VISTEON CORPORATION (Exact Name of Registrant As Speciñed in Its Charter)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Lete Television ' R I Gra

•EE • 'S C I ' LETE TELEVISION ' R I GRA THE ]'he Showcase Editorials Column Comment Editor Speaks Complete Short Story TV Shows This Week LEAPING FOR JOY JIINE 16, 195•' X OL. XXDi, No. 21 •.-•--... ß :. .. .:. ... z.• . .•.. .. .. ß • )=.iiii•-•i•;!-.;............................... ¾.:.:.:.:.:.:.:.:.:.:.:.:.:.:.:.:.:.:_:.:.:.:... , ::::::::::::::::::::::::::::::::::::::::::::::::::::::::: : . ..-_• •..::--. , ;_ wer.. for NewJersey!. ß,i• ' ?"'.....Ei?•--'•'•r-i½ity k•?•i•... working for •u g• hours-a day... and •lic Servicekeeps on th• ••t aad day to •ee to it that you have dependable•r•ee at CHANGES' AT MAHW•--Plant Manager Samuel L. Sim- •our fingertips• •at'• mor•, mons, Ford Motor ,Co., right, congratulates ,E.dward A. Nida, • •ectricity doesso much... left, of •04 Upper Boulevard, Ridgewood, promoted to opera- tions .•nanager on the aft4arnoon •shift, and Martin T. ,Molmch, o! Cups•w Ave., Erskine I•kes, Wanaque, to manager o! Plan- ning and Engineering. ' -:-.. :-. :- -:-:.:-:.:- ..:.:.:.:.:.:.:.:.:.:.:-:.:-:.:.:.:.:.:.:.- ß :'::::::::::::::::::::::: :% % -L: . ß . ...:- ß ..:.. -;:..:.. ß .. '-"•"-:•:K:F-.:.:.::.r:::::::::: ..:'-?'"======================================== :::::::::::::::::::::::::::: ßß ::::'.-':i•::::i:::::.':::-.-::.:.-::.:...:.-•: , :.. -- ' ....:::. - ':' ,,'-'- ':'• -:-:-:-:. -:-:-:-:.:-:-:-:-:--.:.: ..:.:.:.:.:.:.: :rS!:-.::.:.:.:.-½ .: ::I: .-:-:-:-:-:-:--- ß:---.-:.:.: ':'-..:•:•":...'-i'::'.-':•!'-'•' !i:'"':•i:i:i::-'-': ...::::i:M::. ß . ":'::::'-::::-:--'' ¾.'::::-:':-:-:-:::• ====================== -

Australian Radio Series

Radio Series Collection Guide1 Australian Radio Series 1930s to 1970s A guide to ScreenSound Australia’s holdings 1 Radio Series Collection Guide2 Copyright 1998 National Film and Sound Archive All rights reserved. No reproduction without permission. First published 1998 ScreenSound Australia McCoy Circuit, Acton ACT 2600 GPO Box 2002, Canberra ACT 2601 Phone (02) 6248 2000 Fax (02) 6248 2165 E-mail: [email protected] World Wide Web: http://www.screensound.gov.au ISSN: Cover design by MA@D Communication 2 Radio Series Collection Guide3 Contents Foreword i Introduction iii How to use this guide iv How to access collection material vi Radio Series listing 1 - Reference sources Index 3 Radio Series Collection Guide4 Foreword By Richard Lane* Radio serials in Australia date back to the 1930s, when Fred and Maggie Everybody, Coronets of England, The March of Time and the inimitable Yes, What? featured on wireless sets across the nation. Many of Australia’s greatest radio serials were produced during the 1940s. Among those listed in this guide are the Sunday night one-hour plays - The Lux Radio Theatre and The Macquarie Radio Theatre (becoming the Caltex Theatre after 1947); the many Jack Davey Shows, and The Bob Dyer Show; the Colgate Palmolive variety extravaganzas, headed by Calling the Stars, The Youth Show and McCackie Mansion, which starred the outrageously funny Mo (Roy Rene). Fine drama programs produced in Sydney in the 1940s included The Library of the Air and Max Afford's serial Hagen's Circus. Among the comedy programs listed from this decade are the George Wallace Shows, and Mrs 'Obbs with its hilariously garbled language. -

