VII, CBI (AHD SCAM CASES), RANCHI Present: Shiv Pal Singh

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

BJP Leader Said Galwan Valley in Eastern Ladakh Prime Minister Narendra Modi, Accompanied by Roshan”

DAILY EXCELSIOR, JAMMU SATURDAY, OCTOBER 31, 2020 (PAGE 7) PM inaugurates tourism attractions 15th Finance Commission finalises Pak Minister’s admission revealed truth of report, to submit on Nov 9 at Statue of Unity NEW DELHI, Oct 30: The commission will also Pulwama attack, silenced Govt critics: Rajnath KEVADIYA (Guj), Oct 30: 20 emporia, said the govern- children with the underlying present a copy of the report to BHAGALPUR (Bihar), Oct 30: tions," he said. made the supreme sacrifice in the ment release. theme of “Sahi Poshan Desh The 15th Finance Prime Minister Narendra Modi The senior BJP leader said Galwan Valley in eastern Ladakh Prime Minister Narendra Modi, accompanied by Roshan”. Commission will submit its later next month. Defence Minister Rajnath when former prime minister Indira in clashes with Chinese troops to Modi, who is on a two-day report for fiscal years 2021-22 The report, which contains Singh Friday said that a Pakistani Gandhi had divided Pakistan into protect the country. visit to Gujarat, inaugurated to 2025-26 to President Ram recommendations pertaining to Minister’s admission of his two, BJP stalwart late Atal Bihari Moving on to other issues, he four new tourist attractions Nath Kovind on November 9, five financial years, 2021-22 to Country’s involvement in the 2019 Vajpayee had praised her in said the country would have been near the Statue of Unity at an official statement said on 2025-26, will be tabled in Pulwama attack has revealed the Parliament. in a much better position if the Kevadiya in Narmada district Friday. -

03.12.2018 Supplementary List Supplementary List for Today in Continuation of the Advance List Already Circulated

03.12.2018 SUPPLEMENTARY LIST SUPPLEMENTARY LIST FOR TODAY IN CONTINUATION OF THE ADVANCE LIST ALREADY CIRCULATED. THE WEBSITE OF DELHI HIGH COURT IS www.delhihighcourt.nic.in INDEX PRONOUNCEMENT OF JUDGMENTS -----------------> 01 TO 02 REGULAR MATTERS ----------------------------> 01 TO 122 FINAL MATTERS (ORIGINAL SIDE) --------------> 01 TO 13 ADVANCE LIST -------------------------------> 01 TO 95 APPELLATE SIDE (SUPPLEMENTARY LIST)---------> 96 TO 125 APPELLATE SIDE (SUPPLEMENTARY LIST-MID)-----> 126 TO 152 ORIGINAL SIDE (SUPPLEMENTARY I)-------------> 153 TO 160 COMPANY ------------------------------------> 161 TO 162 SECOND SUPPLEMENTARY -----------------------> 163 TO 174 THIRD SUPPLEMENTARY -----------------------> 175 TO 175 MEDIATION CAUSE LIST -----------------------> 01 TO 03 PRE-LOK ADALAT------------------------------> 01 TO 02 NOTE 1. Mentioning of urgent matters will be before Hon'ble DB-I at 10.30 A.M.. DELETIONS 1. FAO(OS)(COMM) 272/2018 listed before Hon'ble DB-II at item No.2 is deleted as the same is fixed for 14.12.2018. 2. FAO(OS) 271/2017 listed before Hon'ble DB-III at item No.11 is deleted as the same is re-registered as FAO(OS)(COM.) 284/2018 and the same is listed before Hon'ble DB-II at item No.41. 3. CO.APPL. 26/2018 listed before Hon'ble DB-V at item No.44 is deleted as the same is returned to Filing Counter. 4. CONT.CAS(C) 688/2018 listed before Hon'ble Mr. Justice Sunil Gaur at item No.32 is deleted as the same is fixed for 05.12.2018. 5. W.P.(C) 12998/2018 listed before Hon'ble Mr. Justice Sunil Gaur at item No.70 is deleted as the same is listed before Hon'ble DB-V. -

