Program Performance Audit Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LPG PIPELINE PROJECT (Loan 1591-IND)

ASIAN DEVELOPMENT BANK PCR:IND 28033 PROJECT COMPLETION REPORT ON THE LPG PIPELINE PROJECT (Loan 1591-IND) IN INDIA September 2003 CURRENCY EQUIVALENTS Currency Unit – Indian rupee/s (Re/Rs) At Appraisal At Project Completion (22 September 1997) (1 March 2001) Re1.00 = $0.028 $0.022 $1.00 = Rs36.14 Rs45.61 ABBREVIATIONS ADB – Asian Development Bank APPS – application software EIL – Engineers India Limited EIRR – economic internal rate of return FIRR – financial internal rate of return GAIL – Gas Authority of India Limited HAZOP – hazardous operation HDD – horizontal directional drilling IDC – interest during construction LA – Loan Agreement LNG – liquefied natural gas LPG – liquefied petroleum gas RPL – Reliance Petroleum Limited SCADA – supervisory control and data acquisition WEIGHTS AND MEASURES bm3 (billion cubic meter) – 1,000,000,000 m3 bars (pressure unit) – 1.019 kg/cm2 cm (centimeter) – 10 millimeters hp (horsepower) – 746 watts kg (kilogram) – 1,000 grams km (kilometer) – 1,000 meters MMCM (million metric cubic meters) – unit of gas volume MMTPA (million metric tons per annum) – unit of mass of LPG MMSCMD (million standard cubic meters per day) – unit of gas volume per day t (ton [metric]) – 1,000 kilograms NOTES (i) The fiscal year (FY) of the Government and Gas Authority of India Limited ends on 31 March. FY before a calendar year denotes the year in which the fiscal year ends. For example, FY2003 begins on 1 April 2002 and ends on 31 March 2003. (ii) In this report, “$” refers to US dollars. CONTENTS Page BASIC DATA iii MAP vii I. PROJECT DESCRIPTION 1 II. EVALUATION OF DESIGN AND IMPLEMENTATION 2 A. -

India: Inventory of Estimated Budgetary Support and Tax Expenditures for Fossil-Fuels

INDIA: INVENTORY OF ESTIMATED BUDGETARY SUPPORT AND TAX EXPENDITURES FOR FOSSIL-FUELS Energy resources and market structure India is one of the fastest growing energy markets in the world. The country is the world’s third largest coal producer owing to its large deposits. Coal is the leading primary fuel in India’s energy mix, accounting for 44% of the country’s total primary energy supply (TPES), with thermal power plants making up the majority of coal consumption. Biomass accounts for 25% of total energy use, followed by oil and natural gas, which account respectively for 22% and 7% of the country’s energy needs. Remaining energy sources, such as nuclear power and hydro-electricity, account for about 1% each. The country’s proven reserves of oil were 5.5 billion barrels as of December 2012; nonetheless, domestic production falls far short of domestic demand and the country depends heavily on imported crude oil. The state-owned coal company, Coal India Limited (CIL), retains a near monopoly of coal extraction, with over 90% of domestic coal extraction attributed to government-controlled mines. Most coal mining occurs in the states of Bihar, Chhattisgarh, Jharkhand, Madhya Pradesh, Orissa, and West Bengal. Market reforms are being implemented to bring competition and transparency to the coal sector. The government has been grappling to get an effective regulatory framework in place, which includes the loosening of regulations for the coal industry, with the objective of moving some grades of coal closer to international market prices, and allocating additional coal blocks through a transparent open bidding process. -