Optn TOMOR TILL 00! 52 U.S

WEDNESDAY, MARCH 29, 1961 PAGE TWENTY-EOXJR ArtngB Daily Net Press Run ^attrtf>Bts^r Sorning iimtlb i For tlM We«k Ended The Weather Much U, 1961 FereoMt of E. 8. Westher BareM Fair and coder tonlxlit Vnw 13,317 26-S2. Friday fair, not eo cod, Member of the Audit cloudIneM in aftemoos. Hlfh 48- BareM of OlronlsUon Manchester-—A City of Village Charm so. VOL. LXXX, NO. 152 (TWENTY-FOUR PAGES— IN TWO SECTIONS) MANCHESTER, CONN., THURSDAY, MARCH 30, 1961 (Clsmifled Advertlslnf on Pmge t t ) PRICE FIVE CENTS 21 Overseas OPtN TOMOR TILL 00! 52 U.S. Bases U.S. Pushing Buildup Other days to 5:45 Face Cutback Of Military Near Laos STAMPS Tomorrow Washington," March SO (A>)— The Defense Department an DOUBLE GREEN nounced today the closing or curtailment of activities at 52 C A S H SALES W ITH ALL military bases and installations in the United States. Twenty- one bases overseas also .nre being closed or cut back. Secretary of Defense Flobert S.^ McNamara said this was the first TB T Reds Want Awaits Red To enter Kathy’s new phas contest, please send yonr Whlllilte House plan to eliminate ob name and telephone niinri- solete or surplus InstEiIlations State J\ews her to Kathy Godfrey. NOW...SPRING COAT SALE! among- the 6.700 bases, big and lit Laos Truce Accord on WINF, Manchester. tle, at home and abroad. The estimated annual savings Roundup from today’s action may eventual ly reach $220 million, although After Talks Ctease-Fire this amount would not be saved COAT VALUES TO $45 during the several years needed Moscow, March 30 (/P)— Vientiane, Laos, March 30 T to carry out the cutback pro Montville Man There were indications in in 29 99 (iP)—The Laotian govern . -

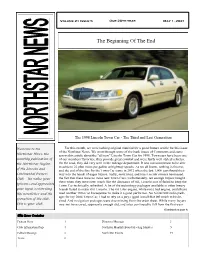

The Beginning of the End

Volume 21 Issue 5 Our 20th year May 1, 2021 The Beginning Of The End The 1998 Lincoln Town Car - The Third and Last Generation Welcome to the Northstar News, the monthly publication of the Northstar Region of the Lincoln and Continental Owners Club. We value your opinions and appreciate your input concerning this newsletter and the operation of the club. This is your club. (Continued on page 4) This Issue Contains Feature Story 1 Directors Message 3 Club Information Page 4 Northstar Monthly Board Meeting Minutes 5 Editors Message 2 North Star Events 15 Trivia 2 NORTHSTAR NEWS Trivia from the Editors Message May 2021 Internet Dear friends and Gentle Readers: little searching online, which was very limited in It is the beginning of May. Hopefully, we will 2001, turned up nice Lexmark Optra S series print- see some warmer and dryer weather in what should ers, black and white, but of good quality and capa- be a beautiful May. We have had a string of cold, ble of printing about 40 pages per minute. I also rainy days, which have really put a damper on what was able to buy an envelope attachment for it to should have been a nice prelude to the start of sum- print the 6x9 inch envelopes that we mailed the mer. newsletters out. I also signed up for Stamps.com, A lot of us have now had the series of Covid- an online postage program that enabled us to print 19 vaccine shots. There are still a significant num- the addresses and postage on the envelopes in one ber of folks out there, pass. -

