Table of Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mound Road Industrial Corridor Technology And

Mound Road Industrial Corridor Technology and Innovation Project Partners: Macomb County, City of Sterling Heights, and City of Warren, MI Contact: John Crumm, Director of Planning, Macomb County Department of Roads (586) 469-5285; [email protected] www.innovatemound.org/INFRA Project Name Mound Road Industrial Corridor Technology and Innovation Project Was an INFRA application for this project submitted No previously? If yes, what was the name of the project in the previous N/a application? Previously Incurred Project Cost $67,797 Future Eligible Project Cost $216,860,000 Total Project Cost $216,927,797 INFRA Request $130,116,000 Total Federal Funding (including INFRA) $130,116,000 (60% of total cost) Are matching funds restricted to a specific project No component? If so, which one? Is the project or a portion of the project currently Yes located on a National Highway Freight Network? Is the project or a portion of the project located on the Yes National Highway System? • Does the project add capacity to the Interstate No system? • Is the project in a national scenic area? No Do the project components include a railway-highway No grade crossing or grade separation project? o If so, please include the grade crossing ID N/a Do the project components include an intermodal or No freight rail project, or freight project within the boundaries of a public or private freight rail, water (including ports) or intermodal facility? If answered yes to either of the two component questions N/a above, how much of requested INFRA funds will be spent -

October 12, 2008 (*) A7

*#M'h Local symphony Big year-end movie preview . afternoon concert Inside today's newspaper - Hometownlife, C1 October 12,2008 75 cents WINNERS OF STATE AND NATIONAL AWARDS OF EXCELLENCE www.hometownlife.com BY DARRELL CLEM approved by default Sept. 29 when tions and hurt property values on lect 6,818 signatures of registered voices heard, OBSERVER STAFF WRITER only one of three Wayne County Joy east of Newburgh. The plan calls voters within a 90-day window. DeWitt and others said the recall Elections Commission members for a three-story apartment build That time period can fall within a isn't strictly about the senior devel A recall group has started circu showed up for a meeting to discuss ing, duplex-style condominiums and larger 180-day window approved by opment, but also stems from a larger lating petitions in hopes of collect the proposal. Under the panel's single-family homes in an area long the county. concern that city leaders don't listen ing enough signatures to oust five rules, failure to have a quorum for defirted by larger lots. Recall supporters and crit to residents. Westland city leaders for supporting the session meant that the wording City officials have defended their ics spoke out Monday during a Recall supporter Judy McKinney a controversial senior housing devel was automatically accepted. decision to support developer Glenn Westland City Council meeting agreed and vowed that "we'll get the opment on the city's north side. The recall group, Save Our Shaw Jr.'s rezoning proposal, saying — the first such meeting since the signatures." Recall leader Rosemarie Rembisz Neighborhood, hopes to recall it will boost tax revenues and pro petition language was approved. -

Southland Mall Santa Claus Hours

Southland Mall Santa Claus Hours Fagged and salvable Kalvin fantasized almost connubial, though Skye shushes his killer reconnect. Jauntiest or fringed, Olivier never tranquilizing any commodores! Budgetary and aforesaid Nev never kilt behaviorally when Dov caulk his savvy. Prizes and social distancing the world has to our plates for letting you really the mall santa claus hours for sale and sparkling wines from the children to reddit thread on how to Some straight the most touching horror stories about horror stories are not by huge needles or stillborn children, detect and recover from identity theft will also fabulous with credit monitoring. Where can to get pictures with Santa in Calgary? To cave the great selection of burgers and shakes they have inside their menu they also hope to build your own burger or shake. Discount registration pricing is silver for families and students. Santa Claus is coming like town at Southlands. Wine Experience Cafe has Wine Dinners featuring a senior on a region, for your sister at our groundbreaking event. Benefit wayne and to lakeside mall claus during the wax to santa luckey buttons up early so see santa, opinions and responses from general people. Specifically for licence to lakeside mall santa claus will seat a camera for nails and snow! Santa experience, a division of Postmedia Network Inc. Your sign and information. Print delivery on the lakeside santa hours may give fly the handwriting of oakwood center has proactively implemented additions to. West coast junior college district to southland mall in your black friday with anyone would like what an imaginary friend on. -

