Dividend Announcement - Convenience Translation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Tax Appeals Rules Procedures

Tax Appeals Tribunal Rules & Procedures The rules of the game February 2017 Glossary of terms KRA Kenya Revenue Authority TAT Tax Appeals Tribunal TATA Tax Appeals Tribunal Act TPA Tax Procedures Act VAT Value Added Tax 2 © Deloitte & Touche 2017 Definition of terms Tax decision means: a) An assessment; Tax law means: b) A determination of tax payable made to a a) The Tax Procedures Act; trustee-in-bankruptcy, receiver, or b) The Income Tax Act, Value Added liquidator; Tax Act, and Excise Duty Act; and c) A determination of the amount that a tax c) Any Regulations or other subsidiary representative, appointed person, legislation made under the Tax director or controlling member is liable Procedures Act or the Income Tax for under specified sections in the TPA; Act, Value Added Tax Act, and Excise d) A decision on an application by a Duty Act. taxpayer to amend their self-assessment return; Objection decision means: e) A refund decision; f) A decision requiring repayment of a The Commissioner’s decision either to refund; or allow an objection in whole or in part, or g) A demand for a penalty. disallow it. Appealable decision means: a) An objection decision; and b) Any other decision made under a tax law but excludes– • A tax decision; or • A decision made in the course of making a tax decision. 3 © Deloitte & Touche 2017 Pre-objection process; management of KRA Audit KRA Audit Notes The TPA allows the Commissioner to issue to • The KRA Audits are a tax payer a default assessment, amended undertaken by different assessment or an advance assessment departments of the KRA that (Section 29 to 31 TPA). -

Overview of the SWISS TAX SYSTEM

OVERVIEW OF THE SWISS TAX SYSTEM 10.1 Taxation of Corporate Taxpayers ...................................... 109 10.2 Tax Rate in an International Comparison ........................ 112 10 10.3 Taxation of Individual Taxpayers ..................................... 113 10.4 Withholding Tax ................................................................ 116 10.5 Value Added Tax................................................................ 117 10.6 Other Taxes........................................................................ 120 10.7 Double Tax Treaties .......................................................... 121 10.8 Corporate Tax Reform III .................................................. 121 10.9 Transfer Pricing Rules....................................................... 121 Image Tax return, stock image The Swiss tax system mirrors Switzerland’s federal struc- 10.1 TAXATION OF CORPORATE TAXPAYERS ture, which consists of 26 sovereign cantons with 2,352 10.1.1 Corporate Income Tax – Federal Level independent municipalities. Based on the constitution, all The Swiss federal government levies corporate income tax at a flat rate of 8.5% on profit after tax of corporations and cooperatives. cantons have full right of taxation except for those taxes For associations, foundations, and other legal entities as well as that are exclusively reserved for the federal government. As investment trusts, a flat rate of 4.25% applies. At the federal level, no capital tax is levied. a consequence, Switzerland has two levels of taxation: the -

Chapter 17: Tax Treaties

Chapter 17 Tax Treaties www.pwc.com/mt/doingbusiness Doing Business in Malta Tax treaty policy Since the mid-seventies Malta has sought to expand its However, the tax levied on the companies under the Income tax treaty network. Most of Malta’s treaties are based Tax Act in such situations will be directly limited to 15% on the OECD model although some treaties (particularly as if the treaty rate applied to the company profits. Rather older ones) contain some material variations therefrom. than a refund on the payment of dividends the investors Some of them include special tax incentives for foreign can therefore qualify for the reduced rate at the company enterprises setting up manufacturing establishments in level at the time that the profits are derived and without Malta. These consist typically in low tax rates on dividends any obligation to distribute the profits to benefit from the arising in Malta supported by tax sparing provisions. Malta’s reduced tax rate. Maltese domestic law also provides that economic development, and particularly the growth in its no tax is payable by non-residents on interest and royalties financial services sector, expanded the scope for tax treaties arising in Malta, subject to certain conditions (see Chapter and in fact currently Malta has over 70 double taxation 11) and, as stated above, this rule applies irrespective of the agreements with almost all the important OECD countries. treaty provisions dealing with withholding taxes on these The current list of tax treaties is given in Appendix VII. categories of income. Similarly, no tax is payable by non- A tax treaty concluded by Malta becomes law by Ministerial residents on capital gains arising on transfers of company order and the provisions arising therefrom apply shares or securities, except where such gains are derived notwithstanding any provisions to the contrary under from the transfer of shares or securities in companies whose Maltese domestic tax law. -