A Tribute to Chetan Datar,Bharangam 13 – All the Plays of B

Snake, Love and Sexuality Ravindra Tripathi’s There are a lot of stories in Indian mythology and folklores where you find the snake or the serpent as sexual motif. Some modern plays are also based upon it. For example Girish Karnad’s play Nagmandala. The snake as sexual motif is not limited only to India. In 13th bharat rang mahotsav, the Japanese play Ugetsu Monogatari (directed by Madoka okada) also presents the snake as a charmer and lover of human being. It is story of 10th century Japan. There is a young man, named Toyoo, son of a fisherman. He lives near seashore. A beautiful woman named Manago comes to his home in a rainy night. Toyoo is attracted towards her. He also lends his umbrella and promises to meet her again in near future. After some days he goes to her house on the pretext of going back his umbrella. During that he gets intimate with her. Manago gives him a beautiful sword as a token of their relationship. But after sometime it comes out that the sword was stolen from a shrine. Toyoo is caught by the officials on the charge of theft. He is taken to the house of Manago and there it is discovered that actually Manago is not a woman but a serpent. She transforms herself as a woman to get Toyoo love. Now the question is what will happen of their relationship. Will Toyoo accept Manago, the serpent as his beloved or leave her? Ugetsu monogatari is a play about coexistence of natural and supernatural in human life. -

Here in the United Online Premieres Too

Image : Self- portrait by Chila Kumari Singh Burman Welcome back to the festival, which this Dive deep into our Extra-Ordinary Lives strand with amazing dramas and year has evolved into a hybrid festival. documentaries from across South Asia. Including the must-see Ahimsa: Gandhi, You can watch it in cinemas in London, The Power of The Powerless, a documentary on the incredible global impact of Birmingham, and Manchester, or on Gandhi’s non-violence ideas; Abhijaan, an inspiring biopic exploring the life of your own sofa at home, via our digital the late and great Bengali actor Soumitra Chatterjee; Black comedy Ashes On a site www.LoveLIFFatHome.com, that Road Trip; and Tiger Award winner at Rotterdam Pebbles. Look out for selected is accessible anywhere in the United online premieres too. Kingdom. Our talks and certain events We also introduce a new strand dedicated to ecology-related films, calledSave CARY RAJINDER SAWHNEY are also accessible worldwide. The Planet, with some stirring features about lives affected by deforestation and rising sea levels, and how people are meeting the challenge. A big personal thanks to all our audiences who stayed with the festival last We are expecting a host of special guests as usual and do check out our brilliant year and helped make it one of the few success stories in the film industry. This online In Conversations with Indian talent in June - where we will be joined year’s festival is dedicated to you with love. by Bollywood Director Karan Johar, and rapidly rising talented actors Shruti Highlights of this year’s festival include our inspiring Opening Night Gala Haasan and Janhvi Kapoor, as well as featuring some very informative online WOMB about one woman gender activist who incredibly walks the entire Q&As on all our films. -

7 KHOON MAAF Special 7 SINS FORGIVEN 7 SINS FORGIVEN 7 SINS FORGIVEN

PS-2030:PS_ 30.01.2011 13:53 Uhr Seite 128 Berlinale 2011 Vishal Bhardwaj Panorama 7 KHOON MAAF Special 7 SINS FORGIVEN 7 SINS FORGIVEN 7 SINS FORGIVEN Indien 2011 Darsteller Susanna Anna- Länge 143 Min. Marie Johannes Priyanka Chopra Format 35 mm, Major Edwin Cinemascope Rodriques Neil Nitin Mukesh Farbe Jimmy Stetson John Abraham Wasiullah Khan Irrfan Khan Stabliste Nicolai Vronsky Alexander Regie Vishal Bhardwaj Dychenko Buch Matthew Robbins Keemat Lal Annu Kapoor Vishal Bhardwaj, Modhusudhon nach der Tarafdar Naseeruddin Shah Erzählung „The sowie Konkana Sen Merry Widow“ von Sharma Ruskin Bond Vivaan Shah Kamera Ranjan Palit Usha Uthup Dialoge Vishal Bhardwaj Harish Khanna Schnitt Sreekar Prasad Shashi Malviya Sounddesign P M Satheesh Shajith Koyeri Musik Vishal Bhardwaj Priyanka Chopra Liedtexte Gulzar Production Design Samir Chanda Maske Vikram Gaikwad 7 SINS FORGIVEN Herstellungsltg. Sanjeev Kumar Sechs Ehemänner hat die schöne Susanna gehabt in einem insgesamt 35 Produzenten Ronnie Screwvala Jahre währenden Eheleben. Keiner der Gatten hat die Ehe mit der eleganten, Vishal Bharadwaj attraktiven Frau überlebt – „die lustige Witwe“ hat sie alle zu Tode geliebt! Co-Produzenten Zarina Mehta Der erste in der Reihe war der Major, der sah so schneidig aus in seiner Deven Khote Sidharth Roy Uniform. Vielleicht war er damals schon ein bisschen zu alt für Susanna? Kapur Aber was soll’s! Liebe macht blind. Rekha Bhardwaj Sehr kurz darauf trat sie mit Jimmy vor den Altar. Der sang so schön und sah Executive Producer Ajay Rai so gut aus. Doch letztlich war Jimmy ein unbeschriebenes Blatt … Associate Producers Manish Hariprasad Susanna ist im Grunde ihres Herzens eine Romantikerin und deshalb sehr Vikas Mehta Creative Producer Vikas Bahl empfänglich für Lyrik. -

