MT BMO Covers

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Master Thesis Innovation Sciences

Eindhoven University of Technology MASTER Financial technology innovation in the financial services industry of Vancouver B.C. Baltissen, J. Award date: 2017 Link to publication Disclaimer This document contains a student thesis (bachelor's or master's), as authored by a student at Eindhoven University of Technology. Student theses are made available in the TU/e repository upon obtaining the required degree. The grade received is not published on the document as presented in the repository. The required complexity or quality of research of student theses may vary by program, and the required minimum study period may vary in duration. General rights Copyright and moral rights for the publications made accessible in the public portal are retained by the authors and/or other copyright owners and it is a condition of accessing publications that users recognise and abide by the legal requirements associated with these rights. • Users may download and print one copy of any publication from the public portal for the purpose of private study or research. • You may not further distribute the material or use it for any profit-making activity or commercial gain Financial technology innovation in the financial services industry of Vancouver B.C. A thesis submitted in fulfilment of the degree: Master of Science, Innovation Sciences Jip Baltissen Supervisors Eindhoven University of Technology Faculty of Industrial Engineering and Innovation Sciences Dr. Bert M. Sadowski Dr. Z.O. Nomaler Prof. dr. F. Alkemade Consulate-General of the Kingdom of the Netherlands Economic department in Vancouver B.C. Canada Barry Nieuwenhuijs – Deputy Consul General Maarten den Ouden – Trade Officer Eindhoven, August 2017 1 Preface From the end of January 2017 until June 2017, I did an internship for five months at the Consulate- General of the Kingdom of the Netherlands in Vancouver B.C., Canada. -

CCAB-AR-2013-FINAL.Pdf

ANNUAL REPORT | 2013 The Resource Sector: Engine of Opportunity powered by ENGAGEMENT & EQUITABLE PARTNERSHIPS 2 MISSION BOARD OF DIRECTORS To foster sustainable business relations between First Nations, Inuit and Métis people and Co-Chair, Ron Jamieson, Corporate Director Co-Chair, Erin Meehan, ESS North America Canadian Business. Treasurer, John Dutschek, Dutschek & Company Chartered Accountants Secretary, Kara Flynn, Syncrude Canada Ltd. VISION To be the recognized source on commercial James Blackman (incoming), Primco Dene Group of Companies opportunities between First Nations, Inuit and Scott Bonikowsky, Tim Hortons Inc. Métis people and Canadian Business. Bonnie Boretsky, Canada Post Corporation Arden Buskell (outgoing), First Nations Bank Tammy Charland-McLaughlin (outgoing), Primco Dene Group of Companies CORE VALUES Stephen Fay, BMO Bank of Montreal • Respect for First Nation, Inuit and Métis cultures Maxime Faille (incoming), Gowlings Michael Fox, Fox High Consulting • Maintain a high standard of business ethics Leanne Hall (incoming), Noront Resources Ltd. • Develop open, honest and transparent Candice Holmstrom, CH Designs Pat Horgan, IBM Canada Ltd. relationships with all stakeholders Dean Johnson, Sodexo Canada Michael Ledgett (incoming), Dentons Canada LLP Stephen Lindley, SNC-Lavalin Group Inc. The Canadian Council for Aboriginal Business (CCAB) was founded Gary Merasty (outgoing), Cameco Corporation in 1984 by a small group of visionary business and community leaders Randy Moore (incoming), committed to the full participation of Aboriginal peoples in the Bee-Clean Building Maintenance Canadian economy. A national non-profit organization, CCAB offers Howard L. Morry, Pitblado Law Clayton Norris, MNP LLP knowledge, resources, and programs to both Aboriginal owned Jacques Plante, Nasittuq Corporation member companies and Canadian Business that foster economic Paul Summers, SteelCraft Inc. -

