For Posting-COR Monitoring As of 27 August 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Frequently Asked Questions on What Is Pesonet?

Frequently Asked Questions on What is PESONet? PESONet is a new electronic fund transfer service that enables customers of participating banks, e- money issuers or mobile money operators to transfer funds in Philippine Peso currency to another customer of other participating banks, e-money issuers or mobile money operators in the Philippines. It is more inclusive platform for Electronic Fund Transfers which will make G2B(Government-to- Business) and G2C(Government-to-Consumer) payments more practical, convenient, fast, and secure. What is the purpose of PESONet? Through PESONet, businesses, government, and individuals will be able to conveniently pay or transfer funds from their account to one or multiple recipient accounts in other financial institutions. PESONet is the perfect alternative to the still widely used paper-based check system. What are the features of PESONet? What are the uses of PESONet? How does PESONet work? Customers instruct their financial institution to send credit instructions to other financial institutions via online banking, mobile banking or over-the-counter transaction. They need to provide the payees’ financial institution, account number, and amount. The credit instruction is transmitted by the financial institution to the clearing switch operator, which currently is the Philippine Clearing House Corporation (PCHC). The funds are settled in the respective financial institutions demand deposit accounts held in Bangko Sentral ng Pilipinas (BSP) through BSP’s Philippine Payments and Settlement System (PhilPaSS). Upon settlement, the beneficiary’s or payee’s financial institution will credit the payee's account. How long does it take to transfer funds via PESONet? The availability of funds to the receiving account shall depend on the facility used to carry out your transaction. -

Country Diagnostic: Philippines

Philippines BETTERTHANCASH COUNTRY DIAGNOSTIC ALLIANCE Empowering People Through Electronic Payments July 2015 Development Results Focused Research Program Country Diagnostic: Philippines by James Hokans, Bankable Frontier Associates Philippines BETTERTHANCASH COUNTRY DIAGNOSTIC ALLIANCE Empowering People Through Electronic Payments July 2015 Development Results Focused Research Program Country Diagnostic: Philippines by James Hokans, Bankable Frontier Associates BETTERTHANCASH ALLIANCE Empowering People Through Electronic Payments INTRODUCTION TO THE BETTER THAN CASH ALLIANCE The Better Than Cash Alliance (the Alliance) is a partnership of governments, companies, and international organizations that accelerates the transition from cash to digital payments in order to drive inclusive growth and reduce poverty. Shifting from cash to digital payments has the potential to improve the lives of low-income people, particularly women, while giving governments, companies and international organizations a more transparent, time- and cost-efficient, and often safer means of making and receiving payments. We partner with governments, companies, and international organizations that are the key drivers behind the transition to make digital payments widely available by: 1. Advocating for the transition from cash to digital payments in a way that advances financial inclusion and promotes responsible digital finance. 2. Conducting research and sharing the experience our members to inform strategies for making the transition 3. Catalyzing the development -

Chapter 1 Introduction

CHAPTER 1 INTRODUCTION Globally, banking system is working continuously from many years. Paper money or cash has been leading payment mechanism worldwide for the centuries. The measure works of a bank to deposits an amount of a customer and returns it to him when he needs. During deposits and withdrawal of the amount bank may use this money for itself as to given loans to other customers who wants to avail it. There are so many types of loan like home loan, agricultural loan, personnel loan, loan for industries and business houses etc. Banks give a particular interest for the depositors on his money and take a certain interest from loan account holder. There are very fast changes occur in the traditional banking operation system. Before a decade ago a bank was involved only with customers when they were at premises of bank. But during this new time a bank provides many more services to the customer’s at their doorsteps. The entire system of banking has changed drastically. In banking system there are two most frequent and important services- one is to deposit cash in the account and second to withdraw cash from the account. Both the service provided to a customer during a time in which banks are open and officials present at that time. Here in this work our main concern is about the withdrawal service provided by the bank. Banks normally provide this cash through teller counters. Only in the past century paper money or cash faced competition from mainly cheques, debit and credit cards. Previously this whole process was thoroughly manual and nowadays it is automatic. -