SIXTEEN TONS Page 1 of 3 Released Apr 98

SIXTEEN TONS Page 1 of 3 Released Apr 98 Choreographer: Annette and Frank Woodruff rue du Camp, 87, B-7034 Mons, Belgium Tel: 32 (0) 65 73 19 40, e-mail: [email protected] Music: Collectables COL 6300, Tennessee Ernie Ford, flip “A hundred pounds of clay" Or mp3 download from Amazon or others. Time 2:33 @ speed 44 Footwork: Opposite unless otherwise indicated (lady ‘s footwork between brackets) Rhythm & RAL Phase: Jive V Sequence: Intro – AB – A – B Mod Re-visited Feb 2016 INTRODUCTION 1 - 4 WAIT ; VINE 3 HOLD ; SLOW HOOK ; UNWIND TO CP ; BFLY WALL wt 4 notes; sd L, XRIB, sd L,-; -, hook RIF (W LIF),-,-; [on “some”] unwind LF full tm to CP WALL; [Part A starts on “people”] PART A 1 - 5 MOOCH TO HNDSHK ;;;;; Trng to 1/2 OP LOD rk bk L, rec R, kck L, sip L; kck R, sip R, rk bk L, rec R; trng RF 1/2 fwd L/cl R, bk L to 1/2 LOP RLOD, rk bk R, rec L; kck R, sip R, kck L, sip L; rk bk R, rec L, trng LF 1/4 fwd R/cl L, fwd R to HNDSHK WALL; 6 - 9 TRIPLE WHEEL LOD ~ CHANGE HANDS BEHIND THE BACK ;;;; Rk apt L, rec R, whl RF sd L/cl R, sd L trng twd ptr & tch W’s bk w/ L hnd (W whl RF sd R/cl L, sd R trng awy from ptr); cont RF whl sd R/cl L, sd R tmg awy from ptr (W cont RF whl sd L cl R, sdL trng twd ptr & tch M's bk w/ L hnd), cont RF wheel sd L/cl R, sd L tmg twd ptr & tch W’s bk w/ L hnd (W cont RF whl trng awy from ptr sd R/cl L, sd R swvlg RF to fc ptr); sd R/cl L, sd R (W spn full RF trn L/ R,L) to LOP-FCG LOD, {Chg Hnds Bhd Bk} rk apt L, rec R; fwd L/cl R, fwd L trn ¼ LF (W rk bk R, rec L, fwd R/cl L, fwd R trn ¼ RF) chg W’s R -

Mark Laver Jazzvertising

Jazzvertising: Music, Marketing, and Meaning by Mark Laver A thesis submitted in conformity with the requirements for the degree of Doctor of Philosophy in Ethnomusicology Faculty of Music University of Toronto © Copyright by Mark Laver 2011 Jazzvertising: Music, Marketing, and Meaning Mark Laver Doctor of Philosophy in Ethnomusicology Faculty of Music University of Toronto 2011 Abstract This dissertation examines jazz from the perspective of advertisers and marketers that have used the music with a view to unraveling the complicated web of cultural meanings and values that attend to jazz in the 21st century. Advertising is a critically important and profoundly complex medium for the mass dissemination of music and musical meaning. Advertisers and marketers therefore offer crucial perspectives on the construction, reification, and circulation of jazz meanings and discourses. At the same time, I argue that historically jazz has been a cultural practice that is uniquely situated on the cusp of the binarized cultural categories of “high art” and “popular/commercial”. With that in mind, I suggest that jazz offers an invaluable lens through which to examine the complex and often contradictory culture of consumption upon which North American capitalism is predicated. In a broad sense, then, I examine the confluence of jazz, consumption, and capitalism as they are articulated through the medium of advertising. ii I contextualize my analysis with a short history of music in advertising and a discussion of jazz’s embeddedness in capitalism and the North American culture of consumption. The core of the dissertation consists of three detailed case studies: an analysis of jazz and luxury in a 2003 Chrysler Canada campaign for the high-end cars Sebring and 300M, featuring Diana Krall; a discussion of the function of jazz in the spectacularization of cultural diversity and individual agency in the television campaign for a 2006 Diet Pepsi product called “Jazz”; and an examination of corporate amorality in the Toronto Dominion Bank’s sponsorship of jazz festivals in Canada. -

Complete Television Programs

PROGRAMS WEEK'S COMPLETE TELEVISION SUND Y E litton East Paterson Fair Lay a arfie:•c• .Maledon Hawfho•'ne •odi Little Falls Mountain View North Holedon Paterson Pore •.• Lakes rosp•c't Park incjac otowa Vayne •esf P•ferson MARCH 29 1959 VOL. XXXl, No. 1 3 ...:. .,...:...:;ß •!::-• '::.:.x!::. '-:.'..... .4. •.. .. ß ß '-'.'-. '" .;::-.i....::::ii•.".'i..:':!,......-".-11•t ':' ':•" :.. '-'::'::i::' .....r.•!• .re:::...... .:.*-'*': :.:.. '- " ß • .;--".•.ß..............•... .i.•'..ii:'.,.'2........:•'.._•.:....'.'..Ji!:.:::.':.•: :•:..:*!';. ..-. .....'"..... ß ß ß .!' '.- :•.?-.•:! • , ....:.:•½6-- ::..::•.½.:s•:% .....• -" , ß ß,..•...*..•-'--'-- ,,:...-..•c•.,,>.... .-.:.:.:.:.:.:-'..x-.^-..½½ • ...... .>.:;•. .:...-' - :::.... i' ...... /- .:.:....• .- ':'•i?-.:½ .-. .:.. .:. , '.f.- i-.• ,.......:::!...: ..: ...................:::::::::::::::::::::::::::::::::::::.. ..... ..-. ß . .- :..." . ß . :. ,, • •:•,, ,,-,. • ß .' . .i...:..':•i;•;.":•:-:: .:.. - .. ß , . •, . : ß .:. • ; ,;. •'"':""': ...... ': "::' -:;" ":'"'":';?"i::::' !:• ;::.. '.' ß.'*. '.:':: -'-' ...i ' .ß' '-'.:--.2 •:- ß '•' '' .-.- "-':"':-I':ti •':'i' ::::'•.•:;:'"..... '-•'::...: ':':i:_- ::...- ..., . .•.¾½!½;!•:.•'.•:.......::.. -.' .. ß :; , .•:•': ß ,.. ß •. ?::•:........ .. ,..-'..-•. •-.. •:;".... ,.:.': ..½-'.-. :.-'%."....e'..•:: •.::';!'-:'-:.-•::!":':" ß .•.t• . .. :. -" •'-;? : ': .'.'•.:•..'.:. .. • ß i. •.?"-•':-. %. ': '-' • •.i::. "' ")" • ::•iii:iii!i...-,•i:."&:::-i!i:'."-....'i'- " 'ø •-.; : i-........ "."•.•:. ,-:: ' ..:'•., ,.½!:'" '... -