Depreciation Report and Insurance Appraisal Specified Property Of

DEPRECIATION REPORT AND INSURANCE APPRAISAL SPECIFIED PROPERTY OF: Strata Plan VAS2893 767 North Road Gibsons, BC Prepared by: Pacific Rim Appraisals Ltd. 550-2950 Douglas Street Victoria, BC V8T 4N5 and #2-57 Skinner Street Nanaimo, BC V9R 5G9 PREMISE OF VALUE AND EFFECTIVE DATE Depreciation Report with 3 Models – April 1, 2013 (Next Fiscal Year) Replacement Cost New for Insurance Purposes – February 16, 2013 Strata Council for VAS2893 February 22, 2013 767 North Road Gibsons, BC To Whom It May Concern: RE: 26 Unit Strata Complex located at 767 North Road, Gibsons, B.C. Strata Plan VAS2893 As requested, we have completed a depreciation report estimate for the improvements utilizing the most recent data available. The effective date of the depreciation report is based on an inspection date of January 5, 2013. The date of next fiscal year of April 1, 2013 is the effective start date for the study. The table below contains Pacific Rim Appraisals Ltd. recommended schedule of payments for the next three years. Failure to follow the proposed schedule of payments may result in inadequate reserve funds or require the use of special levy in the future which is against the intent of the legislation. Model No. 1 Funding based on current contribution of $2,500 increased by multi-family construction inflation only currently estimated at 2.2%. Special levies would be required in years 2018 to 2043. Model Not Recommended by Pacific Rim Appraisals Ltd. Yr. 2013 Yr. 2014 Yr. 2015 Yr. 2016 Year 2017 to 2043 $2,500 $2,555 $2,611 $2,727 See Page 8 of Model 1 Model No. -

Ads Canadian Bank 343 Amex Bank of Canada 303 Bank of America National Association 241 Bank of Canada 177 Bank O

SECTION I NUMERIC LIST / LISTE NUMÉRIQUE 1 ADS CANADIAN BANK 343 Routing Numbers / Numéros d'acheminement Electronic Paper(MICR) Électronique Papier(MICR) Postal Address - Addresse postale 034300012 00012-343 20 Queen Street West - Suite 2600, Toronto, ON M5H 3R3 034300092 00092-343 20 Queen Street West - Suite 2600, Toronto, ON M5H 3R3 AMEX BANK OF CANADA 303 Routing Numbers / Numéros d'acheminement Electronic Paper(MICR) Électronique Papier(MICR) Postal Address - Addresse postale 030300012 00012-303 101 McNabb Street, Markham, ON L3R 4H8 030300022 00022-303 101 McNabb Street, Markham, ON L3R 4H8 030300032 00032-303 101 McNabb Street, 101 McNabb Street, Markham, ON L3R 4H8 BANK OF AMERICA NATIONAL ASSOCIATION 241 Routing Numbers / Numéros d'acheminement Electronic Paper(MICR) Électronique Papier(MICR) Postal Address - Addresse postale 024101312 01312-241 Main Branch, 200 Front St. W., Suite 2700, Toronto, ON M5V 3L2 024156792 56792-241 Main Branch, 200 Front St. W., Suite 2700, Toronto, ON M5V 3L2 BANK OF CANADA 177 Routing Numbers / Numéros d'acheminement Electronic Paper(MICR) Électronique Papier(MICR) Postal Address - Addresse postale 017700000 00000-177 Banking Services, 245 Sparks Street, Ottawa, ON K1A 0G9 017700006 00006-177 Banking Services, 245 Sparks Street, Ottawa, ON K1A 0G9 BANK OF CHINA (CANADA) 308 Routing Numbers / Numéros d'acheminement Electronic Paper(MICR) Électronique Papier(MICR) Postal Address - Addresse postale 030800012 00012-308 50 Minthorn BLVD-Suite 600, Markham, ON L3T 7X8 030800022 00022-308 Toronto Downtown -

Reflections on the Canadian Payments Systems: from Manual Clearing to Electronic Funds Transfers

REFLECTIONS ON THE CANADIAN PAYMENTS SYSTEMS: FROM MANUAL CLEARING TO ELECTRONIC FUNDS TRANSFERS by ALISON L. KIRBY B.A., McGill University, 1981 LL.B., The University of Ottawa, 1987 A THESIS SUBMITTED IN PARTIAL FULFILMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF LAWS in THE FACULTY OF GRADUATE STUDIES (Faculty of Law) We accept this thesis as conforming to the required standard THE UNIVERSITY OF BRITISH COLUMBIA December, 1996 , ©Alison L. Kirby, 1996 In presenting this thesis in partial fulfilment of the requirements for an advanced degree at the University of British Columbia, I agree that the Library shall make it freely available for reference and study. I further agree that permission for extensive copying of this thesis for scholarly purposes may be granted by the head of my department or by his or her representatives. It is understood that copying or publication of this thesis for financial gain shall not be allowed without my written permission. Department of re-cu- ej LCJ^> The University of British Columbia Vancouver, Canada Date \> DE-6 (2/88) 11 ABSTRACT The Canadian payments system encompasses not only those traditional systems which facilitate the processing of paper payment instructions through the Automated Clearing and Settlement System (ACSS) and or the Bank of Canada but those electronic funds transfer (EFT) systems which are capable of processing payment instructions in purely electronic form. Access to the payments system is a key element in the retail and financial services sectors' bid to remain competitive on both national and global scales. Moreover, a complete system of electronic payments will eventually reduce the need for credit cards and, to the extent that it increases the use of deposits for payment purposes, it will reduce the need for currency and cheques as well. -

