Toll's Divisional Structure

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Autumn 2017 Twuwheel

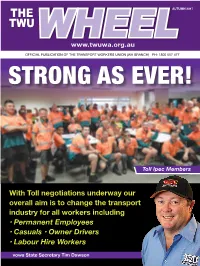

THE AUTUMN 2017 TWUWHEEL www.twuwa.org.au OFFICIAL PUBLICATION OF THE TRANSPORT WORKERS UNION (WA BRANCH) PH: 1800 657 477 STRONG AS EVER! Toll Ipec Members With Toll negotiations underway our overall aim is to change the transport industry for all workers including • Permanent Employees • Casuals • Owner Drivers • Labour Hire Workers vows State Secretary Tim Dawson Do you need a HR truck licence? We offer 1 or 2 day HR-B for $990* or lessons to suit your requirement Other transport essentials available Fatigue Management Certificate III Driver operations First Aid Load Restraint / Secure Cargo Implement Traffic Management Plan Forklift Call us today to discuss your requirements Unit 2 / 347 Great Eastern Hwy Fire Courses Redcliffe WA 6104 Supply Fire & First Aid equipment (08) 6180 -8065 / 0427 159 039 RTO 40599 Considering a career in Public Transport? With 13 depots across Perth and the SouthWest, there is sure to be one near you. Contact 9247 7500 or download an application form at www.swantransit.com.au Published by Perth Advertising Services. Phone: 9375 1922. Fax: 9275 2955. RATECUTTING RIFE! system to tackle the root causes of ‘Things have never many truck crashes. Instead, pressure is increasing on drivers to speed, drive long hours and been this bad for skip their mandatory rest breaks. The Turnbull Government’s own report showed the RSRT would have cut truck owner drivers’ crashes by 28% and yet it went ahead claims TIM DAWSON and tore it down. It is clearly willing to play politics with people’s lives. Throughout the transport industry the highest for any industry, according hundreds of owner-drivers are either to Safe Work Australia. -

Annual Report 2020 Contents Contents

ANNUAL REPORT 2020 CONTENTS CONTENTS About Us ..............................................................................4 ALC Members ......................................................................5 Message From ALC Chair, Philip Davies .............................6 Message From CEO, Kirk Coningham, OAM ......................8 Board Members ...................................................................12 Our Values ...........................................................................14 ALC Team Members ............................................................14 Committees .........................................................................15 Strategic Plan ......................................................................18 COVID-19 ............................................................................20 @AustLogistics Key Policy & Advocacy Achievements ................................22 Key Safety Achievements ....................................................24 linkedin.com/company/australian-logistics-council Appendix .............................................................................26 Policies ..........................................................................27 Suite 17B, National Press Club Building Submissions ..................................................................27 16 National Circuit, BARTON, ACT 2611 P: +61 2 6273 0755 Media Releases .............................................................28 E: [email protected] Financials .......................................................................30 -

For Personal Use Only Use Personal For

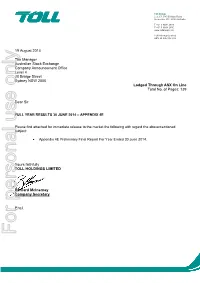

Toll Group Level 7, 380 St Kilda Road Melbourne VIC 3004 Australia T +61 3 9694 2888 F +61 3 9694 2880 www.tollgroup.com Toll Holdings Limited ABN 25 006 592 089 19 August 2014 The Manager Auustralian Stock Exchange Company Announcement Office Level 4 20 Bridge Street Sydney NSW 2000 Lodged Through ASX On Line Total No. of Pages: 139 Dear Sir FULL YEAR RESULTS 30 JUNE 2014 – APPENDIX 4E Please find attached for immediate release to the market the following with regard the abovementioned subject: • Appendix 4E Preliminary Final Report For Year Ended 30 June 2014. Yours faithfully TOLL HOLDINGS LIMITED Bernard McInerney Company Secretary Encl. For personal use only TOLL HOLDINGS LIMITED AND ITS CONTROLLED ENTITIES Preliminary Final Report for the Year Ended 30 June 2014 ASX Appendix 4E Preliminary Final Report Name of entity Toll Holdings Limited ABN 25 006 592 089 Reporting period Year ended 30 June 2014 Previous corresponding period Year ended 30 June 2013 Results for announcement to the market 201 4 201 3 Change Change $M $M $M % Revenue 8,811.2 8,719.4 91.8 +1.1 EBIT pre individually significant items 444.4 425.9 18.5 +4.3 NPAT pre individually significant items 298.5 282.4 16.1 +5.7 Individually significant items (net of tax) (5.4) (190.7) 185.3 Net profit after tax 293.1 91.7 201.4 +219.6 Non-controlling interests (7.0) (7.2) 0.2 +2.8 NPAT attributable to shareholders 286.1 84.5 201.6 +238.6 Refer to attached Media Release for commentary on results. -

