Canadian Energy Research Institute

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pipeline Authority Annual Report 2018

North Dakota Pipeline Authority Annual Report July 1, 2017 – June 30, 2018 Industrial Commission of North Dakota Governor Doug Burgum, Chairman Attorney General Wayne Stenehjem Agriculture Commissioner Doug Goehring North Dakota Pipeline Authority Annual Report July 1, 2017 – June 30, 2018 Overview At the request of the North Dakota Industrial Commission, the Sixtieth Legislature passed House Bill 1128 authorizing the North Dakota Pipeline Authority. It was signed into law on April 11, 2007. The statutory mission of the Pipeline Authority is “to diversify and expand the North Dakota economy by facilitating development of pipeline facilities to support the production, transportation, and utilization of North Dakota energy-related commodities, thereby increasing employment, stimulating economic activity, augmenting sources of tax revenue, fostering economic stability and improving the State’s economy”. As established by the Legislature, the Pipeline Authority is a builder of last resort, meaning private business would have the first opportunity to invest in and/or build additional needed pipeline infrastructure. By law, the Pipeline Authority membership is comprised of the members of the North Dakota Industrial Commission. Upon the recommendation of the Oil and Gas Research Council, the Industrial Commission authorized the expenditure of up to $325,000 during the 2017-2019 biennium for the Pipeline Authority with funding being made available from the Oil and Gas Research Fund. On August 1, 2008 the Industrial Commission named Justin J. Kringstad, an engineering consultant, to serve as Director of the North Dakota Pipeline Authority. The North Dakota Pipeline Authority Director works closely with Lynn Helms, Department of Mineral Resources Director, Ron Ness, North Dakota Petroleum Council President and Karlene Fine, Industrial Commission Executive Director. -

ABOUT PIPELINES OUR ENERGY CONNECTIONS the Facts About Pipelines

ABOUT PIPELINES OUR ENERGY CONNECTIONS THE facts ABOUT PIPELINES This fact book is designed to provide easy access to information about the transmission pipeline industry in Canada. The facts are developed using CEPA member data or sourced from third parties. For more information about pipelines visit aboutpipelines.com. An electronic version of this fact book is available at aboutpipelines.com, and printed copies can be obtained by contacting [email protected]. The Canadian Energy Pipeline Association (CEPA) CEPA’s members represents Canada’s transmission pipeline companies transport around who operate more than 115,000 kilometres of 97 per cent of pipeline in Canada. CEPA’s mission is to enhance Canada’s daily the operating excellence, business environment and natural gas and recognized responsibility of the Canadian energy transmission pipeline industry through leadership and onshore crude credible engagement between member companies, oil production. governments, the public and stakeholders. TABLE OF CONTENTS 1. Canada’s Pipeline Network .................................1 2. Pipeline Design and Standards .........................6 3. Safety and the Environment ..............................7 4. The Regulatory Landscape ...............................11 5. Fuelling Strong Economic ................................13 and Community Growth 6. The Future of Canada’s Pipelines ................13 Unless otherwise indicated, all photos used in this fact book are courtesy of CEPA member companies. CANADA’S PIPELINE % of the energy used for NETWORK transportation in Canada comes 94 from petroleum products. The Importance of • More than half the homes in Canada are Canada’s Pipelines heated by furnaces that burn natural gas. • Many pharmaceuticals, chemicals, oils, Oil and gas products are an important part lubricants and plastics incorporate of our daily lives. -

