Survey of Large-Scale Office Building Market in Tokyo's 23 Cities

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Certified Facilities (Cooking)

List of certified facilities (Cooking) Prefectures Name of Facility Category Municipalities name Location name Kasumigaseki restaurant Tokyo Chiyoda-ku Second floor,Tokyo-club Building,3-2-6,Kasumigaseki,Chiyoda-ku Second floor,Sakura terrace,Iidabashi Grand Bloom,2-10- ALOHA TABLE iidabashi restaurant Tokyo Chiyoda-ku 2,Fujimi,Chiyoda-ku The Peninsula Tokyo hotel Tokyo Chiyoda-ku 1-8-1 Yurakucho, Chiyoda-ku banquet kitchen The Peninsula Tokyo hotel Tokyo Chiyoda-ku 24th floor, The Peninsula Tokyo,1-8-1 Yurakucho, Chiyoda-ku Peter The Peninsula Tokyo hotel Tokyo Chiyoda-ku Boutique & Café First basement, The Peninsula Tokyo,1-8-1 Yurakucho, Chiyoda-ku The Peninsula Tokyo hotel Tokyo Chiyoda-ku Second floor, The Peninsula Tokyo,1-8-1 Yurakucho, Chiyoda-ku Hei Fung Terrace The Peninsula Tokyo hotel Tokyo Chiyoda-ku First floor, The Peninsula Tokyo,1-8-1 Yurakucho, Chiyoda-ku The Lobby 1-1-1,Uchisaiwai-cho,Chiyoda-ku TORAYA Imperial Hotel Store restaurant Tokyo Chiyoda-ku (Imperial Hotel of Tokyo,Main Building,Basement floor) mihashi First basement, First Avenu Tokyo Station,1-9-1 marunouchi, restaurant Tokyo Chiyoda-ku (First Avenu Tokyo Station Store) Chiyoda-ku PALACE HOTEL TOKYO(Hot hotel Tokyo Chiyoda-ku 1-1-1 Marunouchi, Chiyoda-ku Kitchen,Cold Kitchen) PALACE HOTEL TOKYO(Preparation) hotel Tokyo Chiyoda-ku 1-1-1 Marunouchi, Chiyoda-ku LE PORC DE VERSAILLES restaurant Tokyo Chiyoda-ku First~3rd floor, Florence Kudan, 1-2-7, Kudankita, Chiyoda-ku Kudanshita 8th floor, Yodobashi Akiba Building, 1-1, Kanda-hanaoka-cho, Grand Breton Café -

1. 1.1 February 1.2 Conducte 2. 2.1 Between Their Ide 3. 3.1 Will Act 3.2

ISTF/1-IP/1 27/02/12 International Civil Aviation Organization FIRST MEETING OF IONOSPHERIC STUDIES TAKS FORCE (ISTF/1) 27-29 February 2012, Tokayo, Japan MEETING BULLETIN 1. Schedule of meeting 1.1 The opening session of the meeting will be held at 0930 hours on Monday, 27 February 2012 at the Mita Kaigisho, (Mita Conference Hall), Tokyo, Japan. 1.2 The technical tour to Electronic Navigation Research Institute (ENRI) will be conducted from 1000 to 1200 hours on Wednesday, 29 February 2012. 2. Registration of participants 2.1 Participants are requested to register at the Registration Desk of the Mita Kaigisho between 0915 - 0930 hours on the opening day of the meeting. Participants are also requested to wear their identification badge all the time inside the Mita Kaigisho. 3. Officers and Secretariat concerned with the meeting 3.1 Mr. Sujan K. Saraswati, Regional Officer CNS of the ICAO Asia and Pacific Office will act as Secretary of the meeting. His contact address is as follows: Mr. Sujan K. Saraswati, Regional Officer CNS Tel: +66 (2) 537 8189 to 97 Ext. 155 Fax: +66 (2) 537 8199 E-mail: [email protected] 3.2 The daily meeting service is the responsibility of Dr. Susumu Saito. Dr. Saito will provide secretarial support. The contact address is as follows: Dr. Susumu Saito, Senior Researcher, CNS Department Electronic Navigation Research Institute (ENRI) Tel: +81 422 413 191 Fax: +81 422 413 199 E-mail: [email protected] 4. Meeting documents for distribution 4.1 Participants wishing to make presentations or present papers for distribution during the meeting are requested to submit electronic copies to the Secretariat as early as possible, and preferably no later than 13 Febrruary 2012 at the following email addresses: [email protected] and cc: [email protected] ISTF/1-IP/1 -2- 27/02/12 5. -

