IMAX Corporation (Exact Name of Registrant As Specified in Its Charter)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Inpark Magazine – Animax Acquired by Singapore's Cityneon Holdings

11/03/2020 InPark Magazine – Animax acquired by Singapore’s Cityneon Holdings LATEST Two Bit Circus first venue to offer unteathered VR experience Oddball outside New Zealand New waterpark, festivals, and events highlight 2020 season at California’s Great Amer LATEST NEWS ONLINE ISSUES WORLD MARKETS SUBSCRIBE ADVERTISE ABOUT IPM BOOKS FOLLO Animax acquired by Singapore’s Cityneon Holdings Jan 13, 2020 Joe Kleiman Business, Headlines, News, Technology & Media Comments Off SINGAPORE (January 13, 2019) — Cityneon Holdings announced today that it has completed the acquisition of Animax Designs, Inc. Cityneon Holdings is an experience entertainment company specializing in transforming customer and brand experiences, encompassing 4 independent yet integrated business divisions – Interior Architecture, Experiential Environments, Events and Exhibitions. The group also comprises Victory Hill Exhibitions, which focuses on delivering engaging educational and interactive “ready-to-showcase” exhibitions, designed to wow the senses. Animax Designs, Inc., which is based in Nashville, Tennessee in the US, was founded by Chuck Fawcett in 1989 and just celebrated its 30th year anniversary in the creation of cutting-edge animatronic and interactive Categorie characters, animated costumes, and puppets. With a workforce of 150 highly‐skilled employees, Animax serves some of the largest operators in the world in themed entertainment, live attractions, and location‐ IPM Interv based entertainment. Its rich history, years of innovation and use of leading-edge -

Animax Svod - Uk

ANIMAX SVOD - UK DRAFT - CONFIDENTIAL DRAFT - CONFIDENTIAL ANIMAX DNA POSITIONING: ANIMAX is the destination for the ultimate anime experience ATTRIBUTES: ... Loud ... Colourful ... Unconventional ... Authentic ... Cheeky ANIMAX is a digital platform for the best in anime DRAFT - CONFIDENTIAL ANIMAX Target Audience Primary: 18 - 29 years, Secondary: 15 - 45 years Real time, multi-media consumption lies at the core of our viewers’ lifestyle. ANIMAX VIEWERS • Early adopters with relatively high discretionary income • Pop culture fanatics in search of what’s new…now • Multi-tasking consumers of cross-platform content • Aware of global trends and engaged in global issues • They want to watch TV on-line and on their mobile phones • They’re gamers and they own either a Play station or X-Box DRAFT - CONFIDENTIAL What you get with ANIMAX ANIMAX features hit anime series, movies and exclusive material such as behind-the-scenes interviews and music footage. ANIMAX provides…. • Unlimited access to content • Subscription = ad free • Available on IOS, Android, and PS3 from launch, other connected devices in phase 2 • Simulcast – latest shows from Japan ANIMAX strives to offer its devoted fan base dedicated content tailored to a dedicated platform. World-class production values and first look, high-profile titles. Anytime. Anywhere. On Any Device. + + DRAFT - CONFIDENTIAL ANIMAX Program Strategy ANIMAX aims to bring the whole world of anime to a much wider public with programming that includes: • Box Sets – a catalog of complete full seasons • Movies -

The Significance of Anime As a Novel Animation Form, Referencing Selected Works by Hayao Miyazaki, Satoshi Kon and Mamoru Oshii

The significance of anime as a novel animation form, referencing selected works by Hayao Miyazaki, Satoshi Kon and Mamoru Oshii Ywain Tomos submitted for the degree of Doctor of Philosophy Aberystwyth University Department of Theatre, Film and Television Studies, September 2013 DECLARATION This work has not previously been accepted in substance for any degree and is not being concurrently submitted in candidature for any degree. Signed………………………………………………………(candidate) Date …………………………………………………. STATEMENT 1 This dissertation is the result of my own independent work/investigation, except where otherwise stated. Other sources are acknowledged explicit references. A bibliography is appended. Signed………………………………………………………(candidate) Date …………………………………………………. STATEMENT 2 I hereby give consent for my dissertation, if accepted, to be available for photocopying and for inter-library loan, and for the title and summary to be made available to outside organisations. Signed………………………………………………………(candidate) Date …………………………………………………. 2 Acknowledgements I would to take this opportunity to sincerely thank my supervisors, Elin Haf Gruffydd Jones and Dr Dafydd Sills-Jones for all their help and support during this research study. Thanks are also due to my colleagues in the Department of Theatre, Film and Television Studies, Aberystwyth University for their friendship during my time at Aberystwyth. I would also like to thank Prof Josephine Berndt and Dr Sheuo Gan, Kyoto Seiko University, Kyoto for their valuable insights during my visit in 2011. In addition, I would like to express my thanks to the Coleg Cenedlaethol for the scholarship and the opportunity to develop research skills in the Welsh language. Finally I would like to thank my wife Tomoko for her support, patience and tolerance over the last four years – diolch o’r galon Tomoko, ありがとう 智子. -

