Capitacommercial Trust Singapore’S First Listed Commercial REIT

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Strata Management's Portfolio

Knight Frank Property Asset Management – Strata Management’s Portfolio As of 1 May 2021, Knight Frank Property Asset Management (Strata Management) manages the following projects: Residential Properties No MCST Estate Name No. of Units 1 2761 38 Draycott Drive 30 2 2201 7 Claymore 76 3 4480 8M Residences 68 4 2171 9 Holland Hill 24 5 2991 Amaninda 70 6 TOP Amber 45 139 7 3548 Angullia Park Residences @ Orchard 46 8 3583 Ardmore II 118 9 2645 Ardmore Park 330 10 4203 Ardmore Three 84 11 2532 Aspen Heights 609 12 4693 Botanique at Bartley 797 13 4192 Boulevard Vue 28 14 3007 Cairnhill Crest 248 15 1862 Casa Esperanza 90 16 2414 Chestervale 396 17 4064 Coralis 127 18 3316 D'Lotus 83 19 4596 d'Nest 912 20 3174 De Royale 204 21 2653 Dunman Place 69 22 1075 Eastern Lagoon II 220 23 4705 Elite Residences 8 24 3970 Floridian 336 25 TOP Forest Woods 519 26 2549 Glendale Park 448 27 3728 Grange Infinite 68 28 4649 Greenwood Mews 62 29 4638 Highline Residences 500 30 3555 Hillcrest Villa 163 31 4737 Hundred Palms Residences 531 32 3559 Illoura 30 33 4547 J Gateway 738 34 TOP Kandis Residence 130 35 4701 Lake Grande 710 Knight Frank Property Asset Management Pte Ltd 160 Paya Lebar Road #05-05 Orion@Paya Lebar Singapore 409022 Tel: +65 6848 5678 Fax: +65 6848 5600 Reg.No: 200007671Z CEA Licence No: L3009602I KnightFrank.com.sg Other Offices: Knight Frank Pte Ltd 10 Collyer Quay #08-01 Ocean Financial Centre Singapore 049315 KF Property Network Pte Ltd 10 Collyer Quay #08-01 Ocean Financial Centre Singapore 049315 36 4556 Lakeville 699 37 3670 Lumiere -

POISED for a GRADUAL RECOVERY Senior Associate Director | Research | Singapore +65 6531 8567 [email protected]

COLLIERS QUARTERLY OFFICE | SINGAPORE | RESEARCH | Q4 2020 | 14 JANUARY 2021 Shirley Wong POISED FOR A GRADUAL RECOVERY Senior Associate Director | Research | Singapore +65 6531 8567 [email protected] Tricia Song 2021–25 Director and Head | Research | Insights & Q4 2020 Full Year 2021 Annual Average Singapore > CBD Grade A office showed resilience with +65 6531 8536 Recommendations [email protected] 336,900 sq ft net absorption in 2020 despite CBD Grade A rents declined 2.1% GDP contraction of 5.8%, driven by previous QOQ in Q4 2020 and 5.4%* for Demand flexible workspace commitments. In 2021, -59,600 sq ft 787,900 sq ft 894,000 sq ft the full year to SGD9.57 (USD7.24) we expect technology to drive demand. per sq foot, on weak global > We expect relatively muted CBD Grade A economic conditions. We forecast supply in 2021-2022, with annual expansion rents to grow 5.5% by the end of averaging 2.6% of stock versus 4.7% for the 0 sq ft 783,900 sq ft 883,000 sq ft 2021, on an eventual economic Supply last five years. 2023 should see higher supply rebound and benign supply. at 4.5% of stock. We forecast new demand in 2021 Annual Average to be driven by the technology QOQ / YOY / Growth 2021–25 / End Q4 End 2021 End 2025 sector. Meanwhile, Q4 2020 CBD > CBD Grade A rents declined 2.1% in Q4 2020 Grade A vacancy of 5.2% (+1.8pp 1.0pp-2.1%* +3.7% and 5.4%* for the full year to SGD9.57 5.5% YOY) could tighten over the next (USD7.24) per sq foot. -

