2010-11 Annual Report 20 October 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

E-Book Code: REAU1036

E-book Code: REAU1036 Written by Margaret Etherton. Illustrated by Terry Allen. Published by Ready-Ed Publications (2007) © Ready-Ed Publications - 2007. P.O. Box 276 Greenwood Perth W.A. 6024 Email: [email protected] Website: www.readyed.com.au COPYRIGHT NOTICE Permission is granted for the purchaser to photocopy sufficient copies for non-commercial educational purposes. However, this permission is not transferable and applies only to the purchasing individual or institution. ISBN 1 86397 710 4 12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345 12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345 12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345 12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345 12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345 12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012 12345678901234 5 12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345 12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345 -

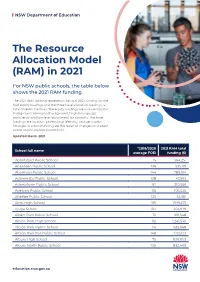

The Resource Allocation Model (RAM) in 2021

NSW Department of Education The Resource Allocation Model (RAM) in 2021 For NSW public schools, the table below shows the 2021 RAM funding. The 2021 RAM funding represents the total 2021 funding for the four equity loadings and the three base allocation loadings, a total of seven loadings. The equity loadings are socio-economic background, Aboriginal background, English language proficiency and low-level adjustment for disability. The base loadings are location, professional learning, and per capita. Changes in school funding are the result of changes to student needs and/or student enrolments. Updated March 2021 *2019/2020 2021 RAM total School full name average FOEI funding ($) Abbotsford Public School 15 364,251 Aberdeen Public School 136 535,119 Abermain Public School 144 786,614 Adaminaby Public School 108 47,993 Adamstown Public School 62 310,566 Adelong Public School 116 106,526 Afterlee Public School 125 32,361 Airds High School 169 1,919,475 Ajuga School 164 203,979 Albert Park Public School 111 251,548 Albion Park High School 112 1,241,530 Albion Park Public School 114 626,668 Albion Park Rail Public School 148 1,125,123 Albury High School 75 930,003 Albury North Public School 159 832,460 education.nsw.gov.au NSW Department of Education *2019/2020 2021 RAM total School full name average FOEI funding ($) Albury Public School 55 519,998 Albury West Public School 156 527,585 Aldavilla Public School 117 681,035 Alexandria Park Community School 58 1,030,224 Alfords Point Public School 57 252,497 Allambie Heights Public School 15 -

Australia's National Heritage

AUSTRALIA’S australia’s national heritage © Commonwealth of Australia, 2010 Published by the Australian Government Department of the Environment, Water, Heritage and the Arts ISBN: 978-1-921733-02-4 Information in this document may be copied for personal use or published for educational purposes, provided that any extracts are fully acknowledged. Heritage Division Australian Government Department of the Environment, Water, Heritage and the Arts GPO Box 787 Canberra ACT 2601 Australia Email [email protected] Phone 1800 803 772 Images used throughout are © Department of the Environment, Water, Heritage and the Arts and associated photographers unless otherwise noted. Front cover images courtesy: Botanic Gardens Trust, Joe Shemesh, Brickendon Estate, Stuart Cohen, iStockphoto Back cover: AGAD, GBRMPA, iStockphoto “Our heritage provides an enduring golden thread that binds our diverse past with our life today and the stories of tomorrow.” Anonymous Willandra Lakes Region II AUSTRALIA’S NATIONAL HERITAGE A message from the Minister Welcome to the second edition of Australia’s National Heritage celebrating the 87 special places on Australia’s National Heritage List. Australia’s heritage places are a source of great national pride. Each and every site tells a unique Australian story. These places and stories have laid the foundations of our shared national identity upon which our communities are built. The treasured places and their stories featured throughout this book represent Australia’s remarkably diverse natural environment. Places such as the Glass House Mountains and the picturesque Australian Alps. Other places celebrate Australia’s Aboriginal and Torres Strait Islander culture—the world’s oldest continuous culture on earth—through places such as the Brewarrina Fish Traps and Mount William Stone Hatchet Quarry. -