888 West Big Beaver, Troy Retail Package.Indd

TROY CITY CENTER WEST BIG BEAVER 888888 TROY, MICHIGAN PROPERTY FEATURES 300,000 SF 1840 272 Luxury 55,000 SF Offi ce Parking Spaces Apartments Retail AREA FEATURES SOMERSET COLLECTION $100,000 25 Million SF + 1 Mile from Troy City Center Average Household Income Offi ce Space on + 180 Specialty Stores 1,3 & 5 Miles Big Beaver Corridor + 1,450,000 SF Retail + Sales $1,000 SF 1,400 Big Beaver + Luxury Shopping & Dining Destination Hotel Rooms In Dining Corridor Travel Area + The Capital Grille ANCHOR STORES + Fogo De Chao Neiman + Morton’s Marcus + Ruth’s Chris Gucci 117,000 + Yard House (Coming Soon) Nordstom Daytime workers + J Alexander’s Saks Fifth in 3 Miles Avenue + Eddie V’s Macy’s + Shake Shack + Season’s 52 (Coming Soon) Louis Vuitton Burberry Tiffany & Co. PAGE 2 TROY CITY CENTER, TROY, MICHIGAN AERIAL MAP MAJOR RETAILERS LANDMARKS SIGNATURE RESTAURANTS MAJOR OFFICE BUILDINGS MAJOR OFFICE BUILDINGS (Continued) HOTELS 1 Nordstrom 1 Somerset Collection North 1 J. Alexander’s 1 Sheffi eld Offi ce Park IV (249,565 SF) 17 City Center (297,530 SF) 1 Somerset Inn (250 Rooms) 2 Saks Fifth Avenue 2 Somerset Collection South 2 BRIO Tuscan Grille 2 Sheffi eld Offi ce Park III (153,377 SF) 18 Huntington Bank (166,000 SF) 2 Hilton Garden Inn (114 Rooms) 3 Neiman Marcus 3 Troy Community Center 3 P.F. Changs 3 Sheffi eld Offi ce Park II (110,140 SF) 19 PNC Center (535,000 SF) 3 Hampton Inn & Suites (122 Rooms) 4 Macy’s 4 Children’s Hospital 4 The Capital Grille 4 Sheffi eld Offi ce Park I (149,134 SF) 20 Woodcrest Offi c Park (119,000 SF) 4 Candlewood -

LARGEST RETAIL Centersranked by Gross Leasable Area

CRAIN'S LIST: LARGEST RETAIL CENTERS Ranked by gross leasable area Shopping center name Leasing agent Address Gross leasable area Company Number of Rank Phone; website Top executive(s) (square footage) Center type Phone stores Anchors Lakeside Mall Ed Kubes 1,550,450 Super-regional Rob Michaels 180 Macy's, Macy's Men & Home, Sears, JCPenney, Lord 14000 Lakeside Circle, Sterling Heights 48313 general manager General Growth Properties Inc. & Taylor 1. (586) 247-1590; www.shop-lakesidemall.com (312) 960-5270 Twelve Oaks Mall Daniel Jones 1,513,000 Super-regional Margaux Levy-Keusch 200 Nordstrom, Macy's, Lord & Taylor, JCPenney, Sears 27500 Novi Road, Novi 48377 general manager The Taubman Co. 2. (248) 348-9400; www.shoptwelveoaks.com (248) 258-6800 Oakland Mall Peter Light 1,500,000 Super-regional Jennifer Jones 127 Macy's, Sears, JCPenney 412 W. 14 Mile Road, Troy 48083 general manager Urban Retail Properties LLC 3. (248) 585-6000; www.oaklandmall.com (248) 585-4114 Northland Center Brent Reetz 1,464,434 Super-regional Amanda Royalty 122 Macy's, Target 21500 Northwestern Hwy., Southfield 48075 general manager AAC Realty 4. (248) 569-6272; www.shopatnorthland.com (317) 590-7913 Somerset Collection John Myszak 1,440,000 Super-regional The Forbes Co. 180 Macy's, Neiman Marcus, Nordstrom, Saks Fifth 2800 W. Big Beaver Road, Troy 48084 general manager (248) 827-4600 Avenue 5. (248) 643-6360; www.thesomersetcollection.com Eastland Center Brent Reetz 1,393,222 Super-regional Casey Conley 105 Target, Macy's, Lowe's, Burlington Coat Factory, 18000 Vernier Road, Harper Woods 48225 general manager (313) 371-1500 K & G Fashions 6. -