A Review of the Singapore Office Market

Singapore Q1/Q2 2019 Published 1st March 2019 Singapore | Hong Kong The Office A review of the Singapore office market Index P2 Building Rental Table (Islandwide) P3 Leasing Options – New Downtown & Economy Range P4 Demand – who is moving where P5 Featured New Development – 9 Penang Road P6 Special Feature – Co-working space P7 Leasing Options – Raffles Place & Tanjong Pagar P8 Supply / Rentals / Forecast Corporate Locations (S) Pte Ltd License No. L3010044A Marina One T +65 6320 8355 / [email protected] / www.corporatelocations.com.sg RENTAL GUIDE 1st March 2019 Summary of Asking Rates Raffles Place / New Downtown Bangkok Bank Building TBA City Hall / Marina Centre / Beach Rd Chinatown / River Valley Road BEA Building $7.50 18 Robinson $12.00 Capital Tower $10.00 11 Beach Road Full Central Mall $7.00 20 Collyer Quay $11.00-$13.00 Cecil Court $5.80 30 Hill Street Full CES Centre $5.50+ 55 Market Street $7.00 China Square Central $8.50 Beach Centre $7.80 Chinatown Point $6.50 6 Battery Road $14.00 City House $7.80+ Bugis Junction Towers $7.80 Great World City $7.00 Asia Square T1 & T2 $14.00 Far East Finance Bldg $7.00 Centennial Tower $14.80 Kings Centre $7.00 Bank of China Building Full Far Eastern Bank Bildg Full Duo Tower $10.50 The Central $9.80 Bank of Singapore Centre $9.50 GB Building $6.00+ Funan $9.00 UE Square $8.00 Bharat Building $6.50 Keck Seng Tower $6.00 Manulife Centre $10.00+ Valley Point $7.00 CapitaGreen $13.50 Manulife Tower $9.50 Millenia Tower $14.80 Capital Square Full MYP Plaza $7.00 Odeon Tower -

Justco Unveils Its First Smart Centre, Partners with the World's First On-Demand Workspace Platform, Switch, and Spatial Analy

JustCo Unveils its First Smart Centre, Partners with the World’s First On-demand Workspace Platform, Switch, and Spatial Analytics Technology Company, SixSense at The Centrepoint Spanning three levels, members at JustCo at The Centrepoint will enjoy smart workspace technologies such as facial recognition, card-free access with Bluetooth capability, on- demand space usage, social distance detection technology and a robot barista café [For immediate release] Singapore, 19 NOVEMBER 2020 JustCo, the leading co-working company in Asia Pacific, continues to revolutionize the future of work. This time, it has notched up a holistic work solution by launching its first technology- enabled workspace. With support from one of its strategic partners, Frasers Property, JustCo has introduced its total work solutions platform at The Centrepoint in Singapore’s iconic retail district, Orchard Road. JustCo at The Centrepoint is set to inject vibrancy and fun into the neighbourhood, while making work better and smarter for businesses and individuals in the heart of town. Piloting at The Centrepoint, JustCo has partnered with workspace on-demand platform Switch to offer users fuss-free access to conducive workspaces as and when they need, and pay for exactly what they use. In addition, this centre will feature other workspace technologies such as facial recognition card-free access via Bluetooth capability and a fully-automated, in-house café by day and cocktail bar by night. Powered by robotics and artificial intelligence, RATIO offers custom-crafted coffee and cocktails, made to a high level of precision. As an added safety feature, the facial recognition turnstiles are designed to detect if members are wearing their face masks, in order to permit them entry. -

Annual Report 2019 01

UOL GROUP LIMITED Contents About Us 01 Building On Our Strengths 02 Sustaining Long-Term Value 04 Extending Our Horizons 06 Financial Highlights 08 Two-Year Financial Highlights 10 Corporate Information 11 Highlights 12 Chairman’s Statement 14 Board Of Directors 16 Key Management Executives 22 Listing Of Senior Management 23 Awards & Accolades 24 Operation Highlights 26 Corporate Governance Report 40 Investor Relations 60 Sustainability 62 Geographical Presence 66 Property Summary 68 Simplified Group Financial Position76 Five-Year Financial Summary 77 Segmental Performance Analysis 79 Value-Added Statement 81 Alex Residences S20009 size:W210mm x H297mm 1st Page 01 ANNUAL REPORT 2019 01 About Us UOL Group Limited (UOL) is one of Singapore’s leading UOL, through hotel subsidiary Pan Pacific Hotels public-listed property companies with total assets of Group Limited (PPHG), owns three acclaimed brands about $20 billion. We have a diversied portfolio of namely “Pan Pacic”, PARKROYAL COLLECTION and development and investment properties, hotels and PARKROYAL. PPHG currently owns and/or manages serviced suites in Asia, Oceania, Europe and North over 30 hotels in Asia, Oceania and North America America. with over 10,000 rooms. Our Singapore-listed property subsidiary, United Industrial Corporation Limited (UIC), With a track record of over 50 years, UOL strongly owns an extensive portfolio of prime commercial assets believes in delivering product excellence and quality and hotels in Singapore. service in all its business ventures. Our unwavering commitment to architectural and quality excellence is UOL values and recognises our people as the leading reected in all our developments, winning us prestigious asset. -