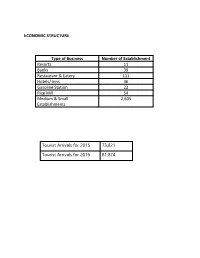

Economic Structure

ECONOMIC STRUCTURE Type of Business Number of Establishment Resorts 11 Banks 39 Restaurant & Eatery 111 Hotels/ Inns 46 Gasoline Station 22 Rice Mill 54 Medium & Small 2,605 Establishments Tourist Arrivals for 2015 73,821 Tourist Arrivals for 2016 81,874 List of Banks with ATM & Offsite ATM NO. NAME OF BANKS LOCATION With ATM ATM Offsi 1 Agri Business Rural Bank Camilmil 1 2 Asia United Bank San Vicente 1 3 Banco Alabang (A Rural Bank) San Vicente West 4 Banco de Mindoro ( A Rural Bank) Ibaba East 5 Banco de Oro Unibank Inc. San Vicente East 2 6 Banco de Oro Unibank Inc. Camilmil 2 7 Bank of Commerce San Vicente 1 8 Bank of Makati Lumangbayan 9 Bank of the Phil. Islands San Vicente East 2 10 Bank of the Phil. Islands Camilmil 3 11 Card Bank, Inc. Comunal 12 Card Bank, Inc. Sta. Isabel 13 Card Bank, Inc. Bucayao 14 Card Bank, Inc. Biga 15 Card Bank, Inc. Comunal 16 Card Rural Bank, Inc. Ilaya 1 17 China Banking Corp. San Vicente South 1 18 City Savings Bank, Inc. Camilmil 1 19 Country Bank San Vicente North 20 Development Bank of the Phils. Sto. Nino 1 1 21 East West Banking Corp San Vicente South 1 22 First Consolidated Bank San Vicente South 1 23 Land Bank of the Phils. Sto. Nino 3 4 24 Maybank Philippines, Inc San Vicente South 1 25 Metrobank San Vicente 2 2 26 Metrobank Lalud 1 27 Microfinance Savings Bank Ibaba East 28 Robinson's Bank Corp Lumangbayan 1 29 Philippine Business Bank San Vicente East 1 30 Philippine National Bank Camilmil 1 31 PNB Savings Bank San Vicente West 1 32 RCBC Savings Bank Camilmil 1 1 33 Rural Bank of Baco San Vicente 34 Rural Bank of Pinamalayan, Inc. -

HSBC CREDIT CARDS Faqs

HSBC CREDIT CARDS FAQs Section 1: Application Q: What HSBC Credit Cards may I apply for? A: You may apply for an HSBC Gold Visa Cash Back, HSBC Platinum Visa or HSBC Red MasterCard credit card. If you are an HSBC Advance or Premier bank depositor, you may apply for an HSBC Advance Visa or HSBC Premier Mastercard credit card. To find the right HSBC credit card the suits your needs, click here: http://www.hsbc.com.ph/1/2/personal/credit/compare. Q: How do I apply for an HSBC Credit Card? A: You may apply for an HSBC Credit Card online at http://www.hsbc.com.ph/1/2/personal/credit/compare or at an HSBC branch near you. Q: What documentation do I need to provide when applying for an HSBC Credit Card? A: You will need to have an annual income of at least Php200K, Other Bank Credit Card/s (Credit Card should be at least 12 months and you should be the primary cardholder) and provide a copy of the following: 1. Proof of Identity with Complete name (at least one of the following) • Passport, Driver’s License, SSS/TIN ID plus NBI Clearance or Voter’s ID Note: Proof of Identity should be valid (not expired), photo-bearing and contain date of birth. 2. Proof of Residence (Note: Must be under the name of the applicant) • Valid ID containing the address of the applicant • Utility bills (electricity, landline phone, mobile phone or cable TV issued within the last 3 months and must match the permanent and primary address) Q: How long will it take to process an HSBC Credit Card application? A: Around 5-10 business days upon submission of a completed application forms and all required documents. -

