Form 10-Q/A Amendment No. 1 SECURITIES and EXCHANGE COMMISSION WASHINGTON, DC 20549

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

1 Mill Gazetteer OFFICIAL

1 Mill Gazetteer OFFICIAL. ORGAN OF THE INTERNATIONAL AND TRI-STATES OIL MILL SUPERINTENDENTS ASSOCIATION Arizona Cottonseed Products Company, Gilbert, Arizona OFFERING THESE UNIQUE, OUTSTANDING FEATURES 0 Custom designed to meet your capacity re- Q No chains, sprockets or sprocket shafts to break quirements. or distort. 0 Will process prepress cake from all vegetable Q Individual basket supports prevent mechanical oilseeds and other materials such as cracklings. stress. 0 Hydraulic drive for opevati iwa 1 siiwgjjiwty and Q Mechanically tested at the factory and shipped mechanical safety. sJS / assembled ready for mounting on its foundation. Bulletin 16i contains operational details. Send for your free copy. THE V. D. ANDERSON COMPANY Division of IBEC 1 935 WEST 96th STREET • CLEVELAND 2, OHIO °LUMS; 7 NUMBER 12 "Our 70th Year" JUNE, 1966 looking for a pure extraction solvent? order■ SK E L L w S O LVE 1. Purity. Hydrogenation plus dual complete recovery. The result— im oil color, odor and low refining loss. refining gives Skellysolve a lower portant savings to you in labor, time 4. Like to know more? W e will benzene content and even greater and steam. be glad to answer any question you purity. Oil and meal are upgraded may have— based on over 30 years Because because you can eliminate foreign 3 .Balanced composition. experience serving the Vegetable Oil of the balanced composition, Skelly tastes, odors and residues. Extraction Industry. Call Les Weber solve has high selective solvency. or Carl Senter for the prompt de 2. Narrow boiling range. Skelly- That’s why you can expect to get pendable delivery that is a tradition solve’s narrow boiling range allows maximum oil yield with improved with Skelly. -

Fall 2013 Volume 11 Number 3 the Community Have Been Students’ Education Outside She Became an Assistant Professor in Former President Dr

The magazine of Missouri Western State University Missouri FallWestern 2013 Looking back, looking forward: Robert A. Vartabedian p.14 AROUND CAMPUS PRESIDENT’S PERSPECTIVE Dear Alumni and Friends, the success of our student athletes both on the field and This issue is about looking back, in the classroom has been a and looking forward. highlight of my presidency. “Miss Saigon” It has been an honor to be your Of particular pride Missouri Western’s summer theatre, Western president for the last five years. are Missouri Western’s Playhouse, captivated audiences in July with I have enjoyed meeting so burgeoning arts programs. its production of the musical, “Miss Saigon.” many members of the Griffon We now have more than 250 The show ran six performances to great crowds. family and learning all of Fireworks followed the July 5 performance. members in the Missouri the ways that Missouri Western State Western Arts Society and numerous University has transformed the lives of accomplishments, awards and special our students, staff, alumni and community events in the visual and performing arts. members. There is also much to anticipate In fact, the tremendous growth in these as I look forward to the next five years of areas has necessitated the creation of the my presidency. School of Fine Arts and the hiring of a At the heart of our University are our founding dean, Dr. Bob Willenbrink. academic programs. Missouri Western But that’s not all. As we look to the next boasts uniformly positive accreditation five years, there is much to anticipate. visits across programs, a rare feat for a University. -

Area Wage Survey: Omaha, Nebraska, Iowa, Metropolitan Area

/ ®? « 'S ; Area " Omaha, Nebraska Iowa, Wage Metropolitan Area Survey October 1979 U.S. Department of Labor Bureau of Labor Statistics Bulletin 2050-51 A# Pottawattamie j r & > c V s v V >kO rfS9 ^ Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis Preface This bulletin provides results of an October 1979 survey of occu pational earnings in the Omaha, Nebraska—Iowa, Standard Metropolitan Statistical Area. The survey was made as part of the Bureau of Labor Statistics' annual area wage survey program. It was conducted by the Bureau's regional office in Kansas City, Mo., under the general direction of Edward Chaiken, Assistant Regional Commissioner for Operations. The survey could not have been accomplished without the cooperation of the many firms whose wage and salary data provided the basis for the statistical information in this bulletin. The Bureau wishes to express sincere appreciation for the cooperation received. Material in this publication is in the public domain and may be reproduced without permission of the Federal Government. Please credit the Bureau of Labor Statistics and cite the name and number of this publication. Note: A current report on occupational earnings in the Omaha area is available for the moving and storage (October 1979) industry. Also available are listings of union wage rates for building trades, printing trades, local-transit operating employees, local truckdrivers and helpers, and grocery store employees. Free copies of these are available from the Bureau's regional offices. (See back cover for addresses.) Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. -