Canadian Pipeline Transportation System Energy Market Assessment

National Energy Office national Board de l’énergie CANADIAN PIPELINE TRANSPORTATION SYSTEM ENERGY MARKET ASSESSMENT National Energy Office national Board de l’énergie National Energy Office national Board de l’énergieAPRIL 2014 National Energy Office national Board de l’énergie National Energy Office national Board de l’énergie CANADIAN PIPELINE TRANSPORTATION SYSTEM ENERGY MARKET ASSESSMENT National Energy Office national Board de l’énergie National Energy Office national Board de l’énergieAPRIL 2014 National Energy Office national Board de l’énergie Permission to Reproduce Materials may be reproduced for personal, educational and/or non-profit activities, in part or in whole and by any means, without charge or further permission from the National Energy Board, provided that due diligence is exercised in ensuring the accuracy of the information reproduced; that the National Energy Board is identified as the source institution; and that the reproduction is not represented as an official version of the information reproduced, nor as having been made in affiliation with, or with the endorsement of the National Energy Board. For permission to reproduce the information in this publication for commercial redistribution, please e-mail: [email protected] Autorisation de reproduction Le contenu de cette publication peut être reproduit à des fins personnelles, éducatives et/ou sans but lucratif, en tout ou en partie et par quelque moyen que ce soit, sans frais et sans autre permission de l’Office national de l’énergie, pourvu qu’une diligence raisonnable soit exercée afin d’assurer l’exactitude de l’information reproduite, que l’Office national de l’énergie soit mentionné comme organisme source et que la reproduction ne soit présentée ni comme une version officielle ni comme une copie ayant été faite en collaboration avec l’Office national de l’énergie ou avec son consentement. -

Transcanada Pipelines Limited Annual Information Form

TRANSCANADA PIPELINES LIMITED ANNUAL INFORMATION FORM February 23, 2009 TRANSCANADA PIPELINES LIMITED i TABLE OF CONTENTS Page PRESENTATION OF INFORMATION..................................................................................................................................................ii FORWARD-LOOKING INFORMATION..............................................................................................................................................ii TRANSCANADA PIPELINES LIMITED............................................................................................................................................... 1 Corporate Structure ............................................................................................................................................................................ 1 Intercorporate Relationships............................................................................................................................................................... 1 GENERAL DEVELOPMENT OF THE BUSINESS .............................................................................................................................. 2 Developments in the Pipelines Business............................................................................................................................................. 2 Developments in the Energy Business............................................................................................................................................... -

Border Crossings of Natural Gas Pipelines, North America Cruces Fronterizos De Ductos De Gas Natural, América Del Norte

140°E 150°E 160°E 170°E 180° 170°W 160°W 150°W 140°W 130°W 120°W 110°W 100°W 90°W 80°W 70°W 60°W 50°W 40°W 30°W 20°W 10°W Border Crossings of Natural Gas Pipelines, North America Cruces Fronterizos de Ductos de Gas Natural, América del Norte E l l e s m e r e I s l a n d 70°N Passages Transfrontaliers de Pipelines de Gaz Naturel, Amérique du Nord Í l e d u E l l e s m e r e 70°N 60°N A l a s k a 60°N N o r t h w e s t Te r r i t o r i e s Yu k o n Te r r i t o i r e s d u N o r d - O u e s t N u n a v u t 50°N 26 N e w f o u n d l a n d a n d L a b r a d o r 50°N 25 Te r r e - N e u v e e t - L a b r a d o r A l b e r t a 23 B r i t i s h C o l u m b i a S a s k a t c h e w a n P a c i f i c C o l o m b i e - B r i t a n n i q u e Ve r m o n t M a n i t o b a 24 40°N O c e a n 22 N e w O n t a r i o Q u é b e c P r i n c e E d w a r d I s l a n d H aÎ ml e - d up P r isn c eh- É dio ura red 1 N e w 2 3 B r u n s w i c k 4 6 8 9 N o u v e a u 11 B r u n s w i c k O c é a n o 27 W a s h i n g t o n 7 P a c í f i c o 5 10 26 M a i n e 12 13 25 N o v a S c o t i a M o n t a n a N o u v e l l e - É c o s s e N o r t h D a k o t a 23 M i n n e s o t a Ve r m o n t 40°N N e w 24 H a m p s h i r e 22 M i c h i g a n 20 N e w M a s s a c h u s e t t s O r e g o n I d a h o W i s c o n s i n S o u t h D a k o t a 19 Yo r k A t l a n t i c 18 C o n n e c t i c u t 14 16 21 30°N O c é a n W y o m i n g R h o d e I s l a n d O c e a n 15 17 P e n n s y l v a n i a P a c i f i q u e N e b r a s k a I o w a N e w J e r s e y O h i o I n d i a n a M -