Celebrating the Continental

Volume 19 Issue 4 April 1, 2019 Celebrating the Continental John Walcek behind the wheel of Don Longheed’s 1940 Cabriolet For April, we took a deep dive into the endless archives of all things Lincoln that I have in floor to ceiling stacks at my humble abode in Burnsville. I found a few interesting articles, one of which we will call our feature article, written by LCOC Club photographer John Walcek. This enjoyable story origi- nally appeared in the September-October 2010 issue of Continental Comments. We hope that you enjoy John Walcek’s nice story about the 70 year anniversary of the Lincoln Continental. Welcome to the Lately, I find myself looking back and reflecting on events that shaped my life, and dwell- ing on the good things. We Americans need any excuse to celebrate the good times and things. Northstar News, the This year, how about celebrating with me the 70th birthday of the first production Lincoln monthly publication of Continental? the Northstar Region I became aware of this car while working on a car calendar with Ken Tibbot for the Early Ford V-8 Club in 1997; we posed a photograph of a Ford tractor pulling his unrestored '40 of the Lincoln and Lincoln Continental Cabriolet out of a barn. The car captivated me. Since then, a junker '41 Continental Owners Lincoln Continental Cabriolet and a nicer '40 Coupe have found me. Club. We value your It's interesting to know the family dynamics and evolution that happened through the decades in the Ford Motor Company. -

Life-By-Time-Inc-Published-January-21

! Meet the Townsleys of South Bend— J. B. Townsley, the father, is 56. W. B. Townsley, the son, is ' 25. Their expert craftsmanship is the kind that puts extra miles of fine performance into every Studebaker. You never pay any premium for the plus value that Studcbaker's painstaking manufacturing a Unchanged in a changing world Studebakers trustworthy Bock from the Army Air Forces to the Studebaker job of father-and-son craftsmanship apprentice tool maker that he left 'way back in 1942, has come W. A. Smith. Jr. His proud father. W. A. Smith, tool supervisor, and a veteran of 26 Studebaker years, here takes time to give the young man some welcome suggestions. CARS vary in appearance with the years. have left the hands oft heir original owners. Mechanical improvements continually For generations, the quality of Stude- come along to add new zest and conven- l aker craftsmanship has been zealously ience to driving. rraintained by responsible workmen who But there's one thing unchanging in the are not only friendly neighbors but solid ever-changing automobile picture — and citizens with their roots deep in South that's the quality of Studcbaker's unique Bend's history. father-and-son craftsmanship. Home-loving, home-owning family men That trustworthy craftsmanship is one themselves, these craftsmen have encour- of the best of many good reasons for buy- aged their own sons, through the years, to ing a Studebaker today, just as it was back join with them in building Studebaker cars in the goggle-and-duster days of the early to the verv highest standards of excellence. -