Country and City Codes

We hope this information will be useful to you in your travels! The information is believed to be reliable and up to date as of the time of publication. However, no warranties are made as to its reliability or accuracy. Check with Full Service Network Customer Service or your operator for official information before you travel. Country and City Codes Afghanistan country code: 93 Albania country code: 355 city codes: Durres 52, Elbassan 545, Korce 824, Shkoder 224 Algeria country code: 213 city codes: Adrar 7, Ain Defla 3, Bejaia 5, Guerrar 9 American Samoa country code: 684 city codes: City codes not required. All points 7 digits. Andorra country code: 376 city codes: City codes not required. All points 6 digits. Angola country code: 244 Anguilla country code: 264 Antarctica Casey Base country code: 672 Antarctica Scott Base country code: 672 Antigua (including Barbuda) country code: 268 city codes: City codes not required. * Footnote: You should not dial the 011 prefix when calling this country from North America. Use the country code just like an Area Code in the U.S. Argentina country code: 54 city codes: Azul 281, Bahia Blanca 91, Buenos Aires 11, Chilvilcoy 341, Comodoro Rivadavia 967, Cordoba 51, Corrientes 783, La Plata 21, Las Flores 224, Mar Del Plata 23, Mendoza 61, Merio 220, Moreno 228, Posadas 752, Resistencia 722, Rio Cuarto 586, Rosario 41, San Juan 64, San Rafael 627, Santa Fe 42, Tandil 293, Villa Maria 531 Armenia country code: 374 city codes: City codes not required. Aruba country code: 297 city codes: All points 8 plus 5 digits The Ascension Islands country code: 247 city codes: City codes not required. -

Termination of Consent Order GRANDVIEW, MO (February 26, 2014) – NASB Financial, Inc

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 8-K CURRENT REPORT Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event reported): February 25, 2014 NASB FINANCIAL, INC. (Exact Name of Registrant as Specified in its Charter) Missouri 0-24033 43 -1805201 (State or Other Jurisdiction of (Commission File Number) (I.R.S. Employer Identification No.) Incorporation or Organization) 12498 South 71 Highway, Grandview, Missouri 64030 (Address of Principal Executive Offices) (Zip Code) Registrant’s telephone number, including area code: (816) 765-2200 Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions: Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14d-2(b)) Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14a-12) Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) Item 8.01 Other Events On February 25, 2014, the Board of Directors of North American Savings Bank, F.S.B. (the “Bank”), a wholly owned subsidiary of NASB Financial, Inc. (the “Company”), was notified by the Office of the Comptroller of the Currency (the “OCC”), the Bank’s primary regulator, that they were terminating their Consent Order with the Bank, dated May 22, 2012, effective immediately. -

Area Wage Survey: the Rockford, Illinois, Metropolitan Area, May

L 7.> 3. 1 1 V\ Dayt Montgomery Co* . r.'ic Library "" f ,5 1971 f OCUMENT COLLECTION ; AREA WAGE SURVEY he Rockford. Illinois, Metropolitan Area, M ay 1971 . ■ ■ EL . ’ ‘ >t * ■ - -i ■■ fffl < .? ' Bulletin 1685-79 Digitized for FRASER U.S. DEPARTMENT OF LABOR / Bureau of Labor Statistics http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis BUREAU OF LABOR STATISTICS REGIONAL OFFICES ALASKA Region I Region II Region III Region IV 1603-A Federal Building 341 Ninth Ave., Rm. 1025 406 Penn Square Building Suite 540 Government Center New York, N.Y. 10001 1317 Filbert St. 1371 Peachtree St. NE. Boston, Mass. 02203 Phone: 971-5405 (Area Code 212) Philadelphia, Pa. 19107 Atlanta, Ga. 30309 Phone: 223-6761 (Area Code 617) Phone: 597-7796 (Area Code 215) Phone: 526-5418 (Area Code 404) Region V Region VI Regions V II and V III Regions IX and X 219 South Dearborn St. 1100 Commerce St., Rm. 6B7 Federal Office Building 450 Golden Gate Ave. Chicago, III. 60604 Dallas, Tex. 75202 911 Walnut St., 10th Floor Box 36017 Phone: 353-7230 (Area Code 312) Phone: 749-3516 (Area Code 214) Kansas City, Mo. 64106 San Francisco, Calif. 94102 Phone: 374-2481 (Area Code 816) Phone: 556-4678 (Area Code 415) Regions V II and V III will be serviced by Kansas City. Regions IX and X will be serviced by San Francisco. Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis U.S. DEPARTMENT OF LABOR J. D. Hodgson, Secretary BUREAU OF LABOR STATISTICS Geoffrey H. -