View Annual Report

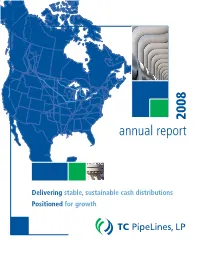

2008 annual report Delivering stable, sustainable cash distributions Positioned for growth financial highlights Year ended December 31 2004 2005 2006 2007 2008 (millions of dollars, except per unit amounts) Income Statement Net income 55.1 50.2 44.7 89.0 107.7 Cash Flow Partnership cash flows* 66.9 66.2 70.3 132.4 156.2 Cash distributions paid 41.8 43.0 43.5 86.7 108.6 Balance Sheet Total assets 332.1 315.7 777.8 1,492.6 1,448.5 Long-term debt (including current maturities) 36.5 13.5 468.1 573.4 536.8 Partners’ equity 294.9 301.6 303.9 900.1 875.6 Common Units Statistics (per unit) Net income $ 2.99 $ 2.70 $ 2.39 $ 2.51 $ 2.75 Cash distributions paid $ 2.250 $ 2.300 $ 2.325 $ 2.565 $ 2.775 Common Units Outstanding** 17.5 17.5 17.5 34.9 34.9 Net Income Cash Distributions Partnership Total Assets (dollars per unit) Paid Cash Flows* (millions of dollars) (dollars per unit) (millions of dollars) 2.99 156.2 1492.6 1448.5 2.70 2.75 2.775 2.51 2.565 132.4 2.39 2.250 2.300 2.325 777.8 66.9 66.2 70.3 332.1 315.7 2004 2005 2006 2007 2008 2004 2005 2006 2007 2008 2004 2005 2006 2007 2008 2004 2005 2006 2007 2008 *Partnership cash flows is a non-GAAP financial measure which is the sum of net income, cash distributions received from Great Lakes and Northern Border, and cash flows provided by Tuscarora’s operating activities less equity income from investments in Great Lakes and Northern Border and Tuscarora’s net income. -

About Pipelines Our Energy Connections the Facts About Pipelines

OUR ENERGY CONNECTIONS ENERGY OUR ABOUT PIPELINES ABOUT Contact Us Canadian Energy Pipeline Association Tel: 403.221.8777 [email protected] aboutpipelines.com @aboutpipelines http://facebook.com/aboutpipelines Statistics Pipeline inside pocket inside IMPORTANT THE FACTS ABOUT PIPELINES This fact book is designed to provide easy access to information about the transmission pipeline industry in Canada. The facts are developed using CEPA member data or sourced from third parties. For more information about pipelines visit aboutpipelines.com. An electronic version of this fact book is available at aboutpipelines.com, and printed copies can be obtained by contacting [email protected]. The Canadian Energy Pipeline Association (CEPA) CEPA’s members represents Canada’s transmission pipeline companies transport around who operate 115,000 kilometres of pipeline in 97 per cent of Canada. CEPA’s mission is to enhance the operating Canada’s daily excellence, business environment and recognized natural gas and responsibility of the Canadian energy transmission pipeline industry through leadership and credible onshore crude engagement between member companies, oil production. governments, the public and stakeholders. TABLE OF CONTENTS 1. Canada’s Pipeline Network .................................1 2. Types of Pipelines ......................................................3 3. The Regulatory Landscape ..................................5 4. Building and Operating Pipelines....................6 5. CEPA Integrity First® Program ......................12 6. The History of Our Pipelines ..........................13 Unless otherwise indicated, all photos used in this fact book are courtesy of CEPA member companies. CANADA’S PIPELINE % of the energy used for NETWORK transportation in Canada comes 94 from refined petroleum products. The Importance of • More than half the homes in Canada are Canada’s Pipelines heated by furnaces that burn natural gas. -