The Alignment of Screens

The Alignment of Screens Felipe Raglianti , B.A.; M.A. Submitted for the degree of Doctor of Philosophy (PhD) Department of Sociology, Lancaster University, 2016 Declaration I declare that this thesis is my own work and that it has not been submitted in any form for the award of a higher degree elsewhere. Felipe Raglianti, June 2016 1 Abstract This thesis makes a distinction between screen and surface. It proposes that an inquiry into screens includes, but is not limited to, the study of surfaces. Screens and screening practices are about doing both divisions and vision. The habit of reducing screens to the display neglects their capacity to emplace separations (think of folding screens). In this thesis an investigation of screens becomes a matter of asking how surfaces and the gaps in between them articulate alignments of people and things with displays that, in practice, always leave something out of sight. Rather than losing touch with screens by reducing them to surfaces, in other words, I am interested in alternative screen configurations. For this task I sketch an approach that touches on screens through the figures of lines, surfaces, textures, folds, knots and cuts. Lines help me to make the case for thinking about screens as alignments. I then ask what kinds of observers emerge from reducing screens to single or digital surfaces. I trace that concern with Google Glass, a pair of “smartglasses” with a transparent display. To distinguish between screen and surface I suggest, through a study of biodetection and assistance dogs, how to qualify or texture screens within webs of relations. -

Remittance Bank List of Philippines Bank Name

Remittance Bank List of Philippines Bank Name AL AMANAH ISLAMIC INVESTMENT BANK ALLBANK ANZ BANK ASIA UNITED BANK BANK OF AMERICA BANK OF CHINA BOF, INC (A Rural Bank) - (BANK OF Florida) BANGKOK BANK PUBLIC CO LTD BDO - BANCO DE ORO BDO NETWORK BANK BDO PRIVATE BANK BOC - BANK OF COMMERCE BPI - BANK OF THE PHILIPPINE ISLANDS BPI FAMILY BANK BPI DIRECT BANKO CAMALIG BANK, INC (A Rural Bank) CEBUANA LHUILLIER RURAL BANK INC CHINA BANK CHINA BANK SAVINGS CTBC BANK ( FORMER CHINA TRUST) CIMB BANK PHILIPPINES, INC. CITIBANK DBP - DEVELOPMENT BANK OF THE PHILIPPINES DEUTSCHE BANK DUNGGANON BANK EAST WEST BANK EASTWEST RURAL BANK EQUICOM SAVINGS BANK INC FIRST CONSOLIDATED BANK HSBC - HONGKONG AND SHANGHAI BANKING CORPORATION HSBC SAVINGS BANK INDUSTRIAL BANK OF KOREA ING BANK N.V. ISLA BANK INC. KEB HANA (Korea Exchange Bank) JP MORGAN CHASE BANK LBP - LAND BANK OF THE PHILIPPINES MALAYAN BANK SAVINGS AND MORTGAGE BANK INC (MALAYAN SVGS) MAYBANK PHILIPPINES INC (PNB Republic) MEGA INTL COMML BANK CO LTD (ICBC) MIZUHO BANK LTD (FUJI BANK) MUFG BANK LTD (BANK OF TOKYO) PARTNER RURAL BANK (COTABATO) INC PBCOM - PHILIPPINE BANK OF COMMUNICATIONS PHIL BUSINESS BANK PHILIPPINE VETERANS BANK PHILTRUST CO (Philtrust Bank) PNB - PHILIPPINE NATIONAL BANK (Allied Bank) PRODUCERS SAVINGS BANK CORP PSBANK - PHILIPPINE SAVINGS BANK QUEZON CAPITAL RURAL BANK INC RCBC - RIZAL COMMERCIAL BANKING CORPORATION ROBINSONS BANK CORPORATION RURAL BANK OF GUINOBATAN INC (RBGI) SECURITY BANK CORPORATION SHINHAN BANK STERLING BANK OF ASIA SUMITOMO MITSUI BANKING CORP SUN SAVINGS BANK INC THE STANDARD CHARTERED BANK UCPB - UNITED COCONUT PLANTERS BANK UCPB SAVINGS BANK UNION BANK OF THE PHILIPPINES (City Savings Bank) UNITED OVERSEAS BANK PHILIPPINES WEALTH DEVELOPMENT BANK YUANTA SAVINGS BANK PHILS INC (Tongyang) . -

