State of Alaska Teachers' Retirement System

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Registered School Board Members & Superintendents for the Fly-In

Full Name Company Title Jackson, Tiffany Aleutians East Borough School District Board Member Smith, Hillary Aleutians East Borough School District School Board Member Marsett, Starr Anchorage School District School Board Vice President Bishop, Dr. Deena Anchorage School District Superintendent Atkinson, Tia Annette Island School District Board President Vlasoff, Roseline Chugach School District School Board Member Totemoff, David Chugach School District School Board Member Vlasoff, Gwen Chugach School District School Board Member Graham, Frankie Chugach School District School Board Vice President Arneson, Charlene Chugach School District School Board President Hanley, Michael Chugach School District Superintendent Hoepfner, Peter Cordova School District Board Member Hamm, Jenna Denali Borough School District Board Member Tench, James Denali Borough School District Board Member Ferguson, Sasha Denali Borough School District Executive Administrative Assistant Polta, Dan Denali Borough School District Superintendent Merriner, Jim Galena City School District Assistant Superintendent Huntington, Fred Galena City School District Board Vice President Sam, Susie Galena City School District Board President Villarreal, Grace Hoonah City Schools School Board Member Jewell, Heidi Hoonah City Schools Vice President Hutton, Robert Hoonah City Schools School Board President Morris, Bonnie Hydaburg City School Board President Story, Andi Juneau School District Board Clerk Johnson, Charley Kake City School District Board Member Bean Jr., William Kake City -

State LEA Name LEA NCES ID School Name School NCES ID Reading

Elementary/ Middle Reading Reading Math Math School NCES School Graduation School Improvement Status for SY State LEA Name LEA NCES ID School Name Proficiency Participation Proficiency Participation ID Other Rate 2010-11 Target Target Target Target Academic Indicator Alaska Alaska Gateway School District 0200050 Gateway Correspondence Yes Yes Yes Yes N/A Yes Corrective Action Restructuring Year 2 Alaska Alaska Gateway School District 0200050 Tetlin School No Yes No Yes N/A No (implementing) Alaska Alaska Gateway School District 0200050 Tok School No Yes Yes Yes N/A Yes School Improvement - Year 1 Restructuring Year 2 Alaska Alaska Gateway School District 0200050 Walter Northway School No Yes No Yes N/A No (implementing) Airport Heights Alaska Anchorage School District 0200180 Elementary No Yes No Yes Yes N/A Corrective Action Alaska Anchorage School District 0200180 Chinook Elementary No Yes Yes Yes Yes N/A Corrective Action Alaska Anchorage School District 0200180 Clark Middle School No Yes No Yes Yes N/A Restructuring Year 1 (Planning) Restructuring Year 2 Alaska Anchorage School District 0200180 Fairview Elementary No Yes No Yes Yes N/A (implementing) Alaska Anchorage School District 0200180 Lake Otis Elementary No Yes Yes Yes Yes N/A Corrective Action Mountain View Alaska Anchorage School District 0200180 Elementary No Yes Yes Yes Yes N/A School Improvement - Year 1 Alaska Anchorage School District 0200180 Muldoon Elementary No Yes No Yes Yes N/A School Improvement - Year 2 Restructuring Year 2 Alaska Anchorage School District 0200180 -

Title I District Improvement List Level 1 and Above Level 1 Districts Level 1 ‐ Alert: Consult with the Department Regarding Reasons for Not Meeting AYP

2012‐2013 Title I District Improvement List Level 1 and Above Level 1 Districts Level 1 ‐ Alert: Consult with the Department regarding reasons for not meeting AYP. Aleutians East Borough School District ** Chatham School District ** Chugach School District ** Copper River School District ** Hoonah City School District ** Hydaburg City School District ** Klawock City School District ** Nenana City School District ** Petersburg City School District ** Pribilof School District ** Southeast Island School District ** Tanana City School District ** Valdez Cityl Schoo District ** Wrangell Public School District Level 2 Districts Level 2 and 3 ‐ District Improvement: District shall develop, issue, and implement a district improvement plan, submit the plan to the Department, request technical assistance from the Department, and provide notice to parents. District must spend 10% of its Title I allocation on professional development. Denali Borough School District Craig City School District ** Kenai Peninsula Borough School District Sitka School District ** Saint Mary's School District Level 3 Districts Delta‐Greely School District ** Ketchikan Gateway Borough School District ** Level 4 Districts Level 4 ‐ Corrective Action: District shall continue to implement a district improvement plan, submit the plan to the Department, request technical assistance from the Department, provide notice to parents, and spend 10% of Title I allocation on professional development. The Department must take one or more corrective actions. Alaska Gateway School District -