File OF-GEN-06 FRR 14 August 2020 To: All Pipeline Companies

File OF-GEN-06 FRR 14 August 2020 To: All Pipeline Companies regulated under the Canadian Energy Regulator Act Commission of the Canada Energy Regulator (Commission) Pipeline Financial Resources Requirements Update on Approval of Financial Resources Plans Background Subsection 138(1) of the Canadian Energy Regulator Act (CER Act) requires pipeline companies to maintain financial resources equal to their absolute liability level. The Pipeline Financial Requirements Regulations (Regulations), which came into force on 11 July 2019, set out absolute liability limits for the non-major oil pipeline companies1 (i.e., all other oil, gas, and commodity pipeline companies). On 29 March 2019, the National Energy Board (NEB) issued the Pipeline Financial Requirements Guidelines (Guidelines). Included in the Guidelines was a schedule for companies to submit their financial resources plans for review and approval. By 16 April 2019, the first Financial Resources Plans from companies with an absolute liability class of Oil Class 2 and 3 were filed with the NEB for review. This was followed by companies with an absolute liability class of Gas Class 1, 2, 3, and 4 filing their Financial Resources Plans. Companies with an absolute liability class of Other Commodity filed their Financial Resources Plans by 11 June 2019. Companies whose Financial Resources Plans were previously approved are listed in Appendix I under the headings “Approved as of” for the following dates: 17 July 2019, 28 August 2019, 18 December 2019, and 3 June 2020. The Commission continues to consider the Financial Resources Plans from Oil, Gas, and Other Commodity companies filed to-date. This letter updates and replaces the Commission’s previous letter dated 3 June 2020. -

Pipeline and Processing Fac... - Pipeline Projects with Length Greater Than 20 Miles

12/29/2015 Pipeline and Processing Fac... - Pipeline projects with Length Greater than 20 Miles Pipeline projects with DEC-29-2015 Pipeline and Processing Facilities : SAVED REPORTS Length Greater than 1:37 PM 20 Miles Pipeline projects with Length Greater than 20 Miles Holding Company or Parent Operating Company: Project Status Project Project Name: Length Organization: Type: (New Miles) AK (6 Pipeline projects) Energia Cura Fairbanks Pipeline Doubtful New Arctic Fox (Fairbanks Pipeline) 443 Company Linc Energy Linc Energy On New Umiat Oil Field Pipeline 80 Hold/Postponed Alaska Housing Finance Alaska Gasline On New Alaska Stand Alone Pipeline (ASAP) 737 Corporation Development Hold/Postponed Corporation BP BP Under New Point Thomson Gas Field 22 Construction NovaGold Resources Inc. Donlin Gold, LLC Advanced New Donlin Gold 312 Development Alaska LNG Early New Alaska LNG (AKLNG) 800 Development TOT 2,394 AL (6 Pipeline projects) Southern Company Alabama Power Under New Gaston Natural Gas Pipeline 30 Construction Spectra Energy Spectra Energy Advanced New Sabal Trail 515 Development Williams Company Transcontinental Gas Early New Hillabee Expansion Project Phase 1 20 Pipeline Company LLC Development Miller Energy Resources Early New Trans - Foreland Pipeline (TFPL) system 23 Development Laclede Gas Alagasco On-going Replacement Alagasco Pipeline replacement program 850 PRP Williams Company Transcontinental Gas Early New Hillabee Expansion Project Phase 2 and 3 24 Pipeline Company LLC Development TOT 1,462 Alberta (43 Pipeline projects) TransCanada Imperial Oil Early New Mackenzie Gas Project 758 Development Enbridge Inc. Enbridge Income Fund Advanced New Northern Gateway Pipeline (westward 731 Development crude for export) TransCanada TransCanada Advanced New Keystone XL 1,661 Development Enhance Energy Inc. -

QUARTERLY FOCUS: Planned Pipeline Construction Designed To

North American Gas Trade * North American Gas Trade * North American Gas Trade * North American Gas Trade * North American Gas Trade QUARTERLY FOCUS: Planned Pipeline Construction Designed to Foster Increased Gas Trade Between the United States and Canada INTRODUCTION capacity additions are projected to occur in the Midwestern and Northeastern corridors. Most of As a part of its regulatory oversight the planned capacity additions provide improved responsibilities, the Office of Natural Gas & access to western Canadian supplies; however, Petroleum Import and Export Activities several of the projects are being built to transport (Import/Export Office) performs various analytical Canadian natural gas reserves located offshore studies related to the import and export of natural Nova Scotia from Sable Island. gas. This Quarterly Focus looks at some of the planned pipeline construction projects which, if The Import/Export Office has obtained built, would increase the ability to transport information about these individual projects from additional volumes of natural gas between the various sources, including regulatory filings made United States and Canada. For the most part, these with the Federal Energy Regulatory Commission proposed projects are being designed to increase (FERC), Department of Energy (DOE), company the importation of natural gas. A similar review of representatives and Internet Web sites, and various proposed construction projects was the subject of trade journals. The review of proposed projects the Quarterly Focus written for the Quarterly include a number of projects recently announced Report issued in the second quarter of 1996; this by the sponsoring companies which have not report merely updates the status of some of the advanced much beyond the conceptual stage in projects reviewed earlier and examines some of development. -

