Kent State University

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Foodie Side of Las Vegas 34 CORPORATE LADDER Groups Flock to the Dining and Entertainment Capital of the World 34 READER SERVICES by Derek Reveron

A COASTAL COMMUNICATIONS CORPORATION PUBLICATION SEPTEMBER/OCTOBER 2014 VOL. 21 NO. 5 $10.00 The Foodie Side of Tom Colicchio Las Vegas American Celebrity Chef Groups Flock to the Founder Craft Restaurant Group Dining and Entertainment Capital of the World Page 26 Credit: © Rayon Richards 2013 Richards © Rayon Credit: 2014 World Class Award Winners Page 10 Caribbean Cachet Page 20 Oceanfront Excellence A landmark since its celebrated opening in 1928, the Ponte Vedra Inn & Club proudly presides as the grand dame of northeast Florida resort hotels. Featured are 250 luxurious rooms and suites, the Atlantic surf, beach, golf, tennis, fitness, spa, fine dining, shopping and a AAA Five-Diamond award for hospitality excellence. Ponte Vedra Beach, Florida • Oceanfront. Just 20 minutes from Jacksonville 888.491.7924 • www.pontevedra.com ISSN 1095-9726 .........................................USPS 012-991 A COASTAL COMMUNICATIONS CORPORATION PUBLICATION SEPTEMBER/OCTOBER 2014 Vol. 21 No. 5 Credit: Alex Alex Karvounis Credit: Page 26 FEATURES Enzo Febbraro, the Naples-born executive chef of Allegro at Wynn Las Vegas, incorporates fresh, 10 World Class imported ingredients in Italian-American favorites. Award Winners DEPARTMENTS 4 PUBLISHER’S MESSAGE DESTINATION 6 INDUSTRY NEWS 7 SNAPSHOTS 20 Caribbean Cache 8 IDEAS Island Incentives That Top Performers Love to Brag About Boost Your Strategic Thinking While Improving By John Buchanan Your Memory of Minutia By Jeff Hurt 26 The Foodie Side of Las Vegas 34 CORPORATE LADDER Groups Flock to the Dining and Entertainment Capital of the World 34 READER SERVICES By Derek Reveron No passport is required to meet in St. John, U.S. -

The Cromwell Las Vegas.Pdf

4493_STA_DLV_11x8.5_book_Cromwell_V1.indd 1 11/30/18 2:53 PM BOLD SOPHISTICATION 4493_STA_DLV_11x8.5_book_Cromwell_V1.indd 2 11/30/18 2:53 PM 4493_STA_DLV_11x8.5_book_Cromwell_V1.indd 3 11/30/18 2:53 PM RETREAT TO LUXURY Our guestrooms and suites mirror modern Parisian loft-style apartments featuring vintage motifs and breathtaking views of the city. 4493_STA_DLV_11x8.5_book_Cromwell_V1.indd 4 11/30/18 2:53 PM Lobby 4493_STA_DLV_11x8.5_book_Cromwell_V1.indd 5 11/30/18 2:53 PM Luxury Room - King 4493_STA_DLV_11x8.5_book_Cromwell_V1.indd 6 11/30/18 2:53 PM ACCOMMODATIONS QUANTITY AMENITIES • 55-inch flat screen TV DELUXE ROOM 360 square feet • One king or two queens 74 rooms • Rain shower • Vanity • 55-inch flat screen TV LUXURY ROOM 360 square feet • One king or two queens 78 rooms • Rain shower • Vanity • Two 55-inch flat screen TVs • Rain shower • Vanity PARLOUR SUITE 723 square feet • Soaking tub 11 rooms • Desk • Living area • Small dining area • Optional connecting room • Two 55-inch flat screen TVs • Rain shower BOULEVARD SUITE 1,061 square feet • Vanity 4 rooms • Soaking tub • Desk • Separate living and dining areas • Small wet bar The Cromwell offers 188 guestrooms and suites. The chart above only features four different room types, but other rooms are available as well. All rooms include the following standard amenities: data ports with high-speed Internet access, phone with voicemail, electronic safe, alarm clock radio, hair dryer, iron and ironing board, On-Demand movies, cable television, 24-hour room service, laundry service, hallway coffee service, and express in-room checkout. 4493_STA_DLV_11x8.5_book_Cromwell_V1.indd 7 11/30/18 2:53 PM FOOD & BEVERAGE Our professional and dedicated staff can help you navigate through our array of options and design a catering plan to suit your event perfectly. -