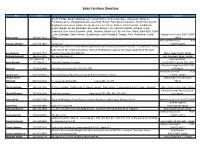

Sales Territory Directory

Sales Territory Directory Rep Cell # Territory Support South Florida: Miami, Miami Beach, Coral Gables, Fort Lauderdale, Hollywood, Miramar, Pembroke pines, Pompano Beach, Deerfield, Stuart, Palm Beach Gardens, West Palm Beach, Boynton beach, Boca Raton, Delray Beach, Fort Myers, Naples, Port Charlotte, Caribbean: Virgin Islands, Aruba, Barbados, Bermuda, Bonaire, the Cayman Islands, Antigua, Cuba, Dominica, Dominican Republic, Haiti, Jamaica, Montserrat, Puerto Rico, Saba, Saint Kitts, Saint Lucia, Grenada, Saint Vincent, Guadeloupe, and Trinidad & Tobago. Plus: Argentina, Costa Fabiola Pierre-Louis 9:00- 5:00ET Alana Lopez 305.609.7122 Rica x8164 Brittany Richardson 9:00- Amanda Webber 310.729.2037 LA CA area. 5:00 PT x6003 Mexico City, Parts of TX-San Antonio, Austin & Corpus Christi; area codes 210, 361, 512, 830, 956. Share codes 254 & 325 w/Denise Kashout. Parts of TX (Midland, Lubbock, San Angel, Amarillo, El Paso and Ann Maupin 830.822.4772 Odessa; area code 432, 806, 915 Becky Taylor 10-6CT x6013 Barbara Bushnell 206.255.5205 WA and Northern ID Scot Campbell 10-6CT x6008 917.445.1714 p Ansley Holmes Barry Skolnik 212.886.8212 Sales Mgr Strategic Business 9:00-5:00 EST ph212.752.2535 Christina Ewing-Perry 9:00-5:00 Ben Coy 713.828.1644 Houston, area codes 281, 713, 832, 979 EST X8160 Krishawna Johnson 9:30- Carol Austin 617.773.7125 Boston Nashua & Manchester, NH, VT & Port Smith NH. Maine 5:30ET x8165 Carolyn Sears- Debbie Deanna 9:00-5:00ET Michaud 860.391.2139 CT, area code 203 & 860, part of MA, all of RI X8170 Carrie Knudsen -

'P Ia Itu Le a L& T

W f ~ * T P * ~/Xe 'P ia itu lea l& t NINETIETH YEAR CHATSWORTH, ILLINOIS, THURSDAY, AUGUST 6, 1964 NUMBER 50 Donald Gerdes Barbara Franey and Wayne Marries Girl From Biasing Married Saturday . Miss Barbara Grace Franey of Ted Grulikowski of Dearborn, Lima, Peru Chatsworth and Wayne Gill Kiss Mich, served as best man and ing of New Lenox were married Allen Hagen of Chicago; Chris Miss Teresa Alge, daughter of Saturday, August 1 at 11 a.m. Klasing of New Lenox, brother of Mrs. Edward Costanda of Lima, at Sts. Peter and Paul Catholic the bridegroom; and Gerry Szon- Peru, and the late Mr. Costanda, Church. The Rev. Michael Van tagh of Grayslake were grooms and Donald L. Gerdes, son of Mr. Raes officiated at the Nuptial men. and Mrs. Donald C. Gerdes of Mass and double ring ceremony Ushering were William and Chatsworth, were married Satur before an altar flanked with pink James Franey of Chatsworth, day afternoon, August 1. gladioli. brothers of the bride. The double ring ceremony was Sister Josette of Chatsworth For her daughter's wedding, performed by the Rev. Michael was organist and the Children’s Mrs. Franey chose a blue em Van Raes at Sts. Peter and Paul Choir sang. broidered linen sheath and the Catholic Church before an altar Parents of the couple are Mr. bridegroom’s mother chose an flanked with pink and white and Mrs. John T. Franey of aqua silk sheath. Both wore an gladioli. Chatsworth and Mr. and Mrs. C. orchid corsage. Sister Josette played organ se L. -