Minutes of the Yupiit School District Regional Board of Education

Yupiit School District Box 51190 ● Akiachak, AK 99551 ● Telephone (907) 825-3600 ● FAX (877) 825-2404 Date: January 16, 2020 To: Regional School Board From: Cassandra Bennett, Superintendent Re: Approval of Agenda The Administration recommends the approval of the Agenda for January 16, 2020. The Mission of the Yupiit School District is to educate all children to be successful in any environment. Regional Board Members Willie Kasayulie, Chairman Ivan M. Ivan, Vice Chairman Peter Gregory SR, Board Secretary Samuel George, Treasurer Moses Owen, Board Member Moses Peter, Board Member Robert Charles, Board Member Regional Board of Education Meeting LOCATION: Akiachak, Alaska DATE: January 16, 2020 I. Call to Order II. Roll Call III. Invocation IV. Recognition of Guests V. Approval of Agenda VI. Approval of Minutes: December 19, 2019 VII. Correspondence: VIII. Action Items: A. 2020 Recommended Certified for Re-Hire B. IX. Reports: A. Attendance Report: B. School Reports: 1. Akiachak 2. Akiak 3. Tuluksak C. Special Ed Director/Curriculum, Assessment Report D. Tribal Ed Director’s Report E. ANE Director’s Report F. Business and Finance Report G. Federal/State Programs Report H. Maintenance & Operations Report I. Technology Director Report J. Superintendent’s Report X. Executive Session: XI. Board Travel/Info: AASB Legislative Fly-In February 8-11, 2020 XII. Public Comments: XIII. Board Comments XIV. Next Regular Meeting: February 20, 2020 XV. Adjournment Yupiit School District Box 51190 ● Akiachak, AK 99551 ● Telephone (907) 825-3600 ● FAX (877) 825-2404 Date: January 16, 2020 To: Regional School Board From: Cassandra Bennett, Superintendent Re: Approval of Minutes The Administration recommends the approval of the Minutes for December 19, 2019. -

Districts Required to Submit Report of Comparability SY20-21

Districts Required to Submit the Title I Report of Comparability All districts are required to submit a Title I Report of Comparability by Friday, February 12, 2021 for the 2020‐21 school year unless one of the following conditions exists: All schools in the district, or all schools except one, have less than 100 students enrolled on the October 1, 2020 count date. The district is a single site district with only one school, or only one school per grade span at a single site. The only schools in the district with an enrollment greater than or equal to 100 are in different grade spans. Districts that do not meet the above conditions are required to submit a report of comparability even if all schools in the district are served as Title I schools. In that situation, the Title I schools are compared with each other rather than with the non‐Title I schools. Based on the October 1, 2020 data for the 2020‐2021 school year, the following districts must file a Title I Report of Comparability for the 2020‐2021 school year: Anchorage School District Kodiak Island Borough School District Bering Strait School District Lower Kuskokwim School District Denali Borough School District Lower Yukon School District Fairbanks North Star Borough School Matanuska‐Susitna Borough School District District Nenana City School District Juneau Borough School District North Slope Borough School District Kenai Peninsula Borough School Northwest Arctic Borough School District District Southwest Region School District Ketchikan Gateway Borough School Yupiit School District District Questions: Courtney Preziosi ESEA/Title I Administrator [email protected] 907‐465‐2888 Report Submissions: Jeanny Smith Education Associate II [email protected] 907‐465‐2884 Form # 05‐12‐021a Districts Required to Submit the Title I Report of Comparability Alaska Department of Education & Early Development . -

