Moss Adams LLP (Headquartered in Seattle, Washington)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The 2020 Ipa Top 400 Firms

THE 2020 INSIDE PUBLIC ACCOUNTING TOP 400 ACCOUNTING FIRMS AUGUST 2020 INSIDE PUBLIC ACCOUNTING / 1 THE 2020 IPA TOP 100 FIRMS ’20 ’19 FIRM / HEADQUARTERS MP / CEO OFFICES FYE NET REVENUE % CHG. × 1 1 Deloitte / New York Joe Ucuzoglu 130 6/19 $21,913,000,000 DND 2 2 PwC / New York Tim Ryan 91 6/19 $17,400,000,000 3.3 3 3 EY / New York Kelly Grier 104 6/19 $15,000,000,000 7.1 4 4 KPMG LLP / New York Lynne Doughtie 102 9/19 $9,970,000,000 5.4 5 5 RSM US LLP / Chicago Joe Adams 91 4/20 $2,706,305,000 10.0 × 6 6 Grant Thornton LLP / Chicago Brad Preber 56 12/19 $1,950,562,000 DND 7 7 BDO USA LLP1 / Chicago Wayne Berson 67 4/20 $1,803,000,000 5.8 8 8 CLA / No Headquarters Identified Denny Schleper 120 12/19 $1,145,980,736 9.9 9 9 Crowe LLP / Chicago James Powers 38 3/20 $983,286,447 3.3 10 10 CBIZ & MHM2 / Cleveland / Kansas City, Mo. Chris Spurio / Andy Burczyk 91 / 27 12/19 $811,000,000 2.8 11 13 Baker Tilly / Chicago Alan Whitman 48 5/20 $789,600,000 4.0 12 12 Moss Adams LLP / Seattle Chris Schmidt 28 12/19 $768,000,000 9.5 13 16 Plante Moran / Southfield, Mich. James E. Proppe 26 6/20 $731,189,000 6.4 14 14 CohnReznick LLP / New York Frank Longobardi 26 1/20 $697,258,732 6.8 15 13 BKD LLP / Springfield, Mo. -

Moss Adams Wealth Advisors Llc Disclosure Brochure and Privacy Policy

MOSS ADAMS WEALTH ADVISORS LLC DISCLOSURE BROCHURE AND PRIVACY POLICY Pursuant to SEC Rule 206(4)-3 March 2021 Main Office: Moss Adams Wealth Advisors LLC 999 Third Ave., Suite 2800 Seattle, WA 98104 (206) 302-6500 This brochure provides information about the qualifications and business practices of Moss Adams Wealth Advisors. If you have any questions about the content of this brochure, please contact us at [email protected] or (206)302-6500. The information in this brochure has not been approved or verified by the United States Securities and Exchange Commission or by any state securities authority. Table of Contents Material Changes 4 Additional Office Locations 5 Advisory Business 6 Introduction 6 Investment Management Services 6 Custom Fixed Income Management 8 Financial Planning 9 Investment Consulting Services 10 Fees and Compensation 11 Fees for Investment Management Services – Private Client 11 Fees for Investment Management Services – Institutional 12 Fees for Custom Fixed Income Management 12 Fees for Financial Planning 15 Fees for Investment Consulting Services 15 Types of Clients 16 Methods of Analysis, Investment Strategies and Risk of Loss 16 Methods of Analysis 16 Investment Strategies 16 Types of Investments 19 Pandemic Risk 20 Disciplinary Information 20 Other Financial Industry Activities or Affiliations 20 Moss Adams 20 Long Road Risk Management Services, LLC / Valmark Policy Management Company 21 Table of Contents – Continued Non-Investment Consulting / Implementation Services 21 Additional Reporting Services -

