Intelligent Documents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

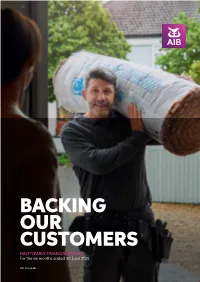

BACKING OUR CUSTOMERS HALF-YEARLY FINANCIAL REPORT for the Six Months Ended 30 June 2021

BACKING OUR CUSTOMERS HALF-YEARLY FINANCIAL REPORT For the six months ended 30 June 2021 AIB Group plc ENSURING A GREENER TOMORROW BY BACKING THOSE BUILDING IT TODAY. AIB is a financial services group. Our main business activities are retail, business and corporate banking, as well as mobile payments and card acquiring. We are committed to supporting the transition to the low-carbon economy and backing sustainable communities. Merchant Services Beekeeper and AIB employee Kevin Power attending to his bees on the roof of our head office in Molesworth St, Dublin. Half-Yearly Financial Report For the six months ended 30 June 2021 01 02 OVERVIEW BUSINESS REVIEW 2 Business performance 16 Operating and financial review 4 Chief Executive’s review 31 Capital 11 Our strategy 12 Highlights 03 04 RISK MANAGEMENT FINANCIAL STATEMENTS 36 Update on risk management and governance 84 Condensed consolidated interim financial statements 37 Credit risk 91 Notes to the condensed consolidated interim 78 Funding and liquidity risk financial statements 82 Interest rate benchmark reform 131 Statement of Directors’ Responsibilities 132 Independent review report to AIB Group plc 133 Forward looking statements This Half-Yearly Financial Report contains forward looking statements with respect to certain of the Group’s plans and its current goals and expectations relating to its future financial condition, performance, results, strategic initiatives and objectives. See page 133. 2 Business Performance AIB Group plc Half-Yearly Financial Report 2021 BUSINESS PERFORMANCE -

The Economics of Mortgage Debt Relief During a Pandemic Edward Gaffney, Fergal Mccann and Johannes Stroebel Vol

The economics of mortgage debt relief during a pandemic Edward Gaffney, Fergal McCann and Johannes Stroebel Vol. 2021, No. 6 The economics of mortgage debt relief during a pandemic Edward Gaffney, Fergal McCann and Johannes Stroebel1 July 2021 Abstract We discuss several features of the economic and institutional environment that are important for determining the design of household debt relief programs in response to aggregate economic shocks. For example, we describe how such program features should depend on the distribution of home equity in the population, the costs of participation to borrowers and lenders, as well as on whether the shocks are temporary or permanent in nature. We analyse the Irish response to the initial COVID-19 shock—which focussed on a broad extension of temporary payment breaks to mortgage borrowers—in light of these factors. Finally, we discuss potential features of adjusted mortgage contracts that may embed some of the benefits of the COVID-19 response in future events without the need for policymaker coordination. 1 Introduction The economic shock resulting from the COVID-19 pandemic has caused exceptional levels of disruption around the world. With more than one year having passed since the onset of the pandemic in Ireland, the depth and uneven nature of the economic shock are now apparent. Although some sectors of the economy are experiencing no effects or even positive demand shocks, in other sectors—particularly in service sectors requiring face-to-face interaction with customers— businesses and their employees have faced on-off disruptions to their incomes, which in some cases risk becoming persistent as the public health situation evolves. -

Faculty of Public Health Medicine Summer Scientific May 26 & 27, 2021

Faculty of Public Health Medicine Summer Scientific May 26 & 27, 2021 Posters Contents Page Submission ID Poster Title 3 Comparing non-Invasive Diabetes Risk Scores for Detecting Patients in Clinical Practice 43 The Burden of Alcohol Related Morbidity and Mortality for 2019 in six Nordic Countries 2 Learning from the experience of Contract Tracers working during the COVID19 Outbreak 35 Cookstove Interventions to reduce exposure to household are pollution in sub-Saharan Africa: A scoping review to inform intervention research 44 Well-being Interventions and Support during Epidemics: Protocol for qualitative longitudinal study of older adults’ experiences during COVID-19 38 DCOVID-19 pandemic impact on employment and mental health in a high risk group-People with Cystic Fibrosis (PWCF) 7 We can Quit2-Results of a pilot randomized controlled trial of a community-based smoking cessation intervention for disadvantaged women in Ireland 6 A breakpoint modelling approach to assess the temporal link between non-pharmaceutical interventions and the incidence of symptomatic COVID-19 in the Republic of Ireland 5 Prognostic modelling of COVID-19 severity in the Republic of Ireland from February to December 29 From evidence to implementation and evaluation: Developing the Self-Harm Assessment and Management for General Hospitals (SAMAGH) Training Programme 41 BreastCheck detected Ductal Carcinoma in Situ, 2008-2020 14 Traumatic Brain Injury Rehabilitation: Preliminary Results from an Irish Study 18 Proposed European contact tracing indicators: does Irish data measure up? 23 An overview of the establishment of a national contact tracing programme in Ireland: A Quality Improvement Approach in a Time of Pandemic 21 A Health Needs Assessment for the Establishment of a Donor Human Milk Bank in the Republic of Ireland 37 Epidemiology of COVID-19 and public health restrictions during the first year of the pandemic in Ireland in 2020/2021 27 An evaluation of a new classification to identify people with Traumatic Brain Injury in routine acute care data. -