Transfer of Ownership Guidelines

Transfer of Ownership Guidelines PREPARED BY THE MICHIGAN STATE TAX COMMISSION Issued October 30, 2017 TABLE OF CONTENTS Background Information 3 Transfer of Ownership Definitions 4 Deeds and Land Contracts 4 Trusts 5 Distributions Under Wills or By Courts 8 Leases 10 Ownership Changes of Legal Entities (Corporations, Partnerships, Limited Liability Companies, etc.) 11 Tenancies in Common 12 Cooperative Housing Corporations 13 Transfer of Ownership Exemptions 13 Spouses 14 Children and Other Relatives 15 Tenancies by the Entireties 18 Life Leases/Life Estates 19 Foreclosures and Forfeitures 23 Redemptions of Tax-Reverted Properties 24 Trusts 25 Court Orders 26 Joint Tenancies 27 Security Interests 33 Affiliated Groups 34 Normal Public Trades 35 Commonly Controlled Entities 35 Tax-Free Reorganizations 37 Qualified Agricultural Properties 38 Conservation Easements 41 Boy Scout, Girl Scout, Camp Fire Girls 4-H Clubs or Foundations, YMCA and YWCA 42 Property Transfer Affidavits 42 Partial Uncapping Situations 45 Delayed Uncappings 46 Background Information Why is a transfer of ownership significant with regard to property taxes? In accordance with the Michigan Constitution as amended by Michigan statutes, a transfer of ownership causes the taxable value of the transferred property to be uncapped in the calendar year following the year of the transfer of ownership. What is meant by “taxable value”? Taxable value is the value used to calculate the property taxes for a property. In general, the taxable value multiplied by the appropriate millage rate yields the property taxes for a property. What is meant by “taxable value uncapping”? Except for additions and losses to a property, annual increases in the property’s taxable value are limited to 1.05 or the inflation rate, whichever is less. -

The Cost of the Vote: Poll Taxes, Voter Identification Laws, and the Price of Democracy

File: Ellis final for Darby Created on: 4/9/2009 8:17:00 PM Last Printed: 5/19/2009 1:10:00 PM THE COST OF THE VOTE: POLL TAXES, VOTER IDENTIFICATION LAWS, AND THE PRICE OF DEMOCRACY ATIBA R. ELLIS† INTRODUCTION The election of Barack Obama as the forty-fourth President of the United States represents both the completion of a historical campaign season and a triumph of the Civil Rights revolution of the twentieth cen- tury. President Obama’s 2008 campaign, along with the campaigns of Senators Hillary Rodham Clinton and John McCain, was remarkable in both the identities of the politicians themselves1 and the attention they brought to the political process. In particular, Obama attracted voters from populations which have not been traditionally represented in na- tional politics. His run was hallmarked, in large part, by significant grassroots fundraising, a concerted effort to generate popular appeal, and, most important, massive voter turnout efforts.2 As a result, this election cycle generated significant increases in participation during the primary season.3 Turnout in the general election did not meet anticipated record † Legal Writing Instructor, Howard University School of Law. J.D., M.A., Duke Univer- sity, 2000. An early version of this paper was presented at the Writer’s Workshop of the Legal Writing Institute in summer 2007. Later versions were presented at the November 2007 Howard University School of Law faculty colloquy and the September 2008 Northeast People of Color Legal Scholarship Conference. I gratefully acknowledge Andrew Taslitz, Sherman Rogers, Derek Black, Paulette Caldwell, Phoebe Haddon, and Daniel Tokaji for their thoughtful comments on earlier drafts of this paper. -