THE OZHARVEST EFFECT Adelaide Brisbane Gold Coast Melbourne

OzHarvest Book of Thanks 2016 THE OZHARVEST EFFECT The OzHarvest Effect can only be achieved thanks to a massive team effort made up of devoted staff, passionate chefs and ambassadors, like-minded partners, generous food and financial donors and the every growing ‘yellow army’ of volunteers. We love and appreciate everyone who is part of this special family and have made every effort to ensure we list all involved. As you can see, the list is very long and we apologise if someone has been overlooked. Please contact us at OzHarvest HQ on 1800 108 006 to ensure we capture you in our next Book of Thanks. Adelaide advisory Amanda Dalton-Winks / Anne Duncan / Harriette Huis in’t Veld / Hayley Everuss / Jason James / Sharyn Booth / Vicki Cirillo COrporate Volunteer AMP / AON Risk Solutions / Aussie / Biogen / BUPA / Caltex / Commonwealth Bank / Country Health SA / Deloitte / Department of Environment / Govenor’s Leadership Foundation Program / KPMG / Mental Illness Fellowship / Michels Warren / O-I Glass / Olympus / Paxus / People’s Choice Credit Union / The University of Adelaide / Victor Harbour Childcare Centre Vodafone / Tropcorp / SA Power Networks / Santos / Uni SA / Woolworths FINANCIAL DONOR 30 Grosvenor Street Pty Ltd as Trustee for FWH Foundation / A Touch of Beauty / Accounting Buddy / Adam Delaine / Adam Wittwer / Adelaide Cellar Door Wine Festival / Adelaide Fuel and Safety / Adelaide Sustainability Centre / Adelaide Youth Courts / Adrian Dipilato / Adrian M Hinton / Albert Bensimon / Ali Roush / Amanda Dalton-Winks / Andrew John -

Christian Porter

Article Talk Read View source View history Search Wikipedia Christian Porter From Wikipedia, the free encyclopedia This is an old revision of this page, as edited by Citation bot (talk | contribs) at 17:14, 25 February 2021 (Add: work. Removed parameters. Main page Some additions/deletions were parameter name changes. | Use this bot. Report bugs. | Suggested by AManWithNoPlan | Pages linked from Contents cached User:AManWithNoPlan/sandbox2 | via #UCB_webform_linked 268/1473). The present address (URL) is a permanent link to this Current events revision, which may differ significantly from the current revision. Random article (diff) ← Previous revision | Latest revision (diff) | Newer revision → (diff) About Wikipedia Contact us For the singer, see The Voice (U.S. season 4). Donate Charles Christian Porter (born 11 July 1970) is an Australian Liberal Party politician and Contribute The Honourable lawyer serving as Attorney-General of Australia since 2017, and has served as Member of Christian Porter Help Parliament (MP) for Pearce since 2013. He was appointed Minister for Industrial Relations MP Learn to edit and Leader of the House in 2019. Community portal Recent changes From Perth, Porter attended Hale School, the University of Western Australia and later the Upload file London School of Economics, and practised law at Clayton Utz and taught law at the University of Western Australia before his election to parliament. He is the son of the 1956 Tools Olympic silver medallist, Charles "Chilla" Porter, and the grandson of Queensland Liberal What links here politician, Charles Porter, who was a member of the Queensland Legislative Assembly from Related changes [4][5] Special pages 1966 to 1980. -