Sarkar-And-Wolf-Documentary-Acts-Interview-With-Madhusree-Dutta.Pdf

LeadershipRoundtable Insights from Jaina text Saman Suttam 21 BioScope Documentary Acts: 3(1) 21–34 © 2012 Screen South Asia Trust An Interview with SAGE Publications Los Angeles, London, Madhusree Dutta New Delhi, Singapore, Washington DC DOI: 10.1177/097492761100300103 http://bioscope.sagepub.com Bhaskar Sarkar Nicole Wolf Keywords Documentary form and language, citizenship, realism, melodrama and performance, authorship and collaboration, the political The following interview is based on a series of conversations we have had with Madhusree Dutta over the past few years. We condensed the breadth and depth of these stimulating exchanges into five ques- tions which we posed to her via email. The text below is thus both a way of reflecting upon as well as a starting point for further engagements with Dutta’s practice and thinking. Bhaskar Sarkar and Nicole Wolf The trajectory of your work, from your first documentary film I Live in Behrampada (1993), via films such as Memories of Fear (1995) or Scribbles on Akka (2000) to your current curatorial practice for the ongoing large scale research and archival project Cinema City, which developed out of 7 Islands and a Metro (2007), shows a constant search for creative practices and formal languages to respond to your current social and political terrain and the questions of urgency this calls forth. Your relation to the Indian women’s movement and your negotiation with the issues and theoretical concerns coming from feminist thought appear to play a significant role here. This relation was even institutionalized via your co- founding of Majlis in 1990, with the feminist lawyer Flavia Agnes, which brought you close to the realm of rights and maybe even law. -

Pronouncement List File:///C:/Users/Admin/Desktop/Html/2019 09 26 B M.Htm

Pronouncement List file:///C:/Users/Admin/Desktop/html/2019_09_26_b_m.htm FOR ORDERS THE THURSDAY DATED 26/09/2019 CR NO 11 HON'BLE MR. JUSTICE DR. RAVI RANJAN 51 FAO-5558-2019 (OI) ORIENTAL INSURANCE COMPANY LIMITED V/S PRIYA RANI AND ASHWANI TALWAR EKTA THAKUR UT-CHANDIGARH OTHERS CM-18601-CII-2019 ASHWANI TALWAR FOR ORDERS THE THURSDAY DATED 26/09/2019 CR NO 43 HON'BLE MR. JUSTICE HARMINDER SINGH MADAAN 51 FAO-411-2001 (NIC(EG)) LAL SINGH V/S JAGAN AJAY CHAUDHARY , ASHWANI TALWAR , Gaurav Singla , HARKESH MANUJA , GURGAON LALIT GARG , MAHENDRA SINGH TEWATIA , PAUL S SAINI, LALIT GARG , R S HOODA CM-2574-CII-2001 AJAY CHAUDHARY (BO DT. 27.10.16/INCOMPLETE CASE) 52 FAO-1735-2016 (UII (OD)) POOJA BHAATU & ANR V/S RANDHIR SINGH & ANR SANDEEP KOTLA , D.P.GUPTA, R.C.KAPOOR FATEHABAD CM-6505-CII-2016 SANDEEP KOTLA WITH FAO-5671-2016 RANDHIR SINGH V/S VIKRAM AND ORS. SUKHVIR SINGH SAHU , LALIT GARG (INJURY CASE) 53 CM-19135-CII-2019 (UII (OD)) POOJA BHAATU & ANR V/S RANDHIR SINGH & ANR SANDEEP KOTLA D.P. GUPTA (OTHER) FATEHABAD IN FAO-1735-2016 SANDEEP KOTLA , D.P.GUPTA, R.C.KAPOOR 54 CR-1437-2019 (IO) SWARAN DASS V/S CHARAN DASS AND OTHERS S.K. CHOUDHARY (OTHER) GURDASPUR FOR ORDERS THE THURSDAY DATED 26/09/2019 CR NO 52 HON'BLE MR. JUSTICE FATEH DEEP SINGH 51 CRM-M-24327-2019 (RBHCAW) MANDEEP V/S STATE OF HARYANA SAJJAN SINGH A.G. HARYANA ROHTAK URGENT D.B. I MOTION PETITION FOR THE THURSDAY DATED 26/09/2019 CR NO 2 HON'BLE THE ACTING CHIEF JUSTICE HON'BLE MR. -