Sector Developments & Insights

Sector Developments & Insights December 2020 Classification:Green Contents Introduction Click here Government Schemes Update Click here Retail Click here Agriculture Click here Food & Drink Click here Healthcare Click here Hospitality Click here Technology, Media and Telecoms (TMT) Click here Motor Sector Click here Introduction from June Butler – Head of Sectors – Bank of Ireland [email protected] 087 601 5415 Welcome to the December issue of our Sector Developments and Insights update. Since our last briefing, we have seen strong activity from Bank of Ireland SME customers; with our allocation under the SBCI Future Growth Loan Scheme fully subscribed in late November. We have also seen a steady increase in enquiries in respect of the COVID-19 Credit Guarantee Scheme with increased engagement expected in Q1 2021. With positive news over the last few weeks in relation to a COVID-19 vaccine, and an improved economic outlook, we are optimistic as we enter into 2021. We will continue to engage proactively with our customers and their advisors as they address the impact of COVID-19 and Brexit and look to respond to growth opportunities in their sectors in 2021. Supporting our Customers We continue to organise topical and informative events for our customers. In November we hosted two key note events: • Government scheme webinar – outlining the variations and requirements across different schemes from a customer perspective. • Hospitality webinar – focusing on the challenges and opportunities facing the wider Irish hospitality sector as we move into 2021. We are cognisant of the importance of an online presence for Irish SME’s to meet customer expectations and sustain their business into 2021 and beyond. -

Sláintecare Implementation Strategy & Action Plan 2021 — 2023

Right Care. Right Place. Right Time. Sláintecare Implementation Strategy & Action Plan 2021 — 2023 Sláintecare Implementation Strategy & Action Plan 2021 — 2023 4 Sláintecare Implementation Strategy & Action Plan 2021 — 2023 Contents 01 Introduction 4 02 Sláintecare Reform Programmes 2021 — 2023 8 03 Reform Programme 1: Improving Safe, Timely Access to Care, and Promoting Health & Wellbeing 12 3.1 Strategic Context 13 3.2 Reform Programme 1 — Summary of key projects 15 3.3 Improving Safe, Timely Access to Care and Promoting Health & Wellbeing — Key projects and deliverables 2021 — 2023 20 04 Reform Programme 2: Addressing Health Inequalities — towards Universal Healthcare 36 4.1 Strategic Context 37 4.2 Reform Programme 2 — Summary of key projects 38 4.3 Addressing Health Inequalities – Key projects and deliverables 2021 — 2023 42 05 Enabling programmes 50 5.1 Public and political engagement and empowerment 51 5.2 Staff engagement and empowerment 52 5.3 Patient Safety and Quality Initiatives 52 06 Governance and the Sláintecare Programme Implementation Office 54 07 Reform Programme Implementation 56 7.1 COVID-Context 57 7.2 Sláintecare Programme Implementation Office (SPIO) 57 7.3 Programmatic Implementation Approach 58 08 Strategic Action Plan Development SWOT Analysis and Risk Assessment 60 8.1 SWOT Analysis 61 8.2 Risk Assessment 62 09 Budget 2021 64 10 Monitoring and reporting progress 66 10.1 Oversight reporting 67 10.2 Metrics, Research, and Evaluation of Reforms 67 Appendix 1: Sláintecare Implementation Progress 2020 68 Appendix 2: Learnings from COVID-19 69 Appendix 3: €1.235billion Sláintecare Reform Budget for 2021 70 Sláintecare Implementation Strategy & Action Plan 2021 — 2023 the permanent capacity of our health services and expand the scale and range of services to be provided in the community. -

