Q1 Financial Review

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Newsletter Nov 7

BAXTER ELEMENTARY SCHOOL BAXTER BULLETIN SPECIAL EDITION 2991 Baxter Rd, Anchorage, AK 99504, 907-742-1750 November 11, 2019 CALENDAR NOV 12 - PTA Mtg 6pm NOV 13 - Community Flu Shot Clinic 2-5PM Join us for a NO COST fu shot clinic at: NOV 15 - Popcorn Friday NOV 22 - Turkey Shoot 6pm NOV 28 & 29th NO SCHOOL; Thanksgiving Baxter Elementary Holiday Wednesday - Nov 13th DEC 6 - Family Bingo Night DEC 10 - Band & Orch Concert 9:45 am 2:00pm - 5:00pm PTA Mtg 6pm DEC 13 - Popcorn Friday • Open to anyone ages 6 months and older. Roar • No insurance required. DEC 18 - Baxter Choir Concert • Parent or guardian consent required for ages 17 and under. • Contact the school nurse with any questons. DECEMBER 20th - JANUARY 5th NO SCHOOL (Winter Break) Important Numbers: Attendance: [email protected] www.facebook.com/ Attendance: 742-1750, Press 1 BaxterElementaryASD Nurse: 742-1751 Cafeteria: 742-1767 http://baxter.asdk12.org Office: 742-1750 November 2019 Sunday Monday Tuesday Wednesday Thursday Friday Saturday 10 11Veterans 12 PTA MTG 13 FLU SHOT 14 15 POPCORN 16 Day-NO 6PM CLINIC FRIDAY SCHOOL 2-5PM 17 18 19 20 21 22 TURKEY 23 SHOOT 6PM 24 25 26 27 28 29 30 THANKSGIVING THANKSGIVING HOLIDAY HOLIDAY December 2019 Sunday Monday Tuesday Wednesday Thursday Friday Saturday 1 2 3 4 5 6 FAMILY 7 BINGO NIGHT 8 9 10 PTA MTG 11 12 13 POPCORN 14 6PM FRIDAY BAND & ORCH ROAR CONCERT 15 16 17 18 CHOIR 19 20 21 CONCERT NO SCHOOL DECEMBER 20TH - JANUARY 5TH. HAVE A HAPPY WINTER BREAK! FROM THE PRINCIPAL’S DESK AND ASSISTANT PRINCIPAL’S DESK Hello Baxter Families, What an interesting November we are having! This mild, wet weather is definitely not the Alaska we are used to. -

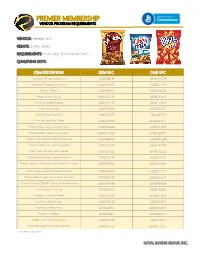

Premier Membership Vendor Program Requirements

PREMIER MEMBERSHIP VENDOR PROGRAM REQUIREMENTS VENDOR: General Mills REBATE: 1.60% rebate REQUIREMENTS: must carry 28 of the top SKU’s QUALIFYING SKU’S: ITEM DESCRIPTION ITEM UPC CASE UPC *Gardetto’s Original Snack Mix 16000166196 16000430379 *Chex Mix Traditional Snack Mix 16000160101 16000351810 *Bugles Original 16000368309 16000280868 *Bugles Nacho Cheese 16000513792 16000280875 *Chex Mix Muddy Buddies 16000507326 16000373010 *Chex Mix Cheddar 16000126060 16000351827 *Chex Mix Bold Snack Mix 16000126077 16000035187 *Chex Mix Cookies & Cream 16000507043 16000324647 *Nature Valley Oats & Honey Granola 16000264694 16000335308 *Nature Valley Sweet & Salty Peanut 16000442825 16000420677 *Nature Valley Sweet & Salty Nut Almond 16000442818 16000420684 *Nature Valley Peanut Butter Granola 16000264793 16000335506 *Fiber One Oats and Chocolate Bar 16000504622 16000146522 *Nature Valley Energy Cranberry Almond 16000506183 16000323152 *Nature Valley Protein Peanut Butter Dark Chocolate 16000507661 16000318493 *Nature Valley Chewy Trail Mix Fruit & Nut 16000439894 16000151205 *Nature Valley Energy Cherry Dark Chocolate 16000506176 16000323145 *Golden Grahams Treat Bar Chocolate Marshmallow 16000505346 16000423364 *Lucky Charms Treat Bar 16000506015 16000435695 *Gardetto’s Mustard Pretzel 16000507319 16000274812 *Gardetto’s Italian Recipe 16000166998 16000430393 *Gardetto’s Reduced Fat 1600016691 16000430386 *Bugles Hot Buffalo 1600050331 16000434377 *Bugles Sweet & Salty Caramel 16000504257 16000147512 *Chex Mix Jalapeno Cheddar Snack Mix 16000505827 -

Revitalization of the Cereal Category: Applying Brand Revival Techniques to Increase Sales of General Mills' Cereal