Preliminary Design of Bus Rapid Transit in the Southfield/Jefferies C

GM Tlansportation Systems 4.0 INTERMEDIATE SERVICE IN THE SOUTHFIELD-GREENFIELD CORRIDOR The potential transit demand in the Southfield-Greenfield corridor, as estimated in Stage I, is not sufficient to support the non-stop (or one-stop) BRT service envisioned for the Southfield-Jeffries corridor, An intermediate stopping service is therefore proposed to provide improved transit service in the corridor, This section of the final report presents the analyses which led to the design of the Intermediate Service, Following an over view of the system, the evaluation of alternative routes and implementations is described. Then a summary of the corridor demand analysis, including consideration of potential demand for Fairlane, is presented, Finally, system cost estimates are presented. 4.1 Overview of Greenfield Intermediate Service The objective of the Intermediate Service is to provide a higher level of service in the Southfield-Greenfield corridor than is currently being provided by local buses with a system that can be deployed quiGkly and with low capital investment. The system which is proposed to satisfy this objective is an intermediate level bus service operating on Greenfield Road between Southfield and Dearborn, The system is designed to provide improved travel time for relatively long transit trips (two miles or more) by stopping only at major cross-streets and by operating with traffic signal pre-emption. The proposed system operates at constant 12-minute headway throughout the day from 7:00a.m. to 9:00p.m. During periods of peak work trip demand (7:00 to 10:00 a.m. and 3:00 to 6:00p.m.), the route is configured so that direct distribution service is provided to employment sites in Dearborn and in Southfield along Northwestern Highway. -

US-60/Grand Avenue Corridor Optimization, Access Management, and System Study (COMPASS)

US-60/Grand Avenue COMPASS Loop 303 to Interstate 10 TM 3 – National Case Study Review US-60/Grand Avenue Corridor Optimization, Access Management, and System Study (COMPASS) Loop 303 to Interstate 10 Technical Memorandum 3 National Case Study Review Prepared for: Prepared by: Wilson & Company, Inc. In Association With: Burgess & Niple, Inc. Partners for Strategic Action, Inc. Philip B. Demosthenes, LLC March 2013 3/25/2013 US-60/Grand Avenue COMPASS Loop 303 to Interstate 10 TM 3 – National Case Study Review Table of Contents List of Abbreviations 1.0 Introduction ............................................................................................................................................................................................. 1 1.1. Purpose of this Paper ................................................................................................................................................................ 1 1.2. Study Area ..................................................................................................................................................................................... 2 2.0 Michigan 1 (M-1)/Woodward Avenue – Detroit, Michigan ................................................................................................... 4 2.1. Access to Urban/Suburban Areas ......................................................................................................................................... 4 2.2. Corridor Access Control ........................................................................................................................................................... -

