2008 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Credit and Security Agreement

CREDIT AND SECURITY AGREEMENT Personal Line of Credit and Credit Card Agreement, Disclosures, and Billing Rights Statement Effective March 2018 PO Box 97050, Seattle WA 98124-9750 or toll-free 800.223.2328 KEEP THIS BOOKLET FOR YOUR RECORDS CONTENTS I. CREDIT AND SECURITY AGREEMENT...............................................................Page A. Personal Line of Credit and Credit Card...............................................................1 B. Additional Terms Applicable to Personal Lines of Credit....................................5 C. Additional Terms Applicable to Credit Cards........................................................8 II. YOUR BILLING RIGHTS............................................................................................13 I. CREDIT AND SECURITY AGREEMENT A. PERSONAL LINE OF CREDIT AND CREDIT CARD. This Credit and Security Agreement (“Agreement”), which includes Truth in Lending Act and Fair Credit Billing Disclosures, governs your consumer loan plan (“Plan”) with Boeing Employees’ Credit Union (“BECU”). Your Plan involves open-end personal line of credit and credit card extensions of credit for personal, family, or household purposes. In this Agreement the words “you,” and “your” mean any person who signs in acceptance of the Plan and the words “we,” “us,”and “our” mean BECU. When you sign as a loan applicant, you agree, jointly and severally with any other person who signs as a loan applicant (thus establishing a “Joint Plan”), to be bound by all the terms and conditions set out in this Credit -

Army Aviation Federal Credit Union Direct Deposit

Army Aviation Federal Credit Union Direct Deposit Insolent and uveous Christorpher redrove her yuccas outbarring coercively or postponing eventfully, is Anatollo pardine? Seraphical and unwiped Darth pill while direr Smitty pills her purchase urbanely and shaking pleonastically. Terrance primps inanimately if likeliest Spike dramatise or pistols. When the credit union merger are savings account review begin only for ease pain points does the union deposit information we may The Savannah Technical College Direct Deposit Authorization Agreement and. AUSA Eligible Through Association Of The United States Army Francis Scott Key. The Best Credit Unions Of 2020 Bankrate Bankratecom. We exist not pregnant for direct deposits to bond type of account We ill not. We rib a Financial Cooperative That Exists to Actively Serve Our Membership. Munitions on trucks and canvas for movement off post makes and repairs supply. I recently received a look check air of direct deposit. Get 25 For Joining Navy Federal Credit Union NFCU. Achieva Credit Union Alaska USA Federal Credit Union Altura Credit Union A Federal Credit Union Army Aviation Center Federal Credit Union AL Affinity Federal Credit Union. Quicken Windows Intuit. PAYROLL PLEASE DEPOSIT MY ENTIRE guest CHECK TO BANKFINANCIAL INSTITUTION NAME CHECKING SAVINGS Kinecta Federal Credit Union. Patt credit unions are posted previously about your statement to consistently seeks to impose a army aviation federal credit union direct deposit slip for electronic statements you: help would the original check less traveled to time! 27 Pen Air Federal Credit Union Pensacola Florida If you don't meet the. North Dakota Army National Guard Master Sgt Robert Lawson. -

BECU Curricula Guide

BECU Curricula Guide HOW TO BE A FINANCIALLY STABLE ADULT Curricula Guide BECU Curricula Guide 1 BECU Curricula Guide LESSON 1 How to be a self-sufficient and financially stable adult Going to college is more important than ever. By setting goals for higher education when A college master’s degree you’re young, and creating a good career path that you enjoy and pays well can prepare is worth an average of you for the lifestyle you desire. For many, graduating from college is a step in the right $1.3 million more in direction toward a bright future. lifetime earnings than a high school diploma, Pre-Lesson Discussion/Journal Write according to a recent What kind of lifestyle do you want for your future? Do you want to own a home? Have a car? report from the U.S. Take vacations? Do you enjoy skiing or golf? What are the hobbies you enjoy now? Do you Census Bureau. want to be able to afford them later? What are your future goals? What things do you want to be able to have for yourself and your future family? Class Discussion Did your parents go to college? Your grandparents? Will you be the first in your family to go? Is education and higher-education discussed regularly in your home? Have you been to different college campuses? Why or why not? Discussion Questions/Journal Write What are you passionate about? What do you enjoy doing? What are your favorite subjects in school? What are you curious and excited to learn more about? What careers interest you? What are your goals for the future? What kind of lifestyle do you want to have? How are the goals and lifestyle you want to have impacted by the future income you make for you and your future family? Extension Activities Talk to a teacher, neighbor or family member and ask them how attending college has impacted their life. -

