent

PRADA’S DEBT PLAN/2 GAP CEDES GERMANY TO H&M/2 WWWDomen’s Wear Daily • The Retailers’FRIDAY Daily Newspaper • February 6, 2004 • $2.00 Beauty Black Magic NEW YORK — Carolina Herrera is out to prove that men can be every bit as stylish as women with Chic for Men, her third men’s scent. The fragrance, which also borrowed inspiration from the simplicity of classic black-and-white photography, will roll out in Saks Fifth Avenue doors at the end of this month, and enter the rest of its 200-door distribution in September. It could do $3.5 million at retail in its first year. For more, see page 13. Luxury on a Roll: Double-Digit Gains for Third Straight Month By Jennifer Weitzman arrival of new spring lines. Chilly Comparable-Store Sales Index and Ross Tucker weather and gift-card redemptions came in with a 5.9 percent increase BY BRYN KENNY NEW YORK — Luxury’s momentum also drove traffic. for the month, its highest gain since continued in January while In turn, retailers reported strong September 2003 when it also consumers were also lured into comparable-store gains. The showed a 5.9 percent increase. stores by clearance sales and the Goldman Sachs Retail Composite See Strong, Page 20 PHOTO BY GEORGE CHINSEE; STYLED 2 WWD, FRIDAY, FEBRUARY 6, 2004 WWDFRIDAY Prada Plans to Halve Debt Beauty By Courtney Colavita Patrizio lion euro, or $82 million, tax re- Patrizio bate from the Italian government BEAUTY Bertelli MILAN — This may or may not Bertelli would enable Prada to cut its Coty Beauty is hoping for back-to-back hits with the launch of a second be the year of Prada’s long- debt to 290 million euros, or 12 Celine Dion fragrance this spring called Celine Dion Parfum Notes. -

The UK Sports - and Underwear Market

The UK Sports - and Underwear Market Bachelor of International Marketing th 16 May 2011 Written by: Iyoel Tesfai Mathilde Melgaard Nina Elvestad Nina Kristin Grav This paper is done as a part of the undergraduate program at BI Norwegian Business School. This does not entail that BI Norwegian Business School has cleared the methods applied, the results presented, or the conclusions drawn. 1 International Marketing Consultancy Project Module ACKNOWLEDGEMENTS This report is an International Marketing Consultancy Project for students at Leeds Metropolitan University, in addition to being a market/commercial report for Pierre Robert. Firstly, we wish to thank our supervisor, Mr. Peter Williams, for his great passion and support during the process of assembling this report. Secondly we wish to show our greatest gratitude towards Pierre Robert Group and our contact person Mr. Erik Aass. Thank you for all your support and for giving us the opportunity to write an interesting and challenging paper. Leeds Metropolitan University 16th May 2011 _________________________ _________________________ Nina Kristin Grav - 77087469 Mathilde Melgaard - 77087403 2 International Marketing Consultancy Project Module _______________________ _________________________ Nina Elvestad - 77087438 Iyoel Tesfai - 77087477 Executive summary Pierre Robert Group is a Norwegian company, which specialises in regular underwear, in addition to sports underwear. The company is currently represented in Sweden and Finland, as well as in their domestic market. Pierre Robert Group wishes to explore the possibilities for a future expansion into the UK sports- and/or underwear market. The purpose of this report is to explore the UK sports- and underwear market in order to ascertain the most appropriate strategy for Pierre Robert, if they were to enter the UK. -