Supporting Materials

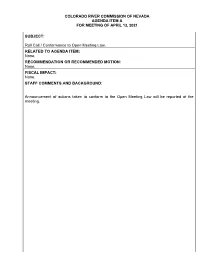

COLORADO RIVER COMMISSION OF NEVADA AGENDA ITEM A FOR MEETING OF APRIL 13, 2021 SUBJECT: Roll Call / Conformance to Open Meeting Law. RELATED TO AGENDA ITEM: None. RECOMMENDATION OR RECOMMENDED MOTION: None. FISCAL IMPACT: None. STAFF COMMENTS AND BACKGROUND: Announcement of actions taken to conform to the Open Meeting Law will be reported at the meeting. COLORADO RIVER COMMISSION OF NEVADA AGENDA ITEM B FOR MEETING OF APRIL 13, 2021 SUBJECT: Comments from the public. (No action may be taken on a matter raised under this item of the agenda until the matter itself has been specifically included on an agenda as an item upon which action may be taken.) RELATED TO AGENDA ITEM: None. RECOMMENDATION OR RECOMMENDED MOTION: None. FISCAL IMPACT: None. STAFF COMMENTS AND BACKGROUND: COLORADO RIVER COMMISSION OF NEVADA AGENDA ITEM C FOR MEETING OF APRIL 13, 2021 SUBJECT: For Possible Action: Approval of minutes of the February 9, 2021 meeting. RELATED TO AGENDA ITEM: None. RECOMMENDATION OR RECOMMENDED MOTION: Approval of the minutes will be recommended at the meeting. FISCAL IMPACT: None. STAFF COMMENTS AND BACKGROUND: The minutes of the February 9, 2021 meeting is enclosed for your review. The Colorado River Commission of Nevada (Commission) meeting was held at 1:30 p.m. on Tuesday, February 9, 2021 via video conference, pursuant to Emergency Directive 006, section 1. COMMISSIONERS IN ATTENDANCE Chairwoman Puoy K. Premsrirut Vice Chairwoman Kara J. Kelley Commissioner Justin Jones Commissioner Marilyn Kirkpatrick Commissioner Allen J. Puliz Commissioner Dan H. Stewart Commissioner Cody T. Winterton DEPUTY ATTORNEY GENERAL Special Counsel, Attorney General Christine Guerci COMMISSION STAFF IN ATTENDANCE Executive Director Eric Witkoski Senior Assistant Director Sara Price Chief of Finance and Administration Douglas N. -

Moss Adams LLP Proposal

February 15, 2013 PROPOSAL FOR City of Milwaukie, Oregon Prepared by: James C. Lanzarotta, Partner Annamarie McNiel, Manager Moss Adams LLP 975 Oak Street, Suite 500 Eugene, Oregon 97401 (541) 686-1040 [email protected] February 15, 2013 Rina M. Byrne City of Milwaukie 10722 SE Main Street Milwaukie, Oregon 97222 Dear Ms. Bryne: We are pleased to present this proposal to the City of Milwaukie (“the City”). We understand this proposal is for the annual financial and compliance examination of the City’s CAFR beginning with the fiscal year ending June 30, 2013 extending through the next four subsequent fiscal years and that upon completion of the audit for each fiscal year the City requires the following reports: • Audit opinion on the City’s financial statements (CAFR) in accordance with Generally Accepted and Government Auditing Standards, including component units not requiring stand-alone financial statements • All reports required for compliance with the provisions of OMB Circular A-133 and Single Audit Act Amendment of 1996, if necessary • Communications with those charged with governance (SAS 114 Letter) • Management Letter related to internal controls, compliance with laws and regulations and accounting systems, functions and procedures especially in regards to Cost effectiveness • Make immediate written reports of irregularities and illegal acts to management • Be available throughout the year to provide ongoing consulting services for minor financial issues that may occur, all at no additional cost We deliver our audits, unlike many firms, with significant partner and senior manager level attention. Your audit team is dedicated to the industry, and our firm is one of the most experienced in conducting audits in accordance with the Single Audit Act and Office of Management and Budget (OMB) Circular A-133. -

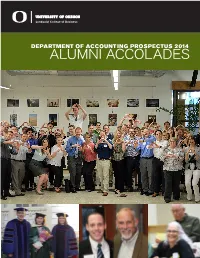

ALUMNI ACCOLADES TABLE of CONTENTS DEPARTMENT of ACCOUNTING 3 Hello from Dave

DEPARTMENT OF ACCOUNTING PROSPECTUS 2014 ALUMNI ACCOLADES TABLE OF CONTENTS DEPARTMENT OF ACCOUNTING 3 Hello from Dave 4 The Accounting Circle 6 Faculty Focus TOP TEN The accounting faculty was ranked second worldwide in 7 Research 1 publishing academic tax research over the past six years. They are ranked third over the past 12 years, and fourth over all years, 8 PhD Program according to ratings compiled by Brigham Young University. 9 MAcc Program 2 Ryan Wilson received the Lundquist College of Business 2014 10 Beta Alpha Psi Goulet Research Excellence Award. This is the sixth consecutive year, and the seventh time in the past eight years, that a member 12 Scholarships of the accounting faculty has been honored with this award. 13 Donor Honor Roll 3 Accounting alumna Tiffany Phillips ’13 was awarded the esteemed Elijah Watt Sells Award for 2013. This award is for people who earned a cumulative average score above 95.5 on the CPA exam, completed testing over the 2013 calendar year, and passed all four sections on their first attempt. This is the second year in a row that a UO accounting alum has earned this honor. 4 Master of Accounting Program alum Yujie “Jack” Zhang ’13, MActg ’14, was one of only 97 students in the United States to win the AICPA Scholarship for Minority Accounting Students for 2013–14. The award recognizes academic achievement, leadership, and commitment to pursuing the CPA. Jack also was honored with the UO Centurion Award for his dedication and outstanding service as a student leader. 5 Tiffany Phillips ’13, William Geller ’12, and Eric Seifert ’12, MActg ’13, earned the three highest scores on the CPA exam in Kelly Bosch presents Anna Karvina Oregon for 2013. -