Kansas City Southern 2003 Annual Report

KANSAS CITY SOUTHERN 2003 ANNUAL REPORT OPERATING FOR THE LONG HAUL Kansas City Southern is a transportation holding company whose primary subsidiary, The Kansas City Southern Railway Company, is one of seven Class I railroads in the United States. KCS also has investments in Grupo TFM in Mexico and the Panama Canal Railway Company in Panama. The combined North American rail network comprises approximately 6,000 miles of rail lines that link commercial and industrial markets in the United States and Mexico. Cover: Frank Newman, Carman, Baton Rouge, LA. © 2002 Robert Fenton Houser KANSAS CITY SOUTHERN 2003 FINANCIAL HIGHLIGHTS Dollars in Millions, Except per Share Amounts, Years Ended December 31 2003 2002 2001 2000 1999 OPERATIONS (i) Revenues $ 581.3 $ 566.2 $ 583.2 $ 578.7 $ 609.0 Operating income 29.1 48.0 55.4 57.8 64.1 Income from continuing operations before cumulative effect of accounting change 3.3 57.2 31.1 16.7 10.2 Net income (ii) 12.2 57.2 30.7 380.5 323.3 FINANCIAL CONDITION Working capital $ 133.3 $ 29.9 $ 7.3 $ (30.1) $ (45.7) Total assets (iii) 2,152.9 2,008.8 2,010.9 1,944.5 2,672.0 Total debt 523.4 582.6 658.4 674.6 760.9 Common stockholders’ equity (iii) 764.6 746.8 674.2 637.3 1,277.0 Total stockholders’ equity (iii) 963.7 752.9 680.3 643.4 1,283.1 PER COMMON SHARE (i) Earnings (loss) per diluted share from continuing operations before cumulative effect of accounting change $ (0.04) $ 0.91 $ 0.51 $ 0.28 $ 0.17 Dividends per share – – – – 0.32 Book value (iv) 12.30 12.22 11.38 10.96 8.36 STOCK PRICE RANGES (i) Preferred -

Annual Report 2016 Education Annual Report

ENTERTAINMENT RETURN ON INSIGHT RECREATION ANNUAL REPORT 2016 EDUCATION ANNUAL REPORT 909 WALNUT, SUITE 200, KANSAS CITY, MO 64106 EPRKC.COM 2016 CORPORATE INFORMATION BOARD OF TRUSTEES EXECUTIVE OFFICERS ROBERT J. DRUTEN GREGORY K. SILVERS Chairman of the Board of Trustees President & Chief Executive Officer THOMAS M. BLOCH MARK A. PETERSON Trustee Executive Vice President, Chief Financial Officer & Treasurer BARRETT BRADY MORGAN G. EARNEST II Trustee Senior Vice President & Chief Investment Officer PETER C. BROWN CRAIG L. EVANS Trustee Senior Vice President, General Counsel & Secretary JACK A. NEWMAN, JR. MICHAEL L. HIRONS Trustee Senior Vice President – Strategy and Asset Management ROBIN P. STERNECK THOMAS B. WRIGHT III Trustee Senior Vice President – Human Resources and Administration GREGORY K. SILVERS TONYA L. MATER Trustee Vice President & Chief Accounting Officer President & Chief Executive Officer ANNUAL SHAREHOLDERS STOCK MARKET MEETING INFORMATION The annual meeting of shareholders will be held at The Company’s common shares of 11:00 a.m. (CST), May 31, 2017, in the Company’s beneficial interest are traded on the office at 909 Walnut, Suite 200, Kansas City, MO. New York Stock Exchange under the symbol EPR. INVESTOR TRANSFER AGENT INDEPENDENT RELATIONS AND REGISTRAR AUDITORS For further information regarding Computershare Trust Company, N.A. KPMG LLP EPR Properties, please direct P.O. Box 43078 1000 Walnut Street inquiries to: Providence, RI 02940-3078 Suite 1000 EPR Properties Kansas City, MO 64106 Investor Relations Department 909 Walnut, Suite 200 Kansas City, MO 64106 [email protected] FOR ACCESS TO ADDITIONAL FINANCIAL INFORMATION, VISIT OUR WEBSITE AT WWW.EPRKC.COM LETTER FROM THE PRESIDENT DEAR FELLOW SHAREHOLDER: I’m pleased to report that 2016 was the strongest year in the Company’s history in terms of revenue, earnings and investment spending. -