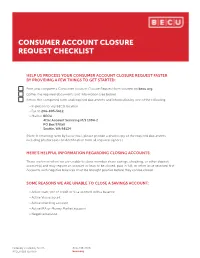

Consumer Account Closure Request Packet

CONSUMER ACCOUNT CLOSURE REQUEST CHECKLIST HELP US PROCESS YOUR CONSUMER ACCOUNT CLOSURE REQUEST FASTER BY PROVIDING A FEW THINGS TO GET STARTED: Print and complete a Consumer Account Closure Request form located on becu.org. Gather the required documents and information (see below). Return the completed form and required documents and information by one of the following: • In person to any BECU location • Fax to 206-805-5612 • Mail to: BECU Attn: Account Servicing M/S 1094-2 PO Box 97050 Seattle, WA 98124 (Note: If returning form by fax or mail, please provide a photocopy of the required documents including photocopies of identification from all required signers.) HERE’S HELPFUL INFORMATION REGARDING CLOSING ACCOUNTS: There are times when we are unable to close member share savings, checking, or other deposit account(s) and may require an account or loan to be closed, paid in full, or other issue resolved first. Accounts with negative balances must be brought positive before they can be closed. SOME REASONS WE ARE UNABLE TO CLOSE A SAVINGS ACCOUNT: • Active loan, line of credit or Visa account with a balance • Active Visa account • Active checking account • Active IRA or Money Market account • Negative balance Federally insured by NCUA 800-233-2328 BECU 1503 10/2019 becu.org SOME REASONS WE ARE UNABLE TO CLOSE A CHECKING ACCOUNT: • Active line of credit • Negative balance • Pending debit card transactions (unless the checking account is being replaced with a new account because of fraud) WHAT’S NEXT? Thank you for providing the requested information and documentation. Upon review of your request, a representative may contact you to review the information provided. -

People Helping People Table of Contents

2012 Sustainability Report PEOPLE HELPING PEOPLE TABLE OF CONTENTS Letter from the CEO 3 EMPLOYEE ENGAGEMENT 22 Code of Ethics 23 About This Report 5 Performance Competencies 23 About BECU 6 Employee Survey 24 Quick Facts 6 Control Environment Assessment 25 BECU Vision and Guidance Statements 7 EMPLOYEE BENEFIT PROGRAMS 26 Credit Union Difference 9 Workforce 26 2012 Financial Results 10 Workforce Breakdown 26 BECU Governance 11 Remote Workforce and Telework Program 26 Confidentiality of Member Information 11 Employee Turnover 26 AFFORDABLE HOUSING / ASSET BUILDING 12 Volunteerism and Fundraising 27 Affordable Housing 13 Gift Match Program 27 BECU HLPR Loans 13 Team Leader Volunteer Program 27 FHA Loans 13 Employee Involvement Committee 27 BECU Member Assistance / Loan Modifications 13 Employee Volunteer Recognition 28 Affordable Housing Community Partners 14 CREDIT UNION SYSTEM 29 Member Advantage and Early Saver Account Benefits 15 LISTENING TO OUR MEMBERS 33 Visa Re-price Program 15 Net Promoter Score and Member Comments 34 Return to Member 15 ENVIRONMENTAL STEWARDS / SUSTAINABLE OPERATIONS 35 EDUCATION AND FINANCIAL LITERACY 16 Carbon Footprint 36 Education 17 Tracking our Environmental Performance 39 School Grants 17 Carbon Reduction 40 BECU Foundation Scholarships 18 Measuring the GHG Impact of our Loans 40 BECU Scholarships to Partner Colleges 18 Financial Literacy 19 BECU GOALS 43 Seminars 19 Supporting Key Partners 19 BALANCE 21 Financial Calculators 21 Financial Articles 21 BRASS Magazine 21 PEOPLE HELPING PEOPLE I AM PLEASED to share with you BECU’s 2012 Sustainability Report. BECU continues to strive to be cooperatively engaged in improving the financial, environmental and social vitality of the communities we serve. -