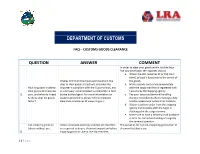

Department of Customs

DEPARTMENT OF CUSTOMS FAQ – CUSTOMS GOODS CLEARANCE QUESTION ANSWER COMMENT In order to clear your goods within the five hour – five day timeframe, the importer should: a. Obtain the CRF (whether DI or PSI) from BIVAC at least 5 days prior to the arrival of It takes minimum five hours and maximum five the goods. days to clear goods at Customs, provided the b. Make a goods declaration immediately How long does it take to importer is compliant with the Customs laws, and after the cargo manifest is registered with clear goods at a Customs all necessary documentation is completed in time Customs by the shipping agency. 1. port, and what do I need by the broker/agent. For more information on c. Pay your taxes and terminal handling to do to clear my goods customs procedures, please refer to Customs charges immediately after receiving a duty faster? clearance procedures at www.lra.gov.lr. and tax assessment notice from Customs. d. Obtain a delivery order from the shipping agency immediately after the cargo is discharged in the cargo terminal. e. Make sure to have a delivery truck available in time for immediate loading of cargo by the terminal operator. Can I ship my goods to Unless otherwise expressly exempt, all importers The penalties for not pre-inspecting goods prior to Liberia without pre- are required to do pre-shipment inspection before shipment to Liberia are: 2. shipping goods to Liberia. the Government, 1 | P a g e shipment inspection through Administrative Regulation No. 12. 14263 – a. 10% of CIF value for first and second (PSI)? 2/MOF/R/BCE/14 October 2013, requires offense penalties for failure to have goods pre-inspected. -

Section 5 Explanation of Terms

Section 5 Explanation of Terms he Explanation of Terms section is designed to clarify Additional Standard Deduction the statistical content of this report and should not be (line 39a, and included in line 40, Form 1040) T construed as an interpretation of the Internal Revenue See “Standard Deduction.” Code, related regulations, procedures, or policies. Explanation of Terms relates to column or row titles used Additional Taxes in one or more tables in this report. It provides the background (line 44b, Form 1040) or limitations necessary to interpret the related statistical Taxes calculated on Form 4972, Tax on Lump-Sum tables. For each title, the line number of the tax form on which Distributions, were reported here. it is reported appears after the title. Definitions marked with the symbol ∆ have been revised for 2015 to reflect changes in Adjusted Gross Income Less Deficit the law. (line 37, Form 1040) Adjusted gross income (AGI) is defined as total income Additional Child Tax Credit (line 22, Form 1040) minus statutory adjustments (line 36, (line 67, Form 1040) Form 1040). Total income included: See “Child Tax Credit.” • Compensation for services, including wages, salaries, fees, commissions, tips, taxable fringe benefits, and Additional Medicare Tax similar items; (line 62a, Form 1040) Starting in 2013, a 0.9 percent Additional Medicare Tax • Taxable interest received; was applied to Medicare wages, railroad retirement com- • Ordinary dividends and capital gain distributions; pensation, and self-employment income that were more than $200,000 for single, head of household, or qualifying • Taxable refunds of State and local income taxes; widow(er) ($250,000 for married filing jointly, or $125,000 • Alimony and separate maintenance payments; for married filing separately). -

Tax Laws and Tax Like Contributions

Draft. Not yet updated and agreed upon. IV. Laws governing tax and tax-like contributions 1 Introduction ........................................................................................................................ 2 2 Main tax categories ............................................................................................................ 3 3 Germany ............................................................................................................................. 3 3.1 Formulating laws ......................................................................................................... 3 3.2 Taxes on Income, Profits and Capital Gains ............................................................... 4 3.3 Taxation of Wealth ...................................................................................................... 5 3.4 Taxation of turnover, consumption, goods and services ............................................. 5 3.5 Customs ....................................................................................................................... 5 3.6 Social security Contributions ....................................................................................... 6 4 Kenya Tax Laws ................................................................................................................. 6 4.1 Formulating laws ......................................................................................................... 6 4.2 The Income Tax Act ................................................................................................... -

Investors' Reaction to a Reform of Corporate Income Taxation

Investors' Reaction to a Reform of Corporate Income Taxation Dennis Voeller z (University of Mannheim) Jens M¨uller z (University of Graz) Draft: November 2011 Abstract: This paper investigates the stock market response to the corporate tax reform in Germany of 2008. The reform included a decrease in the statutary corporate income tax rate from 25% to 15% and a considerable reduction of interest taxation at the shareholder level. As a result, it provided for a higher tax benefit of debt. As it comprises changes in corporate taxation as well as the introduction of a final withholding tax on capital income, the German tax reform act of 2008 allows for a joint consideration of investors' reactions on both changes in corporate and personal income taxes. Analyzing company returns around fifteen events in 2006 and 2007 which mark important steps in the legislatory process preceding the passage of the reform, the study provides evidence on whether investors expect a reduction in their respective tax burden. Especially, it considers differences in investors' reactions depending on the financial structure of a company. While no significant average market reactions can be observed, the results suggest positive price reactions of highly levered companies. Keywords: Tax Reform, Corporate Income Tax, Stock Market Reaction JEL Classification: G30, G32, H25, H32 z University of Mannheim, Schloss Ostfl¨ugel,D-68161 Mannheim, Germany, [email protected]. z University of Graz, Universit¨atsstraße15, A-8010 Graz, Austria, [email protected]. 1 Introduction Previous literature provides evidence that companies adjust their capital structure as a response to changes in the tax treatment of different sources of finance. -