Government of India Ministry of Micro, Small and Medium Enterprises

GOVERNMENT OF INDIA MINISTRY OF MICRO, SMALL AND MEDIUM ENTERPRISES LOK SABHA UNSTARRED QUESTION NO. 4232 TO BE ANSWERED ON 07.01.2019 PUBLIC PROCUREMENT POLICY 4232. SHRI ADHALRAO PATIL SHIVAJIRAO: SHRI SHRIRANG APPA BARNE: SHRI KUNWAR PUSHPENDRA SINGH CHANDEL: DR. SHRIKANT EKNATH SHINDE: SHRI ANANDRAO ADSUL: SHRI VINAYAK BHAURAO RAUT: Will the Minister of MICRO, SMALL AND MEDIUM ENTERPRISES be pleased to state: (a) the details of the total annual procurement of goods and services by each Public Sector Enterprise (PSE) in the year 2014-15, 2015-16, 2016-17 and 2017-18; (b) the quantity of calculated value of goods and services procured under Public Procurement Policy Order, 2012 during the said period in each PSE; (c) the status of procurement under this policy from MSMEs owned by SC/ST and non-SC/STs during the said period by each PSE; (d) whether the public procurement policy is not being complied with by many Government departments/PSEs; and (e) if so, the details thereof and the reasons therefor along with corrective steps taken/being taken by the Government in this regard? ANSWER MINISTER OF STATE (INDEPENDENT CHARGE) FOR MICRO, SMALL AND MEDIUM ENTERPRISES (SHRI GIRIRAJ SINGH) (a) to (e): The details of annual procurement of goods & services by the Central Public Sector Enterprise (CPSE) as per information provided by Department of Public Enterprises (DPE) are as under: Year No. of Total Procurement Procurement from MSEs CPSEs Procurement From MSEs owned by SC/ST (Rs. in Crore) (Rs. in Crore) Entrepreneur (Rs. in Crore) 2014-15 133 131766.86 15300.57 59.37 2015-16 132 279167.15 12566.15 50.11 2016-17 142 245785.31 25329.44 400.87 2017-18 169 280785.49 24226.51 442.52 Ministry of MSME has taken several measures for effective implementation of the Public Procurement Policy. -

India CCS Scoping Study: Final Report

January 2013 Project Code 2011BE02 India CCS Scoping Study: Final Report Prepared for The Global CCS Institute © The Energy and Resources Institute 2013 Suggested format for citation T E R I. 2013 India CCS Scoping Study:Final Report New Delhi: The Energy and Resources Institute. 42pp. [Project Report No. 2011BE02] For more information Project Monitoring Cell T E R I Tel. 2468 2100 or 2468 2111 Darbari Seth Block E-mail [email protected] IHC Complex, Lodhi Road Fax 2468 2144 or 2468 2145 New Delhi – 110 003 Web www.teriin.org India India +91 • Delhi (0)11 ii Table of Contents 1. INTRODUCTION ..................................................................................................................... 1 2. COUNTRY BACKGROUND ...................................................................................................... 1 3. CO2 SOURCES ......................................................................................................................... 7 4. CURRENT CCS ACTIVITY IN INDIA ..................................................................................... 15 5. ECONOMIC ANALYSIS .......................................................................................................... 19 6. POLICY & LEGISLATION REVIEW ......................................................................................... 26 7. CAPACITY ASSESSMENT ...................................................................................................... 27 8. BARRIERS TO CCS IMPLEMENTATION IN INDIA ............................................................... -

Nayara Energy Limited Annual Report 2015-16

Excellence Breeds Success 2015-16 Annual Report Essar Oil limited Contents 01-13 COMPANY OVERVIEW Excellence Breeds Success 01 Key Performance Indicators 02 Chairman’s Message 04 MD & CEO’s Message 06 Night view of Vadinar Refinery Board of Directors 10 Senior Management 12 14-49 STATUTORY REPORT Directors' Report 14 Indradhanush – Shiksha ke Saat Rang. Committed to 50-168 FINANCIAL STATEMENTS Nation Building Cover Images Standalone Independent Auditors’ Report 50 02 Balance Sheet 58 Statement of Profit and Loss 59 01 03 Cash Flow Statement 60 04 Notes to Financial Statements 62 Consolidated 01 Vacuum Column in CDU-1 Complex Independent Auditors’ Report 109 Partners in Progress through Consolidated Balance Sheet 114 02 education Statement of Consolidated Profit and Loss 115 Product jetty, pipeline Consolidated Cash Flow Statement 116 03 Notes to Consolidated Financial Statements 118 04 Retail outlet in Bhuj, Gujarat Form AOC - 1 168 NOTICE For more details, Please visit: 169-194 www.essaroil.co.in Excellence breeds success In a period that was marked by global line with the philosophy to incubate, The year volatility and a severe downturn in nurture and scale up ideas into world- 2015-16 has been crude prices, we have reported our class businesses and create value for best-ever results. Our refinery clocked all stakeholders, the promoters have a landmark one for the highest current price Gross decided to sell 98% of Essar oil to the us at Essar Oil. We Refining Margin, leading to the highest world’s leading oil and gas companies. have successfully ever EBIDTA and Profit After Tax in our We are proud to be the source of the history. -

