Handbook on Exempted Supplies Under GST

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Rabindra Sangeet

UNIVERSITY GRANTS COMMISSION NET BUREAU Subject: MUSIC Code No.: 16 SYLLABUS Hindustani (Vocal, Instrumental & Musicology), Karnataka, Percussion and Rabindra Sangeet Note:- Unit-I, II, III & IV are common to all in music Unit-V to X are subject specific in music www.careerindia.com -1- Unit-I Technical Terms: Sangeet, Nada: ahata & anahata , Shruti & its five jaties, Seven Vedic Swaras, Seven Swaras used in Gandharva, Suddha & Vikrit Swara, Vadi- Samvadi, Anuvadi-Vivadi, Saptak, Aroha, Avaroha, Pakad / vishesa sanchara, Purvanga, Uttaranga, Audava, Shadava, Sampoorna, Varna, Alankara, Alapa, Tana, Gamaka, Alpatva-Bahutva, Graha, Ansha, Nyasa, Apanyas, Avirbhav,Tirobhava, Geeta; Gandharva, Gana, Marga Sangeeta, Deshi Sangeeta, Kutapa, Vrinda, Vaggeyakara Mela, Thata, Raga, Upanga ,Bhashanga ,Meend, Khatka, Murki, Soot, Gat, Jod, Jhala, Ghaseet, Baj, Harmony and Melody, Tala, laya and different layakari, common talas in Hindustani music, Sapta Talas and 35 Talas, Taladasa pranas, Yati, Theka, Matra, Vibhag, Tali, Khali, Quida, Peshkar, Uthaan, Gat, Paran, Rela, Tihai, Chakradar, Laggi, Ladi, Marga-Deshi Tala, Avartana, Sama, Vishama, Atita, Anagata, Dasvidha Gamakas, Panchdasa Gamakas ,Katapayadi scheme, Names of 12 Chakras, Twelve Swarasthanas, Niraval, Sangati, Mudra, Shadangas , Alapana, Tanam, Kaku, Akarmatrik notations. Unit-II Folk Music Origin, evolution and classification of Indian folk song / music. Characteristics of folk music. Detailed study of folk music, folk instruments and performers of various regions in India. Ragas and Talas used in folk music Folk fairs & festivals in India. www.careerindia.com -2- Unit-III Rasa and Aesthetics: Rasa, Principles of Rasa according to Bharata and others. Rasa nishpatti and its application to Indian Classical Music. Bhava and Rasa Rasa in relation to swara, laya, tala, chhanda and lyrics. -

The West Bengal College Service Commission State

THE WEST BENGAL COLLEGE SERVICE COMMISSION STATE ELIGIBILITY TEST Subject: MUSIC Code No.: 28 SYLLABUS Hindustani (Vocal, Instrumental & Musicology), Karnataka, Percussion and Rabindra Sangeet Note:- Unit-I, II, III & IV are common to all in music Unit-V to X are subject specific in music Unit-I Technical Terms: Sangeet, Nada: ahata & anahata , Shruti & its five jaties, Seven Vedic Swaras, Seven Swaras used in Gandharva, Suddha & Vikrit Swara, Vadi- Samvadi, Anuvadi-Vivadi, Saptak, Aroha, Avaroha, Pakad / vishesa sanchara, Purvanga, Uttaranga, Audava, Shadava, Sampoorna, Varna, Alankara, Alapa, Tana, Gamaka, Alpatva-Bahutva, Graha, Ansha, Nyasa, Apanyas, Avirbhav,Tirobhava, Geeta; Gandharva, Gana, Marga Sangeeta, Deshi Sangeeta, Kutapa, Vrinda, Vaggeyakara Mela, Thata, Raga, Upanga ,Bhashanga ,Meend, Khatka, Murki, Soot, Gat, Jod, Jhala, Ghaseet, Baj, Harmony and Melody, Tala, laya and different layakari, common talas in Hindustani music, Sapta Talas and 35 Talas, Taladasa pranas, Yati, Theka, Matra, Vibhag, Tali, Khali, Quida, Peshkar, Uthaan, Gat, Paran, Rela, Tihai, Chakradar, Laggi, Ladi, Marga-Deshi Tala, Avartana, Sama, Vishama, Atita, Anagata, Dasvidha Gamakas, Panchdasa Gamakas ,Katapayadi scheme, Names of 12 Chakras, Twelve Swarasthanas, Niraval, Sangati, Mudra, Shadangas , Alapana, Tanam, Kaku, Akarmatrik notations. Unit-II Folk Music Origin, evolution and classification of Indian folk song / music. Characteristics of folk music. Detailed study of folk music, folk instruments and performers of various regions in India. Ragas and Talas used in folk music Folk fairs & festivals in India. Unit-III Rasa and Aesthetics: Rasa, Principles of Rasa according to Bharata and others. Rasa nishpatti and its application to Indian Classical Music. Bhava and Rasa Rasa in relation to swara, laya, tala, chhanda and lyrics. -