Automated Teller Machine - Wikipedia, the Free Encyclopedia

Automated teller machine - Wikipedia, the free encyclopedia http://en.wikipedia.org/wiki/Automated_teller_machine From Wikipedia, the free encyclopedia An automated teller machine or automatic teller machine (ATM), also known as an automated banking machine (ABM) in Canada, and a Cashpoint (which is a trademark of Lloyds TSB), cash machine or sometimes a hole in the wall in British English, is a computerized telecommunications device that provides the clients of a financial institution with access to financial transactions in a public space without the need for a cashier, human clerk or bank teller. ATMs are known by various other names including ATM machine, automated banking machine, and various regional variants derived from trademarks on ATM systems held by particular banks. On most modern ATMs, the customer is identified by inserting a plastic ATM card with a magnetic stripe or a plastic smart card with a chip, that contains a unique card number and some security information such as an expiration date or CVVC (CVV). Authentication is provided by the customer entering a personal identification number (PIN). Using an ATM, customers can access their bank accounts in order to make cash withdrawals, debit card cash advances, and check their account balances as well as purchase prepaid cellphone credit. If the currency being withdrawn from the ATM is different from that which An NCR Personas 75-Series interior, the bank account is denominated in (e.g.: Withdrawing Japanese Yen multi-function ATM in the United from a bank account containing US Dollars), the money will be States converted at an official wholesale exchange rate. -

Annual Report 2017

ANNUAL REPORT 2017 METRO CEBU PUBLIC SAVINGS BANK Email: [email protected] Address: Sia Bldg., N. Bacalso Ave., Brgy. Duljo Fatima, Cebu City Tel No.: 231-4043 / 231-3923 2 CONTENTS CORPORATE POLICY______________________________________________________ 3 Vision __________________________________________________________________ 3 Mission _________________________________________________________________ 3 Company Profile __________________________________________________________ 4 A MESSAGE FROM THE PRESIDENT _________________________________________ 5 Financial Highlights 2017 ___________________________________________________ 7 Financial Summary ______________________________________________________ 10 RISK MANAGEMENT FRAMEWORK __________________________________________11 Overall Risk Management Culture and Philosophy ______________________________ 11 AML Governance and Culture ______________________________________________ 12 CORPORATE GOVERNANCE _______________________________________________ 13 Governance Structure ____________________________________________________ 13 Chairman of the Board of Directors __________________________________________ 14 Board Composition_______________________________________________________ 15 THE BOARD OF DIRECTORS _______________________________________________ 16 Board Committees, Membership and Functions __________________________________ 21 Directors’ Attendance at Board and Committee Meetings __________________________ 27 List of Executive Officers ____________________________________________________ -