13.0 Remaking the Landscape

12 Chapter 13: Remaking the Landscape 13.0 Remaking the landscape 13.1 Research Question The Conservatorium site is located within one of the most significant historic and symbolic landscapes created by European settlers in Australia. The area is located between the sites of the original and replacement Government Houses, on a prominent ridge. While the utility of this ridge was first exploited by a group of windmills, utilitarian purposes soon became secondary to the Macquaries’ grandiose vision for Sydney and the Governor’s Domain in particular. The later creations of the Botanic Gardens, The Garden Palace and the Conservatorium itself, re-used, re-interpreted and created new vistas, paths and planting to reflect the growing urban and economic importance of Sydney within the context of the British empire. Modifications to this site, its topography and vegetation, can therefore be interpreted within the theme of landscape as an expression of the ideology of colonialism. It is considered that this site is uniquely placed to address this research theme which would act as a meaningful interpretive framework for archaeological evidence relating to environmental and landscape features.1 In response to this research question evidence will be presented on how the Government Domain was transformed by the various occupants of First Government House, and the later Government House, during the first years of the colony. The intention behind the gathering and analysis of this evidence is to place the Stables building and the archaeological evidence from all phases of the landscape within a conceptual framework so that we can begin to unravel the meaning behind these major alterations. -

Sandstone Sales

May 29 - June 14 Volume 32 - Issue 11 In the early 1900s the state government’s well organised Department of Agriculture conducted experimental and demonstration farms to assist citrus farmers with horticultural advice, crop management and pest control. At Dural regular field days were held for the farmers with some orchardists being accompanied by their wives. (SPF ML SLNSW) DOORAL DOORAL “Can you keep my dog from Sandstone The place we now know as Dural is derived from getting out?” ‘dooral dooral’ delightful sounding Aboriginal MARK VINT words understood to mean ‘a hollow tree on Sales fire at the bottom and smoking on the top’. The 9651 2182 Buy Direct From the Quarry Aboriginal method of hunting possums was 270 New Line Road to smoke them out of hollow trees. James Dural NSW 2158 9652 1783 Meehan, the ex-convict surveyor, spelled the [email protected] Handsplit name on his 1817 Map and Field Book as ABN: 84 451 806 754 Random Flagging $55m2 Dooral. Renowned for its ‘inexhausible forests’ WWW.DURALAUTO.COM 113 Smallwood Rd Glenorie Dural’s early days focussed on sawpits and timber yards. William Waddell and William C & M AUTO’S Jaga were sawing and splitting shingles here in Free 1849 and Burton’s Timberyard made shingles battery ONE STOP SHOP backup when Let us turn your tired car into a for St. Jude’s and fruit cases for growers. Ernie you mention finely tuned “Road Runner” Bennett’s 1950’s to 1970s mill was one of the this ad “We Certainly Can!” ~ Rego Checks including Duel Fuel, LPG Inspections & Repairs last to find that the ‘inexhaustable forests’ had ~ New Car Servicing ~ All Fleet Servicing ~ All General Repairs (Cars, Trucks & 4WD) become exhausted. -

Old Government House and Domain, Parramatta Park Management Plan

OLD GOVERNMENT HOUSE AND DOMAIN, PARRAMATTA PARK MANAGEMENT PLAN 2008 A New South Wales Contributory Site: Australian Convict Sites World Heritage Nomination Cover illustration: Montage of Old Government House, Governor Brisbane’s Bath house, and the Flat Rocks in Parramatta River: Photographer: David Wallace/Parramatta Park Trust The cover of this management plan is badged with a representation of the Great Seal of NSW used between 1790 and 1832. The seal shows on its obverse (front) a design that alludes to the intended redemptive qualities of the convict settlement, and was described in the Royal Warrant granting the seal as follows: Convicts landed at Botany Bay; their fetters taken off and received by Industry, sitting on a bale of goods with her attributes, the distaff [a spindle for spinning wool or flax], bee-hive, pick axe, and spade, pointing to an oxen ploughing, the rising habitations, and a church on a hill at a distance, with a fort for their defence. Motto: Sic fortis etruria crevit [So, I think, this is how brave Etruria grew]; with this inscription round the circumference, Sigillum Nov. Camb. Aust. [Seal of New South Wales] Image source: State Library of NSW, Digital image a1328002 Crown Copyright 2008 Disclaimer Whilst every reasonable effort has been made to ensure that this document is correct at the time of printing, the State of New South Wales, its agents and employees disclaim any and all liability to any persons in respect of anything or the consequences of anything done or omitted to be done in reliance upon the whole or any part of this document. -

Summer 2017 Newcastle Cruising Yacht Club

Farr 4 Regatta 12 Sailors with DisAbilities 18 NCYC Cruising Division 19 summer 17 Newcastle Cruising Yacht Club • 95 Hannell Street Wickham NSW 2293 • Ph 02 4940 8188 • www.ncyc.net.au SUMMER 2017 NEWCASTLE CRUISING YACHT CLUB Unwind | Share | Laugh | Enjoy In this issue 11 Summer 2017 journal A quarterly publication EVERY ISSUE Commodore's Report ..................................................... 4 Rear Commodore’s Report ............................................ 5 CEO Report .................................................................... 6 Marina & Assets Manager’s Report ............................... 7 Melbourne Cup Our Club......................................................................... 8 Social Highlights .......................................................... 10 14 Club Sailing ................................................................. 12 Laser Sailing ................................................................ 16 NCYC Cruising Division ............................................. 19 Sailing Academy .......................................................... 20 Borrelli Quirk Newcastle Real Estate .......................... 28 Founders Day ESSENTIAL INFORMATION Security Phone Numbers .............................................. 27 Coming Events ............................................................. 27 FEATURE ARTICLES Tenacity Award............................................................... 8 26 Melbourne Cup Images ................................................ 11 Newcastle Game -