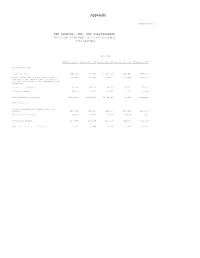

Appendix Limitedbran

Appendix EXHIBIT 12 ---------- THE LIMITED, INC. AND SUBSIDIARIES RATIO OF EARNINGS TO FIXED CHARGES (Thousands) Year Ended ------------------------------------------------------------------------------------ February 3, 2001 January 29, 2000 January 30, 1999 January 31, 1998 February 1, 1997 ---------------- ---------------- ---------------- ---------------- ---------------- Adjusted Earnings ----------------- Pretax earnings $758,905 $831,759 $2,351,494 $390,653 $675,088 Portion of minimum rent ($653,820 in 2000, 217,940 223,987 229,747 246,162 237,419 $671,960 in 1999, $689,240 in 1998, $738,487 in 1997, and $712,258 in 1996) representative of interest Interest on indebtedness 58,244 78,297 68,528 68,728 75,363 Minority interest 69,345 72,623 63,616 55,610 45,466 ------------ ------------ ------------ ------------ ------------ Total earnings as adjusted $1,104,434 $1,206,666 $2,713,385 $761,153 $1,033,336 ============ ============ ============ ============ ============ Fixed Charges ------------- Portion of minimum rent representative of interest $217,940 $223,987 $229,747 $246,162 $237,419 Interest on indebtedness 58,244 78,297 68,528 68,728 75,363 ------------ ------------ ------------ ------------ ------------ Total fixed charges $276,184 $302,284 $298,275 $314,890 $312,782 ============ ============ ============ ============ ============ Ratio of earnings to fixed charges 4.00x 3.99x 9.10x 2.42x 3.30x ============ ============ ============ ============ ============ Exhibit 13 6 FINANCIAL SUMMARY (Millions except per share amounts, -

JOURNAL-NOTICE-Novem

Vol. 16 - No. 22 Belmopan, November 4, 2016 1 INTELLECTUAL PROPERTY JOURNAL BELIZE INTELLECTUAL PROPERTYO OFFICE BEL P Vol. 16 - No. 22 Belmopan, November 4, 2016 2 BELIPO’S MISSION STATEMENT “To build a modern intellectual property system that values and protects the vibrant creative culture of Belize” Vol. 16 - No. 22 Belmopan, November 4, 2016 3 CONTENTS Page Numbers TRADEMARKS: APPLICATIONS FOR TRADEMARK REGISTRATION ………………….…………………………………………….…… 4-56 NOTICES OF TRADEMARK RENEWAL ………………………………….……………………………………………….... 57-78 NOTICES OF ASSIGNMENT……………………………………………………………………………….………………...… 79-80 NOTICE OF CHANGE OF ADDRESS OF PROPRIETOR ………………….……………………..……………………….….. 81-83 NOTICE OF CHANGE OF NAME OF PROPRIETOR ……………………………………….………………………….….….. 84 NOTICE OF RECORDAL OF AGENT AND ADDRESS FOR SERVICE………………………………………….……..…… 85 NOTICE OF MERGER……………………………………………………………………………………………………………. 86 NOTICE OF PUBLICATION CORRECTION…………………………………………………………………………….……. 87 NOTICE OF AMENDMENT……………………………………………………………………………………………………. 88 NOTICES OF TRADEMARK REGISTRATIONS………………………………………………………………..….….…. …. 89-92 INDUSTRIAL DESIGN: NOTICE OF RENEWAL OF INDUSTRIAL DESIGN………………………………………………………………………… 93 PATENTS: NOTICE OF CHANGE OF AGENT AND ADDRESS FOR SERVICE………………………………………………………… 94 NOTICE OF PATENT GRANT……………………………………………………………………………………………….. .. 95-96 NOTE: CFE - International Classification of the Figurative Elements of Marks under the Vienna Agreement (Sixth Edition) __________ …________ Vol. 16 - No. 22 Belmopan, November 4, 2016 4 APPLICATIONS FOR TRADEMARK REGISTRATION -