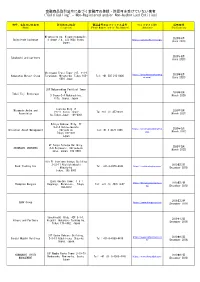

金融商品取引法令に基づく金融庁の登録・許認可を受けていない業者 ("Cold Calling" - Non-Registered And/Or Non-Authorized Entities)

金融商品取引法令に基づく金融庁の登録・許認可を受けていない業者 ("Cold Calling" - Non-Registered and/or Non-Authorized Entities) 商号、名称又は氏名等 所在地又は住所 電話番号又はファックス番号 ウェブサイトURL 掲載時期 (Name) (Location) (Phone Number and/or Fax Number) (Website) (Publication) Miyakojima-ku, Higashinodamachi, 2020年6月 SwissTrade Exchange 4-chōme−7−4, 534-0024 Osaka, https://swisstrade.exchange/ (June 2020) Japan 2020年6月 Takahashi and partners (June 2020) Shiroyama Trust Tower 21F, 4-3-1 https://www.hamamatsumerg 2020年6月 Hamamatsu Merger Group Toranomon, Minato-ku, Tokyo 105- Tel: +81 505 213 0406 er.com/ (June 2020) 0001 Japan 28F Nakanoshima Festival Tower W. 2020年3月 Tokai Fuji Brokerage 3 Chome-2-4 Nakanoshima. (March 2020) Kita. Osaka. Japan Toshida Bldg 7F Miyamoto Asuka and 2020年3月 1-6-11 Ginza, Chuo- Tel:+81 (3) 45720321 Associates (March 2021) ku,Tokyo,Japan. 104-0061 Hibiya Kokusai Bldg, 7F 2-2-3 Uchisaiwaicho https://universalassetmgmt.c 2020年3月 Universal Asset Management Chiyoda-ku Tel:+81 3 4578 1998 om/ (March 2022) Tokyo 100-0011 Japan 9F Tokyu Yotsuya Building, 2020年3月 SHINBASHI VENTURES 6-6 Kojimachi, Chiyoda-ku (March 2023) Tokyo, Japan, 102-0083 9th Fl Onarimon Odakyu Building 3-23-11 Nishishinbashi 2019年12月 Rock Trading Inc Tel: +81-3-4579-0344 https://rocktradinginc.com/ Minato-ku (December 2019) Tokyo, 105-0003 Izumi Garden Tower, 1-6-1 https://thompsonmergers.co 2019年12月 Thompson Mergers Roppongi, Minato-ku, Tokyo, Tel: +81 (3) 4578 0657 m/ (December 2019) 106-6012 2019年12月 SBAV Group https://www.sbavgroup.com (December 2019) Sunshine60 Bldg. 42F 3-1-1, 2019年12月 Hikaro and Partners Higashi-ikebukuro Toshima-ku, (December 2019) Tokyo 170-6042, Japan 31F Osaka Kokusai Building, https://www.smhpartners.co 2019年12月 Sendai Mubuki Holdings 2-3-13 Azuchi-cho, Chuo-ku, Tel: +81-6-4560-4410 m/ (December 2019) Osaka, Japan. -