Wambo Coal Pty Ltd

WAMBO COAL PTY LTD NORTH WAMBO UNDERGROUND MINE EXTRACTION PLAN LONGWALLS 8 TO 10A APPENDIX D HERITAGE MANAGEMENT PLAN WAMBO COAL PTY LTD NORTH WAMBO UNDERGROUND MINE HERITAGE MANAGEMENT PLAN LONGWALLS 8 - 10A PREPARED BY WAMBO COAL PTY LTD AND RESOURCE STRATEGIES PTY LTD APRIL 2015 Project No. WAM-09-15 Document No. 00666580.doc Heritage Management Plan – North Wambo Underground Mine Longwalls 8-10A DOCUMENT CONTROL Document No. HMP LW8-10A Title Heritage Management Plan for North Wambo Underground Mine Longwalls 8 to 10A General Description Management of potential environmental consequences on heritage sites or values for mining of Longwalls 8 to 10A at North Wambo Underground Mine. Key Support Documents Wambo Homestead Complex Mine Management Plan Wambo Coal Mine Salvage and Management Programme Revisions Rev No Date Description By Checked A October 2012 Original Draft WCPL and − Resource Strategies B November 2012 Draft for Consultation WCPL and T. Favell Resource Strategies C December 2012 Final for Submission WCPL and T. Favell Resource Strategies D December 2013 Revised to include WCPL and − Longwalls 9 and 10 Resource Strategies E February 2014 Final for Submission WCPL and T. Favell Resource Strategies F March 2015 Revised to include WCPL and T. Favell Longwall 10A Resource Strategies G April 2015 Final for Submission WCPL and P. Jaeger Resource Strategies Approvals Name Position Signed Date Environment and Originator T. Favell 10/04/2015 Community Manager Technical Services Checked T. Britten 10/04/2015 Manager NWU Manager of -

HBR Business News

DECEMBER 2020 VOLUME 16 NUMBER 11 Print Post Approved 100002454 mag.com.au HBRHunter Business Review 16TH YEAR OF PUBLICATION WOMEN IN BUSINESS Australia $6.60 MINING & ISSN 2202 - 8838 (Print) ISSN 2202 - 8846 (Online) ENERGY UPDATE HUNTER BUSINESS REVIEW HUNTER BUSINESS REVIEW Connecting & informing business people Connecting & informing business people WHAT WOULD YOUR BUSINESS DO WITH UP TO $20,000? KEEN TO GROW YOUR BUSINESS IN 2021? You may be eligible to receive grant funding for a new website, digital marketing, or other services! Scan the QR code to learn more: websites • digital marketing • creative Call (02) 4962 2236 Business Growth Grants Campaign-A4-01_02.indd 3 30/11/20 12:02 pm HBR contents PUBLISHED BY: Hunter Business Publications Pty Ltd ABN: 15 112 838 945 265 King Street Newcastle NSW 2300 PO Box 853, Hamilton NSW 2303 4 From the Editor Phone: (02) 4062 8133 Business News PUBLISHER and EDITOR: 5 Garry Hardie GARRY Mob: 0414 463 125 New Appointments [email protected] 17 ART DIRECTOR: Sandie Collie 18 Property [email protected] CONTENT MANAGER: 20 Women in Business Jason Duncan [email protected] SANDIE 26 Mining & Energy Update PRINTING: NCP Printing Phone: (02) 4926 1300 30 Business Services Directory [email protected] www.ncp.com.au 31 Funny Business Published monthly (except January) Hard copy circulation: 5,000 Also available online www.HBRmag.com.au JASON HUNTER BUSINESS PUBLICATIONS PTY LTD 2020 ALL RIGHTS RESERVED OUR PHONE NUMBER HAS CHANGED! Reproduction in any part prohibited without the written consent The number for Hunter Business Publications is now of the publisher. -