14195NCJRS.Pdf

If you have issues viewing or accessing this file contact us at NCJRS.gov. !))l' -., •• This microfiche wu produced from documents received for DIRECTORY OF U~ITED STATES PROBATION OFFICERS inclusion in the NCJRS data base. Since NCJRS cannot -exercise Federal Penal and Correctional Institutions control over the physic~ll condition of the documents submitted, • the individual f~ame quality. will .vary. The resolution chart on and this frame may U. S. Disciplinary Barracks • Ii !I - l I • I 1.1 -- .. 14 IIIII 1.25 11111 . 111111,6_ • I June 1974 I • I rvllCROCOPY RESOLUTION TEST CHART I NATIONAL BUREAU OF STANDARDS-J963-A • Microfilminl procedures usd to' create this fic~e comply with the standards set forth in 41CFR 101·11.504 • Points of view or opinions stated in this document are those of the authorl sl and do not represent the official t.O . position or policies of the U.S. Department of Justic~. • 0- U.S. DEPARTMENT OF JUSTICE Probation Division LAW ENFORCEMENT ASSISTANCE 'ADMINISTRATION .:;r Stat(~s Administrative Office of the United Courts e' •• Supreme Court Building NATIONAL CRIMINAL JUSTICE REFERENCE SERVICE • Washington, D. C. 20544 WASHINGTON, D.C. 20531 4 r-~--' . ! I. 0 LD ate . f i i_~m~~i!t J 8/26/75 1 ADNINISTRATIVE OFFICE OF THE UNITED STATES COURTS OFFICES AND ADDRESS AND HOME DISTRIC,!L TELEPHONE Rilllli§ Supreme Court Bui1ding,Washington, D. C. 20544 . ., .,. l' •• •• ALABAMA NORTHERN Rowland F. Kirks Director j William E. Foley Deputy Director [ ~M. Foster Jordan (Chief) Birmingham 35203 822-5811 Joseph F. Spaniol, Jr. Executive Assistant to j the Director John W. -

Building Technology Publications, Supplement 5 : 1980

Building Technology Publications supplement 5: 1980 (Cover photograph courtesy of the Department of Housing and Urban Development.) UknotiAi, tnjuKAv LIBIURT JUL 9 1381 Building Technology Publications Supplement 5: 1980 Steve Webber, Editor Center for Building Technology National Engineering Laboratory National Bureau of Standards Washington, DC 20234 June 1981 Malcolm Baldrige, Secretary S. DEPARTMENT OF COMMERCE, NATIONAL BUREAU OF STANDARDS, Ernest Ambler, Director Library of Congress Catalog Card Number: 78-323849 National Bureau of Standards Special Publication 457-5 Nat. Bur. Stand. (U.S.), Spec. Publ. 457-5, 90 pages (June 1981) CODEN: XNBSAV U.S. GOVERNMENT PRINTING OFFICE WASHINGTON: 1981 For sale by the Superintendent of Documents, U.S. Government Printing Office Washington, DC 20402 - Price $4.50 (Add 25 percent for other than U.S. mailing) Introduction This report presents the National Bureau of Standards' Center for Building Technology (CBT) publications for 1980. It is the fifth supplement to NBS Special Publication 457, Building Technology Publications 1965-1975, and lists CBT documents issued or recorded during the period January 1 to December 31, 1980. It includes titles and abstracts of each NBS publication and each paper published in non-NBS media, key word and author indexes, and general information and instructions on how to order CBT publications. This report communicates the results of CBT research to various technical audiences, as well as to the general public. Publications constitute a major end product to CBT's efforts and, in 1980, appeared in several NBS publication series (Building Science Series, Technical Notes, Special Publications, NBS Interagency Reports, and Grant/ Contract Reports) as well in non-NBS media such as technical and trade publications.