Media Release

Toll Group Level 7, 380 St Kilda Road Melbourne VIC 3004 Australia T +61 3 9694 2888 www.tollgroup.com Toll Holdings Limited ABN 25 006 592 089 Media Release 30 October 2017 Peter Stokes joins Toll Group global leadership team Toll Group has appointed Peter Stokes as President, Group Operational Services, where he will lead a centralised network of operational functions to service Toll’s three divisions in express networks, contract logistics and global forwarding. Mr Stokes brings with him over 20 years of senior leadership experience in logistics and mining operations, with previous leadership roles at Barminco, Linfox and Accenture. He brings significant global experience having worked in markets across Africa, Asia, Australia, the UK and the USA. Toll Group’s Managing Director, Michael Byrne said Mr Stokes joins Toll at an important period, as the business builds a world-class logistics operations capability. “Mr Stokes brings a wealth of senior leadership experience, with a strong focus on safety and operational excellence. He will play a key role in delivering the next generation of Toll’s operational capability so we can support our customers and drive significant improvements in safety and productivity,” said Mr Byrne. Created in July 2017, Toll’s Group Operational Services covers linehaul, equipment, labour resourcing, property and procurement. The formation of the Group is expected to drive significant improvements to safety, operating efficiency and procurement outcomes through standardization of process and removal of duplication. Mr Stokes holds a MBA from Bond University, Queensland and recently attended an Advanced Management Program at Harvard Business School. -

CAE in Australia

CAE in Australia Overview CAE is an experienced training systems integrator across air, naval, land and public safety domains. The company employs 10,000 people at more than 160 sites and training locations in 35 countries. CAE offers customers a complete range of highly innovative products, services and training centre solutions designed to help them meet their mission critical needs for safety, efficiency and readiness. Defence and Security For over 25 years CAE Australia Pty Ltd, now based in Homebush, New South Wales, has had a significant presence in Australia that today includes approximately 200 employees supporting training in Australia and New Zealand at more than 20 sites serving the defence, civil aviation and healthcare markets. CAE Australia Pty Ltd is one of the key regional business operations that make up CAE’s global Defence and Security business unit. CAE Australia is consistently recognized as one of the top small-to-medium sized enterprises in Australia. Leveraging the full breadth of CAE’s global capabilities and leading-edge simulation technologies, CAE Australia brings proven solutions to the Australian market and surrounding region in addition to delivering world-class engineering and support services. Major programs for the Australian Defence Forces ÎÎRAAF Hawk Mk 127 Lead-in Fighter training ÎÎMRH90 training systems and support and support services at RAAF Pearce and services at Oakey and Townsville; RAAF Williamtown; ÎÎMH-60R Seahawk training systems and ÎÎPrime contractor on the Maintenance and support services at HMAS Albatross; Support of ADF Aerospace Simulators ÎÎAP-3C maintenance support services at RAAF (MSAAS) contract, as well as the Edinburgh; In addition, CAE supports the Royal Aerospace Simulation Through Life Support (ASTLS) contract; ÎÎKing Air 350 full-flight simulator training and Australian Air Force’s participation in support services at East Sale; Coalition Virtual Flag, which is one of the ÎÎKC-30A training systems and comprehensive world’s largest virtual air combat exercises. -