ECI 2021 Dublin, On

BID PROPOSAL 6th European Congress of Immunology 8th -11th September 2021 Dublin, Ireland 6th European Congress of Immunology Contents 2 Executive Summary 4 Letters of Support 12 International Conferences Held in Dublin 13 Support for the ECI 2021 in Ireland 14 Organising Structure 18 Scientific Programme 21 Immunology Research in Ireland 23 Congress Schedule 24 Conference Organiser 1 26 Access to Dublin 30 The Convention Centre Dublin 36 Finance and Budgets 40 Accommodation 44 Social Events 50 Dublin as a Congress Venue 52 What Dublin Has to Offer 56 Accompanying Persons Programme 58 Conclusions Executive Summary Executive Summary – Why Dublin? Location Attractions » Dublin is a popular, historic capital city, friendly and » Strong local society and tradition of Immunology English-speaking research » Base of premier European low cost airline – frequent, » Wide range of accommodation within walking distance very low cost flights to all major European cities of the venue – all hotel categories, university rooms and budget options, city apartments suitable for groups/ » Daily direct flights to North America and via Middle- families East hubs to Asia » General scenic and cultural attractions of Ireland Congress Venue integrated into the social events and tour options for the congress » National Convention Centre with exclusive use for European Congress of Immunology 2021 Supports 3 » Award-winning, purpose-built venue » Recognition as an “Exceptional Conference” for » City-centre location, 20 minutes from Dublin Airport, government and city -

Ireland's Data Hosting Industry

Ireland’s Data Hosting Industry 2018 Q2 Update “Irish Data Centres, an Industry of Substance” Ireland’s Data Hosting Industry 2018 Q2 Update July 2018 Ireland’s Data Hosting Industry 2018 Q2 Update Foreword It has been an eventful three months for the recognition of the challenges facing the data centre industry in Ireland with the main industry in areas such as renewable energy, focus of attention landing squarely at Apple’s infrastructure and planning. decision not to progress with its €850m data centre investment in Athenry. Ireland’s contribution to the global data centre industry continues to grow also with demand There was much cause for concern that the increasing for Irish companies, skills and impact of the decision would greatly temper expertise to lead projects across the US, Ireland Inc’s ability to attract continued Europe and Asia cementing our position as a investment in data centres but our 2018 global industry player. Quarter 2 report shows momentum continues to grow. We are also seeing potential for the use of data centres to augment any future district From April to June of this year over €1 billion heating systems here in Ireland. While the of new data centre investments were heat off the data centres is low grade it is announced from CyrusOne, Crag Digital, consistent with how centres can add value to Equinix and others. This brings the total already established and functioning district investment expected from the construction of heating systems which have been seen across data centres up until 2021 in Ireland to €9.3 the US and Europe and could make a tangible billion. -

For the Three Months Ended March 31, 2020

ADVENTUS MINING CORPORATION MANAGEMENT’S DISCUSSION & ANALYSIS FOR THE THREE MONTHS ENDED MARCH 31, 2020 TABLE OF CONTENTS Cautionary Note Regarding Forward-Looking Statements ............................................................................................ 1 Business Overview ......................................................................................................................................................... 3 Corporate Highlights ...................................................................................................................................................... 3 South32 Earn-In ...................................................................................................................................................... 4 Exploration Outlook in Ecuador ..................................................................................................................................... 4 Exploration and evaluation assets ................................................................................................................................. 5 Ecuadorian Projects ....................................................................................................................................................... 7 Curipamba .............................................................................................................................................................. 7 Exploration Alliance – Pijilí project ........................................................................................................................ -

Document Register - AGM of the National Council 2018

Document Register - AGM of the National Council 2018 Scouting Ireland, National Office, Larch Hill, Dublin 16 T 01 4956300 / F 01 4956300 E [email protected] www.scouts.ie Meeting Number: NC 18001: First Mailing No: TITLE: 0 Document Register 1 First Notice of National Council 2 Annual Report 2017 - Click HERE to download from my.scouts.ie 3 Draft Minutes of the AGM of the National Council 2017 4 Status report on Motions Passed at National Council 2017 5 Proposal Forms 6 Nomination Form 7 Nomination Acceptance Form 8 Procedure for dealing with motion to National Council 9 Brief Guide to Motions 10 Membership Figures - Click HERE to download from my.scouts.ie 11 Audited Accounts of Scouting Ireland Services CLG 12 Constitution 13 Rules 14 SID 86 11 National Council Elections Policy Ref: L03 /2018 - National Council AGM 2018 First Notice Circulation by Email/SMS/my.scouts.ie 16th February 2018 Dear Scouter, In accordance with Rule 113, I enclose details for the forthcoming meeting of the National Council. This notice is issued to members listed below. All information regarDing the first mailing announcement is available to DownloaD anD view on www.scouts.ie. Log-on, go to ‘Scouter’ then ‘National Stuff’ then ‘National Council 2018’. Group LeaDers should bring this notice to the attention of their Group Councils and in particular to the four delegates that will be nominated by the Group Council to attend National Council. County Commissioners & County Secretaries should bring this notice to the attention of their County Boards and in particular to the County Chairperson, County Treasurer & the County Youth Fora. -