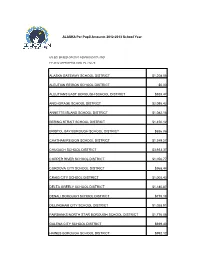

Alaska Gateway School District $1,208.06 Aleutian

ALASKA Per Pupil Amounts 2012-2013 School Year US ED: BASED ON 2010 CENSUS DATA AND FY 2012 APPROPRIATION, PL 112-74 ALASKA GATEWAY SCHOOL DISTRICT $1,208.06 ALEUTIAN REGION SCHOOL DISTRICT $0.00 ALEUTIANS EAST BOROUGH SCHOOL DISTRICT $935.47 ANCHORAGE SCHOOL DISTRICT $2,095.42 ANNETTE ISLAND SCHOOL DISTRICT $1,082.18 BERING STRAIT SCHOOL DISTRICT $1,450.12 BRISTOL BAY BOROUGH SCHOOL DISTRICT $856.06 CHATHAM REGION SCHOOL DISTRICT $1,349.27 CHUGACH SCHOOL DISTRICT $3,933.37 COPPER RIVER SCHOOL DISTRICT $1,056.77 CORDOVA CITY SCHOOL DISTRICT $968.44 CRAIG CITY SCHOOL DISTRICT $1,005.43 DELTA GREELY SCHOOL DISTRICT $1,180.87 DENALI BOROUGH SCHOOL DISTRICT $715.18 DILLINGHAM CITY SCHOOL DISTRICT $1,028.91 FAIRBANKS NORTH STAR BOROUGH SCHOOL DISTRICT $1,776.06 GALENA CITY SCHOOL DISTRICT $939.40 HAINES BOROUGH SCHOOL DISTRICT $992.12 HOONAH CITY SCHOOL DISTRICT $1,181.58 HYDABURG CITY SCHOOL DISTRICT $2,520.88 IDITAROD AREA SCHOOL DISTRICT $1,645.38 JUNEAU BOROUGH SCHOOL DISTRICT $1,556.96 KAKE CITY SCHOOL DISTRICT $1,675.79 KASHUNAMIUT SCHOOL DISTRICT $1,554.43 KENAI PENINSULA BOROUGH SCHOOL DISTRICT $1,692.27 KETCHIKAN GATEWAY BOROUGH SCHOOL DISTRICT $978.87 KLAWOCK CITY SCHOOL DISTRICT $1,280.64 KODIAK ISLAND BOROUGH SCHOOL DISTRICT $919.41 KUSPUK SCHOOL DISTRICT $1,650.53 LAKE AND PENINSULA SCHOOL DISTRICT $1,292.44 LOWER KUSKOKWIM SCHOOL DISTRICT $1,268.35 LOWER YUKON SCHOOL DISTRICT $1,486.26 MATANUSKA-SUSITNA BOROUGH SCHOOL DISTRICT $1,789.15 NENANA CITY SCHOOL DISTRICT $1,266.52 NOME CITY SCHOOL DISTRICT $915.79 NORTH SLOPE BOROUGH -

Alaska State Profile: Fresh Fruit and Vegetable Program 2018-2019

Alaska State Profile: Fresh Fruit and Vegetable Program Congress founded the Fresh Fruit and Vegetable Program (FFVP) in 2002 to expose low income elementary students to a wider variety of fresh fruits and vegetables. The program is overwhelmingly popular with schools, parents, and students – and extensive evaluation has shown that the program can reduce obesity rates and increase consumption both within the snack program and at school lunch. Today, 7,600 schools reaching four million students participate in FFVP! 2018-2019 School Year School District Schools Alaska Gateway School District 7 Anchorage School District 36 Annette Island School District 1 Bering Strait School District 15 Bristol Bay Borough School District 1 Chatham School District 1 Cordova City School District 1 Craig City School District 1 Dillingham City School District 1 Fairbanks North Star Borough School District 4 Haines Borough School District 1 Hoonah City School District 1 Iditarod Area School District 7 Juneau Borough School District 4 Kashunamiut School District 1 Kenai Peninsula Borough School District 13 Ketchikan Gateway Borough School District 4 Klawock City School District 1 Kodiak Island Borough School District 9 Kuspuk School District 7 Lake and Peninsula Borough School District 12 Lower Kuskokwim School District 29 Lower Yukon School District 10 Matanuska-Susitna Borough School District 13 Nenana City School District 1 North Slope Borough School District 7 Northwest Arctic Borough School District 11 Petersburg Borough School District 1 Saint Mary’s School District 1 Sitka School District 2 Southeast Island School District 7 Southwest Region School District 8 Yukon Flats School District 6 Yukon Koyukuk School District 10 Yupiit School District 3 . -