Trishaan,C.S.A

Trishaan,C.S.A. +919167549854 , +919372625905 [email protected]_____________________________________________________________________ Diploma in acting from Barry john’s IMAGO Acting school P.G Diploma in film making & acting from F.T.I.I., Pune Features: Hotel Mumbai(Casting Director) Producer-Thunder Road Pictures, Julie Ryan, Kent Kubena, John Collee, Jonathan Fuhrman, Garry Hamilton, Mike Gabrawy, Basil Iwanyk, Andrew Ogilvie, Director-Anthony Maras Cast-Dev Patel, Armi Hammer, Naznin Boniadi, Jason Issacs, Anupam Kher The Wedding Guest(Casting Director) Producer-Dev Patel, Anthony Wilcox, Michael Winterbottom, Deepak Nayar, Pravesh Sahni, Nik Bower, Melissa Parmenter Director-Michael Winterbottom Cast-Dev Patel, Radhika Apte, Jim Sarb, Harish Khanna The Field(Casting Director) Producer-Rohit Karn Batra & Guy L.Luthan Director-Rohit karan Batra Cast-Prem Chopra, Ronit Roy, Neeraj Kabi, Brenden Fraser, Ali haji, Ekavali Khanna Bioscopewala(Casting Director) Producer-Sunil Doshi(Alliance media) Director-Deb Medhekar Cast- Danny Denzongpa, Adil Hussain, Geetanjali Thapa, Tisca Chopra, Simon Frenay, Ekavali Khanna Chaman Bahar(Casting Director) Producer-Saregama India, Siddharth Anand Kumar, Vikram Mehra Director-Apurva Dhar Badgaiyann Cast-Jitendra Kumar, Bhuvan Arora, Dhirendra Tiwari, Ashwani Kumar Soni(Casting Director) Producer-Kimi Singh Director-Ivan Ayr Cast-Saloni Batra, Geetika Vidya Ohlyan Viceroy House(Casting Associate) Producers-Gurinder Chadha, BBC, Pathe Films, Paul Meyda Berges, Deepak Nayar Director-Gurnder Chadha -

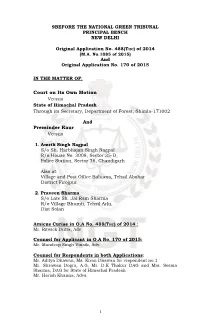

Deforestation Shimla NGT Judgement.Pdf

9BEFORE THE NATIONAL GREEN TRIBUNAL PRINCIPAL BENCH NEW DELHI Original Application No. 488(THC) of 2014 (M.A. No.1085 of 2015) And Original Application No. 170 of 2015 IN THE MATTER OF: Court on Its Own Motion Versus State of Himachal Pradesh Through its Secretary, Department of Forest, Shimla-171002 And Preminder Kaur Versus 1. Amrik Singh Nagpal S/o Sh. Harbhajan Singh Nagpal R/o House No. 3008, Sector 35-D, Police Station, Sector 36, Chandigarh Also at: Village and Post Office Baluana, Tehsil Abohar District Firojpur 2. Praveen Sharma S/o Late Sh. Jai Ram Sharma R/o Village Bhumti, Tehsil Arki, Dist Solan Amicus Curiae in O.A No. 488(THC) of 2014 : Mr. Ritwick Dutta, Adv Counsel for Applicant in O.A No. 170 of 2015: Mr. Mandeep Singh Vinaik, Adv. Counsel for Respondents in both Applications: Mr. Aditya Dhawan, Ms. Kiran Dhawan for respondent no.1 Mr. Shrawan Dogra, A.G, Mr. D.K Thakur DAG and Mrs. Seema Sharma, DAG for State of Himachal Pradesh Mr. Harish Khanna, Advs. 1 JUDGEMENT PRESENT: Hon’ble Mr. Justice Swatanter Kumar (Chairperson) Hon’ble Mr.Justice Raghuvendra S. Rathore (Judicial Member) Hon’ble Mr. Bikram Singh Sajwan (Expert Member) Reserved on: 31st January, 2017 Pronounced on: 1st August, 2017 1. Whether the judgment is allowed to be published on the net? 2. Whether the judgment is allowed to be published in the NGT Reporter? RAGHUVENDRA S. RATHORE, J (JUDICIAL MEMBER) 1. While sitting in Circuit Bench at Shimla, the Tribunal came across a newspaper report published by The Tribune on 20.11.2014 that 200 trees have been cut near Tara Devi Temple. -