CAPITALAND COMMERCIAL TRUST Capitaland Group Corporate Day, Bangkok 14 August 2019 Important Notice

CAPITALAND COMMERCIAL TRUST CapitaLand Group Corporate Day, Bangkok 14 August 2019 Important Notice This presentation shall be read in conjunction with CCT’s 2Q 2019 Unaudited Financial Statement Announcement. The past performance of CCT is not indicative of the future performance of CCT. Similarly, the past performance of CapitaLand Commercial Trust Management Limited, the manager of CCT is not indicative of the future performance of the Manager. The value of units in CCT (CCT Units) and the income derived from them may fall as well as rise. The CCT Units are not obligations of, deposits in, or guaranteed by, the CCT Manager. An investment in the CCT Units is subject to investment risks, including the possible loss of the principal amount invested. Investors have no right to request that the CCT Manager redeem or purchase their CCT Units while the CCT Units are listed. It is intended that holders of the CCT Units may only deal in their CCT Units through trading on Singapore Exchange Securities Trading Limited (SGX-ST). Listing of the CCT Units on the SGX-ST does not guarantee a liquid market for the CCT Units. This presentation may contain forward-looking statements that involve assumptions, risks and uncertainties. Actual future performance, outcomes and results may differ materially from those expressed in forward-looking statements as a result of a number of risks, uncertainties and assumptions. Representative examples of these factors include (without limitation) general industry and economic conditions, interest rate trends, cost of capital and capital availability, competition from other developments or companies, shifts in expected levels of occupancy rate, property rental income, charge out collections, changes in operating expenses (including employee wages, benefits and training costs), governmental and public policy changes and the continued availability of financing in the amounts and the terms necessary to support future business. -

Independent Market Overview by CBRE Pte Ltd

45 Annual Report 2017/18 Independent Market Overview By CBRE Pte Ltd 1. THE SINGAPORE ECONOMY Chart 1: Singapore GDP Growth Rate at 2010 Prices 1.1 Economic Overview 6.0% According to the Ministry of Trade & Industry (“MTI”), 5.1% Singapore’s economy expanded by 3.6% in 2017, an 5.0% 3.9% 3.6% improvement from the 2.4% growth achieved in 2016. Growth 4.0% was driven primarily by robust expansion in the manufacturing 2.4% 3.0% 2.2% sector, which grew by 10.1%. It was led by the precision engineering and electronics clusters amidst a decline in output 2.0% within the biomedical manufacturing, transport engineering 1.0% and general manufacturing clusters. The services sector also saw an overall expansion of 2.8% in 2017 which was supported 2013 2014 2015 2016 2017 by the wholesale & retail trade, transportation & storage and Sources: MTI and CBRE finance & insurance sectors. Conversely, the construction sector 2. THE OFFICE MARKET contracted by 8.4% on the back of weaknesses in private sector 2.1 Existing Office Supply construction activities. The total office stock in Singapore stood at 59.5 million sf in 1Q 2018, representing a 3.9% year-on-year increase. This is According to the MAS, headline inflation for 2017 came in at due largely to the completion of new developments such as 0.6%. Meanwhile, core inflation averaged 1.5% for the year. MAS UIC Building (277,540 sf) and Marina One East & West Tower expects core inflation to stay in the range of 1-2% in 2018. -

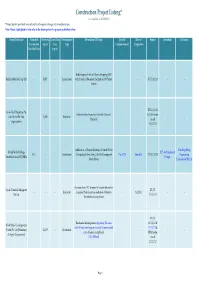

Construction Project Listing* (Last Updated on 20/12/2013) *Project Details Provided May Subject to Subsequent Changes by Owner/Developer