X-12 Ins. Page (Paper-II)

www.Vidyarthiplus.com PAPER-II MUSIC Signature and Name of Invigilator 1. (Signature) __________________________ OMR Sheet No. : ............................................... (Name) ____________________________ (To be filled by the Candidate) 2. (Signature) __________________________ Roll No. (Name) ____________________________ (In figures as per admission card) Roll No.________________________________ D 1 6 1 0 (In words) 1 Time : 1 /4 hours] [Maximum Marks : 100 Number of Pages in this Booklet : 24 Number of Questions in this Booklet : 50 Instructions for the Candidates ¯Ö¸üßÖÖÙ£ÖµÖÖë êú ×»Ö ×Ö¤ìü¿Ö 1. Write your roll number in the space provided on the top of 1. ¯ÖÆü»Öê ¯ÖéÂü êú ú¯Ö¸ü ×ÖµÖÖ Ã£ÖÖÖ ¯Ö¸ü ¯ÖÖÖ ¸üÖê»Ö Ö´²Ö¸ü ×»Ö×Ö this page. 2. ÃÖ ¯ÖÏ¿Ö-¯Ö¡Ö ´Öë ¯ÖÖÖÃÖ ²ÖÆãü×¾Öú»¯ÖßµÖ ¯ÖÏ¿Ö Æïü 2. This paper consists of fifty multiple-choice type of questions. 3. ¯Ö¸üßÖÖ ¯ÖÏÖ¸ü´³Ö ÆüÖêÖê ¯Ö¸ü, ¯ÖÏ¿Ö-¯ÖãÛÃÖúÖ Ö¯ÖúÖê ¤êü ¤üß ÖÖµÖêÖß ¯ÖÆü»Öê ¯ÖÖÑÖ 3. At the commencement of examination, the question booklet ×´ÖÖü Ö¯ÖúÖê ¯ÖÏ¿Ö-¯ÖãÛÃÖúÖ ÖÖê»ÖÖê Ö£ÖÖ ÃÖúß ×Ö´Ö×»Ö×ÖÖ ÖÖÑÖ êú will be given to you. In the first 5 minutes, you are requested ×»Ö ×¤üµÖê ÖÖµÖëÖê, ×ÖÃÖúß ÖÖÑÖ Ö¯ÖúÖê ¾Ö¿µÖ ú¸üÖß Æîü : to open the booklet and compulsorily examine it as below : (i) ¯ÖÏ¿Ö-¯ÖãÛÃÖúÖ ÖÖê»ÖÖê êú ×»Ö ÃÖêú ú¾Ö¸ü ¯ÖêÖ ¯Ö¸ü »ÖÖß úÖÖÖ úß (i) To have access to the Question Booklet, tear off the paper ÃÖᯙ úÖê ±úÖÍü »Öë Öã»Öß ÆãüÔ µÖÖ ×²ÖÖÖ Ãüßú¸ü-ÃÖᯙ úß ¯ÖãÛÃÖúÖ seal on the edge of this cover page. -