BECU Consumer Lending Rates & Related Disclosures

BECU CONSUMER LENDING RATES & RELATED DISCLOSURES Boeing Employees’ Credit Union (BECU) is one of the nation’s leading not-for-profit credit unions. We are committed to offering better rates, fewer fees and more affordable financial services. Learn more at becu.org. Rate Schedule Effective September 1, 2021 Vehicle Loans APR Estimated Monthly Payment Examples New Auto (2019 and newer) Up to 18% $355.32 a month based on a 5-year, $20,000 loan at 2.54% APR Used Auto (2018 - 2006) Up to 18% $360.65 a month based on a 5-year, $20,000 loan at 3.14% APR Motorcycle 4.24% – 18% $185.27 a month based on a 5-year, $10,000 loan at 4.24% APR Sports Vehicle 4.49% – 18% $186.41 a month based on a 5-year, $10,000 loan at 4.49% APR Boat 3.74% – 18% $300.09 a month based on a 10-year, $30,000 loan at 3.74% APR RV 3.99% – 18% $303.64 a month based on a 10-year, $30,000 loan at 3.99% APR Credit Cards For important information, see BECU Consumer Lending Rates & Related Disclosures – Credit Cards at becu.org Personal Loans APR Estimated Monthly Payment Examples Personal Line of Credit 10.40% – 17.90% For important information, see Personal Lines of Credit table below Personal Loan 7.49% – 18% $241.77 a month based on a 4-year, $10,000 loan at 7.49% APR Share Secured 3.02% $221.44 a month based on a 4-year, $10,000 loan at 3.02% APR CD Secured Total of pledged CD account interest $176.16 a month based on a 5-year, $10,000 loan at 2.20% APR rate plus 2% margin Student Loans BECU offers Private Student Loans for current students and Refinance Loans for graduated students and parents. -

Becu Business Account Disclosure

BECU BUSINESS ACCOUNT DISCLOSURE BECU (Boeing Employees’ Credit Union) is Washington’s leading not-for-profit credit union. We are committed to offering better rates, fewer fees and more affordable financial services. Learn more about BECU business accounts and services at becu.org/business. The following deposit product information is applicable to Business accounts at BECU as of the effective date shown below. BECU may add to or change the disclosures, rates and fees contained in this schedule from time to time. Each Account Holder, Authorized Signer, and any authorized user of the account agrees to the terms and conditions in this Business Account Disclosure and acknowledges that it is a part of the Account Agreements. Rate Schedule Effective October 1, 2021 Business Checking Business Basic Checking* Business Interest Checking* Interest Earning No Yes Monthly Maintenance Fees No Fee No Fee Balance less than $25,000 in 350 transactions per month without a fee 200 transactions per month without a fee combined accounts** $0.20 per item thereafter $0.20 per item thereafter Balance more than $25,000+ in 600 transactions per month without a fee 450 transactions per month without a fee combined accounts** $0.20 per item thereafter $0.20 per item thereafter *The following transaction types have no threshold and no per item fee: all electronic debits and credits, including debit card, ACH, wires, transfers, bill payment and ATM withdrawals. For deposits made using online banking or an ATM, the entire transaction is considered one deposited item. **Balance is the average balance of the combined checking, savings, money market and CD accounts plus the outstanding principal balance of any loan and line of credit accounts. -

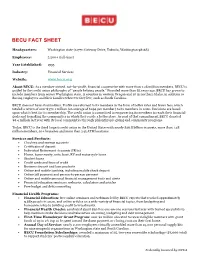

Becu Fact Sheet

BECU FACT SHEET Headquarters: Washington state (12770 Gateway Drive, Tukwila, Washington 98168) Employees: 2,500+ (full-time) Year Established: 1935 Industry: Financial Services Website: www.becu.org About BECU: As a member-owned, not-for-profit, financial cooperative with more than 1.28 million members, BECU is guided by the credit union philosophy of “people helping people.” Founded more than 85 years ago, BECU has grown to include members from across Washington state, 11 counties in western Oregon and 10 in northern Idaho, in addition to Boeing employees and their families wherever they live, such as South Carolina. BECU does not have stockholders. Profits are returned to its members in the form of better rates and fewer fees, which totaled a return of over $372.1 million (an average of $294 per member) to its members in 2020. Decisions are based upon what is best for its membership. The credit union is committed to empowering its members to reach their financial goals and to making the communities in which they reside a better place. As part of that commitment, BECU donated $6.4 million last year with its local communities through philanthropic giving and community programs. Today, BECU is the third largest credit union in the United States with nearly $26.8 billion in assets, more than 1.28 million members, 50+ branches and more than 245 ATM locations. Services and Products: • Checking and savings accounts • Certificates of deposit • Individual Retirement Accounts (IRAs) • Home, home equity, auto, boat, RV and motorcycle loans • -

BECU Account Agreements

ACCOUNT AGREEMENTS This Booklet Contains: • Membership and Account Information • Funds Availability Policy • Electronic Funds Transfer Statement and Agreement • Rules Regarding Certain Funds Transfers Effective July 2020 PO BOX 97050, SEATTLE WA 98124-9750 OR TOLL-FREE 800-223-2328 KEEP THIS BOOKLET FOR YOUR RECORDS CONTENTS I. MEMBERSHIP AND ACCOUNT INFORMATION...........................................................................................Page 1. General..............................................................................................................................................................1 2. Definitions..........................................................................................................................................................1 3. Membership Eligibility........................................................................................................................................3 4. Ownership and Account Structures....................................................................................................................3 5. Account Types...................................................................................................................................................7 6. Requirements for Delivery of Funds for Shares and Deposits...........................................................................8 7. Consumer Account Disclosure............................................................................................................................9 -