Construction Project Listing* (Last Updated on 20/12/2013) *Project details provided may subject to subsequent changes by owner/developer. Note: Words highlighted in blue refer to the latest updates for projects published before. Owner/Developer Estimated Site Area Gross Floor Development Description Of Project Date Of Date of Source Consultant Contractor Construction (sq m) Area Type Commencement Completion Cost ($million) (sq m) Redevelopment into a 6 Storey Shopping Mall Raffles Medical Group Ltd - 5,827 - Institutional with 2 levels of Basement Carpark at 100 Taman - - ST 17/12/13 - - Warna BT 11/12/13 Grow-Tech Properties Pte Industrial development at Gambas Crescent & URA tender Ltd (Part of Far East - 14,302 - Industrial -- -- (Parcel 3) result Organization) 13/12/13 Addition of a 5 Storey Building to United World Kim Seng Heng United World College BLT Architecture & 42.5 - - Institutional College South East Asia (UWCSEA) campus at Dec-2013 Aug-2015 BT 13/12/13 Engineering South East Asia (UWCSEA) Design Dover Road Construction Pte Ltd Erection of an LPG Terminal to import alternative Vopak Terminals Singapore BT/ST - - - Industrial Liquefied Petroleum Gas feedstock at Banyan - 1Q 2016 -- Pte Ltd 11/12/13 Terminal in Jurong Island BT/ST Residential development comprising 281 units 16/11/12 & World Class Developments with 24 hour concierge service and 18 commercial 11/12/13 & (North) Pte Ltd [Subsidiary - 10,170 - Residential -- -- units at Jalan Jurong Kechil URA tender of Aspial Corporation] (The Hillford) result 22/11/12 Page 1 Construction Project Listing* (Last Updated on 20/12/2013) *Project details provided may subject to subsequent changes by owner/developer. -

Presentation Slides

CapitaLand Commercial Trust Singapore’s First Commercial REIT First Quarter 2016 Financial Results Friday, 15 April 2016 1 Important Notice This presentation shall be read in conjunction with CCT’s 1Q 2016 Unaudited Financial Statement Announcement. The past performance of CCT is not indicative of the future performance of CCT. Similarly, the past performance of CapitaLand Commercial Trust Management Limited, the manager of CCT is not indicative of the future performance of the Manager. The value of units in CCT (CCT Units) and the income derived from them may fall as well as rise. The CCT Units are not obligations of, deposits in, or guaranteed by, the CCT Manager. An investment in the CCT Units is subject to investment risks, including the possible loss of the principal amount invested. Investors have no right to request that the CCT Manager redeem or purchase their CCT Units while the CCT Units are listed. It is intended that holders of the CCT Units may only deal in their CCT Units through trading on Singapore Exchange Securities Trading Limited (SGX-ST). Listing of the CCT Units on the SGX-ST does not guarantee a liquid market for the CCT Units. This presentation may contain forward-looking statements that involve assumptions, risks and uncertainties. Actual future performance, outcomes and results may differ materially from those expressed in forward- looking statements as a result of a number of risks, uncertainties and assumptions. Representative examples of these factors include (without limitation) general industry and economic conditions, interest rate trends, cost of capital and capital availability, competition from other developments or companies, shifts in expected levels of occupancy rate, property rental income, charge out collections, changes in operating expenses (including employee wages, benefits and training costs), governmental and public policy changes and the continued availability of financing in the amounts and the terms necessary to support future business. -

Capitaland Commercial Trust

CAPITALAND COMMERCIAL TRUST FY 2019 Financial Results – Additional Information 22 January 2020 FY 2019 Gross Revenue higher by 4.7% YoY Higher gross revenue mainly from Gallileo, Main Airport Center, Asia Square Tower 2 and 21 Collyer Quay S$ million FY 2018 FY 2019 110.3 105.0 91.1 91.4 71.4 73.1 68.9 67.2 Divested on 29 Aug 2018 25.3 27.2 20.4 12.8 12.5 11.8 10.1 7.7 - - (1) (2) Asia Square CapitaGreen Capital Tower Six Battery Road 21 Collyer Quay Gallileo Main Airport Bugis Village Twenty Anson Tower 2 Center (MAC) (1) Notes: (1) CCT owns 94.9% of Gallileo and MAC which contributed revenue and income from 19 June 2018 and 18 September 2019 respectively. The reported figure is on 100.0% basis. (2) Bugis Village returned to the State on 1 April 2019. 2 CapitaLand Commercial Trust Presentation Jan 2020 FY 2019 Net Property Income higher by 2.1% YoY Net property income lifted mainly by Asia Square Tower 2, Gallileo, 21 Collyer Quay S$ million FY 2018 FY 2019 83.4 80.0 73.3 72.0 54.8 56.3 55.1 52.8 Divested on 29 Aug 2018 24.7 22.5 20.3 12.3 9.3 9.4 5.0 4.5 - - Asia Square CapitaGreen Capital Tower Six Battery Road 21 Collyer Quay Gallileo (1) Main Airport Bugis Village(2) Twenty Anson Tower 2 Center (MAC)(1) Notes: (1) CCT owns 94.9% of Gallileo and MAC which contributed revenue and income from 19 June 2018 and 18 September 2019 respectively. -