Fabrication Specification Catalog

Fabrication Specification Catalog Hunter Douglas Hospitality delivers unmatched quality, competitive pricing, and on-schedule delivery on fabricated draperies and bedding. COLLABORATION CONTACT US We have worked hand-in-hand with designers To find a Sales Representative near you, on a wide variety of projects, from hotels, please call us at 800-229-5300 or visit resorts, and casinos to healthcare, retail, and HDhospitality.com restaurant environments, and many other commercial properties. Our portfolio includes some of the world’s most extraordinary interiors. PAGE PRODUCT PAGE PRODUCT 1 . .Project List 15 . .Bedding Specifications 3 . .Drapery Specifications 16 . .Bedspread and Coverlet 5 . .Standard Options 16 . .Top Sheet 6 . .Pinch Pleat 16 . .Duvet 7 . .Ripplefold 18 . .SmartZip Duvet 8 . .Valance 18 . .Bed Scarf 9 . .Cornice 19 . .Bed Skirt 10 . .Shower Curtain 19 . .SmartZip Bed Skirt 11 . .Roman Shades 20 . .Pillows 14 . .Blackout Roman Shades 20 . .Bolsters The Mirage, Las Vegas, NV Project List Over the years, Hunter Douglas Hospitality has proudly built relationships with many hotels and resorts. This is a partial list of where our drapery and fabrication capabilities can be seen. • Aria at City Center, Las Vegas, NV • Hilton, Las Vegas, NV • Paris Hotel & Resort, Las Vegas, NV • Aureole Restaurant, Las Vegas, NV • Holiday Inn Express (nationwide) • Red Rock Hotel & Resort, • Beau Rivage, Biloxi, MS • Home 2 Suites (nationwide) Las Vegas, NV • Bellagio, Las Vegas, NV • Hyatt Place (nationwide) • Sheraton Hotels, Honolulu, Hawaii -

Fourth Floor Conference Space Special Venues

4490_STA_ENT_11x8.5_Book_LINQ_V4.indd 1 1/14/19 10:20 AM SOCIALLY INNOVATIVE 4490_STA_ENT_11x8.5_Book_LINQ_V4.indd 2-3 1/14/19 10:20 AM SOCIALLY INNOVATIVE 4490_STA_ENT_11x8.5_Book_LINQ_V4.indd 2-3 1/14/19 10:20 AM EXCEPTIONAL CONVENIENCE Designed with your social needs in mind, our guestrooms and suites feature cutting-edge technology to always keep you connected. Luxury Room - King 5 4490_STA_ENT_11x8.5_Book_LINQ_V4.indd 4-5 1/14/19 10:20 AM EXCEPTIONAL CONVENIENCE Designed with your social needs in mind, our guestrooms and suites feature cutting-edge technology to always keep you connected. Luxury Room - King 5 4490_STA_ENT_11x8.5_Book_LINQ_V4.indd 4-5 1/14/19 10:20 AM ACCOMMODATIONS QUANTITY AMENITIES • 47-inch flat screen TV • One king, two queens, or two doubles DELUXE ROOM 250-400 square feet • Rain shower 1,853 rooms • Vanity • Desk • 47-inch flat screen TV • One king, two queens, or two doubles LUXURY ROOM 400 square feet • Rain shower 69 rooms • Vanity • Desk • 47 and 55-inch flat screen TVs • Rain shower KING SUITE 600 square feet • Vanity 198 rooms • Desk • Separate living and dining areas • 1 ½ baths • 1 bedroom • Rain shower • Double vanity PENTHOUSE SUITE 1,067 square feet • Desk 2 rooms • Wet bar • Separate living and dining areas • 1 ½ baths The LINQ Hotel & Casino offers 2,252 guestrooms and suites. The chart above only features four different room types, but other rooms are available as well. All rooms include the following standard amenities: data ports with high-speed Internet access, phone with voice mail, electronic safe, alarm clock radio, hair dryer, iron and ironing board, On-Demand Penthouse Suite – Wet Bar movies, cable television, 24-hour room service, laundry service, and express in-room checkout. -