Condensed 8-27-16 Delegate List for Website

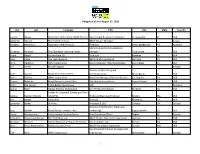

Delegate List as of August 27, 2016 First Last Company Title City State Country Lauren Alleva World Golf Hall of Fame IMAX Theater Marketing & Promotions Manager St. Augustine FL USA Abdullah Alshtail The Scientific Center IMAX Theater Manager Kuwait Stephen Amezdroz December Media Pty Ltd Producer South Melbourne VIC Australia Marketing and Communications Christina Amrhein The Challenger Learning Center Manager Tallahassee FL USA Violet Angell Golden Gate 3D Producer Berkeley CA USA John Angle The Tech Museum IMAX Chief Projectionist San Jose CA USA Chris Appleton IMAX Corporation Senior Manager, Aftermarket Sales Los Angeles CA USA Tim Archer Masters Digital Canada Director of Marketing and Katie Baasen McWane Science Center Communications Birmingham AL USA Doris Babiera IMAX Corporation Associate Manager, Film Distribution Los Angeles CA USA Shauna Badheka MacGillivray Freeman Films Distribution Coordinator Laguna Beach CA USA Peter Bak-Larsen Tycho Brahe Planetarium CEO Denmark Janine Baker nWave Pictures Distribution Snr VP Film Distribution Burbank CA USA Center for Science & Society and Twin JoAnna Baldwin Mallory Cities PBS Producer/Executive Producer Boston MA USA Jim Barath Sonics ESD Principal Monterey CA USA Jonathan Barker SK Films President & CEO Toronto ON Canada Director of Distribution Media and Chip Bartlett MacGillivray Freeman Films Technology Laguna Beach CA USA Sandy Baumgartner Saskatchewan Science Centre Chief Executive Officer Regina SK Canada Samantha Belpasso-Robinson The Tech Museum IMAX Theater Operations Supervisor San Jose CA USA Amanda Bennett Denver Museum of Nature & Science Marketing Director Denver CO USA Jenn Bentz Borcherding Pacific Science Center IMAX Projectionist Supervisor Seattle WA USA Vice President Product Development Tod Beric IMAX Corporation Engineering Mississauga ON Canada 1 Delegate List as of August 27, 2016 First Last Company Title City State Country Jonathan Bird Oceanic Research Group, Inc. -

Graeme Ferguson

Ontario Place - home of IMAX Ferguson: It's a film about what it's hke film in Cinesphere? to join the circus, to be a Ferguson: Not for the pubhc. We'll Graeme performer in the circus. The film is pro probably be doing our pre duced and directed by my partner views there. It's the only existing theatre Roman Kroitor, and will probably be Ferguson called "This Way to the Big Show." where we can look at an IMAX film. Ques: Will IMAX be part of all world Ques: Did he use actors in the fUm? — by Shelby M. Gregory and Phyllis Expos to come? Wilson. Ferguson: No, he used only circus per Ferguson: There is an Expo taking place sonnel. Roman took the cam Graeme Ferguson is the Director- in Spokane in 1974, and the era right into the circus, and filmed Cameraman-Producer of "North of United States PaviUon will feature an during actual performances. It was very Superior". He is also president of Multi- IMAX theatre. Screen Corporation Limited, located in difficult because they could only get Gait-Cambridge, Ontario (developers of about two or three shots in any one Ques: Are they paying for the produc IMAX). performance. tion of a film? Ques: Was this filmed with the standard Ferguson: Yes, Paramount Pictures is Ques: What have you been doing since IMAX camera? producing, and Roman and I North of Superior? are involved. Ferguson: Yes, John Spotton was the Ferguson: We're just finishing a film for cameraman. Eldon Rathburn, Ques: Is it a feature film? Ringhng Brothers and Bar- who did the music for Labyrinth, is num and Bailey. -