West Contra Costa Unified School District

FORENSIC ACCOUNTING INVESTIGATION IMPLEMENTATION REVIEW WORK PLAN FOR WEST CONTRA COSTA UNIFIED SCHOOL DISTRICT Peder Jensen, CCA, Senior Manager Moss Adams LLP 101 Second Street, Suite 900 San Francisco, CA 94105 (415) 956-1500 Dear Mr. Johnston: Thank you for the opportunity to present our approach for forensic accounting investigation implementation review services for the West Contra Costa Unified School District (the District). We understand you’re seeking a service provider with a depth of functional skills necessary to review the implementation of recommendations from the forensic accounting investigation performed by Vincenti, Lloyd & Stutzman LLP (VLS) in 2016. Our team will consistently provide the District with the highest quality services. We bring experienced professionals with deep knowledge of the construction industry, as well as school district and bond program management and oversight. Our approach is collaborative, and we’ll include your team in every step of the review process to successfully deliver value-added results. Our performance as construction auditors and business advisors will demonstrate our commitment to high-quality services that are consistent with our proven track record. August 8, 2017 We look forward to helping the District monitor the implementation of David Johnston recommendations previously identified and improve the processes, procedures, and Executive Director management of the bond program. If you’ve questions regarding this work plan, General Services please don’t hesitate to contact me. West -

22Nd Annual AGC/CFMA Construction Financial Management Conference Name Company City, State

22nd Annual AGC/CFMA Construction Financial Management Conference Name Company City, State Alabama Matt Griffith ML Griffith CPA, LLC Birmingham, AL Mindy Reed RSM Birmingham, AL Arizona Garey Bryant FNF Construction, Inc. Tempe, AZ Woodrow Chamberlain eMars Inc. Scottsdale, AZ John Corcoran CICPAC Fountain Hills, AZ David Doerge eMars Inc. Scottsdale, AZ Kyla Greene West Point Contractors, Inc. Tucson, AZ Mark Liss Explorer Software North Vancouver, AZ Blair McCarty Beneco Scottsdale, AZ Randy Riter DPR Construction Gilbert, AZ Lawrence Rosenblum CBIZ & Mayer Hoffman McCann, PC Phoenix, AZ Michelle Walker SSC Boring Phoenix, AZ California Abir Alameddine Kana Pipeline, Inc. Riverside, CA Eric Bader Pacific Rim Mechanical San Diego, CA Katharine Baldwin The Dutra Group San Anselmo, CA Michael Barrows Barrows & Company, CPA's Camarillo, CA Kristine Bearden Moss Adams, LLP Rancho Cordova, CA Ron Benoza Procore Carpinteria, CA Jackie Buck Harper Construction Company, Inc. San Diego, CA Tracey Burns Century Housing Corp. Culver City, CA John Callan CliftonLarsenAllen, LLCP Walnut Creek, CA John Cassidy Mark III Construction Sacramento, CA Kimberly Cook KZ Miller Construction Inc. Irvine, CA Matt Cruzat MGE Underground Paso Robles, CA Todd Daily Herman Construction Group, Inc. Escondido, CA Robin Davis American General Construction, Inc. Long Beach, CA Jeffrey DiMercurio Johnston, Gremaux & Rossi, LLP Pleasant Hill, CA John Donahue PlanGrid San Francisco, CA Jeff Douglas LCPtracker, Inc. Orange, CA David Eveland Southern Contracting Company San Marcos, CA Victoria Feigin All Seasons Roofing & Waterproofing San Jose, CA Chris Gewain Moss Adams, LLP Irvine, CA Debbie Ghadiri Johnstone Moyer, Inc. San Carlos, CA Janet Godfrey Webcor Construction, LP Alameda, CA Bryson Groat Risk Management Advisors, Inc. -