Ucd Centre for Economic Research Working Paper Series

UCD CENTRE FOR ECONOMIC RESEARCH WORKING PAPER SERIES 2021 A Framework to Measure Regional Disparities in Battery Electric Vehicle Diffusion in Ireland Sanghamitra Chattopadhyay Mukherjee, University College Dublin WP21/19 August 2021 UCD SCHOOL OF ECONOMICS UNIVERSITY COLLEGE DUBLIN BELFIELD DUBLIN 4 A framework to measure regional disparities in battery electric vehicle diffusion in Ireland Sanghamitra Chattopadhyay Mukherjee UCD Energy Institute & UCD School of Economics, University College Dublin, Ireland Abstract: This work studies the role of socio-economic and geospatial factors in shaping battery electric vehicle adoption for the case study of Ireland. It provides new insights on the level and timing of likely adoption at scale using a Bass diffusion model combined with a spatial model. The Bass model demonstrates that a country like Ireland may experience peak sales between 2025 and 2030 given current trends, reaching overall uptake levels that are not commensurate with current policy goals, whilst also potentially creating gulfs in regional take-up. The key conclusion from the spatial analysis is that location matters for uptake, through various channels that help or hinder adoption such as resources, information, and policy. Additional investment in public charging infrastructure facilities may also be needed as gaps in coverage exist, especially in rural areas to the West and South-West of the country. Although Ireland enjoys good network coverage overall, this study suggests that more charge points may be needed in some counties and Dublin city and suburbia where the number of charge points is currently disproportionate to a minimum network coverage comparable with the land area, population size, number of private vehicle owners, and travel behaviour. -

Public Health Measures and Strategies to Limit the Spread of COVID-19 Health Information and Quality Authority

Public health measures and strategies to limit the spread of COVID-19 Health Information and Quality Authority Public health measures and strategies to limit the spread of COVID-19: an international review Update submitted to NPHET: 16 March 2021 Published: 22 March 2021 Page 1 of 130 Public health measures and strategies to limit the spread of COVID-19 Health Information and Quality Authority Version history Version Date Specific updates V1.0 24 November 2020 Provided to the National Public Health Emergency Team (NPHET) for information. V2.0 1 December 2020 Updated and provided to NPHET for information. Included an additional table (Table 2) to summarise the recent changes in current public health measures. Updated the epidemiological data to the latest available data from the European Centre for Disease Prevention and Control (ECDC). Included information on the proposed plans for mass testing in Austria. V3.0 8 December 2020 Updated and provided to NPHET for information. Updated the epidemiological data to the latest available data from the European Centre for Disease Prevention and Control (ECDC). V4.0 15 December 2020 Updated and provided to NPHET for information. Updated the epidemiological data to the latest available data from the European Centre for Disease Prevention and Control (ECDC). V5.0 23 December 2020 Updated and provided to NPHET for information. Reduced version of report created with updated public health measures on education only. V6.0 06 January 2021 Updated and provided to NPHET for information. Page 2 of 130 Public health measures and strategies to limit the spread of COVID-19 Health Information and Quality Authority . -

Monitoring Decent Work in Ireland Report

RESEARCH SERIES MonitoringRESEARCH SERIES Decent Work in IrelandMonitoring Decent FrancesWork McGinnity, in Ireland HelenFrances Russell, McGinnity, Helen Russell, Ivan PrivalkoIvan Privalko & & Shannen Enright Shannen Enright Monitoring Decent Work in Ireland Frances McGinnity, Helen Russell, Ivan Privalko & Shannen Enright Available to download from www.esri.ie and www.ihrec.ie © 2021. Copyright is held jointly by the Economic and Social Research Institute and the Irish Human Rights and Equality Commission. Irish Human Rights and Equality Commission, 16–22 Green Street, Dublin 7. The Economic and Social Research Institute, Whitaker Square, Sir John Rogerson’s Quay, Dublin 2 ISBN: 978-1-913492-05-2 https://doi.org/10.26504/bkmnext414 This Open Access work is licensed under a Creative Commons Attribution 4.0 International License (https://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly credited. Monitoring Decent Work in Ireland Frances McGinnity, Helen Russell, Ivan Privalko & Shannen Enright Available to download from www.esri.ie and www.ihrec.ie © 2021. Copyright is held jointly by the Economic and Social Research Institute and the Irish Human Rights and Equality Commission. Irish Human Rights and Equality Commission, 16–22 Green Street, Dublin 7. The Economic and Social Research Institute, Whitaker Square, Sir John Rogerson’s Quay, Dublin 2 ISBN: 978-1-913492-05-2 https://doi.org/10.26504/bkmnext413 This Open Access work is licensed under a Creative Commons Attribution 4.0 International License (https://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly credited.