Programme Anglais Inde Barbier.Pdf

• * • • • • 0 te•i • • • • • 49 1• • • • • • • •l 1 • • • • • • • • • O ' • • • • 1 • • • • • • • 0• •• • • • ‘I0 • • • • • • • • •0 *•• • • • • 0 • • • 4 • • ea 0• 0 • • • ee •••' 4••••• • • • • 000000, • • • • • • •e • •••• ••i •••• • • • • • •••• •* •• •• • • • à* •• • 9 • le*: e e 00. • • • • • ••• • 4Ie • • • •• • • • • • • • le• • e• • • •• • • • • •*• • • • * tit, • • • 6 • - re • • g fle • .0 • • • e • 111 • • • .• • • • 0 ;à • • • • • • e • • • • • • s • • • • Ce**. k' e • • • • i• • • • • • 9 •e• • * • • • a ge • • ••• • O0 • se g •• • • 1111 3 • • • I. • •• • • • • • 0 • 4,0 • • • 0 • • 9 • • • • • • • 0 • • • • • • • •••• • • • •• •• 0 0 • • Il> le MI 411 el ...... ver •er. Ys di là. .Jéià 0 • 4 January 2011 onward, Enqumes: 23073647, 23387137 ono Elio* NATIONAL SCHOOL OF DRAMA NATIONAL SCHOOL OF DRAMA SRC L.T.G. BAFIUTV1UKFI SAMMUKTI KAMAN1 ABHIMANCH NSD OPEN AIR T1E SPACE 4:30 pm 5:30 pm 6.00 pm 6.00 pm 7:00 pm 9:30 pm 6:30 pm 6:30 pm FRI 7 1NAUGURAl_. CEREMONY-KAMANlat 5.30 pm, Play CHARAND o . àlywright:1-Iabib Tanvir, Dir.Anupl-lazarika, Assamese 35min, Guwahati AN AUTOBIOGRAPHY OF A DEVIL Playwright: Kakarkapudi Narasimha Yoga Patanjali Dir: Shiva Prasad Hindi, 1 hr, Delhi LE BARBIER DE SEVILLE E— 8 PARK SANTA MARIA DE GREAT EXPECTATIONS SALAAM INDIA BITTER BELIEF OF COTRONE Playwright Et Dir: Manav IQUIQUE: REVENGE OF lnspired by the original by Author: Pierre Augustin Playwright: Nicholas THE MAGICIAN Kaul RAMON RAMON Charles Dickens Caron De Beaumarchais Kharkongor Playwright and Dir: Andrea Hindi, 1 hr 20min Dir: Manuel Loyola Dir: Swati Mittal Dir: Eric Vigner Dir: Lushin Dubey Cusumano Mumbai Non-verbal, 55min Hindi, 1 hr 10 min Albanian with English Hindi/English English Et Italian, 55 mins Chile New Delhi subtitles, 1 hr 17 mins 1 hr 30 min, New Delhi France/Albania MAHAKABYER PARE EN UN SOL AMARILLO ...ABOUT RAM MS. -