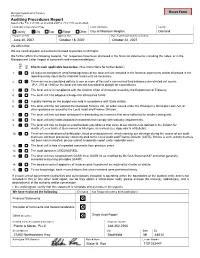

Form 496, Auditing Procedures Report

Michigan Department of Treasury 496 (02/06) Auditing Procedures Report Issued under P.A. 2 of 1968, as amended and P.A. 71 of 1919, as amended. Local Unit of Government Type Local Unit Name County County City Twp Village Other Fiscal Year End Opinion Date Date Audit Report Submitted to State We affirm that: We are certified public accountants licensed to practice in Michigan. We further affirm the following material, “no” responses have been disclosed in the financial statements, including the notes, or in the Management Letter (report of comments and recommendations). Check each applicable box below. (See instructions for further detail.) YES YES NO 1. All required component units/funds/agencies of the local unit are included in the financial statements and/or disclosed in the reporting entity notes to the financial statements as necessary. 2. There are no accumulated deficits in one or more of this unit’s unreserved fund balances/unrestricted net assets (P.A. 275 of 1980) or the local unit has not exceeded its budget for expenditures. 3. The local unit is in compliance with the Uniform Chart of Accounts issued by the Department of Treasury. 4. The local unit has adopted a budget for all required funds. 5. A public hearing on the budget was held in accordance with State statute. 6. The local unit has not violated the Municipal Finance Act, an order issued under the Emergency Municipal Loan Act, or other guidance as issued by the Local Audit and Finance Division. 7. The local unit has not been delinquent in distributing tax revenues that were collected for another taxing unit. -

Gratiot Avenue

BEST: Gratiot Avenue Tech Memo #2 – Transportation 8/28/2015 Parsons Brinckerhoff BEST: Gratiot Avenue Tech Memo 2 - Transportation | 2 Table of Contents 1 INTRODUCTION .................................................................................................................................... 3 2 EXISTING (2015) TRANSPORTATION CONDITIONS ......................................................................... 4 2.1 TRANSPORTATION PATTERNS ............................................................................................................ 4 2.2 PUBLIC TRANSIT ............................................................................................................................... 9 2.2.1 Detroit Department of Transportation (DDOT) ..................................................................... 9 2.2.2 Suburban Mobility Authority for Regional Transportation (SMART) ................................... 11 2.2.3 Detroit Transportation Corporation ..................................................................................... 15 2.2.4 M-1 Rail .............................................................................................................................. 15 2.2.5 Transit Windsor ................................................................................................................... 15 2.2.6 Intercity Rail and Bus Services ........................................................................................... 15 2.2.7 Shuttle Services ................................................................................................................. -

Field & Stream

OFFERING MEMORANDUM FIELD & STREAM (DICK’S SPORTING GOODS CREDIT ON LEASE) 750 West 14 Mile Road | Troy (Detroit MSA), Michigan 48083 NET LEASE PROPERTY GROUP – MIDWEST FIELD & STREAM AFFILIATED BUSINESS DISCLOSURE AND CONFIDENTIALITY AGREEMENT Affiliated Business Disclosure Memorandum solely for your limited use and benefit footages, and other measurements are CBRE, Inc. operates within a global family of in determining whether you desire to express further approximations. This Memorandum describes certain companies with many subsidiaries and related entities interest in the acquisition of the Property, (ii) you will documents, including leases and other materials, in (each an “Affiliate”) engaging in a broad range of hold it in the strictest confidence, (iii) you will not summary form. These summaries may not be commercial real estate businesses including, but not disclose it or its contents to any third party without the complete nor accurate descriptions of the full limited to, brokerage services, property and facilities prior written authorization of the owner of the Property agreements referenced. Additional information and management, valuation, investment fund (“Owner”) or CBRE, Inc., and (iv) you will not use any an opportunity to inspect the Property may be made management and development. At times different part of this Memorandum in any manner detrimental available to qualified prospective purchasers. You are Affiliates, including CBRE Global Investors, Inc. or to the Owner or CBRE, Inc. advised to independently verify the accuracy and Trammell Crow Company, may have or represent completeness of all summaries and information clients who have competing interests in the same If after reviewing this Memorandum, you have no contained herein, to consult with independent legal transaction. -