Las Vegas Visitor's Guide

Convention 2019 • June 26–28, 2019 LAS VEGAS VISITOR’S GUIDE 1 TABLE OF CONTENTS Tipping Guide . 3 Transportation . 4. Attractions . 8 For Kids . 11 Sports . 12 Get Outdoors . 13 Welcome to Las Vegas Sign . 15 LGBTQIA+ . 15 Buffet Guide . 16 Recreational Marijuana . 16 Union Casinos . 17 Shopping . 19 2 TIPPING GUIDE Housekeeper $5 minimum per day; leave a note so the housekeepers know it’s for them; tip more for suites. Bellman $3-$5 per bag; tip higher end for heavy luggage (for check in and check out); $20 for full bell cart Server 20% of bill Buffet Service/Banquet 10% Server Bartender/ 20% of tab Cocktail Server Valet $2-$5; tip when car is returned Shuttle Drivers $1-$2 per person or $4-$5 per party Taxis 15-20% of fare Restroom Attendant $1-$3 Skycap/Airport Bag Check In $5 per bag Other Airport Assistance, $5-$10 e.g. pushing a wheelchair Doorman $1-$4 for carrying luggage; $1-$2 for hailing a cab; extra dollar if raining Concierge $5-$10 for tickets or restaurant reservations; $15 for hard to get tickets or reservations Delivery of Special Requests/ $2–$5 per item Items Room Service 20% of bill Dealers $5/hour; can tip in chips Slot Attendants (hand pays) 1% Street Performers $1-$2 Tour Guide $10-$20 Front Desk $10-$20 if they upgrade your room 3 BUS ROUTES ON LAS VEGAS STRIP & DTLV Public transportation is perfect for sightseeing and traveling the Las Vegas strip at your own pace. Vegas Strip & All Access Pass: 2-hours $6.00; 24-hours $8.00; 3-days $20.00 4 5 LAS VEGAS MONORAIL The Las Vegas Monorail has seven stations and travels the entire distance of the Las Vegas Strip. -

Fabrication Specification Catalog

Fabrication Specification Catalog Hunter Douglas Hospitality delivers unmatched quality, competitive pricing, and on-schedule delivery on fabricated draperies and bedding. COLLABORATION CONTACT US We have worked hand-in-hand with designers To find a Sales Representative near you, on a wide variety of projects, from hotels, please call us at 800-229-5300 or visit resorts, and casinos to healthcare, retail, and HDhospitality.com restaurant environments, and many other commercial properties. Our portfolio includes some of the world’s most extraordinary interiors. PAGE PRODUCT PAGE PRODUCT 1 . .Project List 15 . .Bedding Specifications 3 . .Drapery Specifications 16 . .Bedspread and Coverlet 5 . .Standard Options 16 . .Top Sheet 6 . .Pinch Pleat 16 . .Duvet 7 . .Ripplefold 18 . .SmartZip Duvet 8 . .Valance 18 . .Bed Scarf 9 . .Cornice 19 . .Bed Skirt 10 . .Shower Curtain 19 . .SmartZip Bed Skirt 11 . .Roman Shades 20 . .Pillows 14 . .Blackout Roman Shades 20 . .Bolsters The Mirage, Las Vegas, NV Project List Over the years, Hunter Douglas Hospitality has proudly built relationships with many hotels and resorts. This is a partial list of where our drapery and fabrication capabilities can be seen. • Aria at City Center, Las Vegas, NV • Hilton, Las Vegas, NV • Paris Hotel & Resort, Las Vegas, NV • Aureole Restaurant, Las Vegas, NV • Holiday Inn Express (nationwide) • Red Rock Hotel & Resort, • Beau Rivage, Biloxi, MS • Home 2 Suites (nationwide) Las Vegas, NV • Bellagio, Las Vegas, NV • Hyatt Place (nationwide) • Sheraton Hotels, Honolulu, Hawaii -