Coal River Tourism Project Coal River Historic Site Stage 1

Coal River Tourism Project Coal River Historic Site Stage One HHHiiissstttooorrriiicccaaalll AAAnnnaaalllyyysssiiisss ooofff SSSiiittteeesss aaannnddd RRReeelllaaattteeeddd HHHiiissstttooorrriiicccaaalll aaannnddd CCCuuullltttuuurrraaalll IIInnnfffrrraaassstttrrruuuccctttuuurrreee by Cynthia Hunter, August 2001 Watercolour by unknown artist, c. 1820 Original held at Dixson Library, State Library of New South Wales. This illustration encapsulated principal elements of the Coal River Historic Site. The ocean, Nobbys and South Head, the coal seams, the convicts at work quarrying building the breakwater wall and attending to the communication signals, the river, the foreshore, in all, the genesis of a vital commercial city and one of the world’s great ports of the modern industrial age. COAL RIVER HISTORIC SITE 1 Coal River Tourism Project Coal River Historic Site Stage 1 Prepared by CCCyyynnnttthhhiiiaaa HHHuuunnnttteeerrr August 2001 CCCooonnnttteeennnttt Provide a Statement of Significance in a National and State context which qualifies the connected cultural significance of the Coal River sites and the Newcastle East precinct ~ Section 1 Identify key sites and secondary sites ~ Section 2 Identify and link areas, sites and relics ~ Section 3 Propose a conceptual framework for an interpretation plan for Stage 3 ~ Section 4 Advise on likelihood and location of the tunnels based on historical research ~ Section 5 COAL RIVER HISTORIC SITE 2 Coal River Time Line 1796 Informal accounts reach Sydney of the reserves of coal at ‘Coal River’. 1797 Lt Shortland and his crew enter Coal River and confirm the coal resources 1801 Formal identification of the great potential of the coal reserves and the river and first and brief attempt to set up a coal mining camp. -

Australian Lighthouses by Ian Arthur

1 Australian Lighthouses By Ian Arthur The idea of writing an article on lighthouses for ASHET News originated in my reading a paper in the journal of the Society for the History of Technology, based in America. The paper by Michael Brian Schiffer is titled The Electric Lighthouse in the Nineteenth Century: Aid to Navigation and Political Technology and is published in the Volume 46 Number 2, April 2005 edition of the Society’s journal Technology and Culture. The paper mentions that the second Macquarie Lighthouse in Australia, when it opened in 1883, had the most powerful electric light in the world. This led me to read more about lighthouses in Australia, and this article is the result. It is timely, since the Australian Maritime Safety Authority (AMSA), responsible for providing aids to ocean and coastal navigation in Australia, celebrated its 100th anniversary in 2015, and 2018 will be the 200th anniversary of the opening of the first Australian lighthouse, the Macquarie Lighthouse on South Head in Sydney. The earliest lighthouses The first authenticated record of a lighthouse is that of the Pharos of Alex- andria, one of the Seven Wonders of the ancient world. It was built around 280 BC on the island of Pharos at the entrance to the port of Alexandria. It was large even by modern standards, around 120 m high, built of stone faced with marble. At the top was a wood fired beacon that could be seen under good conditions 30 miles out to sea. The Romans and the Phoenicians built many fire-beacons and a few lighthouses wherever they traded regularly, at locations reaching from the Eastern Mediterranean and the Black Sea to the Atlantic coast of Spain and to Britain. -

'Governor's Travels' (Newcastle Herald Weekender 27 March 2010 Pp. 10-13)

A couple of hundred years on, Lachlan Macquarie is still making his presence felt in these parts, writes NEILJAMESON. is fingers traced the furrows in the trunk of the blue gum. H They were as clear as the day the youth had taken the knife and etched them in the bark. On one side of the tree H H he had inscribed HJ.M. On the other HL.M. 4 Jany. 1812 • On their first visit to Hunter's River they had pitched their tents here in the encampment ground near Raymond Terrace and the young man had searched around tofind a suitable place to mark their passing. The older man had looked on as the youth laboured earnestly with the knife, standing back to admire his work. Now, six years later, amid the dappled lightof the same eucalypt grove, Lachlan Macquarie, career soldier and Governor of NSW, hung his head in reflection. Macquarie's young cousin was gone. J.M. - LieutenantJohn Maclaine had died in Ceylon just six months earlier, on January 13, 1881, shot by Kandyan militia while leading a mounted detachment through heavy jungle. The opinion of the commanding officer, that Lieutenant Maclaine had disregarded the advice of his men not to expose himself to enemy fire, came as no surprise. John Maclaine had always been bold-hearted, some would say foolhardy, There, with one palm resting on the blue gum's solid trunk, lost in thought, Macquarie may have recalled the time the boy officer had fallen from a ship's mast and broken his arm during a drunken party, or the occasions he had discharged the young man's debts to preserve his reputation.