TOKYO TRAIN & SUBWAY MAP JR Yamanote

JR Yamanote Hibiya line TOKYO TRAIN & SUBWAY MAP Ginza line Chiyoda line © Tokyo Pocket Guide Tozai line JR Takasaka Kana JR Saikyo Line Koma line Marunouchi line mecho Otsuka Sugamo gome Hanzomon line Tabata Namboku line Ikebukuro Yurakucho line Shin- Hon- Mita Line line A Otsuka Koma Nishi-Nippori Oedo line Meijiro Sengoku gome Higashi Shinjuku line Takada Zoshigaya Ikebukuro Fukutoshin line nobaba Todai Hakusan Mae JR Joban Asakusa Nippori Line Waseda Sendagi Gokokuji Nishi Myogadani Iriya Tawara Shin Waseda Nezu machi Okubo Uguisu Seibu Kagurazaka dani Inaricho JR Shinjuku Edo- Hongo Chuo gawa San- Ueno bashi Kasuga chome Naka- Line Higashi Wakamatsu Okachimachi Shinjuku Kawada Ushigome Yushima Yanagicho Korakuen Shin-Okachi Ushigome machi Kagurazaka B Shinjuku Shinjuku Ueno Hirokoji Okachimachi San-chome Akebono- Keio bashi Line Iidabashi Suehirocho Suido- Shin Gyoen- Ocha Odakyu mae Bashi Ocha nomizu JR Line Yotsuya Ichigaya no AkihabaraSobu Sanchome mizu Line Sendagaya Kodemmacho Yoyogi Yotsuya Kojimachi Kudanshita Shinano- Ogawa machi Ogawa Kanda Hanzomon Jinbucho machi Kokuritsu Ningyo Kita Awajicho -cho Sando Kyogijo Naga Takebashi tacho Mitsu koshi Harajuku Mae Aoyama Imperial Otemachi C Meiji- Itchome Kokkai Jingumae Akasaka Gijido Palace Nihonbashi mae Inoka- Mitsuke Sakura Kaya Niju- bacho shira Gaien damon bashi bacho Tameike mae Tokyo Line mae Sanno Akasaka Kasumi Shibuya Hibiya gaseki Kyobashi Roppongi Yurakucho Omotesando Nogizaka Ichome Daikan Toranomon Takaracho yama Uchi- saiwai- Hachi Ebisu Hiroo Roppongi Kamiyacho -

Guideline for Community Development

Peripheral Area of Tamachi Station West Exit/Fudanotsuji Crossing Guideline for Community Development February 2013 Minato City The community, from Edo to Tokyo, continues creating a future where comfortable and active living blends in with bustling streets, bringing splendid harmony Greetings, The peripheral area of Tamachi Station West Exit/Fudanotsuji Crossing (hereinafter referred to as “the District”) used to be an area with a place called “Fudanotsuji” where there was a place to post a notice board called “kosatsuba,” and functioned as the main entrance of Edo City. In this area, there was also a kurayashiki (warehouse-residence) of Satsuma domain where Ta- kamori Saigo and Kaishu Katsu had an interview for negotiating the bloodless surrender of Edo Castle. As time goes by after the Edo Period, the District and its surrounding areas have experienced various changes in the community; firstly, a number of educational and academic institutions were built, factories which supported the living of the residents were built afterwards, and now the community has become a business-oriented area. In the meantime, we have a great city- scape with rich greenery on the hilltop of Takanawa, as well as a bustling shopping street full of vitality. The District, along with the peripheral area of Tamachi Station East Exit, is designated as a national “Area to be Emergently Developed for Specified City Reproduction,” and expected to form a new hub district where a variety of functions are integrated in order to strengthen Tokyo’s global competitiveness. Taking this opportunity to promote future reconstruction in Minato City, we have prepared the “Peripheral area of Tamachi Station West/Fudanotsuji Crossing Guideline for Community De- velopment” as a manual in order to solve problems and to develop a comfortable and attractive community. -

A Student Study Abroad Survival Guide University of Rhode Island Japanese International Engineering Program

A Student Study Abroad Survival Guide University of Rhode Island Japanese International Engineering Program Table of Contents Pre-Departure Preparation……………………………………………………………2-6 Academic Year …………………………………………………………………. 2 Course Requirements………………………………………………………….. 2 Timeline for Preparing for your Year Abroad ……………………………… 2 Scholarships ………………………………………………………………….... 2 Additional Japanese Language Study Opportunities………..……………… 3 Visa Process……………………………………………….…………………….3 Summer ………………………………………………………………………...4 Travel……………….………………………………………………….. 4 Packing ………………………………………………………………… 5 Banking and Money ………………………………………………….. 6 Year Abroad …………………………………………………………………………... 7 Things to do upon arrival …………………………………………………….. 7 Leaving the Airport ………………………………………………….. 7 Establish Residency …………………………………………………… 8 Housing............………………………………………………………… 8 Communication and Cell Phones ……………………………………. 8 Banking ………………………………………………………………... 8 Orientation …………………………………………………………………….. 9 Life in Tokyo ………………………………………………………………….. 9 Transportation ……………………………………………………….. 10 Groceries ……………………………………………………………… 10 Nightlife ………………………………………………………………. 11 Day Trips ……………………………………………………………… 11 Cultural Integration ………………………………………………… 11 Health and Safety Tips…………………………………………... …………...12 Academics ……………………………………………………………………... 12 Internships ...…………………………………………………………………... 13 After Returning ……………………………………………………………………….. 14 Sharing Your Experiences! …………………………………………………... 14 Pre-departure Preparation This Survival Guide has been developed and maintained by students -