Regional Area Surcharge

Toll Group Level 7, 380 St Kilda Road Melbourne VIC 3004 Australia Toll Transport Pty Ltd ABN: 31006604191 Regional Area Surcharge Regional area surcharges are applicable for pick up or delivery to regional, remote or off-shore locations where Toll incurs additional costs to service. Priority Service Suburb Postcode Price Abingdon Downs 4892 $ 51.50 Acacia Hills 0822 $ 26.00 Adavale 4474 $ 51.50 Adelaide River 0846 $ 26.00 Aherrenge 0872 $ 26.00 Alawa 0810 $ 26.00 Ali Curung 0872 $ 26.00 Alice Springs 0872 $ 26.00 Alice Springs 0870 $ 26.00 Almaden 4871 $ 51.50 Aloomba 4871 $ 51.50 Alyangula 0885 $ 26.00 Amata 0872 $ 26.00 American Beach 5222 $ 51.50 American River 5221 $ 51.50 Amoonguna 0873 $ 51.50 Ampilatwatja 0872 $ 26.00 Anatye 0872 $ 26.00 Andamooka 5722 $ 77.50 Anduramba 4355 $ 51.50 Angledool 2834 $ 51.50 Angurugu 0822 $ 26.00 Anindilyakwa 0822 $ 26.00 Anmatjere 0872 $ 26.00 Annie River 0822 $ 26.00 Antewenegerrde 0872 $ 26.00 Anula 0812 $ 26.00 Araluen 0870 $ 26.00 Archer 0830 $ 26.00 Archer River 4892 $ 51.50 Archerton 3723 $ 26.00 Area C Mine 6753 $ 51.50 Areyonga 0872 $ 26.00 Arnold 0852 $ 26.00 Arumbera 0873 $ 51.50 Ascot 4359 $ 77.50 Atitjere 0872 $ 26.00 Aurukun 4892 $ 51.50 Austinville 4213 $ 26.00 Avon Downs 0862 $ 26.00 Ayers Range South 0872 $ 26.00 Ayers Rock 0872 $ 26.00 Ayton 4895 $ 51.50 Badu Island 4875 $ 77.50 Bagot 0820 $ 26.00 1 Regional Area Surcharge (RAS) Baines 0852 $ 26.00 Bakewell 0832 $ 26.00 Balgowan 5573 $ 26.00 Balladonia 6443 $ 77.50 Balranald 2715 $ 77.50 Bamaga 4876 $ 77.50 Banks Island 4875 $ 77.50 -

CAE in Australia

CAE in Australia Overview technologies, CAE Australia brings proven In addition, CAE supports the Royal solutions to the Australian market and Australian Air Force’s participation in CAE is an experienced training systems surrounding region in addition to delivering Coalition Virtual Flag, which is one of the integrator across air, land, naval and world-class engineering and support world’s largest virtual air combat exercises. public safety domains. The company services. Some of the major programs led CAE Australia also includes an experienced employs 8,500 people at more than 160 by CAE Australia for the Australian Defence professional services group, which is a sites and training locations in 35 countries. Forces include: market-leading consulting and engineering CAE offers customers a complete range services organization that leverages of highly innovative product, service and ÎÎRAAF Hawk 127 Lead-in Fighter training and modelling and simulation technologies training centre solutions designed to help support services at Pearce and Williamtown; and expertise to develop software-based them meet their mission critical needs for ÎÎManagement and Support of ADF Aerospace solutions for decision support and training safety, efficiency and readiness. Simulators (MSAAS) – CAE Australia is an Authorised Engineering Organisation and in complex environments. delivers a range of training support services; ÎÎKC-30A training systems and comprehensive training services at RAAF Amberley; ÎÎC-130J training systems and support services at RAAF Richmond, including a C-130J Fuselage Trainer in development and live C-130J flight instruction; ÎÎS-70A Black Hawk full-flight and mission simulator, maintenance training systems CMMI Level 3 rating and support services at Oakey; CAE Australia is the first defence contractor ÎÎMRH90 training systems and support in Australia to achieve the CMMI Level For over 20 years CAE Australia Pty Ltd, services at Oakey and Townsville; 3 rating specifically for Services. -