E-Commerce Lingerie, Notre Analyse

http://www.capitaine-commerce.com E-commerce lingerie, notre analyse Par Ergonomiks, dimanche 6 avril 2008 à 22:34 :: Revues de site :: #578 :: rss Nous sommes persuadés que la lingerie est un produit encore plus difficile à vendre que les autres vêtements car non seulement l’ajustement doit être parfait mais en plus, le produit doit concilier confort, maintien et séduction. Cependant, une fois ces nombreux obstables à l’achat éliminés (pas d’essayage immédiat, beaucoup plus de voyeurs que d’acheteurs, impossible de toucher la matière, crainte des retours, du cadeau qui ne plait pas, etc.), la vente se fait plus facilement que pour d’autres produits (confort de l’essayage à domicile, achat d’une parure complète et produits annexes, fidélité à l’enseigne si satisfaction, relation privilégiée des clients avec les marques/l’enseigne, retours faciles, etc.). Ces freins et ces facilitateurs constituent notre grille d’analyse dans laquelle nous allons passer quelques sites au crible. Notre sélection de sites sera bien sûr restrictive car nous ne souhaitons pas vous ennuyer trop longtemps sur un sujet aussi ascétique. La grille sera divisée en thèmes que nous vous invitons à commenter (car on est très Web 2.0 chez Capitaine Commerce). Nous allons publier au rythme d'un chapitre par semaine. Sommaire Introduction 1 : Frais de port et retours 2 : Démonstration produit 3 : Tailles/disponibilité/Réassurance 4 : Bien présenter les coloris produit 5 : Valoriser le produit 6 : Ventes additionnelles avec produits coordonnés et associés 7 : Les fiches multi-produits 8 : Les services associés 9 : La facilité à offrir/se faire offrir un produit 10 : Navigation "américaine" vs. -

L Brands, Inc

New York Paris Northern California Madrid Washington DC Tokyo São Paulo Beijing London Hong Kong Davis Polk William H. Aaronson Davis Polk & Wardwell LLP 212 450 4000 tel 450 Lexington Avenue 212 701 5800 fax New York, NY 10017 January 31, 2020 VIA Email Office of Chief Counsel Division of Corporation Finance Securities and Exchange Commission 100 F Street, N.E. Washington, D.C. 20549 via email: [email protected] Ladies and Gentlemen: We refer to our letter dated January 10, 2020 (the “No-Action Request”), submitted on behalf of L Brands, Inc., a Delaware corporation (the “Company”), pursuant to which we requested that the Staff of the Division of Corporation Finance (the “Staff”) of the Securities and Exchange Commission concur with the Company’s view that the shareholder proposal (as revised, the “Proposal”) submitted by John Chevedden (the “Proponent”) may be excluded from the proxy materials the Company intends to distribute in connection with its 2020 Annual Meeting of Stockholders (the “2020 Proxy Materials”). In accordance with Rule 14a-8(j), a copy of this submission is being sent simultaneously to the Proponent. The No-Action Request stated the Company’s view that the Proposal may be excluded from the 2020 Proxy Materials because the Company’s Board of Directors (the “Board”) was expected, at its meeting held on January 30, 2020 (the “January Board Meeting”), to consider resolutions approving an amendment to the Company’s Restated Certificate of Incorporation (the “Certificate of Incorporation”) to eliminate the Company’s classified board structure resulting in all directors being elected annually beginning at the Company’s 2021 Annual Meeting of Stockholders (the “Charter Amendment”), which would substantially implement the Proposal under Rule 14a-8(i)(10). -

L Brands Announces Transformative Transaction with Sycamore Partners to Drive Shareholder Value

L Brands Announces Transformative Transaction With Sycamore Partners to Drive Shareholder Value February 20, 2020 Bath & Body Works to Become Focused, Standalone Public Company Majority 55% Interest in Victoria’s Secret Lingerie, Victoria’s Secret Beauty and Pink to be Acquired by Sycamore Partners, With L Brands Retaining 45% Minority Stake, at a Total Enterprise Value of $1.1 Billion Upon Closing of Transaction, Leslie H. Wexner to Step Down as Chairman and CEO; To Become Chairman Emeritus Andrew Meslow Promoted to CEO of Bath and Body Works; Upon Closing of Transaction, Meslow to be Appointed CEO of L Brands and Will Join Its Board L Brands Extends Agreement With Barington Capital Group, L.P. L Brands Updates Fourth Quarter Sales and Earnings Estimates COLUMBUS, Ohio, Feb. 20, 2020 (GLOBE NEWSWIRE) -- L Brands, Inc. (NYSE: LB) and Sycamore Partners, a private equity firm specializing in consumer and retail investments, today announced a strategic transaction that is intended to deliver long-term value to L Brands shareholders by positioning Bath & Body Works as a highly profitable, standalone public company and separating Victoria’s Secret Lingerie, Victoria’s Secret Beauty and PINK (collectively, Victoria’s Secret) into a privately-held entity focused on reinvigorating its market-leading businesses and returning them to historic levels of profitability and growth. A Transaction Committee of the Board of Directors, consisting of independent directors Allan Tessler and Sarah Nash, led the review process resulting in the transaction, which has been approved by a unanimous vote of the L Brands Board of Directors. Under the terms of the transaction, Victoria’s Secret, with a total enterprise value of $1.1 billion, will be separated from L Brands into a privately-held company majority-owned by Sycamore. -