Innovation and Shifting Paradigms 2016 Health Care Conference MOSS ADAMS | 2016 Health Care Conference | 1

Innovation and Shifting Paradigms 2016 Health Care Conference MOSS ADAMS | 2016 Health Care Conference | 1 Innovation and Shifting Paradigms 2016 Health Care Conference NOVEMBER 3, 2016 Thank you for joining us here at the beautiful Red Rock Resort. We’re excited to present this year’s conference, Positioning for the Future: Innovations and Shifting Paradigms. This event promises to be thought provoking during this unprecedented time in health care, with an uncertain political future, evolving risk-sharing programs, game-changing technology, and a new focus on consumerism. Our goal is to provide a forum that empowers you, as leaders of your respective organizations, with insight from panels and discussions with industry visionaries. On the eve of the 2016 presidential election, we’re excited to hear from our keynote speakers, the Honorable Newt Gingrich and Senator Joe Lieberman, who will present their predictions for health care policy in a point-counterpoint discussion moderated by Emmy Award-winning journalist Farland Chang. In other sessions, you’ll hear from Lisa Bielamowicz, executive director and CMO of The Advisory Board Company, and Roni Zeiger, co-founder of Smart Patients and former Chief Health Strategist at Google. During our two days together, we’ll tackle vital industry topics such as health care reform with new health system strategies, lessons learned from mergers and acquisitions, integrating behavioral health into the triple aim, using big data to impact population health, and more. We’d like to extend our utmost appreciation to our sponsors—Foley & Lardner, Lancaster Pollard, UnitedHealthcare, Arthur J. Gallagher & Co., and State of Reform. Their support enhances our ability to present a stimulating and enlightening conference. -

Comply with State Laws Using State-By-State Apportionment Schedules

WHITE PAPER Comply with State Laws Using State-by-State Apportionment Schedules A version of this white paper was previously published in the June 2018 edition of the Journal of Multistate Taxation and Incentives. 02 APPORTIONMENT SCHEDULES BY STATE Determining the appropriate sales factor numerator and denominator 02 PASS-THROUGH ENTITY APPORTIONMENT CONSIDERATIONS: requires navigating multiple, often contradictory state tax rules—especially CURRENT OPERATIONS for a taxpayer with several sources of revenue, complex operations, and a AND TRANSACTIONS potentially global reach. The increasingly common practice of conducting business through pass-through entities (PTEs), such as limited liability 04 INCLUDING TRANSACTIONS companies (LLCs), adds another dimension to the analysis. WHEN CALCULATING THE When a taxpayer disposes of its investment in a business contained SALES FACTOR: BASE RULES in a PTE, either through selling the assets or selling the interest in the 05 INCLUDING TRANSACTIONS WHEN PTE, various state rules—either statutory or developed through case CALCULATING THE SALES FACTOR: law—may apply. The taxpayer may need to analyze whether, and how, the EXCLUSION FOR SUBSTANTIAL transaction should be reflected in the sales factor and documented in the RECEIPTS FROM OCCASIONAL SALES apportionment schedules. 06 ANALYSIS OF THE EXCLUSION Taxpayers should also consider new, potentially significant changes OF SUBSTANTIAL RECEIPTS resulting from tax reform, commonly known as the Tax Cuts and Jobs Act FROM OCCASIONAL SALES: (TCJA). One such addition is the new class of Subpart F Income, which is TREATMENT OF GOODWILL AND effective for tax years ending on December 31, 2017. OTHER INTANGIBLE ASSETS 07 STATE SOURCING OF RECEIPTS 09 MARKET SOURCING AND THE REVISED MTC REGULATION 10 DIVIDENDS 13 CONCLUSION The material appearing in this communication is for informational purposes only and should not be construed as advice of any kind, including, without limitation, legal, accounting, or investment advice. -

Do You Have What It Takes? Eligibility Apply

Do You Have What It Takes? About Us Enhancing your leadership skills. Getting ahead of the competition. Moss Adams LLP is the largest accounting and Jump‐starting your career. consulting firm headquartered in the West and one of the largest in the United States. If you’re an exceptional student interested in gaining a greater understanding of Founded in 1913 and headquartered in Seattle, the dynamic field of public accounting, we invite you to apply for our summer we serve our clients from 24 locations leadership conference. It’s an interactive training program designed to throughout Washington, Oregon, California, New Mexico, Arizona, Kansas, and Texas. illuminate the factors critical to your future success. We provide audit, accounting, tax, and business What’s more, you’ll meet and network with your peers as well as with advisory services to middle‐market enterprises Moss Adams professionals. We’ll discuss what it means to be in public (both public and private) and their owners, and accounting today, with a special focus on enhancing your leadership skills. we’re among the market leaders in many industry sectors, including manufacturing, Don’t miss this opportunity to take your first step into the world of public construction, apparel, not‐for‐profit, financial accounting. institutions, forest products, health care, telecom, and automotive dealerships. Eligibility We serve clients with regional and national needs, and we have an international practice We’re seeking bright and ambitious students who have approximately two years that enables clients to develop and grow their remaining in their accounting coursework and a strong desire to pursue a career business on a global scale. -