YOUR DONATION to PHCA Ashland Bellsouth Corp

Argonaut Group. Bass, Berry and Sims, PLC Butler Manufacturing Co. Ariel Capital Management Baxter International Cadence Design Systems Aristokraft Bay Networks Calex Manufacturing Co. Arkema BEA Systems Calpine, Corp. Armstrong World Industries Bechtel Group CambridgeSoft Armtek, Corp. Becton Dickinson and Co. Campbell Soup Foundation Arrow Electronics Belden Wire and Cable Co. Canadian Pacific Railway YOUR DONATION to PHCA Ashland BellSouth Corp. Capital Group Cos. Aspect Telecommunications Bemis Co. Capital One Services Companies with Matching Gift Programs Associates Corp. of North BeneTemps Cardinal Health (contact your HR Dept. for instructions) America L.M. Berry and Co. Cargill Assurant Health BHP Minerals International Carnegie Corp. of New York Astoria Federal Savings Binney and Smith Castrol North America AAI Corp. Amerada Hess Corp. AstraZenca Bituminous Casualty Corp. Carson Products Co. Abbott Laboratories Ameren Corp. AT&T Black and Decker Corp. Catalina Marketing, Corp. ABN AMBRO North American Electric Power Atlantic City Electric Co. Blount Foundation Catepillar America American Express Co. Atlantic Data Services Blue Bell Central Illinois Light Co. Accenture American General Corp. Autodest BMC Industries Chesapeake Corp. ACF Industries American Honda Motor Corp. Automatic Data Processing BMO Financial Group, US ChevronTexaco Corp. Acuson American International Group AVAYA BOC Group Chicago Mercantile Exchange ADC Telecommunications American National Bank Avery Dennison, Corp. Boeing Co. Chicago Title and Trust Co. Addison Weley Longman American Optical Corp. Avon Products Bonneville International Corp. Chicago Tribune Co. Adobe Systems American Standard AXA Financial Borden Family of Cos. Chiquita Brands International Advanced Micro Devices American States Insurance Baker Hughes Boston Gear Chubb and Sone AEGON USA American Stock Exchange Ball Corp. -

Real Estate Sector 4 August 2015 Japan

Deutsche Bank Group Markets Research Industry Date Real estate sector 4 August 2015 Japan Real Estate Yoji Otani, CMA Akiko Komine, CMA Research Analyst Research Analyst (+81) 3 5156-6756 (+81) 3 5156-6765 [email protected] [email protected] F.I.T.T. for investors Last dance Bubbles always come in different forms With the big cliff of April 2017 in sight, enjoy the last party like a driver careening to the cliff's brink. Japan is now painted in a completely optimistic light, with the pessimism which permeated Japan after the Great East Japan Earthquake in 2011 forgotten and expectations for the 2020 Tokyo Olympics riding high. The bank lending balance to the real estate sector is at a record high, and we expect bubble-like conditions in the real estate market to heighten due to increased investment in real estate to save on inheritance taxes. History repeats itself, but always in a slightly different form. We have no choice but to dance while the dance music continues to play. ________________________________________________________________________________________________________________ Deutsche Securities Inc. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 124/04/2015. Deutsche Bank Group Markets Research Japan Industry Date 4 August 2015 Real Estate Real estate sector FITT Research Yoji Otani, CMA Akiko Komine, CMA Research Analyst Research Analyst Last dance (+81) 3 5156-6756 (+81) 3 5156-6765 [email protected] [email protected] Bubbles always come in different forms Top picks With the big cliff of April 2017 in sight, enjoy the last party like a driver Mitsui Fudosan (8801.T),¥3,464 Buy careening to the cliff's brink. -