9. IMAX Technology and the Tourist Gaze

Charles R. Acland IMAX TECHNOLOGY AND THE TOURIST GAZE Abstract IMAX grew out of the large and multiple screen lm experiments pro- duced for Expo ’67 in Montréal. Since then, it has become the most suc- cessful large format cinema technology.IMAX is a multiple articulation of technological system, corporate entity and cinema practice. This article shows how IMAX is reintroducing a technologically mediated form of ‘tourist gaze’, as elaborated by John Urry,into the context of the insti- tutions of museums and theme parks. IMAX is seen as a powerful exem- plar of the changing role of cinema-going in contemporary post-Fordist culture, revealing new congurations of older cultural forms and practices. In particular,the growth of this brand of commercial cinema runs parallel to a blurring of the realms of social and cultural activity,referred to as a process of ‘dedifferentiation’. This article gives special attention to the espistemological dimensions of IMAX’s conditions of spectatorship. Keywords cinema; epistemology; postmodernism; technology; tourism; spectatorship Technologies and institutional locations of IMAX N E O F T H E rst things you notice at the start of an IMAX lm, after the suspenseful atmosphere created by the mufed acoustics of the theatre, andO after you sink into one of the steeply sloped seats and become aware of the immense screen so close to you, is the clarity of the image. As cinema-goers, we are accustomed to celluloid scratches, to dirty or dim projections, and to oddly ubiquitous focus problems. The IMAX image astonishes with its vibrant colours and ne details. -

Paramount Pictures' 3-D Movie Transformers: Dark of The

PARAMOUNT PICTURES’3 -D MOVIE TRANSFORMERS: DARK OF THE MOON LAUNCHES BACK INTO IMAX® THEATRES FOR EXTENDED TWO-WEEK RUN Film Grosses $1,095 Billion to Date Los Angeles, CA (August 23, 2011) – IMAX Corporation (NYSE:IMAX; TSX:IMX) and Paramount Pictures announced today that Transformers: Dark of the Moon, the third film in the blockbuster Transformers franchise, is returning to 246 IMAX® domestic locations for an extended two-week run from Friday, Aug. 26 through Thursday, Sept. 8. During those two weeks, the 3-D film will play simultaneously with other films in the IMAX network. Since its launch on June 29, Transformers: Dark of the Moon has grossed $1,095 billion globally, with $59.6 million generated from IMAX theatres globally. “The fans have spoken and we are excited to bring Transformers: Dark of the Moon back to IMAX theatres,”said Greg Foster, IMAX Chairman and President of Filmed Entertainment. “The film has been a remarkable success and we are thrilled to offer fans in North America another chance to experience the latest chapter in this history making franchise.”Transformers: Dark of the Moon: An IMAX 3D Experience has been digitally re-mastered into the image and sound quality of The IMAX Experience® with proprietary IMAX DMR® (Digital Re-mastering) technology for presentation in IMAX 3D. The crystal-clear images, coupled with IMAX’s customized theatre geometry and powerful digital audio, create a unique immersive environment that will make audiences feel as if they are in the movie. About Transformers: Dark of the Moon Shia LaBeouf returns as Sam Witwicky in Transformers: Dark of the Moon. -

Underglobalization Beijing’S Media Urbanism and the Chimera of Legitimacy

Underglobalization Beijing’s Media Urbanism and the Chimera of Legitimacy Joshua Neves Underglobalization Beijing’s Media Urbanism and the Chimera of Legitimacy Joshua Neves duke university press | durham and london | 2020 © 2020 Duke University Press All rights reserved Printed in the United States of Amer i ca on acid- free paper ∞ Designed by Drew Sisk Typeset in Portrait Text, SimSun, and Univers by Westchester Publishing Services Library of Congress Cataloging- in- Publication Data Names: Neves, Joshua, [date] author. Title: Underglobalization : Beijing’s media urbanism and the chimera of legitimacy / Joshua Neves. Description: Durham : Duke University Press, 2020. | Includes bibliographical references and index. Identifiers: lccn 2019032496 (print) | lccn 2019032497 (ebook) isbn 9781478007630 (hardcover) isbn 9781478008057 (paperback) isbn 9781478009023 (ebook) Subjects: lcsh: Product counterfeiting— Law and legislation— China. | Piracy (Copyright)— China. | Legitimacy of governments—China. | Globalization—China. Classification: lcc knq1160.3.n48 2020 (print) | lcc knq1160.3 (ebook) | ddc 302.230951— dc23 lc record available at https:// lccn . loc. gov / 2019032496 lc ebook record available at https:// lccn . loc. gov / 2019032497 Cover art: Xing Danwen, detail from Urban Fictions, 2004. Courtesy of the artist and Danwen Studio. Chapter 5 was originally published in “Videation: Technological Intimacy and the Politics of Global Connection,” in Asian Video Cultures: In the Penumbra of the Global, edited by Joshua Neves and Bhaskar -