GST Notifications (Rate) / Compensation Cess, Updated As On

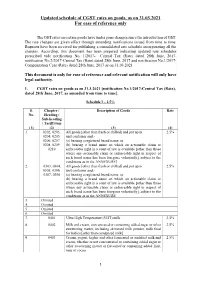

Updated schedule of CGST rates on goods, as on 31.03.2021 For ease of reference only The GST rates on certain goods have under gone changes since the introduction of GST. The rate changes are given effect through amending notifications issued from time to time. Requests have been received for publishing a consolidated rate schedule incorporating all the changes. According, this document has been prepared indicating updated rate schedules prescribed vide notification No. 1/2017- Central Tax (Rate) dated 28th June, 2017, notification No.2/2017-Central Tax (Rate) dated 28th June, 2017 and notification No.1/2017- Compensation Cess (Rate) dated 28th June, 2017 as on 31.03.2021 This document is only for ease of reference and relevant notification will only have legal authority. 1. CGST rates on goods as on 31.3.2021 [notification No.1/2017-Central Tax (Rate), dated 28th June, 2017, as amended from time to time]. Schedule I – 2.5% S. Chapter / Description of Goods Rate No. Heading / Sub-heading / Tariff item (1) (2) (3) (4) 1. 0202, 0203, All goods [other than fresh or chilled] and put up in 2.5% 0204, 0205, unit container and,- 0206, 0207, (a) bearing a registered brand name; or 0208, 0209, (b) bearing a brand name on which an actionable claim or 0210 enforceable right in a court of law is available [other than those where any actionable claim or enforceable right in respect of such brand name has been foregone voluntarily], subject to the conditions as in the ANNEXURE] 2. 0303, 0304, All goods [other than fresh or chilled] and put up in 2.5% 0305, 0306, unit container and,- 0307, 0308 (a) bearing a registered brand name; or (b) bearing a brand name on which an actionable claim or enforceable right in a court of law is available [other than those where any actionable claim or enforceable right in respect of such brand name has been foregone voluntarily], subject to the conditions as in the ANNEXURE 3. -

MUSIC Hindustani

The Maharaja Sayajirao University of Baroda, Vadodara Ph. D Entrance Tet (PET) SYLLABUS Subject: MUSIC PET ExamCode : 21 Hindustani (Vocal, Instrumental & Musicology), Karnataka, Percussion and Rabindra Sangeet Note:- Unit-I, II, III & IV are common to all in music Unit-V to X are subject specific in music -1- Unit-I Technical Terms: Sangeet, Nada: ahata & anahata , Shruti & its five jaties, Seven Vedic Swaras, Seven Swaras used in Gandharva, Suddha & Vikrit Swara, Vadi- Samvadi, Anuvadi-Vivadi, Saptak, Aroha, Avaroha, Pakad / vishesa sanchara, Purvanga, Uttaranga, Audava, Shadava, Sampoorna, Varna, Alankara, Alapa, Tana, Gamaka, Alpatva-Bahutva, Graha, Ansha, Nyasa, Apanyas, Avirbhav,Tirobhava, Geeta; Gandharva, Gana, Marga Sangeeta, Deshi Sangeeta, Kutapa, Vrinda, Vaggeyakara Mela, Thata, Raga, Upanga ,Bhashanga ,Meend, Khatka, Murki, Soot, Gat, Jod, Jhala, Ghaseet, Baj, Harmony and Melody, Tala, laya and different layakari, common talas in Hindustani music, Sapta Talas and 35 Talas, Taladasa pranas, Yati, Theka, Matra, Vibhag, Tali, Khali, Quida, Peshkar, Uthaan, Gat, Paran, Rela, Tihai, Chakradar, Laggi, Ladi, Marga-Deshi Tala, Avartana, Sama, Vishama, Atita, Anagata, Dasvidha Gamakas, Panchdasa Gamakas ,Katapayadi scheme, Names of 12 Chakras, Twelve Swarasthanas, Niraval, Sangati, Mudra, Shadangas , Alapana, Tanam, Kaku, Akarmatrik notations. Unit-II Folk Music Origin, evolution and classification of Indian folk song / music. Characteristics of folk music. Detailed study of folk music, folk instruments and performers of various regions in India. Ragas and Talas used in folk music Folk fairs & festivals in India. -2- Unit-III Rasa and Aesthetics: Rasa, Principles of Rasa according to Bharata and others. Rasa nishpatti and its application to Indian Classical Music. Bhava and Rasa Rasa in relation to swara, laya, tala, chhanda and lyrics. -