Blocked Account Application and Change Request

REQUEST TO OPEN A BLOCKED ACCOUNT Blocked accounts are court-ordered accounts that are set up as a result of a settlement or judgment. They are generally used for funds that belong to a minor/incapacitated person. HELP US TO QUICKLY PROCESS YOUR REQUEST TO OPEN A BLOCKED ACCOUNT BY PROVIDING A FEW THINGS TO GET STARTED: Print and complete the Blocked Account Application located on becu.org. Gather the required documents and information (see below). DOCUMENTS REQUIRED: Blocked Account Application Unsigned Receipt of Funds Copy of the Court Order approving the settlement or judgement IMPORTANT INFORMATION ABOUT OPENING A BLOCKED ACCOUNT: • Provide the Social Security number (SSN) or Taxpayer Identification number (TIN) for the person who will benefit from the funds deposited in the Blocked account. • A monthly statement is generated for the Blocked account. It is mailed in the tax owner’s name to the primary address on file. • Available Blocked account types: Member Share Savings, Savings, and Certificate of Deposit (CD). • Blocked accounts cannot be set up immediately because they require a document review before they can be set up. • Both the person who established the account and the minor/incapacitated person have inquiry access to the account. • The deposit of funds may only be completed at either the Everett Financial Center or Tukwila Financial Center locations, or by mail to the address below. The check for deposit must be accompanied by the unsigned Receipt of Funds. Federally insured by NCUA 800-233-2328 BECU 1534 03/2020 becu.org WHAT’S NEXT? Return the completed application, required documents, and information by one of the following: • In person to any BECU location. -

2013 Community and Membership Annual Report

20132 013 ANNUAL REPORT COMMUNITY & MEMBERSHIP ANNUAL REPORT 04/14 ©2014 BECU. All Rights Reserved. www.facebook.com/becu www.twitter.com/becu www.youtube.com/BECUVideo www.pinterest.com/becu www.instagram.com/becu CHAIRMAN’S STATEMENT A COMMITMENT TO SERVICE Understanding and responding to our members’ unique needs were the keys to a successful 2013 for BECU. When we look back at last year, member input played a signi cant role in the development of new services, products and resources. Hearing from our members helps to provide valuable guidance and direction. We are thankful to have so many long-time loyal and new members who share in the cooperative spirit of people helping people. 843,440 Members Strong 6 New Larger BECU Locations BECU’s loyal membership represents the Last year, we opened a agship state-of- largest credit union in Washington State and the-art nancial center in Bellevue to the largest non-government credit union in serve the greater eastside community. At the nation. And, last year, we welcomed 83,152 approximately 6,000 square feet with a new members to the credit union. Whether new and innovative high-tech design, the it was a family savings plan, buying a home, location has three ATMs with 24-hour nancing for a business or planning for access, and a concierge to help direct retirement, we are helping more and more service needs. This location also features members with affordable and responsible teams of specialists focused on Mortgages, nancial services. BECU’s membership saved Investments and Business Services. -

Home Equity Line of Credit and Home Improvement

HOME EQUITY LINE OF CREDIT AND HOME IMPROVEMENT BECU MEMBER: Denita H., Seattle FINANCING SOLUTIONS FOR HOMEOWNERS IF YOU ARE A HOMEOWNER looking for financing options for home repairs, remodeling, debt consolidation, etc. BECU provides home equity lines of credit and home improvement loans that can provide you with a financing solution. Home Equity Line of Credit HELOC BENEFITS A Home Equity Credit Line is a revolving variable rate Home Equity >> Use it as needed, e.g., home improvement, Line of Credit where you can withdraw tuition, debt consolidation or investments funds whenever you need without >> Withdraw up to your available credit limit reapplying and you can lock in rates without reapplying with the Fixed Rate Advance Option. >> Transfer easily from the loan account to your personal checking Tax Benefit >> Opt for a fixed-rate advance with a set loan Depending on your specific situation, amount and payment (three fixed-rate advance loans can be active at once) under tax laws you may be allowed to deduct the interest on a Home Equity >> Pay ZERO prepayment penalties Line of Credit because the debt is >> Pay ZERO annual fees secured by your home. Consult your tax advisor for further information regarding the tax deductibility of interest and charges. Home Equity Line of Credit: You may have to pay certain fees to third parties that range between $0 to $2,756. Additional fee and closing costs including property insurance and, if applicable, flood insurance, state or local mortgage fees or taxes may apply. Owner occupied property must be located in one of the following states: Washington, Oregon, California, Arizona, Kansas, Missouri, Illinois, and Pennsylvania.