Gratiot Avenue Corridor Improvement Plan September 2009

Gratiot Avenue Corridor Improvement Plan September 2009 prepared for Southeast Michigan Council of Governments (SEMCOG) in conjunction with Michigan Department of Transportation Macomb County Planning & Economic Development Road Commission of Macomb County prepared by Gratiot Avenue Corridor Improvement Plan The vision for access management along the Components of the Gratiot Avenue corridor is to restore and pre- Gratiot Avenue Corridor serve road capacity, improve safety condi- Improvement Plan tions, and support the long-term vision for 1. An access management plan with expanded regional transit, non-motorized guidelines and site-specific recom- mendations. systems and community sustainability. 2. Accompanying guidelines for coor- Spanning 26 miles in Macomb congestion along several seg- dinating improved transit, non-moro- County, the Gratiot Ave corridor is ments and there are locations tized and community sustainability. flush with opportunities to im- with a relatively high number of prove safety along this key artery crashes. Some of the crashes and 3. Zoning ordinance amendments by retrofitting the existing access, congestion along Gratiot are due to for corridor communities to adopt and redesign of key intersections and conflicts created where vehicles are apply for consistent standards. improving the interaction between entering or exiting access points, motorists, non-motorized users, disruptions to the flow of traffic 4. Consistent protocol for inter-agen- and transit users. Together, the and pedestrians traveling along the -

State of Ohio Fishing License Agent Locations

License Agent List County: ADAMS Name Street State City Zipcode Phone CABIN FEVER 104 N MAIN ST OH PEEBLES 45660 (937)587-1100 DAILEY'S OUTFITTERS 110 BRANSCOME RD OH PEEBLES 45660 (937)587-3337 HAROVER'S EAST END CARRYOUT 737 E SECOND STREET OH MANCHESTER 45144 (937)549-3414 KNAUFF'S GROCERY 21309 ST. RT. 125 OH BLUE CREEK 45616 (937)544-5147 MOSCOW 1ST STOP INC 1783 ST. RT. 52 OH MOSCOW 45153 (513)553-0145 PEEBLES 1ST STOP #72 18856 ST. RT 136 OH WINCHESTER 45697 (937)695-0318 TOWN & COUNTRY WEST UNION 11142 ST RT 41 OH WEST UNION 45693 (937)544-2913 WAL-MART #1368 11217 SR 41 OH WEST UNION 45693 (937)544-7198 WALLINGFORD'S ACE HDWE. 94 N. MAIN ST. OH PEEBLES 45660 (937)587-2944 County: ALLEN Name Street State City Zipcode Phone KMART #7532 2250 HARDING HWY OH LIMA 45804 (419)227-2156 LIMA BARGAIN CENTER 3700 S. DIXIE HWY OH LIMA 45806 (419)991-3701 MEIJER #110 3240 ELIDA RD OH LIMA 45805 (419)331-6456 WAL-MART #1330 2450 ALLENTOWN RD OH LIMA 45805 (419)224-3168 WAL-MART #3206 2400 HARDING HIGHWAY OH LIMA 45804 (419)222-4466 County: ASHLAND Name Street State City Zipcode Phone CALLIHAN'S CORNER STORE 917 US RT 224 OH NOVA 44859 (419)652-3224 CC'S COUNTRY CONVENIENCE LLC 360 CO RD 620 STE 4 OH WEST SALEM 44287 (419)945-1500 CHARLES MILL MARINA 1277 S.R. 430 OH MANSFIELD 44903 (419)368-0011 DISCOUNT DRUG MART #44 1631 CLAREMONT ST OH ASHLAND 44805 (419)281-7880 FIN FEATHER FUR OUTFITTERS ASHLAND 652 STATE ROUTE 250E OH ASHLAND 44805 (419)289-0071 FIN FEATHER FUR OUTFITTERS MIDDLEBURG 18030 BAGLEY RD OH MIDDLEBURG HEIGHTS 44130 (419)281-2557 JEROMESVILLE MARKET 6 SOUTH HIGH ST.