Agenda for 21 GST Council Meeting

Confidential Agenda for 21st GST Council Meeting 9 September 2017 Hyderabad, Telangana Page 2 of 173 F.No. 144/21st Meeting/GST Council/2017 GST Council Secretariat Room No.275, North Block, New Delhi Dated: 5 September 2017 Notice for the 21st Meeting of the GST Council on 9 September 2017 The undersigned is directed to refer to the subject cited above and to say that the 21st meeting of the GST Council will be held on 9 September 2017 at Hyderabad International Convention Centre, Novotel Hotel, Madhapur, Hyderabad. The schedule of the meeting is as follows: i. Saturday, 9 September 2017 : 1100 hours onwards 2. In addition, an officers’ meeting will be held at the same venue as per the following schedule: ii. Friday, 8 September 2017 : 1500 hours onwards 3. The agenda items for the 21st GST Council Meeting are attached. 4. Keeping in view the constraints of rooms in the hotel, it is requested that participation from each State may be limited to 2 officers in addition to the Hon’ble Member of the GST Council. 5. Please convey the invitation to the Hon’ble Members of the GST Council to attend the 21st GST Council Meeting. - Sd - (Dr. Hasmukh Adhia) Secretary to the Govt. of India and ex-officio Secretary to the GST Council Tel: 011 23092653 Copy to: 1. PS to the Hon’ble Minister of Finance, Government of India, North Block, New Delhi with the request to brief Hon’ble Minister about the above said meeting. 2. PS to Hon’ble Minister of State (Finance), Government of India, North Block, New Delhi with the request to brief Hon’ble Minister about the above said meeting. -

DU MA Percussion Music

DU MA Percussion Music Topic:- DU_J19_MA_PM 1) Which of the following is not a Yati? इनमे से कौन यत नहं ह? [Question ID = 213] 1. Pipilika / पपीलका [Option ID = 850] 2. Mridanga / मदृ ंगा [Option ID = 849] 3. Anagat / अनागत [Option ID = 852] 4. Sama / समा [Option ID = 851] Correct Answer :- Mridanga / मदृ ंगा [Option ID = 849] 2) Which artist was famous for ‘Dance Accompaniment? नयृ के साथ संगत करने म कौन से कलाकार स थे? [Question ID = 186] 1. Pt. Pagal Das / पं. पागल दास [Option ID = 742] 2. Pt. Birju Maharaj / पं. बरज ू महाराज [Option ID = 743] 3. Pt. Kudau Singh / पं. कु दऊ सहं [Option ID = 744] 4. Pt. Kishan Maharaj / पं. कशन महाराज [Option ID = 741] Correct Answer :- Pt. Kishan Maharaj / पं. कशन महाराज [Option ID = 741] 3) Which gharana plays with variation of ‘Theka’ ? ‘ठेके ’ के वतार के साथ कस घराने का वादन होता है:- [Question ID = 215] 1. Delhi gharana / दल घराना [Option ID = 857] 2. Ajrada Gharana / अजराड़ा घराना [Option ID = 858] 3. Banaras Gharana / बनारस घराना [Option ID = 860] 4. Lucknow gharana / लखनऊ घराना [Option ID = 859] Correct Answer :- Delhi gharana / दल घराना [Option ID = 857] 4) Which Gharana is influenced by the compositions of Pakhawaj ? कौन सा घराना पखावज़ क बंदश से भावत है? [Question ID = 249] 1. Delhi / दल [Option ID = 993] 2. Ajrada / अजराड़ा [Option ID = 996] 3. -

![THE GAZETTE of INDIA : EXTRAORDINARY [PART II—SEC. 3(I)] NOTIFICATION New Delhi, the 22Nd September, 2017 No.28/2017-Union](https://docslib.b-cdn.net/cover/2596/the-gazette-of-india-extraordinary-part-ii-sec-3-i-notification-new-delhi-the-22nd-september-2017-no-28-2017-union-2342596.webp)