About Bancnet

About BancNet Presented at 19th Floor, Equitable Tower, 8751 Paseo de Roxas Makati City 1226 Who is BancNet • Electronic Switch Network that has financial institutions as its shareholders / members • 113 Member Banks • The largest inter bank network in the Philippines • First and Largest ATM Consortium in the Philippines • More than 23 years experience in ATM Networks • 113 Member Banks and Subscribers … and growing • Over 33.2 Million Active Cardholders, 11,383 ATMs • Strategy of Going Beyond ATM Banking • Multi-Bank, Multi-Channel Electronic Payment Network National and International Interconnection • ATM Networks Expressnet, Megalink • ATM Networks Mastercard, VISA • ATM & POS Network China Union Pay (CUP) • International partnership with NYCE BancNet Network I.CAN Government Agencies EPS POS POS Network ATM Network Network WeePay Member Banks ECS Bankard POS Network GHL BDO POS Network ATM Network Channels, Products & Services Point-of-Sale Internet Mobile Phone Mobile Phone Cash Withdrawal Intrabank Fund Transfer Cash Advance Inter Bank Fund Transfer Intrabank Fund Transfer Debit Card Purchase/Cash (CUP/VISA/JBC/Discover/D Checkbook Reorder Inter Bank Fund Transfer Withdrawal or Cash-out iners/MasterCard/Local) e-Shopping Checkbook Reorder Intrabank Fund Transfer Tax Payment e-Load Inter Bank Fund Transfer SSS-EDI Corporate G-Cash Reload Checkbook Reorder Philhealth (softlaunch) Statement Request Pagibig (Soon) G-Cash Reload/Auto Reload Balance Inquiry and Bills Payment Going Beyond ATM Banking BANCNET TAX PAYMENT ENROLLMENT PROCESS via BIR WEBSITE BANCNET BIR RDO EMPLOYER HSBC-AAB INFRASTRUCTURE Enroll via BIR Website Validate required documents submitted by Employer Bank to enroll the ff: via BancNet TPG Receive email 1. -

BSP Digital Payments Transformation Roadmap Report

BSP Digital Payments Transformation Roadmap 2020-2023 I. Vision and Strategic Outcomes (Targets by 2023) The BSP’s thrust to promote financial inclusion and digitalization of payments are mutually reinforcing: they go hand-in-hand, each enabling the other. As the BSP continues to foster the growth and development of digital payment innovations through enabling policies and regulations, it also promotes further financial inclusion. Digital payment innovations lower transaction costs and eliminate the oft-cited barriers to owning a transaction account. The widespread use of the internet and emergence of technological innovations make digital payments ubiquitous, more accessible and affordable, thereby propelling the progressive shift towards a cash-lite economy. Moreover, with the sudden onset of the COVID-19 global pandemic, the shift towards digital payments has become an imperative as physical distancing rules become the norm under the “New Economy” environment. By using digital payments with due care and vigilance, Filipinos reduce the need for mobility and prevent health risks from face-to-face and over-the-counter (OTC) financial transactions. The greater usage of digital payments will also facilitate the growth of Fintech businesses engaged in e-commerce businesses as the consumption of goods and services is increasingly driven by online purchases. Objective An efficient, inclusive, safe and secure digital payments ecosystem that supports the diverse needs and capabilities of individuals and firms, towards achievement of the BSP’s mandates Strategic Outcomes a. Strengthened customer preference for digital payments by: • Converting 50% of the total volume of retail payments into digital form, considering that payment services are the gateway of most Filipinos to the formal financial system. -

2020 Annual Report

Chairman’s Message While 2020 will be remembered as the year of COVID-19, it was also year that allowed us at FCB to reflect. The year 2020 showed us PURPOSE. The importance of our role as bankers to ensure the functionality and strength of our communities was made exceedingly clear to us. Our depositors need continued access to their deposits, and our borrowers need access to liquidity for their needs, especially during times of calamity. We at FCB are proud to have provided steadfast service in all our areas. The year 2020 proved our RESILIENCE. We have had to be mentally and emotionally strong to face the unexpected challenges this year, as individuals, and as an organization. Our company was committed to taking care of our people, and our people remained committed to our mission to provide affordable banking services to our clients. The year 2020 is also a year that showed us the importance of ADAPTABILITY. COVID-19 has reminded us that we operate in a Darwinian landscape. It is not the biggest or largest that will survive, but the fastest to adapt. We have adjusted as restrictions and rules kept changing. We have maintained a proactive mindset, while providing tools to support this mindset and to adjust to the New Normal. Offering the online application process for qualified borrowers, offering various outlets for releases, introducing new products, and identifying new markets have all been part of adapting. Maintaining support staff in regional clusters in order to ensure operational continuity has also been essential. We are also proud to announce that our mobile banking app, FCBPay, which is not only responsive to the needs of this time but also an important step towards the future, was officially launched in February 2021.