View Annual Report

19 October 2017 ASX Announcement Annual Report Notice of Annual General Meeting and proxy form Attached below are Qube’s 2017: . Annual Report; and . Notice of Annual General Meeting and proxy form. Adam Jacobs Company Secretary BUILT STRONG FOR LONg-TERM GROWTH QUBE HOLDINGS LIMITED HOLDINGS QUBE ANNU A L REPORT 2017 REPORT L QUBE HOLDINGS LIMITED ANNUAL REPORT 2017 ABN 14 149 723 053 QUBE’S VISION IS TO BE AUSTRALIA’S LEadING PROVIDER OF INTEGRATED LOGISTICS SOLUTIONS FOCUSED ON IMPORT AND EXPORT SUPPLY CHAINS Contents 13 Operational Summary 2 Chairman’s Letter 20 Financial Information 4 Managing Director’s Report 134 Shareholder Information 10 Safety, Health and Environment 137 Corporate Directory ANNUAL REPORT 2017 1 Over 100 locations across Australia and NZ Over 6,500 employees and contractors No.1 in our core markets Over $3.75 billion in market capitalisation Annual General Meeting The 2017 Annual General Meeting of Qube Holdings Limited will be held at PricewaterhouseCoopers (PwC), Level 15, One International Towers Sydney, Watermans Quay, Barangaroo Sydney on Wednesday 22 November 2017 at 10.00am (Sydney time). 2 QUBE HOLDINGS LIMITED down as Chairman just prior to the end of the 2017 financial year. As many of you know, it was Chris and our Deputy Chairman Sam Kaplan, who 10 years ago began assembling the assets which would become Qube today. Under Chris’s leadership Qube has grown from a 200 million dollar investment fund to being an ASX-listed top 100 company with a market capitalisation of more than 3.75 billion dollars. I can say confidently that Chris has realised his vision of Qube becoming a major player in the freight CHAIRMan’s logistics market in Australia bringing COMpleteD overdue efficiencies to the import-export Letter acQUISITIon supply chain. -

Celebrating Clayton Utz We Have Undergone Many Changes Since Then

CELEBRATING Clayton Utz We have undergone many changes since then. However the essence of Clayton Utz, expressed in the personal qualities of our founding father George Robert Nichols, remains very much the same. Among his many virtues, Nichols was known for his legal astuteness, his passion for justice, and his desire to improve his community. These are qualities for which Clayton Utz is still known, and it is with great pride that we reflect on the contribution that George Robert Nichols and the individuals who followed in his footsteps have made in making Clayton Utz the firm we are today. In an increasingly competitive legal market, Clayton Utz consistently stands out for the quality of our legal work and our people. Our commitment to the community is also an important part of who we are, and we are proud of our Community Connect program which reaches out to hundreds of individuals and organisations across the country through pro bono legal work, financial assistance through grants, and volunteering. We thank our people for their ongoing support of the program, and for the investment they have made and continue to make in our firm. In celebrating 175 years of legal service to the Australian community, One hundred and seventy five years ago, the we also acknowledge the enormous contribution of the many people who over the years have helped to build the Clayton Utz community. foundations were laid for what today is one From a one-man firm in colonial Sydney, we are now a truly national of Australia’s greatest law firms - our firm, firm with 216 partners and over 950 lawyers in six offices around Australia, servicing the needs of our many valued and loyal clients whenever - and wherever - they are doing business. -

QUBE SUBORDINATED NOTES Prospectus for the Issue of Qube Subordinated Notes to Be Listed on ASX

QUBE SUBORDINATED NOTES Prospectus for the issue of Qube Subordinated Notes to be listed on ASX Issuer Joint Structuring Advisers Joint Lead Managers Co-Managers Qube Holdings Limited National Australia Bank ANZ Securities Crestone Wealth Management ABN 14 149 723 053 UBS National Australia Bank JBWere UBS Morgans IMPortant notiCes This Prospectus information on how Qube (and its agents) collects, in Appendix A. If there is any inconsistency in This Prospectus is issued by Qube Holdings Limited holds and uses this personal information. definitions between the Prospectus and the Terms, the definitions in the Terms prevail. (ABN 14 149 723 053) (“Qube”). Restrictions on distribution This Prospectus is dated and was lodged with the This Prospectus does not constitute an offer of Notes Time Australian Securities and Investments Commission or invitation in any place in which, or to any person Unless otherwise stated or implied, references to (“ASIC”) on 7 September 2016. This is a to whom, it would not be lawful to make such an times in this Prospectus are to Sydney time. replacement prospectus that replaces the prospectus offer or invitation. Refer to Section 6.3.2 for further Disclaimer dated and lodged with ASIC on 30 August 2016 information. (“Original Prospectus”). This Prospectus expires on No person is authorised to give any information Notes have not been, and will not be, registered the date which is 13 months after 30 August 2016 or to make any representation in connection with under the U.S. Securities Act of 1933, as amended (“Expiry Date”) and no subordinated notes (“Notes”) the Offer described in this Prospectus which is not (the “U.S.