Alaska Designated Schools List 2018-2019

2018-2019 System for School Success Alaska Schools Designated for Support Comprehensive Support (Lowest 5%) - 2018 School Name District Name Tetlin School Alaska Gateway School District Wales School Bering Strait School District Johnnie John Sr. School Kuspuk School District Joseph S. & Olinga Gregory Elementary Kuspuk School District Zackar Levi Elementary Kuspuk School District Nome Elementary Nome Public Schools Nuiqsut Trapper School North Slope Borough School District Naukati School Southeast Island School District William "Sonny" Nelson School Southwest Region School District Twin Hills School Southwest Region School District Arctic Village School Yukon Flats School District Circle School Yukon Flats School District Akiachak School Yupiit School District Tuluksak School Yupiit School District Comprehensive Support (Lowest 5%) - 2019 School Name District Name Tanacross School Alaska Gateway School District Diomede School Bering Strait School District Naknek Elementary Bristol Bay Borough School District Old Harbor School Kodiak Island Borough School District Pilot Point School Lake and Peninsula Borough School District Negtemiut Elitnaurviat School Lower Kuskokwim School District Ambler School Northwest Arctic Borough School District Davis-Ramoth School Northwest Arctic Borough School District Togiak School Southwest Region School District Access additional demographic information and Designation Reports for designated schools at: System for School Success 2018-2019 System for School Success Comprehensive Support (Lowest 5% - SSR) - 2018 School Name District Name Blackwell School Iditarod Area School District Top of the Kuskokwim School Iditarod Area School District Comprehensive Support (Graduation Rate) - 2019 School Name District Name Alaska REACH Academy Alaska Gateway School District AVAIL School Anchorage School District McLaughlin Secondary School Anchorage School District Benson Secondary/S.E.A.R.C.H. -

Minutes of the Yupiit School District Regional Board of Education

Yupiit School District Box 51190 Akiachak, AK 99551 Phone (907) 825-3600 Fax (877) 825-2404 www.yupiit.org Date: July 16, 2020 To: Regional School Board From: Cassandra Bennett, Superintendent Re: Committee Meeting and Work-session The topics for the Committee Meeting and Work-session are the following: Strategic Plan Report/Review, Board Evaluations, Goal Settings, Board Self Assessments and Joel Isaak, Project Coordinator, State-Tribal Ed Compacting. “To educate all children to be successful in any environment.” Yupiit School District Box 51190 ● Akiachak, AK 99551 ● Telephone (907) 825-3600 ● FAX (877) 825-2404 Strategic Plan Approved August 17, 2018 Mission Statement: To educate all children to be successful in any environment Vision Statement (new draft): All members of the community are proud and committed to our school system. Students have a positive learning environment, speak the Yupiaq language, know their culture, attend school regularly and graduate prepared to be successful in any environment. The majority of our teachers and school staff are Yupik and speak their language, and the curriculum and instruction is based in Yupik values and traditions. Our community members, elders, parents, and students feel ownership in our schools. Values Love for Children Spirituality Sharing Humility Hard work Respect for Others and Their Property Cooperation Family Roles Knowledge of family tree Hunter Success Domestic Skills Knowledge of Language Avoid conflict Humor Respect For Land Respect For Nature Akiak School Akiachak School Tuluksak School P.O. Box 49 P.O. Box 51189 P.O. Box 115 Akiak, Alaska 99552 Akiachak, Alaska 99551 Tuluksak, Alaska 99679 Tel. (907) 765-4600 Tel. -