Northern Conference Film and Video Guide on Native and Northern Justice Issues

DOCUMENT RESUME ED 287 653 RC 016 466 TITLE Northern Conference Film and Video Guide on Native and Northern Justice Issues. INSTITUTION Simon Fraser Univ., Burnaby (British Columbia). REPORT NO ISBN-0-86491-051-7 PUB DATE 85 NOTE 247p.; Prepared by the Northern Conference Resource Centre. AVAILABLE FROM Northern Conference Film Guide, Continuing Studies, Simon Fraser University, Burnaby, British Columbia, Canada V5A 1S6 ($25.00 Canadian, $18.00 U.S. Currency). PUB TYPE Reference Materials - Bibliographies (131) EDRS PRICE MF01 Plus Postage. PC Not Available from EDRS. DESCRIPTORS Adolescent Development; *American Indians; *Canada Natives; Children; Civil Rights; Community Services; Correctional Rehabilitation; Cultural Differences; *Cultural Education; *Delinquency; Drug Abuse; Economic Development; Eskimo Aleut Languages; Family Life; Family Programs; *Films; French; Government Role; Juvenile Courts; Legal Aid; Minority Groups; Slides; Social Problems; Suicide; Tribal Sovereignty; Tribes; Videotape Recordings; Young Adults; Youth; *Youth Problems; Youth Programs IDENTIFIERS Canada ABSTRACT Intended for teacheLs and practitioners, this film and video guide contains 235 entries pertaining to the administration of justice, culture and lifestyle, am: education and services in northern Canada, it is divided into eight sections: Native lifestyle (97 items); economic development (28), rights and self-government (20); education and training (14); criminal justice system (26); family services (19); youth and children (10); and alcohol and drug abuse/suicide (21). Each entry includes: title, responsible person or organization, name and address of distributor, date (1960-1984), format (16mm film, videotape, slide-tape, etc.), presence of accompanying support materials, length, sound and color information, language (predominantly English, some also French and Inuit), rental/purchase fees and preview availability, suggested use, and a brief description. -

Paranormal Activity 1 Br Rip 1080P Movies Torrents

Paranormal Activity 1 Br Rip 1080p Movies Torrents Paranormal Activity 1 Br Rip 1080p Movies Torrents 1 / 3 2 / 3 [kat.cr]paranormal.activity.the.ghost.dimension.2015.alternate.unrated.720p.brrip.x264.aac.etrg (1).torrent. (15k). Jeu Franco,. Jan 10, 2016, 9:11 PM. v.1.. Paranormal Activity 1 Mp4 ->>->>->> http://shurll.com/dwqrx ... paranormal activity full movie ... BrRip..5.1. ... Torrents..for. ... Paranormal-Activity-2.2010.1080p.. [2010]DvDrip[MKV] torrent or any other torrent from the Video Movies. ... Download Paranormal Activity 2 Tokyo Night-BRrip 720p torrent or any other ... Video HD The Pirate Bay Seeders: 3; Leechers: 0; Comments: 1 Also a.. Ashley Palmer in Paranormal Activity (2007) Katie Featherston and Micah Sloat in ... 1. There is a scene in the Theatrical Cut not present in the Director's Cut that takes ... Katie awakes shortly after midnight on the final night, gets out of bed and stares at ... Well, Oren Peli's little indie film is everything a scary movie should be.. BluRay.720p.x2 torrent or any other torrent from the Video HD - Movies. ... Â Come and download paranormal activity brrip is safe 1 absolutely for free. ... Paranormal Activity The Marked Ones (2014) 720p BRRiP H264 5 1CH-BLiTZCRiEG.. Download Paranormal.Activity.2.2010.UNRATED.BRRip.XviD.MP3-XVID Torrent - RARBG. ... Torrent: Paranormal. ... Category: Movies/XVID.. bb4f9be48f Download YIFY Movies Directed by William Brent Bell via YIFY Torrent ... Download Inside Out (2015) 1080p BrRip x264 - YIFY torrent ... Results 1 - 8 30 Nights of Paranormal Activity with the Devil Inside the Girl.. Paranormal Activity (2007) 720p BrRip x264 - 550MB - YIFY 551 MB Paranormal Activity (2007) 720p BrRip x264 - 550MB - YIFY 551 MB Paranormal Activity ... -