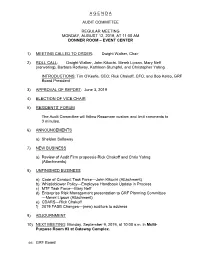

Audit Agenda, Aug. 12, 2019

A G E N D A AUDIT COMMITTEE REGULAR MEETING MONDAY, AUGUST 12, 2019, AT 11:00 AM DONNER ROOM – EVENT CENTER 1) MEETING CALLED TO ORDER: Dwight Walker, Chair 2) ROLL CALL: Dwight Walker, John Kikuchi, Merek Lipson, Mary Neff (nonvoting), Barbara Rothway, Kathleen Stumpfel, and Christopher Yahng INTRODUCTIONS: Tim O’Keefe, CEO; Rick Chakoff, CFO; and Bob Kelso, GRF Board President 3) APPROVAL OF REPORT: June 3, 2019 4) ELECTION OF VICE CHAIR 5) RESIDENTS’ FORUM The Audit Committee will follow Rossmoor custom and limit comments to 3 minutes. 6) ANNOUNCEMENTS a) Sheldon Solloway 7) NEW BUSINESS a) Review of Audit Firm proposals-Rick Chakoff and Chris Yahng (Attachments) 8) UNFINISHED BUSINESS a) Code of Conduct Task Force—John Kikuchi (Attachment) b) Whistleblower Policy—Employee Handbook Update in Process c) MTF Task Force—Mary Neff d) Enterprise Risk Management presentation to GRF Planning Committee —Merek Lipson (Attachment) e) CDARS—Rick Chakoff f) 2019 FASB Changes—(new) auditors to address 9) ADJOURNMENT 10) NEXT MEETING: Monday, September 9, 2019, at 10:00 a.m. in Multi- Purpose Room #3 at Gateway Complex. cc: GRF Board 3-1 AUDIT COMMITTEE REPORT REGULAR MEETING MONDAY, JUNE 3, 2019, AT 10:00 A.M. A regular meeting of the Audit Committee was convened by the Chair, Dwight Walker, at 10:00 a.m. on Monday, June 3, 2019, in the Board Room at Gateway Complex. Members present were Dwight Walker, Chair; John Kikuchi, Mary Neff, Alan Swanson, Roll Call Barbara Rothway and Chris Yahng. Excused absence: Sheldon Solloway, Also attending were Tim O’Keefe, CEO; Rick Chakoff, CFO; and GRF Board members: Dale Harrington and Kathleen Stumpfel; and Chris Preminger, Business Ops Manager 1. -

This Brochure Provides Information About the Qualifications and Business Practices of Moss Adams Wealth Advisors

This brochure provides information about the qualifications and business practices of Moss Adams Wealth Advisors. If you have any questions about the content of this brochure, please contact us at [email protected] or (206)302‐6717. The information in this brochure has not been approved or verified by the United States Securities and Exchange Commission or by any state securities authority. Material Changes This brochure, dated March 2017, includes the below material changes since Moss Adams Wealth Advisors LLC’s last update in March 2016. Moss Adams Wealth Advisors’ clients may request a full copy of the latest version of this brochure at any time by contacting your advisor or Gidget Furness, Chief Compliance Officer, at the Seattle office. Additional information about Moss Adams Wealth Advisors is also available on the SEC’s website at www.adviserinfo.sec.gov. Please note: Registration with the SEC does not imply a certain level of skill or training. Material Changes: In August 2016, Erica Coogan took over as Partner in Charge of Moss Adams Wealth Advisors LLC. She took over leadership from Rebecca Pomering, who assumed the Chief Practice Officer position for Moss Adams LLP. Ms. Coogan has been with Moss Adams Wealth Advisors for over 18 years, leading the practice in the Puget Sound region for much of her tenure. She has chaired the investment team and currently serves as a member of the Moss Adams partner review committee. In her new role, Coogan is responsible for the growth of Moss Adams Wealth Advisors, including strategic planning, sales and marketing, team development and mergers and acquisitions.