Aug 2017 YSD Board Packet

Yupiit School District Box 51190 ● Akiachak, AK 99551 ● Telephone (907) 825-3600 ● FAX (877) 825-2404 Date: August 17, 2017 To: Regional School Board From: Rayna Hartz, Superintendent Re: Work-session – Strategic Plan Review The Strategic Plan 2015-2020 was updated July 2017. This is presented for your review and discussion. DRAFT Yupiit School District Strategic Plan 2015-2020: Updated July 2017 Mission Statement: To educate all children to be successful in any environment Vision Statement (new draft): All members of the community have pride and commitment in our school system. Students have a positive learning environment, speak the Yupiaq language, know their culture, attend school regularly and graduate prepared to be successful in any environment. The majority of our teachers and school staff are Yupik and speak their language, and the curriculum and instruction is based in Yupik values and traditions. Our community members, elders, parents, and students feel ownership in our schools. Values (taken from Yu’pik values posted in Yupiit schools): Love for Children Spirituality Sharing Humility Hard worK Respect for Others Cooperation Family Roles Knowledge of family tree Hunter Success Domestic Skills Knowledge of Language Avoid conflict Humor Respect for nature Respect For Land Respect For Nature DRAFT Strategic Actions: 1) Students Succeed Culturally and Academically a. Language and Culture: Implement YupiK culture and language curriculum at all grade levels. Develop dual language program. b. Attendance: Increase student attendance at all grade levels. c. Recognition: Establish program to ensure academic, athletic, and artistic student efforts are recognized on a regular basis. d. Academic Progress/Growth: Increase academic progress and growth at all grade levels. -

2018 School District Maintenance Employee Conference - Lakefront Millennium

2018 School District Maintenance Employee Conference - Lakefront Millennium Full Name Email Address Company Title Scott Adams [email protected] Chatham School District Maintenance Judy Anderson [email protected] Yupiit School District Maintenance Director Elliot Anderson [email protected] Bristol Bay School Maintenance Director Edwin Atcherian Sr. [email protected] Kashunamiut School District Maintenance Michael Bartolaba [email protected] Sitka School District Maintenance Director Joshua Blatchley [email protected] Wrangell Public Schools Maintenance Director Wade Boney [email protected] Alaska Gateway School District Maintenance Director Chris Borst [email protected] Anchorage School District Supervisor Randall Brower [email protected] Tanana City School District Facility Supervisor Henry Copsey [email protected] Kake City School Distrtict Maintenance Technician Rick Dallmann [email protected] Southwest Region School District Director of Facilities Gary Eckenweiler [email protected] Bering Strait School District Facilities Director Craig Fredeen [email protected] Cold Climate Engineering, LLC President Charles Furman [email protected] Northwest Arctic Borough School District Computerized Maintenance Program Spec. Christopher Giron [email protected] Southeast Regional Resource Center (SERRC) Facilities Maintenance Management Specialist Steve Graham [email protected] Iditarod Area School District Maintenance Director Darin Hargraves [email protected] Anchorage School District -

State School Year LEA Name School Name Reading Proficiency Target

Elementary/ Middle School Reading Reading Math Math Other School Proficiency Participation Proficiency Participation Academic Graduation School Improvement Status for SY 2007- State Year LEA Name School Name Target Target Target Target Indicator Rate 08 Alaska 2006-07 Alaska Gateway School District 0200050 Walter Northway School 020005000027 Y Y Corrective Action Alaska 2006-07 Anchorage School District 0200180 Avail School 020018000714 N N Corrective Action Alaska 2006-07 Anchorage School District 0200180 William Tyson Elementary 020018000154 X Y Y Corrective Action Alaska 2006-07 Anchorage School District 0200180 Williwaw Elementary 020018000122 Y Y Corrective Action Alaska 2006-07 Anchorage School District 0200180 Willow Crest Elementary 020018000123 Y Y Corrective Action Alaska 2006-07 Bering Strait School District 0200020 Shishmaref School 020002000015 Y X Y Corrective Action Alaska 2006-07 Iditarod Area School District 0200520 Holy Cross School 020052000242 Y Y X Corrective Action Alaska 2006-07 Iditarod Area School District 0200520 Top of the Kuskokwim School 020052000245 Y Y X Corrective Action Alaska 2006-07 Kashunamiut School District 0200005 Chevak School 020000500582 Y Y Corrective Action Alaska 2006-07 Kuspuk School District 0200760 Aniak Jr/Sr High School 020076000663 Y Y Corrective Action Alaska 2006-07 Kuspuk School District 0200760 Jack Egnaty Sr. School 020076000352 Y Y Corrective Action Alaska 2006-07 Lake and Peninsula Borough School District 0200485 Newhalen School 020048500199 Y Y X Corrective Action Alaska 2006-07