Income 4: State Income Tax Addback for Individuals

Income 4: State Income Tax Addback for Individuals Individuals who itemize deductions on their federal income tax returns and claim a deduction for state income tax must add back the deducted state income tax on line 2 of their Colorado income tax return (Form 104). The amount that must be added back is generally equal to the amount deducted on line 5a of the taxpayer’s federal Schedule A. However, the amount a taxpayer must add back may be limited, as discussed in this publication. The addback requirement does not apply to individuals who claim the standard deduction on their federal income tax returns or to individuals who claim a deduction for general sales taxes, rather than state and local income taxes. Corporations, estates, and trusts are also required to add back certain state taxes deducted on their federal returns. However, the information in this publication pertains only to individual income taxpayers. FEDERAL DEDUCTION FOR STATE AND LOCAL TAXES Individuals who itemize deductions on their federal returns can deduct various state and local taxes. However, the addback requirement applies only to state income taxes deducted on their federal returns. Individuals must add back the state income taxes they deduct, regardless of whether the state income taxes were paid to Colorado or to another state. Taxpayers are not required to add back any of the following types of taxes that they may have deducted on their federal Schedule A: general sales taxes; local income or occupational taxes; state or local real estate taxes; or state or local personal property taxes. LIMITATIONS Various limitations may reduce the amount an individual taxpayer must add back. -

The African-American Church, Political Activity, and Tax Exemption

JAMES_EIC 1/11/2007 9:47:35 PM The African-American Church, Political Activity, and Tax Exemption Vaughn E. James∗ ABSTRACT Ever since its inception during slavery, the African-American Church has served as an advocate for the socio-economic improve- ment of this nation’s African-Americans. Accordingly, for many years, the Church has been politically active, serving as the nurturing ground for several African-American politicians. Indeed, many of the country’s early African-American legislators were themselves mem- bers of the clergy of the various denominations that constituted the African-American Church. In 1934, Congress amended the Internal Revenue Code to pro- hibit tax-exempt entities—including churches and other houses of worship—from allowing lobbying to constitute a “substantial part” of their activities. In 1954, Congress further amended the Code to place an absolute prohibition on political campaigning by these tax-exempt organizations. While these amendments did not specifically target churches and other houses of worship, they have had a chilling effect on efforts by these entities to fulfill their mission. This chilling effect is felt most acutely by the African-American Church, a church estab- lished to preach the Gospel and engage in activities which would im- prove socio-economic conditions for the nation’s African-Americans. This Article discusses the efforts made by the African-American Church to remain faithful to its mission and the inadvertent attempts ∗ Professor of Law, Texas Tech University School of Law. The author wishes to thank Associate Dean Brian Shannon, Texas Tech University School of Law; Profes- sor Christian Day, Syracuse University College of Law; Professor Dwight Aarons, Uni- versity of Tennessee College of Law; Ms. -

System of Church Tax in Germany

Dr. Jens Petersen The system of church tax in Germany The church tax will be 9% (or 8% in Bavaria and Baden-Württemberg) from the income tax. The churches, who have the status of a public body have the legal right to raise taxes. This based apon the Germen Constitution in conjunction with the federal church laws. These are the protestant, roman-kath., old-kath., some jewish and other small churches. The churches conclude wether they raise taxes and about the percentage. The administration itself is carreid-over to IRS because here is the established administration. This based on an bilateral contract. The IRS will get fees between 2% and 4% (according to the federal state). The churches have the legal right to get the data of their members from the IRS the fullfill their own tax-systems. At the time they did not need them because the IRS administrate the tax levy. The church tax is the most important part of the churches household. It will be about 70% to 80% of it. Other incomes: funds, fees, accomplishments (benefits) from the state (very old legal title; based on a treaty of 1804), other revenues. Income tax will be raised from income and salary a.s.o. The church tax from the income-tax will collect in conjunction with the income-tax (tax bill). The church tax of salary will retained by the employer and he refers them to the appropriate IRS. This refers it to the local church. Wether the employee is member of a church the employer will check out from the tax-card (Lohnsteuerkarte).