Government of India Ministry of Heavy Industries and Public Enterprises Department of Public Enterprises

GOVERNMENT OF INDIA MINISTRY OF HEAVY INDUSTRIES AND PUBLIC ENTERPRISES DEPARTMENT OF PUBLIC ENTERPRISES LOK SABHA UNSTARRED QUESTION NO. 1428 TO BE ANSWERED ON THE 11th FEBRUARY, 2020 ‘Job Reservation for SCs, STs and OBCs in PSUs’ 1428. SHRI A.K.P. CHINRAJ : SHRI A. GANESHAMURTHI : Will the Minister of HEAVY INDUSTRIES AND PUBLIC ENTERPRISES be pleased to state:- (a) whether the Government is planning to revamp job reservations issue for Scheduled Castes (SCs), Scheduled Tribes (STs) and Other Backward Classes (OBCs) in State-run companies following sharp fall of employment opportunities to them consequent upon disinvestment in all the Public Sector Enterprises (PSEs); (b) if so, the details thereof; (c) whether it is true that the Department of Investment and Public Asset Management (DIPAM) is examining the issue of job reservations for SCs, STs and OBCs in State run companies following disinvestment and if so, the details thereof; (d) the total disinvestment made in various PSEs company and category-wise during the last three years along with the reasons for disinvestment; (e) the total number of SCs, STs and OBCs presently working in various PSEs company and category-wise; and (f) the total number of SCs, STs and OBCs who lost their jobs in these companies during the said period? ANSWER THE MINISTER FOR HEAVY INDUSTRIES & PUBLIC ENTERPRISES (SHRI PRAKASH JAVADEKAR) (a to d): Job reservation is available to Scheduled Castes (SCs), Scheduled Tribes (STs) and Other Backward Classes (OBCs) in Central Public Sector Enterprises (CPSEs) as per the extant Government policy. The Government follows a policy of disinvestment in CPSEs through Strategic Disinvestment and Minority Stake sale. -

Evolution of Brazil-India Economic and Trade Relations: the Future Prospect

Brazil-India: 70 Years of Diplomatic Relations Evolution of Brazil-India Economic and Trade Relations: The Future Prospect Pranav Kumar Head - International Trade Policy Confederation of Indian Industry New Delhi India and Brazil Economy – Key Features Brazil India • The Brazilian economy is among • India is the world’s seventh-largest the ten largest in the world. economy. India is growing Economic activity is relatively faster than any other large diversified, with the GDP share of economy except for China. While services on an upward trend and focus is on reviving manufacturing, those of manufacturing and mining but services sector continues to be on a downward path. the main pillar of economy. • UNCTAD named India as the 9th • UNCTAD named Brazil the 7th largest destination for global FDI largest destination for global FDI flow in 2016. flow in 2016. • Labour intensive manufacturing • Agriculture exports continued to and services like ITES have largest dominate, increasing their share in share in India’s exports. total exports from 35.6% in 2012 to 41.5% in 2016. © Confederation of Indian Industry India-Brazil Bilateral Trade • Brazil is one of the most important trading partners of India in the entire LAC (Latin America and Caribbean) region. India-Brazil bilateral trade has increased substantially in the last two decades. However, given the economic recession in Brazil, the volume of trade continued to decrease since 2014-15. • India and Brazil have reasonably diversified trade basket. While India’s exports to Brazil includes petroleum, polyester yarn, chemical products, drugs and cotton yarn, Brazilian exports to India includes mainly crude oil, cane sugar, copper ore, soya oil • Indian exports to Brazil stood at US$2.48bn in year 2016-17 as against US$5.9bn in 2014-15. -