West Ministers Agree on Summit

4 .,. ' / '■ -'^ . ■■ /:.■ . ' 'T h fl Wwthcr' " * / 9- . WEDNESDAY, APRIL 18, I860 Average Daily Net PreM Ron Feraiaant of U. B W anitef 'Umsoag r PA€E TWENTY-EIGHT For tho WMk Ended - " ■ 'I .:- liattflii^ater lEufttittg Iggratt April t, IMO Fair and w am tonight ahd fM -' . ' >v'^ ’:5 day. IMW tsniflbt M ar M . B|gk for th* sale may ca ll-W s. -U l- returned home after spending the The senior choir of the Salva 13,095 Friday In Mb. Dale Brown, a graduate of Man- tion Army will sponsor its annual llan Perrett, 49 Keeney S t cheater High School, haa been winter in S t Petersburg, and Member at the Audit A b o u t T ow n Gulfport Fla. Food Sale Saturday'at »:80 a.m. in Boreaa of CNrenlatlon M anche»ter-^A City o f Village Charm elected treasurer of the new stu the vestibule of the church. Mrs. The F ^ s Keynolds Group of Hale’s Self Siene anil Meat Detit dent government at High Point Frank Duncan and Miss Olatos Second Congregational' Church College, High Point N. C. The -midweek service at ' the will meet tomorrow at 10 a.m. in Sam Y uIjtm, M Florence S t, Is Church of the Nazareno will be White are co-chairmen of the sale, ») Pjj^CB FIV E dtolTB ■pending ■ tw6 weeks' vacation In which will offer a variety of c^es, Hie church parlors. Hostesses will MANCHESTER, CONN., THURSDAY, APRIL 14, 1960 John Munsle, 829 Main St. held tomorrow at 7:80 p.m. -

Tommy Dorsey Catalog 1 9

TOMMY DORSEY CATALOG 1 9 4 3 Prepared by: DENNIS M. SPRAGG YEAR-BY-YEAR CHRONOLOGY Volume 1 / Chapter 9 Updated February 24, 2016 1 January 1943 ELLINGTON WINS SWING POLL Tommy Dorsey Best In Sweet “After starting in a first place tie with Benny Goodman in the Sixth Annual “Down Beat” All Start Swing Poll, Duke Ellington cooled his heels for a reluctant two incomplete tabulations, constantly straining at the thin thread that kept him from Benny, and finally, in the terrific flood of final ballots, edged up top a small but decisive victory over Benny Goodman. The victory was the tightest since Artie Shaw topped King Benny for 1938s crown in that department. Almost as close was Tommy Dorsey’s lead over Glenn Miller for the sweet band lead. Tommy’s crown was re-acquired in the year of his string addition despite many adverse comments from the critics on the style change. Tommy held the crown in 1939 and then bowed to Glenn for the 1940 and 1941 seasons to recapture the coveted award again this year.1 January 1, 1943 (Fri) 10:30 - 11:00 pm Hollywood Palladium (KNX) (Local) (Sustaining) January 2, 1943 (Sat) M-G-M Studios Culver City, California Soundtrack Recording Session M-G-M Film Production “Girl Crazy” I GOT RHYTHM (Ira Gershwin-George Gershwin) Vocal refrain by Judy Garland, Mickey Rooney, Six Hits And A Miss, The Music Maids, Hal Hopper, Trudy Erwin, Barbara Canvin and the M-G-M Studio Chorus Continued from of December 29, 1942 recording session Also continued to February 2, 1943 recording session CD: Rhino R2 72732, R2 75290 January -

The Life and Work of Robert Russell Bennett

''KJ, 'n THE LIFE AND WORK OF ROBERT RUSSELL BENNETT by ROY BENTON HAWKINS, B.M.Ed., M.M. A DISSERTATION IN FINE ARTS Submitted to the Graduate Faculty of Texas Tech University in Partial Fulfillment of the Requirements for the Degree of DOCTOR OF PHILOSOPHY Approved, August, 1989 • he Copyright 1989 Roy Benton Hawkins ACKNOWLEDGMENTS Anyone who has ever undertaken a project of this nature is surely aware that its completion would have been impossible without the kind ness, assistance, patience, and support of many people. This study stands as an example of one that could not even have begun without the cooperation of several key persons. Foremost among these is Kean K. McDonald, the grandson of Robert Russell Bennett. Mr. McDonald's kind permission to allow the author access to Bennett's memoirs was the central element in the decision to attempt this study. Only marginally less important was the contribution of Gayle T. Harris, whose compilation of two thick binders of material about Bennett amounted to a head start for the author of months, or perhaps years. Her catalogue, "Another Russell Bennett Notebook," gave structure to the wealth of information that she had collected. In fact, the appendix of this study should be considered an updated version of a portion of the Harris catalogue. Finally, and perhaps most importantly, her lively intellectual curiosity, the thoroughness of her scholarship, her cooperativeness, and her devotion to the memory of Bennett (whom she knew) served as both object lesson and inspiration to the author. Gratitude must also be expressed to Barbara G.