Domestic Hotels, Resorts & Dmcs

TENEOHG.COM SLEEPING TOTAL MEETING LARGEST MEETING LOCATION HOTELS, RESORTS & DMCs ROOMS SPACE (Indoor) SPACE DOMESTIC HOTELS, RESORTS & DMCS ALASKA MEMBER DMC: CANTRAV SERVICES - PLATINUM DMC COLLECTION ALASKA & CANADA: (VANCOUVER, WHISTLER,TBD BANFF, KELOWNA,TBD TORONTO) TBD GIRDWOOD Alyeska Resort 304TBD 8,000TBD S.F. 3,000TBD S.F. ARIZONA MEMBER DMC: SOUTHWEST CONFERENCE PLANNERS - DMC NETWORK (PHOENIX/SCOTTSDALE, TUCSON,TBD SEDONA, GRAND CANYON)TBD TBD MARICOPA Harrah's Ak-Chin 529TBD 28,350TBD S.F. 18,024TBD S.F. SCOTTSDALE Fairmont Scottsdale Princess 754TBD 156,000TBD S.F. 22,500TBD S.F. SCOTTSDALE Omni Scottsdale Resort & Spa at Montelucia 293TBD 27,000TBD S.F. 9,216TBD S.F. SCOTTSDALE Sanctuary Camelback Mountain Resort & Spa (Paradise Valley) 105TBD 9,000TBD S.F. 5,500TBD S.F. SCOTTSDALE Talking Stick Resort 496TBD 50,000TBD S.F. 24,556TBD S.F. SCOTTSDALE The Scott Resort & Spa 204TBD 14,258TBD S.F. 6,800TBD S.F. SCOTTSDALE The Scottsdale Plaza Resort (Paradise Valley) 404TBD 40,000TBD S.F. 10,000TBD S.F. TUCSON Omni Tucson National Resort 128TBD 10,500TBD S.F. 2,870TBD S.F. CALIFORNIA MEMBER DMC: ARRANGEMENTS UNLIMITED - DMC NETWORK (SAN DIEGO, ORANGE COUNTY, PALM SPRINGS)TBD TBD TBD MEMBER DMC: BIXEL & COMPANY - DMC NETWORK (LOS ANGELES AREA) TBD TBD TBD MEMBER DMC: CAPPA & GRAHAM TERRAMAR - DMC NETWORK (SAN FRANCISCO, NAPA, CARMEL,MONTEREY,TBD SAN JOSE) TBD TBD LAGUNA BEACH Surf & Sand Resort 167TBD 10,000TBD S.F. 2,500TBD S.F. LAGUNA BEACH The Ranch at Laguna Beach 97TBD 6,000TBD S.F. 3,127TBD S.F. LOS ANGELES 1 Hotel West Hollywood (West Hollywood) 285TBD 12,000TBD S.F. -

Nevada Casinos 2019 (Copyright 2019 Jon Friedl LLC) - 2/23/19, 9:15 PM / 1

Nevada Casinos 2019 (Copyright 2019 Jon Friedl LLC) - 2/23/19, 9:15 PM / 1 Nevada Casinos 2019 Casinos in Nevada There are 166 non-tribal casinos and two American Indian tribal casinos in Nevada, the greatest number of casinos to be found in any U.S. state. Once completed in late 2020, the largest casino in Nevada will be the Resorts World Casino Las Vegas in Winchester having 3,250 gaming machines and 250 table games. Construction began in late 2017 on the former site of the Stardust Resort and Casino. The second largest casino is Treasure Island Las Vegas (htps://www.treasureisland.com) having 2,500 gaming machines and 185 table games. Get My Free Report Revealing... Non-Tribal Casinos in Nevada The 166 non-tribal commercial casinos located in Nevada are listed below along with the city they are located. Given certain website limitations for providing the URL of each casino, I have had to create a separate, downloadable List of Nevada Casinos by City (). Without links to their individual webpages, here are the currently open casinos in Nevada organized by city alongside the county they are located within. Amargosa Valley (91 miles northwest of Las Vegas) in Nye County Longstreet Inn Casino and RV Resort Batle Mountain (215 miles northeast of Reno) in Lander County Owl Club Casino & Restaurant Beaty (120 miles northwest of Las Vegas) in Nye County Stagecoach Hotel & Casino Get My Free Report Revealing... Boulder City (22 miles southeast of Las Vegas) in Clark County Hoover Dam Lodge Hotel & Casino Carson City (32 miles south of Reno), -