Essar Oil Limited (Registered Office Address: Khambhalia Post, Post Box

ESSAR OIL LIMITED (REGISTERED OFFICE ADDRESS: KHAMBHALIA POST, POST BOX. NO.24, DIST. JAMNAGAR – 361305, GUJARAT) REVISED FINANCIAL STATEMENTS 2009 - 10 AMENDMENT TO THE DIRECTORS’ REPORT FOR THE FINANCIAL YEAR 2009-10 To, The Members of Essar Oil Limited The Board of Directors had adopted its report on the financial statements for the financial year 2009-10 on July 26, 2010. Sales Tax Incentive The Hon’ble Supreme Court of India, on January 17, 2012, allowed an appeal filed by the Gujarat Government and set aside a judgment of the Gujarat High Court dated April 22, 2008, thus denying the Company benefits under a sales tax incentive scheme of the Government of Gujarat. Hence, the sales tax amount collected and retained by the Company from May 1, 2008 to January 17, 2012 became payable and the income arising out of defeasement of sales tax liability need to be reversed. The Company proposes to re-open the books of accounts for three financial years 2008-09, 2009-10 and 2010-11 for the limited purpose of reflecting a true and fair view in the books of account. The Company has received approval from the Ministry of Corporate Affairs for the above purpose. Necessary resolution seeking approval of shareholders for re-opening of the said financial statements has been incorporated in nd the Notice dated November 9, 2012 convening the 22 Annual General Meeting on December 20, 2012. Abridged reopened and revised financial statements for the financial year ended on March 31, 2010 form part of the annual report. Consequent to reopening of books -

CHAPTER - I Through International Competitive Biddings in a 1

CHAPTER - I through international competitive biddings in a 1. INTRODUCTION deregulated scenario. Appraisal of 35% of the total sedimentary basins is targeted together with 1.1 The Ministry of Petroleum & Natural Gas acquisition of acreages abroad and induction of (MOP&NG) is concerned with exploration & advanced technology. The results of the initiatives production of oil & natural gas (including import taken since 1999 have begun to unfold. of Liquefied Natural Gas), refining, distribution & 1.8 ONGC-Videsh Limited (OVL) a wholly owned marketing, import, export and conservation of subsidiary of ONGC is pursing to acquire petroleum products. The work allocated to the exploration acreage and oil/gas producing Ministry is given in Appendix-I. The names of the properties abroad. OVL has already acquired Public Sector Oil Undertakings and other discovered/producing properties in Vietnam (gas organisations under the ministry are listed in field-45% share), Russia (oil & gas field – 20% Appendix-II. share) and Sudan (oil field-25% share). The 1.2 Shri Ram Naik continued to hold the charge as production from Vietnam and Sudan is around Minister of Petroleum & Natural Gas during the 7.54 Million Metric Standard Cubic meters per financial year 2003-04. Smt. Sumitra Mahajan day (MMSCMD) of gas and 2,50,000 barrels of assumed the charge of Minister of State for oil per day (BOPD) respectively. The first Petroleum & Natural Gas w.e.f 24.05.2003. consignment of crude oil from Sudan project of OVL was received in May, 2003 by MRPL 1.3 Shri B.K. Chaturvedi continued to hold the charge (Mangalore Refinery Petrochemicals Limited) in as Secretary, Ministry of Petroleum & Natural Gas. -

PRSI National Awards-2020 Winners

PRSI NATIONAL AWARDS- 2020 Results Public Relations Society of India www. prsi.org.in PRSI NATIONAL AWARDS - 2020 No of S No Category Name of Organization entries 1 First Prize HP Samachar Hindustan Petroleum Corporation Ltd – Mumbai House Journal (Hindi) Second Petroleum Swar Prize Bharat Petroleum Corporation Ltd – Mumbai Third Prize Prayas Numaligarh Refinery Limited – Guwahati 2 First Prize Sail News House Journal (English) Steel Authority of India - New Delhi First Prize Varta Garden Reach Shipbuilders & Engineers Ltd. Second HP News Prize Hindustan Petroleum Corporation Ltd – Mumbai Second Kribhco News Prize Kribhco, Noida Third Prize IndianOil News Indian Oil Corporation - Marketing Division HO,Mumbai 3 Newsletter (English) First Prize Heritage Institute of Technology / Kalyan Bharti Trust, kolkata Second Ordnance Factory Board (OFB), Prize Kolkata Third Prize Aditya Birla Fashion & Retail Limited - Bengaluru, Karnataka / Mumbai 4 Third Prize Indian Oil Corporation Ltd - Barauni Newsletter (Hindi) Refinery ,Barauni 5 First Prize NTPC Ltd - New Delhi Special/Prestige Publication Second Steel Authority of India - New Delhi Prize Third Prize Indian Oil Corporation - Marketing Division (HO), Mumbai 6 Coffee Table Book First Prize Indian Oil Corporation - Marketing Division (HO) Second Garden Reach Shipbuilders & Prize Engineers Ltd. Kolkata Third Prize AIRADS Ltd. Third Prize Ordnance Factory Board (OFB) Kolkata 7 Sustainable Development Report First Prize ITC Ltd – Kolkata Second Indian Oil Corporation Ltd - Prize Corporate Office, New -