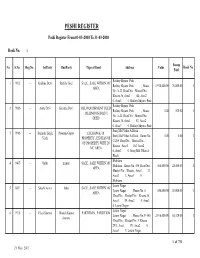

Peshi Register

PESHI REGISTER Peshi Register From 01-03-2010 To 31-03-2010 Book No. 1 Stamp No. S.No. Reg.No. IstParty IIndParty Type of Deed Address Value Book No. Paid Radhey Shyam Park 19813 -- Krishna Devi Sushila Goel SALE , SALE WITHIN MC Radhey Shyam Park , House 1,920,000.00 76,800.00 1 AREA No. A-22 ,Road No. , Mustail No. , Khasra 36, Area1 140, Area2 0, Area3 0 Radhey Shyam Park Radhey Shyam Park 29836 -- Anita Devi Krishna Devi RELINQUISHMENT DEED Radhey Shyam Park , House 0.00 100.00 1 , RELINQUISHMENT No. A-22 ,Road No. , Mustail No. , DEED Khasra 36, Area1 83, Area2 0, Area3 0 Radhey Shyam Park Suraj Mal Vihar A Block 38906 -- Surinder Singh Poonam Gupta EXCHANGE OF Suraj Mal Vihar A Block , House No. 0.00 0.00 1 Virdi PROPERTY , EXCHANGE C-289 ,Road No. , Mustail No. , OF PROPERTY WITH IN Khasra , Area1 162, Area2 MC AREA 0, Area3 0 Suraj Mal Vihar A Block Shahdara 49435 -- Gullo mamta SALE , SALE WITHIN MC Shahdara , House No. 490 ,Road No. , 560,000.00 22,400.00 1 AREA Mustail No. , Khasra , Area1 33, Area2 0, Area3 0 Shahdara Laxmi Nagar 58831 -- Shashi Arora Indu SALE , SALE WITHIN MC Laxmi Nagar , House No. 6 650,000.00 26,000.00 1 AREA ,Road No. , Mustail No. , Khasra 36, Area1 59, Area2 0, Area3 0 Laxmi Nagar Laxmi Nagar 69718 -- Vikas Sharma Manish Kumar PARTITION , PARTITION Laxmi Nagar , House No. F-145 2,916,000.00 58,320.00 1 sharma ,Road No. , Mustail No. -

PART-II Will Be Taken up on Thursday Only

24.02.2012 R-1 ( Regular Matters) 24.02.2012 REGULAR MATTERS COURT NO. 1 (DIVISION BENCH-1) HON'BLE THE ACTING CHIEF JUSTICE HON'BLE MR. JUSTICE RAJIV SAHAI ENDLAW [ Note I: In regular matters & final hearing matters , the parties should keep ready,short synopsis running into not more than 3 pages each.] Note II: PART-II will be taken up on Thursday only. PART-I REGULAR MATTERS RESERVED MATTERS----NO.4.LPA 338/2009 1 .LPA 1327/2007---------| BOARD OF CONTROL FOR CRICKET MAHESH AGARWAL,RISHI SUB TO O/N PH | IN INDIA AND ANR AGGARWAL,B.S. SHUKLA,RAJEEV NOT TILL 24.02.2012 Vs. PRASAR BHARTI, SHARMA,VINEET | BROADCASTING CORPORATION OF MALHOTRA,YOGESH VERMA,VIJAY INDIA AND ANR HANSARIA,RAJEEV SINGH,P.P. | MALHOTRA,RAJEEV MEHRA 2 .W.P.(C) 8458/2007 BOARD OF CONTROL FOR CRICKET RISHI AGGARWAL,RAJEEV SUB TO O/N PH | IN INDIA AND ANR SHARMA,ANIRUDDHA RAY,VINEET NOT TILL 24.02.2012 Vs. PRASAR BHARTI, MALHOTRA,ABHISHEK | BROADCASTING CORPORATION OF BIRTHRAY,NIHAR RANJAN INDIA AND ANR MOHAPATRA,ANIL MENON,CHETAN | CHAWLA,AKSHAY RINGE,PRADEEP K. BAKSHI 3 .W.P.(C) 9610/2007 | RAVI DEV GUPTA D.K.SINGH,RAVEEV SHARMA, SUB TO O/N PH------| Vs. UOI AND ANR NIHAR RANJAN MOHAPATRA, NOT TILL 24.02.2012 ABHISHEK,MAHESH AGARWAL,SAMEER PAREKH 5 . W.P.(C) 4158/2011 AK ENTERPRISES DC PANDEY,MANEESHA DHIR CM APPL. 8580/2011 Vs. UOI AND ORS VIRES NO.1 6 . W.P.(C) 859/2008------| G.D.BUILDTECH P.LTD. J.K.MITTAL,MUKESH ANAND TOP | Vs.