THE GAZETTE of INDIA : EXTRAORDINARY [PART II—SEC. 3(I)] NOTIFICATION New Delhi, the 22Nd September, 2017 No.28/2017-Union

66 THE GAZETTE OF INDIA : EXTRAORDINARY [P ART II—SEC . 3(i)] 111. उडुकईi 112. चंडे 113. नागारा - केटलेG स कƙ जोड़ी 114. प बाई - दो बेलनाकार Gम कƙ इकाई 115. पैराित पु, हगी - sेम Gम दो िटϝस के साथ खेला 116. संबल 117. िटक डफ या िटक डफ - लाठी के साथ खेला जाने वाला टġड मĞ डेफ 118. तमक 119. ताशा - केटलेGम का Oकार 120. उƞम 121. जलातरंग िच पēा - पीतल के ƚजगल के साथ आग टĪग 122. चĞिगल - धातु िडक 123. इलाथलम 124. गेजर - Qास पोत 125. घटक और मटकाम (िमŝी के बरतन बतϕन Gम) 126. घुंघĐ 127. खारट या िच पला 128. मनजीरा या झंज या ताल 129. अखरोट - िमŝी के बतϕन 130. संकरजांग - िल थोफोन 131. थाली - धातु लेट 132. थाकुकाजामनाई 133. कंचारांग, कांच के एक Oकार 134. कथाततरंग, एक Oकार का जेलोफ़ोन [फा सं.354/117/2017-टीआरयू-भाग II] मोिहत ितवारी, अवर सिचव Ɨट पणी : Oधान अिधसूचना सं. 2/2017- संघ राϤ यϓेJ कर (दर), तारीख 28 जून, 2017, सा.का.िन. 711 (अ) तारीख 28 जून, 2018 ůारा भारत के राजपJ , असाधारण, भाग II, खंड 3, उपखंड (i) ůारा Oकािशत कƙ गई थी । NOTIFICATION New Delhi, the 22nd September, 2017 No.28/2017-Union Territory Tax (Rate) G.S.R.1196 (E).— In exercise of the powers conferred by sub-section (1) of section 8 of the Union Territory Goods and Services Tax Act, 2017 (14 of 2017), the Central Government, being satisfied that it is necessary in the public interest so to do, on the recommendations of the Council, hereby makes the following amendments in the notification of the Government of India in the Ministry of Finance (Department of Revenue), No.2/2017-Union territory Tax (Rate), dated the 28th June, 2017, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. -

The Arunachal Pradesh Gazette EXTRAORDINARY PUBLISHED by AUTHORITY

The Arunachal Pradesh Gazette EXTRAORDINARY PUBLISHED BY AUTHORITY No. 411, Vol. XXIV, Naharlagun, Wednesday, October 4, 2017 Asvina 12, 1939 (Saka) GOVERNMENT OF ARUNACHAL PRADESH DEPARTMENT OF TAX & EXCISE ITANAGAR ————— Notification No. 28/2017-State Tax (Rate) The 26th September, 2017 No. GST/24/2017.— In exercise of the powers conferred by sub-section (1) of Section 11 of the Arunachal Pradesh Goods and Services Tax Act, 2017 (7 of 2017), the State Government, on the recommendations of the Council, hereby makes the following amendments in the notification of the Government of Arunachal Pradesh, Department of Tax & Excise, No.2/2017-State Tax (Rate), dated the 28th June, 2017, published in the Extra ordinary Gazette of Arunachal Pradesh, vide number 192, Vol XXIV, dated the 30th June, 2017, namely:- In the said notification,- (B) in the Schedule,- (i) against serial number 27, in column (3), for the words “other than put up in unit containers and bearing a registered brand name”, the words, brackets and letters “other than those put up in unit container and,- (a) bearing a registered brand name; or (b) bearing a brand name on which an actionable claim or enforceable right in a court of law is available [other than those where any actionable claim or enforceable right in respect of such brand name has been foregone voluntarily, subject to the conditions as in the ANNEXURE I]”, shall be substituted ; (jj) against serial numbers 29 and 45, in column (3), for the words “other than put up in unit container and bearing a registered brand -