C:\Docume~1\Mahesh~1.Bud

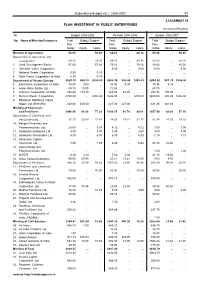

Expenditure Budget Vol. I, 2006-2007 39 STATEMENT 14 PLAN INVESTMENT IN PUBLIC ENTERPRISES (In crores of Rupees) Sl. Budget 2005-2006 Revised 2005-2006 Budget 2006-2007 No. Name of Ministry/Enterprise Total Budget Support Total Budget Support Total Budget Support Plan Plan Plan Outlay Equity Loans Outlay Equity Loans Outlay Equity Loans Ministry of Agriculture 58.00 ... 58.00 84.16 ... 84.16 50.00 ... 50.00 Department of Agriculture and Cooperation 58.00 ... 58.00 84.16 ... 84.16 50.00 ... 50.00 1. Land Development Banks 57.00 ... 57.00 79.16 ... 79.16 45.00 ... 45.00 2. Damodar Valley Corporation ... ... ... 5.00 ... 5.00 5.00 ... 5.00 3. National Seeds Corporation 0.30 ... 0.30 ... ... ... ... ... ... 4. State Farms Corporation of India 0.70 ... 0.70 ... ... ... ... ... ... Department of Atomic Energy 5529.70 568.10 2004.00 4205.38 300.05 1280.03 4294.34 991.19 1606.00 5. Electronics Corporation of India 34.00 9.00 ... 34.00 9.00 ... 39.34 9.34 ... 6. Indian Rare Earths Ltd. 85.10 10.00 ... 72.80 ... ... 80.79 ... ... 7. Uranium Corporation of India 280.60 119.10 ... 225.55 64.05 ... 292.36 100.00 ... 8. Nuclear Power Corporation 4700.00 ... 2004.00 3646.03 ... 1280.03 3400.00 400.00 1606.00 9. Bharatiya Nabhikiya Vidyut Nigam Ltd (BHAVINI) 430.00 430.00 ... 227.00 227.00 ... 481.85 481.85 ... Ministry of Chemicals and Fertilisers 1096.96 91.09 77.29 1109.35 41.70 80.61 1057.54 88.39 57.15 Department of Chemicals and Petrochemicals 97.70 53.60 21.00 49.33 18.21 31.12 91.46 47.53 18.15 10. -

IBEF Presentataion

OIL and GAS For updated information, please visit www.ibef.org November 2017 Table of Content Executive Summary……………….….…….3 Advantage India…………………..….……...4 Market Overview and Trends………..……..6 Porters Five Forces Analysis.….…..……...28 Strategies Adopted……………...……….…30 Growth Drivers……………………..............33 Opportunities…….……….......…………..…40 Success Stories………….......…..…...…....43 Useful Information……….......………….….46 EXECUTIVE SUMMARY . In FY17, India had 234.5 MMTPA of refining capacity, making it the 2nd largest refiner in Asia. By the end of Second largest refiner in 2017, the oil refining capacity of India is expected to rise and reach more than 310 million tonnes. Private Asia companies own about 38.21 per cent of total refining capacity World’s fourth-largest . India’s energy demand is expected to double to 1,516 Mtoe by 2035 from 723.9 Mtoe in 2016. Moreover, the energy consumer country’s share in global primary energy consumption is projected to increase by 2-folds by 2035 Fourth-largest consumer . In 2016-17, India consumed 193.745 MMT of petroleum products. In 2017-18, up to October, the figure stood of oil and petroleum at 115.579 MMT. products . India was 3rd largest consumer of crude oil and petroleum products in the world in 2016. LNG imports into the country accounted for about one-fourth of total gas demand, which is estimated to further increase by two times, over next five years. To meet this rising demand the country plans to increase its LNG import capacity to 50 million tonnes in the coming years. Fourth-largest LNG . India increasingly relies on imported LNG; the country is the fourth largest LNG importer and accounted for importer in 2016 5.68 per cent of global imports.