Harrahslv V4.Pdf

BREAK FROM CONVENTION Valley Tower Room - King STAY IN STYLISH COMFORT Shake up the business world and then retreat into your own sanctuary in one of our guestrooms and suites. Valley Tower Executive Suite Living Room Valley Tower Vice Presidential Suite ACCOMMODATIONS QUANTITY AMENITIES • 49-inch flat screen TV • One king or two queens VALLEY TOWER ROOM 300 square feet • Rain shower 1,400 rooms • Vanity • Desk • 49-inch flat screen TV • One king or two queens MARDI GRAS ROOM 300 square feet • Rain shower 828 rooms • Vanity • Desk • Two 55-inch flat screen TVs • Rain shower VALLEY TOWER 680 square feet • Vanity EXECUTIVE SUITE 119 rooms • Desk • Soaking tub • Living area • 55 and 65-inch flat screen TVs • Rain shower VALLEY TOWER 1,360 square feet • Vanity VICE PRESIDENTIAL SUITE 15 rooms • Desk • Soaking tub • Living area • Separate bar and dining area Harrah’s Las Vegas offers 2,540 guestrooms and suites. The chart above only features four different room types, but other rooms are available as well. All rooms include the following standard amenities: data ports with high-speed internet access, phone with voicemail, electronic safe, alarm clock radio, hair dryer, iron and ironing board, On-Demand movies, cable television, 24-hour room service, laundry service, and express in-room checkout. EXTRAORDINARY MEETINGS With 25,000 square feet of flexible meeting space, Harrah’s Las Vegas delivers friendly and professional service where you are always the center of attention. Nevada Ballroom Nevada Ballroom CORPORATE CONVENTION CENTER At the heart of our facilities is the 12,000-square-foot Nevada Ballroom, which is perfect for large events and can be divided into six individual meeting rooms. -

April 2019 - Announced June 2019 (Because We Give Our Members 30 Days to Report Their Commutes, We Wait Until the End of the Next Month to Draw Our Winners)

April 2019 - Announced June 2019 (Because we give our members 30 days to report their commutes, we wait until the end of the next month to draw our winners). Company Name Winner Name Prize Name AAA Insurance Nkani, Seyram 30 Day Bus Pass Albertsons LLC Leopoldo, Melissa $25 Target Gift Card Alorica- Badura Anguiano, Kristin A. $10 Target Gift Card Alorica- Badura Cebada, Tina $10 Target Gift Card Alorica- Badura Hall, Sheila $10 Target Gift Card Alorica- Pilot Road Gipson, Cierra $10 Target Gift Card Amazon Courtney, Mona $10 Target Gift Card Amazon Sort Center LAS5 Long, Antonio $10 Target Gift Card Aquarius Casino Resort Hermosillo, John $10 Target Gift Card ARIA Aviles, Rosa $10 Target Gift Card ARIA Casillas, Carmen Y. $10 Target Gift Card ARIA Lares, Angelina $10 Target Gift Card ARIA Tara, Liliana $10 Target Gift Card ARIA Vela, Rosaura $50 Walmart Gift Card Arizona Charlies - Boulder Collazo, Roberto $10 Target Gift Card Arizona Charlies - Boulder Barikzi, Ahmed $25 Gas Card Arizona Charlies - Boulder Garo, Rose $25 Target Gift Card Arizona Charlies - Boulder Hernandez, Ramon $25 Target Gift Card Arizona Charlie's - Decatur Casillas, Jeanette $10 Target Gift Card Arizona Charlie's - Decatur Harmon, Angela L. $25 Target Gift Card Ark Las Vegas Restaurant Corporation Cummings, Kala $10 Target Gift Card Asurion Belcher, Unique $10 Target Gift Card Asurion Haynes, Ezra $10 Target Gift Card Asurion Natherne, Kevin $10 Target Gift Card Asurion Wright, Terema $25 Gas Card Bally's Casino Resort Guiza, Victoria $10 Target Gift Card Bellagio Almanzar, Antonio $10 Target Gift Card Bellagio Chinn, Maria $10 Target Gift Card Bellagio Dominguez, Jesus $10 Target Gift Card Bellagio Moreno, Kim $10 Target Gift Card Bellagio Ramirez, Katherine $25 Gas Card Bellagio Cruz, Daniel $25 Target Gift Card Bellagio McBride, Billie $25 Target Gift Card Bellagio Meyers, Al $25 Target Gift Card Bellagio Pereira, Mark S. -