2018 Winners & Finalists

2018 Finalists 2018-09-24, 521 PM 2018 WINNERS & FINALISTS HRD Canada Magazine in partnership with Ultimate Software would like to congratulate the winners of the 2018 Canadian HR Awards. Winners were revealed live on Thursday, September 20th, 2018 at The Liberty Grand Toronto. QUICK LINKS Best Corporate Social Responsibility Strategy Best Employment & Labour Lawyer (Within a Practice) Best Talent Management Strategy Labour & Employment Law Boutique of the Year Canadian HR Champion (CEO) Canadian HR Rising Star of the Year Canadian HR Team of the Year (Fewer Than 500 Employees) Canadian HR Team of the Year (Finance or Insurance) Canadian HR Team of the Year (Retail or Hospitality) The Accompass Award for Canadian HR Team of the Year (500 Employees or More) The Dentsu Aegis Network Award for Best HR Communication Strategy The Globoforce Award for Best Reward & Recognition Strategy The HRD Readers’ Choice Award For Best Service Provider (100 Staff or More) The HRD Readers’ Choice Award For Best Service Provider (Fewer than 100 Staff) The Ivey Academy Award for Lifetime Achievement in HR Industry The KPMG in Canada Award for HR Leader of the Year The Leadership Agency Award for Woman Of Distinction The MaxSys StaZng & Consulting Award for Most Effective Recruitment Strategy The Mercer Award for Excellence in Diversity & Inclusion The Seneca Award for Best Learning & Development Strategy The TalentEgg Award for Best Employer Branding The Ultimate Software Award for Best Workplace Culture The University of Waterloo Award for Best Next Generation -

Strategic Analysis of a Retail Banking Firm

STRATEGIC ANALYSIS OF A RETAIL BANKING FIRM Tracy Tong Bachelor of Commerce, University of British Columbia, 1997 PROJECT SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF BUSINESS ADMINISTRATION In the Faculty of Business Administration O Tracy Tong 2005 SIMON FRASER UNIVERSITY Summer 2005 All rights reserved. This work may not be reproduced in whole or in part, by photocopy or other means, without permission of the author. APPROVAL Name: Tracy Tong Degree: Master of Business Administration Title of Project: Strategic Analysis of a Retail Banking Firm Supervisory Committee: Senior Supervisor Ed Bukszar, Associate Professor Second Reader Neil Abramson, Associate Professor Date Approved: SIMON FRASER UNIVERSITY Partial Copyright Licence The author, whose copyright is declared on the title page of this work, has granted to Simon Fraser University the right to lend this thesis, project or extended essay to users of the Simon Fraser University Library, and to make partial or single copies only for such users or in response to a request from the library of any other university, or other educational institution, on its own behalf or for one of its users. The author has further granted permission to Simon Fraser University to keep or make a digital copy for use in its circulating collection. The author has further agreed that permission for multiple copying of this work for scholarly purposes may be granted by either the author or the Dean of Graduate Studies. It is understood that copying or publication of this work for financial gain shall not be allowed without the author's written permission. -

To the Owners of Bank of Montreal Bank of Montreal Group of Companies

Bank of Montreal Group of Companies 182nd Annual Report 1999 To the Owners of Bank of Montreal Bank of Montreal Group of Companies Bank of Montreal is a diversified financial services company offering a broad range of products and services. These are the companies that serve our clients. Personal and Commercial Client Group Private Client Group Investment Banking Group 2 Chairman’s Message 6 Personal and Commercial Client Group 11 Investment Banking Group 14 Private Client Group 17 Enterprise-Wide Mandates 18 Our Workforce 19 Our Community 20 Management Analysis of Operations 73 Consolidated Financial Statements 100 Corporate Governance 104 Glossary 105 Shareholder Information This is a Report to the millions of people in Canada and around the world whose savings and pensions are invested in shares of Canada’s first bank. You look to your ownership of Bank of Montreal for the financial security you need to help raise your children, build your homes andretireincomfort.AttheBankourgoalistogiveyouatotal return, from dividends and the growth in value of your shares, that will be in the top 25% of investments in comparable North American financial services companies. In an ever more competitive world, achieving that goal means building relationships with our customers that will set new standards of service for them, while maximizing value for our shareholders. In the following pages, you can read about our initiatives and results in 1999, and of how we plan to build on them in the year ahead. Financial Performance: ten consecutive years of.. -