Yojana Magazine Summary for August 2020 Issue

Philosophical Nature of Indian Music • The Indian classical music, be it Hindustani or Carnatic, has essentially got a spiritual component inherent in it. Reasons for the development of spiritual component are: o Temples provided a platform where these arts flourished; o Bhakti or selfless devotion that was the underlying essence; o The artistic principles of Indian classical music are formulated and structured in such a way that it becomes an inward journey for its practitioners so that they get intimately connected with their within. Spiritual Features of Indian Music A. Nadopasana - The Invocation of the Primordial Sound • For a true practitioner of classical music, the approach used to be Nadopdsana – the invocation of the primordial sound. For these practitioners, music became an internal journey for the realisation of the ultimate truth. • Even the selection of the Raga and the composition at the time of a performance was a result of the intuition and the inspiration of the moment. B. The Guru-Shishya and Gharana tradition • It is another crucial feature which is common for all the classical music traditions of India. For centuries, this Guru-shishya transmission has made it possible to carry forward the intense experiences innately embedded in this great tradition of enlightened practitioners of music. • The musical gharanas of north Indian or Hindustani classical music have also contributed to the diversity of their form of music by presenting a distinct style of it. The Origin and Historical Development of Different Forms of Indian Music • The origin of Indian music can be traced back to the chanting of Vedic hymns and mantras. -

Yojana Kurukshetra GIST – AUGUST 2020 IASBABA

Yojana Kurukshetra GIST – AUGUST 2020 IASBABA www.iasbaba.com Page 1 Yojana Kurukshetra GIST – AUGUST 2020 IASBABA Preface This is our 65th edition of Yojana Gist and 56th edition of Kurukshetra Gist, released for the month of August 2020. It is increasingly finding a place in the questions of both UPSC Prelims and Mains and therefore, we’ve come up with this initiative to equip you with knowledge that’ll help you in your preparation for the CSE. Every issue deals with a single topic comprehensively sharing views from a wide spectrum ranging from academicians to policy makers to scholars. The magazine is essential to build an in-depth understanding of various socio-economic issues. From the exam point of view, however, not all articles are important. Some go into scholarly depths and others discuss agendas that are not relevant for your preparation. Added to this is the difficulty of going through a large volume of information, facts and analysis to finally extract their essence that may be useful for the exam. We are not discouraging from reading the magazine itself. So, do not take this as a document which you take read, remember and reproduce in the examination. Its only purpose is to equip you with the right understanding. But, if you do not have enough time to go through the magazines, you can rely on the content provided here for it sums up the most essential points from all the articles. You need not put hours and hours in reading and making its notes in pages. We believe, a smart study, rather than hard study, can improve your preparation levels. -

Background Material on GST Acts and Rules

Background Material on GST Acts and Rules The Institute of Chartered Accountants of India (Set up by an Act of Parliament) New Delhi © The Institute of Chartered Accountants of India All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form, or by any means, electronic, mechanical, photocopying, recording, or otherwise without prior permission, in writing, from the publisher. DISCLAIMER: The views expressed in this book are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s). The information cited in this book has been drawn primarily from the www.cbec.gov.in and other sources. While every effort has been made to keep the information cited in this book error free, the Institute or any office of the same does not take the responsibility for any typographical or clerical error which may have crept in while compiling the information provided in this book. First Edition : May, 2017 Second Edition : September, 2017 Revised Edition : January 2018 Committee/Department : Indirect Taxes Committee E-mail : [email protected] Website : www.icai.org; www.idtc.icai.org Price : e-publication ISBN : 978-81-8441-869-9 Published by : The Publication Department on behalf of the Institute of Chartered Accountants of India, ICAI Bhawan, Post Box No. 7100, Indraprastha Marg, New Delhi - 110 002. Foreword Implementation of Goods and Services Tax (GST) in India is one of the major economic reforms. GST aims to make India a common market with common tax rates and procedures and remove the economic barriers thus, paving the way for an integrated economy at the national level.