Lingerie Trend Mini Report Aug 2009

Lingerie Trends Mini Report Alexandra Suhner Isenberg and Katie Pitman Fashion Trendsetter August 2009 © 2009 Fashion Trendsetter | www.fashiontrendsetter.com Lingerie Trends Mini Report TABLE OF CONTENTS Introduction 2 The Current Market 3 Brand Profiles 4 Opportunities Product 18 Retailing 22 Marketing 24 Future Trends 25 Conclusion 32 All Rights Reserved The facts of this report are believed to be correct at the time of publication but cannot be guaranteed. Please note that the findings, conclusions and recommendations that Fashion Trendsetter delivers will be based on information gathered in good faith from both primary and secondary sources, whose accuracy we are not always in a position to guarantee. As such Fashion Trendsetter can accept no liability whatever for actions taken based on any information that may subsequently prove to be incorrect. Alexandra Suhner and Katie Pitman 1 © 2009 Fashion Trendsetter | www.fashiontrendsetter.com Lingerie Trends Mini Report INTRODUCTION This mini-report aims to introduce the reader to the current opportunities in the UK and European lingerie markets, as well as introducing the key players and future trends. Image courtesy of Marks and Spencer Alexandra Suhner and Katie Pitman 2 © 2009 Fashion Trendsetter | www.fashiontrendsetter.com Lingerie Trends Mini Report THE CURRENT MARKET The lingerie market, like most fashion markets, is feeling the impact of the credit crunch and global recession. According to Mintel’s UK underwear Retailing Report 2009, most customers plan on spending less on lingerie in the near future, because of their economic situations. Where does that leave lingerie brands and retailers? Product innovation, inventive retailing strategies, and original marketing techniques are key to survival in this market. -

Victoria's Secret As a Do-It-Yourself Guide Lexie Kite University of Utah

Running Head: VS as a Do‐It‐Yourself Guide 1 From Objectification to Self-Subjectification: Victoria’s Secret as a Do-It-Yourself Guide Lexie Kite University of Utah Third-Year Doctoral Student Department of Communication 1 Running Head: VS as a Do‐It‐Yourself Guide 2 In the U.S. and now across the world, a multi-billion-dollar corporation has been fighting a tough battle for female empowerment since 1963, and according to their unmatched commercial success, women appear to be quite literally buying what this ubiquitous franchise is selling. Holding tight to a mission statement that stands first and foremost to “empower women,” and a slogan stating the brand is one to “Inspire, Empower and Indulge,” the franchise “helps customers to feel sexy, bold and powerful” (limitedbrands.com, 2010). This is being accomplished through the distribution of 400 million catalogs to homes each year, a constant array of television commercials all hours of the day, a CBS primetime show viewed by 100 million, and 1,500 mall storefront displays in the U.S. alone (VS Annual Report, 2009). And to the tune of 5 billion dollars every year, women are buying into the envelope-pushing “empowerment” sold by Victoria’s Secret, the nation’s premiere lingerie retailer. Due to Victoria’s Secret’s ubiquitous media presence and radical transformation from a modest, Victorian-era boutique to a sexed-up pop-culture phenomenon in the last decade, a critical reading of VS’s media texts is highly warranted. Having been almost completely ignored in academia, particularly in the last 15 years as the company has morphed from a place for men to shop for women to a women-only club (Juffer, 1996, p.