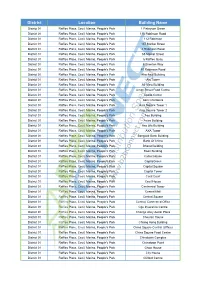

District Location Building Name

District Location Building Name District 01 Raffles Place, Cecil, Marina, People's Park 1 Finlayson Green District 01 Raffles Place, Cecil, Marina, People's Park 110 Robinson Road District 01 Raffles Place, Cecil, Marina, People's Park 112 Robinson District 01 Raffles Place, Cecil, Marina, People's Park 137 Market Street District 01 Raffles Place, Cecil, Marina, People's Park 4 Robinson Road District 01 Raffles Place, Cecil, Marina, People's Park 55 Market Street District 01 Raffles Place, Cecil, Marina, People's Park 6 Raffles Quay District 01 Raffles Place, Cecil, Marina, People's Park 6 Shenton Way District 01 Raffles Place, Cecil, Marina, People's Park 80 Robinson Road District 01 Raffles Place, Cecil, Marina, People's Park Afro-Asia Building District 01 Raffles Place, Cecil, Marina, People's Park Aia Tower District 01 Raffles Place, Cecil, Marina, People's Park Air View Building District 01 Raffles Place, Cecil, Marina, People's Park Amoy Street Food Centre District 01 Raffles Place, Cecil, Marina, People's Park Apollo Center District 01 Raffles Place, Cecil, Marina, People's Park Asia Chambers District 01 Raffles Place, Cecil, Marina, People's Park Asia Square Tower 1 District 01 Raffles Place, Cecil, Marina, People's Park Asia Square Tower 2 District 01 Raffles Place, Cecil, Marina, People's Park Aso Building District 01 Raffles Place, Cecil, Marina, People's Park Aviva Building District 01 Raffles Place, Cecil, Marina, People's Park Axa Life Building District 01 Raffles Place, Cecil, Marina, People's Park AXA Tower District 01 -

1 CAPITALAND COMMERCIAL TRUST ANNOUNCEMENT ASSET VALUATION Pursuant to Rule 703 of the Singapore Exchange Securities Trading

CAPITALAND COMMERCIAL TRUST (Constituted in the Republic of Singapore pursuant to a Trust Deed dated 6 February 2004 (as amended)) ANNOUNCEMENT ASSET VALUATION Pursuant to Rule 703 of the Singapore Exchange Securities Trading Limited (“ SGX-ST ”) Listing Manual, CapitaLand Commercial Trust Management Limited (the “Manager ”), as manager of CapitaLand Commercial Trust (“ CCT ”), wishes to announce that independent valuations as at 30 June 2020, have been obtained for the properties owned/ jointly owned by CCT. Notwithstanding the announcement by the Manager on 26 February 2020 that it will conduct property valuations on an annual basis, in light of the proposed merger between CCT and CapitaLand Mall Trust (“ CMT ”) which was announced on 22 January 2020 (the “ Merger ”), the Manager had commissioned the valuations as part of the process to update certain information required for purposes of the Merger. The value of CCT’s Singapore properties comprising Asia Square Tower 2, CapitaGreen, Capital Tower, Six Battery Road and 21 Collyer Quay was S$7,020.5 million in aggregate as at 30 June 2020. This figure of S$7,020.5 million excludes CCT’s 60.0% interest in Raffles City Singapore held through RCS Trust, 50.0% interest in One George Street held through One George Street LLP and 45.0% interest in CapitaSpring held through Glory Office Trust and Glory SR Trust. The value of Raffles City Singapore as at 30 June 2020 was S$3,266.0 million. CCT’s 60.0% interest in Raffles City Singapore held through RCS Trust was S$1,959.6 million. The value of One George Street was S$1,122.0 million as at 30 June 2020.