Toronto Financial Services Cluster Review (City Wide)

CITY CLERK Clause embodied in Report No. 3 of the Economic Development and Parks Committee, which was before the Council of the City of Toronto at its regular meeting held on April 23, 24, 25, 26, 27, and its special meeting held on April 30, May 1 and 2, 2001. 1 Toronto Financial Services Cluster Review (City Wide) (City Council at its regular meeting held on April 23, 24, 25, 26, 27, and its special meeting held on April 30, May 1 and 2, 2001, deferred consideration of this Clause to the next regular meeting of City Council scheduled to be held on May 30, 2001.) The Economic Development and Parks Committee recommends the adoption of the following report (March 7, 2001) from the Commissioner of Economic Development, Culture and Tourism: Purpose: The purpose of this report is to present the findings of the Economic Development Division’s review of the Financial Services Cluster (FS). This review recognizes Toronto’s role as the Financial Services Centre of Canada, identifies the challenges facing the industry, recommends strategic directions for encouraging the further growth of the cluster and a process for implementation. Financial Implications and Impact Statement: There are no financial implications resulting from the adoption of this report. Recommendations: It is recommended that: (1) the Federal and Provincial Ministers of Finance and Economic Development be requested to formally recognize Toronto as Canada’s Financial Services Centre given the concentration of the nation’s financial services businesses that are located in the city; (2) Council endorse the Economic Development strategies related to the marketing and promotion, business development, advocacy, competitive intelligence and human resource development of the Financial Services sector as outlined in detail in the attached Financial Services Cluster Review (Attachment No. -

Routing Numbers / Numéros D'acheminement Electronic Paper(MICR) Électronique Papier(MICR) Postal Address - Addresse Postale

SECTION I NUMERIC LIST / LISTE NUMÉRIQUE 1 ADS CANADIAN BANK 343 Routing Numbers / Numéros d'acheminement Electronic Paper(MICR) Électronique Papier(MICR) Postal Address - Addresse postale 034300012 00012-343 20 Queen Street West - Suite 2600, Toronto, ON M5H 3R3 034300092 00092-343 20 Queen Street West - Suite 2600, Toronto, ON M5H 3R3 AMEX BANK OF CANADA 303 Routing Numbers / Numéros d'acheminement Electronic Paper(MICR) Électronique Papier(MICR) Postal Address - Addresse postale 030300012 00012-303 101 McNabb Street, Markham, ON L3R 4H8 030300022 00022-303 101 McNabb Street, Markham, ON L3R 4H8 030300032 00032-303 101 McNabb Street, 101 McNabb Street, Markham, ON L3R 4H8 BANK OF AMERICA NATIONAL ASSOCIATION 241 Routing Numbers / Numéros d'acheminement Electronic Paper(MICR) Électronique Papier(MICR) Postal Address - Addresse postale 024101312 01312-241 Main Branch, 200 Front St. W., Suite 2700, Toronto, ON M5V 3L2 024156792 56792-241 Main Branch, 200 Front St. W., Suite 2700, Toronto, ON M5V 3L2 BANK OF CANADA 177 Routing Numbers / Numéros d'acheminement Electronic Paper(MICR) Électronique Papier(MICR) Postal Address - Addresse postale 017700000 00000-177 Banking Services, 245 Sparks Street, Ottawa, ON K1A 0G9 017700006 00006-177 Banking Services, 245 Sparks Street, Ottawa, ON K1A 0G9 BANK OF CHINA (CANADA) 308 Routing Numbers / Numéros d'acheminement Electronic Paper(MICR) Électronique Papier(MICR) Postal Address - Addresse postale 030800012 00012-308 50 Minthorn BLVD-Suite 600, Markham, ON L3T 7X8 030800022 00022-308 Toronto Downtown -