Estta1050036 04/20/2020 in the United States Patent And

Trademark Trial and Appeal Board Electronic Filing System. http://estta.uspto.gov ESTTA Tracking number: ESTTA1050036 Filing date: 04/20/2020 IN THE UNITED STATES PATENT AND TRADEMARK OFFICE BEFORE THE TRADEMARK TRIAL AND APPEAL BOARD Proceeding 91254173 Party Plaintiff IMAX Corporation Correspondence CHRISTOPHER P BUSSERT Address KILPATRICK TOWNSEND & STOCKTON LLP 1100 PEACHTREE STREET, SUITE 2800 ATLANTA, GA 30309 UNITED STATES [email protected], [email protected], [email protected] 404-815-6500 Submission Motion to Amend Pleading/Amended Pleading Filer's Name Christopher P. Bussert Filer's email [email protected], [email protected], [email protected] Signature /Christopher P. Bussert/ Date 04/20/2020 Attachments 2020.04.20 Amended Notice of Opposition for Shenzhen Bao_an PuRuiCai Electronic Firm Limited.pdf(252165 bytes ) IN THE UNITED STATES PATENT AND TRADEMARK OFFICE BEFORE THE TRADEMARK TRIAL AND APPEAL BOARD In the matter of Application Serial No. 88/622,245; IMAXCAN; Published in the Official Gazette of January 21, 2020 IMAX CORPORATION, ) ) Opposer, ) ) v. ) Opposition No. 91254173 ) SHENZHEN BAO’AN PURUICAI ) ELECTRONIC FIRM LIMITED, ) ) Applicant. ) AMENDED NOTICE OF OPPOSITION Opposer IMAX Corporation (“Opposer”), a Canadian corporation whose business address is 2525 Speakman Drive, Sheridan Science and Technology Park, Mississauga, Ontario, Canada L5K 1B1, believes that it will be damaged by registration of the IMAXCAN mark as currently shown in Application Serial No. 88/622,245 and hereby submits this Amended Notice of Opposition pursuant to 37 C.F.R. §2.107(a) and Fed. R. Civ. P. 15, by which Opposer opposes the same pursuant to the provisions of 15 U.S.C. -

CN Tower Makes Waves with 3D Theatre Premiere on Canada Day

CN Tower Makes Waves with 3D Theatre Premiere on Canada Day June 30, 2010 (Toronto, ON) Premiering Canada Day, July 1 st , the CN Tower will launch a new 3D theatre experience featuring The Ultimate Wave Tahiti 3D, the Toronto premiere of the first 3D surf film ever created. “We are always looking at innovative ways to make the CN Tower experience more exciting and our state of the art high definition 3D theatre featuring a spectacular film about surfing in Tahiti will be an exciting new addition to the lineup of thrilling experiences that we offer,” said Jack Robinson, Chief Operating Officer. Visitors will be able to experience the phenomenon of new, improved 3D at the CN Tower’s new state of the art high definition theatre featuring The Ultimate Wave Tahiti 3D . The Ultimate Wave Tahiti 3D is a 45 minute film created by Canada’s own Stephen Low Productions. Audiences are immersed into the stunning beauty of an island paradise on a quest to find the perfect wave-riding experience. The film follows nine-time world surfing champion Kelly Slater and Tahitian surfer Raimana Van Bastolaer as they seek out the best waves at Tahiti’s famed reef at Teahupo’o. As their quest unfolds, the audience is plunged beneath the surface of things, to explore the magic of Tahiti, the life of the reef and the hidden forces at work shaping ocean waves and the islands that lie in their path. Hailing from Montreal, Director Stephen Low is one of Canada’s most experienced filmmakers, bringing to his work a unique storytelling vision and an understanding of the language and tremendous possibilities of 3D cinema.