Shanghai, China Overview Introduction

Shanghai, China Overview Introduction The name Shanghai still conjures images of romance, mystery and adventure, but for decades it was an austere backwater. After the success of Mao Zedong's communist revolution in 1949, the authorities clamped down hard on Shanghai, castigating China's second city for its prewar status as a playground of gangsters and colonial adventurers. And so it was. In its heyday, the 1920s and '30s, cosmopolitan Shanghai was a dynamic melting pot for people, ideas and money from all over the planet. Business boomed, fortunes were made, and everything seemed possible. It was a time of breakneck industrial progress, swaggering confidence and smoky jazz venues. Thanks to economic reforms implemented in the 1980s by Deng Xiaoping, Shanghai's commercial potential has reemerged and is flourishing again. Stand today on the historic Bund and look across the Huangpu River. The soaring 1,614-ft/492-m Shanghai World Financial Center tower looms over the ambitious skyline of the Pudong financial district. Alongside it are other key landmarks: the glittering, 88- story Jinmao Building; the rocket-shaped Oriental Pearl TV Tower; and the Shanghai Stock Exchange. The 128-story Shanghai Tower is the tallest building in China (and, after the Burj Khalifa in Dubai, the second-tallest in the world). Glass-and-steel skyscrapers reach for the clouds, Mercedes sedans cruise the neon-lit streets, luxury- brand boutiques stock all the stylish trappings available in New York, and the restaurant, bar and clubbing scene pulsates with an energy all its own. Perhaps more than any other city in Asia, Shanghai has the confidence and sheer determination to forge a glittering future as one of the world's most important commercial centers. -

Kagurazaka Campus 1-3 Kagurazaka,Shinjuku-Ku,Tokyo 162-8601

Tokyo University of Science Kagurazaka Campus 1-3 Kagurazaka,Shinjuku-ku,Tokyo 162-8601 Located 3 minutes’ walk from Iidabashi Station, accessible via the JR Sobu Line, the Tokyo Metro Yurakuchom, Tozai and Namboku Lines, and the Oedo Line. ACCESS MAP Nagareyama- Unga Otakanomori Omiya Kasukabe Noda Campus 2641 Yamazaki, Noda-shi, Chiba Prefecture 278-8510 Kanamachi Kita-Senju Akabane Tabata Keisei-Kanamachi Ikebukuro Nishi- Keisei-Takasago Nippori Katsushika Campus 6-3-1 Niijuku, Katsushika-ku, Nippori Oshiage Tokyo 125-8585 Asakusa Ueno Iidabashi Ochanomizu Shinjuku Kinshicho Akihabara Asakusabashi Kagurazaka Campus Kanda 1-3 Kagurazaka, Shinjuku-ku, Tokyo 162-8601 Tokyo ■ From Narita Airport Take the JR Narita Express train to Tokyo Station. Transfer to the JR Yamanote Line / Keihin-Tohoku Line and take it to Akihabara Station. Transfer to the JR Sobu Line and take it to Iidabashi Station. Travel time: about 1 hour 30 minutes. ■ From Haneda Airport Take the Tokyo Monorail Line to Hamamatsucho Station. Transfer to the JR Yamanote Line / Keihin-Tohoku Line and take it to Akihabara Station. Transfer to the JR Sobu Line and take it to Iidabashi Station. Travel time: about 45 minutes. ■ From Tokyo Station Take the JR Chuo Line to Ochanomizu Station. Transfer to the JR Sobu Line and take it to Iidabashi Station. Travel time: about 10 minutes. ■ From Shinjuku Station Take the JR Sobu Line to Iidabashi Station. Travel time: about 12 minutes. Building No.10 Building No.11 Annex Building No.10 Building No.5 CAMPUS MAP Annex Kagurazaka Buildings For Ichigaya Sta. Building No.11 Building No.12 Building No.1 1 Building No.6 Building No.8 Building Building No.13 Building Building (Morito Memorial Hall) No.7 No.2 No.3 3 1 The Museum of Science, TUS (Futamura Memorial Hall) & Building Mathematical Experience Plaza No.9 2 2 Futaba Building (First floor: Center for University Entrance Examinations) Tokyo Metro Iidabashi Sta. -