Most Socially Active Professionals

The World’s Most Socially Active Financial Services Professionals – October 2020 Position Company Name LinkedIN URL Location Size No. Employees on LinkedIn No. Employees Shared (Last 30 Days) % Shared (Last 30 Days) 1 Meu Pé de Bitcoin https://www.linkedin.com/company/49111529 Brazil 201-500 383 275 71.80% 2 Banque PSA Finance https://www.linkedin.com/company/9703673 France 1001-5000 342 224 65.50% 3 HipoGes Iberia https://www.linkedin.com/company/2423768 Spain 501-1000 614 397 64.66% 4 Warren Brasil https://www.linkedin.com/company/10414116 Brazil 201-500 306 142 46.41% 5 Easynvest https://www.linkedin.com/company/856199 Brazil 201-500 493 224 45.44% 6 dLocal https://www.linkedin.com/company/15156062 United States 201-500 264 118 44.70% 7 Galileo Financial Technologies https://www.linkedin.com/company/26606 United States 201-500 304 132 43.42% 8 Pleo https://www.linkedin.com/company/10275909 Denmark 201-500 210 91 43.33% 9 RSM BRASIL (ACAL) https://www.linkedin.com/company/973230 Brazil 501-1000 374 162 43.32% 10 Eagle Strategies, LLC https://www.linkedin.com/company/770585 United States 1001-5000 702 304 43.30% 11 Ualá https://www.linkedin.com/company/16255916 Argentina 201-500 484 202 41.74% 12 Equitable Advisors https://www.linkedin.com/company/14023910 United States 5001-10000 2,991 1,233 41.22% 13 Naranja X https://www.linkedin.com/company/20480199 Argentina 201-500 260 101 38.85% 14 Zoop https://www.linkedin.com/company/2757629 Brazil 201-500 323 122 37.77% 15 Steward Partners Global Advisoryhttps://www.linkedin.com/company/3525767 United States 201-500 234 86 36.75% 16 Grant Thornton Luxembourg https://www.linkedin.com/company/2314033 Luxembourg 201-500 210 76 36.19% 17 WestPac Wealth Partners https://www.linkedin.com/company/3719612 United States 201-500 246 89 36.18% 18 Grupo Recovery https://www.linkedin.com/company/1233529 Brazil 201-500 293 106 36.18% 19 U.S. -

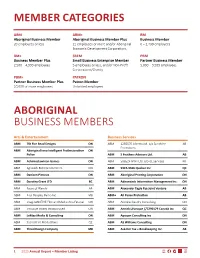

2020 Listing

MEMBER CATEGORIES ABM ABM+ BM Aboriginal Business Member Aboriginal Business Member Plus Business Member 20 employees or less 21 employees or more and/or Aboriginal 6 – 2,499 employees Economic Development Corporations BM+ SBEM PBM Business Member Plus Small Business Enterprise Member Partner Business Member 2,500 – 4,999 employees 5 employees or less, and/or Non-Profit 5,000 – 9,999 employees Corporations/Charity PBM+ PATRON Partner Business Member Plus Patron Member 10,000 or more employees Unlimited employees ABORIGINAL BUSINESS MEMBERS Arts & Entertainment Business Services ABM 7th Fire Bead Designs ON ABM 1255570 Alberta Ltd. o/a Sunshine AB Promotions ABM Aboriginal Innu Intelligent Professionalism ON Police ABM 5 Feathers Advisors Ltd. AB ABM Achimostawinan Games ON ABM 506524 NWT Ltd. o/a GL Services NT ABM Aglukark Entertainment Inc. ON ABM 9324-3566 Quebec Inc QC ABM Denizen Pictures ON ABM Aboriginal Printing Corporation ON ABM Dorothy Grant LTD BC ABM Adirondack Information Management Inc. ON ABM Faces of Wendy AB ABM Alexander Eagle Eye Joint Venture AB ABM+ First Peoples Radio Inc. MB ABM+ All Peace Protection AB ABM imagineNATIVE Film and Media Arts Festival ON ABM Andrew Gaudry Consulting ON ABM Inclusive Voices Incorporated ON ABM Annick Lévesque //7290179 Canada inc QC ABM LeMay Media & Consulting ON ABM Apoqon Consulting Inc ON ABM Sacred Fire Productions QC ABM AS Williams Consulting ON ABM Thred Design Company MB ABM Ask-Her Tax + Bookkeeping Inc. AB 1 2020 Annual Report – Member Listing ABM+ Athabasca Basin Security SK ABM+ IMI Material Handling Logistics Inc. ON ABM Basque Associates Inc.