Introduction to Nevada Slot Machine Casino Gambling - 12/27/17, 5:11 PM / 1

Introduction to Nevada Slot Machine Casino Gambling - 12/27/17, 5:11 PM / 1 Nevada Gambling Establishments There are currently 164 casinos in the state of Nevada. The Venetian Las Vegas is the largest casino in Nevada. The second largest casino in Nevada is Red Rock Casino Resort & Spa in Las Vegas. In 2020, once it opens, the Nevada casino expected to have the biggest casino floor will be the Resorts World Casino Las Vegas with 175,000 square feet of gaming space. The Nevada casino reputed to consistently have the best slots payout return statistics in Nevada is located in Downtown Las Vegas at the Rampart Casino. For an alphabetical listing of Nevada casinos, including the district they are located in, please visit the Wikipedia page List of Casinos in Nevada. All current Nevada casinos, listed alphabetically by the city they are located within, are: Amargosa Valley (91 miles northwest of Las Vegas) • Longstreet Inn Casino and RV Resort Batle Mountain (215 miles northeast of Reno) • Owl Club Casino & Restaurant Beaty (120 miles northwest of Las Vegas) • Stagecoach Hotel & Casino Boulder City (22 miles southeast of Las Vegas) • Hoover Dam Lodge Hotel & Casino Carson City (32 miles south of Reno) Introduction to Nevada Slot Machine Casino Gambling - 12/27/17, 5:11 PM / 2 • Carson Nugget Casino Hotel • Casino Fandango • Gold Dust West - Carson City • Max Casino Carson City Elko (289 miles northeast of Reno) • Commercial Casino • Gold Dust West - Elko • Red Lion Hotel & Casino • Stockmen’s Hotel & Casino Ely (317 miles east of Reno) • Hotel -

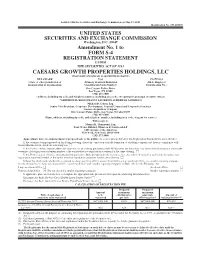

Caesars Growth Properties Holdings

As filed with the Securities and Exchange Commission on May 15, 2015 Registration No. 333-203106 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Amendment No. 1 to FORM S-4 REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 CAESARS GROWTH PROPERTIES HOLDINGS, LLC (Exact name of registrant as specified in its charter) DELAWARE 7993 37-1751234 (State or other jurisdiction of (Primary Standard Industrial (I.R.S. Employer incorporation or organization) Classification Code Number) Identification No.) One Caesars Palace Drive Las Vegas, NV 89109 (702) 407-6000 (Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) *ADDITIONAL REGISTRANTS LISTED ON SCHEDULE A HERETO Michael D. Cohen, Esq. Senior Vice President, Corporate Development, General Counsel and Corporate Secretary Caesars Acquisition Company One Caesars Palace Drive, Las Vegas, Nevada 89109 (702) 407-6000 (Name, address, including zip code, and telephone number, including area code, of agent for service) With a copy to: Monica K. Thurmond, Esq. Paul, Weiss, Rifkind, Wharton & Garrison LLP 1285 Avenue of the Americas New York, New York 10019-6064 (212) 373-3000 Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective. If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ‘ If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.