1999 Annual Report

THE ENERGY BRIDGE 1999 ANNUAL REPORT 1 Highlights 2 Letter to Shareholders 8 Operations Review 14 Management’s Discussion and Analysis 31 Financial Statements and Notes 57 Supplementary Information 58 Five Year Consolidated Highlights 60 Shareholder and Investor Information BRIDGING THE GAP Enbridge bridges the gap between energy supply and the customer, providing seamless service and delivery. Enbridge is also bridging the gap from the present to an innovative and exciting energy future. As a transporter of energy, Enbridge operates, in Canada and the United States, the world’s longest crude oil and liquids pipeline system. The Company also is involved in liquids marketing and international energy projects, and has a growing involvement in the natural gas transmission and midstream businesses. As a distributor of energy, Enbridge owns and operates Canada’s largest natural gas distribution company, which provides gas to 1.5 million customers in Ontario, Quebec and New York State. Enbridge is also involved in the distribution of electricity, and provides retail energy products and services to a growing number of Canadian and United States markets. The Company employs approximately 5,500 people, primarily in Canada, the United States and Latin America. Enbridge common shares trade on the Toronto Stock Exchange under the symbol “ENB”, and on The NASDAQ National Market in the United States under the symbol “ENBR”. Information about Enbridge is available on the World Wide Web at www.enbridge.com. Inuvik Norman Wells Zama Fort St. John Fort McMurray Edmonton Hardisty Ottawa Montreal Cornwall Casper Toronto Salt Lake City Dawn Chicago Toledo Patoka Liquids Pipelines Jose Terminal Gas Pipelines Coveñas Gas Distribution Cusiana/ Electric Power Distribution Cupiagua Gas Gathering and Processing Bogota Enbridge Inc. -

NAESB Members

North American Energy Standards Board Membership List As of July 31, 2021 NAESB membership extends to all employees of the member company, but does not extend to other companies with which the member company may have an organizational relationship – such as partnerships, liaisons, affiliates, subsidiaries, holding companies or parent companies. Should those companies be interested in joining they would hold separate memberships. Membership is specific to the quadrant(s) and segment(s) in which the company holds membership. Should an individual wish to represent a quadrant or segment in which the company member does not hold a membership, that individual will be considered a non-member. To obtain information on membership or verify membership status, please contact the NAESB Office ([email protected]). NAESB Membership Report - Quadrant/Segment Membership Analysis Number of Members WGQ Segments TOTAL 114 End Users 15 Distributors 22 Pipelines 35 Producers 9 Services 33 RMQ Segments TOTAL 36 Retail Electric End Users/Public Agencies 17 Retail Gas Market Interests Segment 8 Retail Electric Utilities 6 Retail Electric Service Providers/Suppliers 5 WEQ Segments TOTAL 131 End Users 15 Distributors 17 Transmission 41 Generation 20 Marketers 20 None Specified 1 Independent Grid Operators/Planners 7 Technology /Services 10 Total Membership 281 Page 1 North American Energy Standards Board Membership List As of July 31, 2021 Organization Seg1 Contact Retail Markets Quadrant (RMQ) Members: 1 Agility CIS s Mary Do 2 American Public Gas Association (APGA) g Donnie Sharp 3 Big Data Energy Services s J. Cade Burks, Jennifer Teel 4 California Energy Commission e Melissa Jones 5 California Public Utilities Commission e Katherine Stockton 6 CenterPoint Energy Houston Electric, LLC u John Hudson 7 City of Houston e Ray Cruz 8 Dominion Energy u Brandon Stites 9 Duke Energy Corporation u Stuart Laval, David Lawrence 10 Electric Reliability Council of Texas, Inc.