Tokyo Sightseeing Route

Mitsubishi UUenoeno ZZoooo Naationaltional Muuseumseum ooff B1B1 R1R1 Marunouchiarunouchi Bldg. Weesternstern Arrtt Mitsubishiitsubishi Buildinguilding B1B1 R1R1 Marunouchi Assakusaakusa Bldg. Gyoko St. Gyoko R4R4 Haanakawadonakawado Tokyo station, a 6-minute walk from the bus Weekends and holidays only Sky Hop Bus stop, is a terminal station with a rich history KITTE of more than 100 years. The “Marunouchi R2R2 Uenoeno Stationtation Seenso-jinso-ji Ekisha” has been designated an Important ● Marunouchi South Exit Cultural Property, and was restored to its UenoUeno Sta.Sta. JR Tokyo Sta. Tokyo Sightseeing original grandeur in 2012. Kaaminarimonminarimon NakamiseSt. AASAHISAHI BBEEREER R3R3 TTOKYOOKYO SSKYTREEKYTREE Sttationation Ueenono Ammeyokoeyoko R2R2 Uenoeno Stationtation JR R2R2 Heeadad Ofccee Weekends and holidays only Ueno Sta. Route Map Showa St. R5R5 Ueenono MMatsuzakayaatsuzakaya There are many attractions at Ueno Park, ● Exit 8 *It is not a HOP BUS (Open deck Bus). including the Tokyo National Museum, as Yuushimashima Teenmangunmangu The shuttle bus services are available for the Sky Hop Bus ticket. well as the National Museum of Western Art. OkachimachiOkachimachi SSta.ta. Nearby is also the popular Yanesen area. It’s Akkihabaraihabara a great spot to walk around old streets while trying out various snacks. Marui Sooccerccer Muuseumseum Exit 4 ● R6R6 (Suuehirochoehirocho) Sumida River Ouurr Shhuttleuttle Buuss Seervicervice HibiyaLine Sta. Ueno Weekday 10:00-20:00 A Marunouchiarunouchi Shuttlehuttle Weekend/Holiday 8:00-20:00 ↑Mukojima R3R3 TOKYOTOKYO SSKYTREEKYTREE TOKYO SKYTREE Sta. Edo St. 4 Front Exit ● Metropolitan Expressway Stationtation TOKYO SKYTREE Kaandanda Shhrinerine 5 Akkihabaraihabara At Solamachi, which also serves as TOKYO Town Asakusa/TOKYO SKYTREE Course 1010 9 8 7 6 SKYTREE’s entrance, you can go shopping R3R3 1111 on the first floor’s Japanese-style “Station RedRed (1 trip 90 min./every 35 min.) Imperial coursecourse Theater Street.” Also don’t miss the fourth floor Weekday Asakusa St. -

Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16

Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16:57:32 Desc Main Document Page 1 of 137 Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16:57:32 Desc Main Document Page 2 of 137 Exhibit A Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16:57:32 Desc Main Document Page 3 of 137 Exhibit A1 Served via Overnight Mail Name Attention Address 1 Address 2 City State Zip Country Aastha Broadcasting Network Limited Attn: Legal Unit213 MezzanineFl Morya LandMark1 Off Link Road, Andheri (West) Mumbai 400053 IN Abs Global LTD Attn: Legal O'Hara House 3 Bermudiana Road Hamilton HM08 BM Abs-Cbn Global Limited Attn: Legal Mother Ignacia Quezon City Manila PH Aditya Jain S/O Sudhir Kumar Jain Attn: Legal 12, Printing Press Area behind Punjab Kesari Wazirpur Delhi 110035 IN AdminNacinl TelecomunicacionUruguay Complejo Torre De Telecomuniciones Guatemala 1075. Nivel 22 HojaDeEntrada 1000007292 5000009660 Montevideo CP 11800 UY Advert Bereau Company Limited Attn: Legal East Legon Ars Obojo Road Asafoatse Accra GH Africa Digital Network Limited c/o Nation Media Group Nation Centre 7th Floor Kimathi St PO Box 28753-00100 Nairobi KE Africa Media Group Limited Attn: Legal Jamhuri/Zaramo Streets Dar Es Salaam TZ Africa Mobile Network Communication Attn: Legal 2 Jide Close, Idimu Council Alimosho Lagos NG Africa Mobile Networks Cameroon Attn: Legal 131Rue1221 Entree Des Hydrocarbures Derriere Star Land Hotel Bonapriso-Douala Douala CM Africa Mobile Networks Cameroon Attn: Legal BP12153 Bonapriso Douala CM Africa Mobile Networks Gb,