Revitalization of the Cereal Category: Applying Brand Revival Techniques to Increase Sales of General Mills' Cereal Item Type text; Electronic Thesis Authors Watts, Amanda Elizabeth Publisher The University of Arizona. Rights Copyright © is held by the author. Digital access to this material is made possible by the University Libraries, University of Arizona. Further transmission, reproduction or presentation (such as public display or performance) of protected items is prohibited except with permission of the author. Download date 05/10/2021 19:34:37 Item License http://rightsstatements.org/vocab/InC/1.0/ Link to Item http://hdl.handle.net/10150/578929 REVITALIZATION OF THE CEREAL CATEGORY: APPLYING BRAND REVIVAL TECHNIQUES TO INCREASE SALES OF GENERAL MILLS’ CEREAL By AMANDA ELIZABETH WATTS ____________________ A Thesis Submitted to The Honors College In Partial Fulfillment of the Bachelors degree With Honors in Marketing THE UNIVERSITY OF ARIZONA M A Y 2 0 1 5 Approved by: ______________________________ Dr. Hope Jensen Schau Department of Marketing, Eller College of Management Table of Contents Abstract…………………………………………………………………………………….. 4 Statements of Purpose and Relevance……………………………………………………. 5 Introduction……………………………………………………………………………….... 6 Literature Review………………………………………………………………………….. 6 Brand Sustainability and Revitalization…………………………………………………... 6 Nostalgia Tactics………………………………………………………………………….. 7 The Snacking Occasion………………………………………………………………….... 8 Sustainable Packaging…………………………………………………………………….. 8 General Mills Plans a Revival……………………………………………………………. -

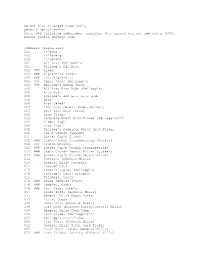

Cereal List Arranged Numerically Generic Default=***** Note: ### Following Codenumber Signifies That Cereal Was Not Updated in 2001, Please Choose Another Code

Cereal List arranged numerically generic default=***** Note: ### following codenumber signifies that cereal was not updated in 2001, please choose another code COMPLETE CEREAL LIST 000 ***None 000 ***Rarely 000 ***Seldom 001 All Bran (Kellogg's) 001 Kellogg's All Bran 002 ### Alpen 003 ### Alpha-Bits (Post) 003 ### Post Alpha-Bits 004 ### Apple Jacks (Kellogg's) 004 ### Kellogg's Apple Jacks 005 All Bran Bran Buds (Kellogg's) 005 Bran Buds 005 Kellogg's All Bran Bran Buds 006 Bran 006 Bran Cereal 007 100% Bran Cereal (Nabisco/Post) 007 Post 100% Bran Cereal 009 Bran Flakes 009 Complete Wheat Bran Flakes (Kellogg's)*** 009 Fiber, High 009 High Fiber 009 Kellogg's Complete Wheat Bran Flakes 011 Cap'n Crunch (Quaker) 011 Quaker Cap'n Crunch 012 ### Cap'n Crunch Crunchberries (Quaker) 012 ### Crunch Berries 012 ### Quaker Cap'n Crunch Crunchberries 013 ### Cap'n Crunch Peanut Butter (Quaker) 013 ### Quaker Cap'n Crunch Peanut Butter 014 Cheerios (General Mills) 014 General Mills Cheerios 014 Toasted Oats 015 Cocoa Krispies (Kellogg's) 015 Kellogg's Cocoa Krispies 015 Krispies, Cocoa 016 ### Cocoa Pebbles (Post) 016 ### Pebbles, Cocoa 016 ### Post Cocoa Pebbles 017 Cocoa Puffs (General Mills) 017 General Mills Cocoa Puffs 017 Puffs, Cocoa 019 Chex, Corn (General Mills) 019 Corn Chex (Ralston Purina/General Mills) 019 General Mills Corn Chex 020 Corn Flakes (Kellogg's)*** 020 Kellogg's Corn Flakes 022 Corn Total (General Mills) 022 General Mills Total Corn Flakes 022 Total Corn Flakes (General Mills) 023 ### Corn Flakes, Country (General Mills) -

Brand Nutrition

Ranking Table 1 Brand Nutrition Ranking by overall nutritional quality (Nutrition Profile Index [NPI] score) in 2012 Includes nutrition information for child and family brands as of May 15, 2009 and May 1, 2012* Average NPI score 2012 nutrition NPI Sugar # of score content Rank Company Brand varieties 2012 2009 range range (%) Best 1 Kellogg Mini-Wheats 11 73 71 54-82 0-22 2 Kashi Golden Goodness 1 72 - 72 13 3 General Mills Cheerios (regular) 1 70 58 70 4 4 Cascadian Farm Purely O’s 1 58 46 58 3 4 (tie) Quaker Life Crunchtime 2 58 - 58 19-22 6 Barbara’s Bakery Puffins 6 58 52 46-68 19-20 Puffins Puffs (formerly 7 Barbara’s Bakery Organic Wild Puffs) 2 56 58 54-58 23 Kashi Squares (formerly 8 Kashi Honey Sunshine) 2 55 56 54-56 20-23 9 General Mills Kix 3 54 51 52-56 10-21 9 (tie) Cascadian Farm Chocolate O’s 1 54 - 54 29 11 Annie’s Bunnies 5 53 50 50-64 7-28 12 Quaker Life 3 53 53 52-54 19-25 13 General Mills Dora the Explorer 1 52 50 52 22 13 (tie) Cascadian Farm Clifford Crunch 1 52 54 52 27 15 Nature’s Path Envirokidz Organic 5 51 52 44-54 23-40 16 Post Raisin Bran 1 50 48 50 32 16 (tie) Cascadian Farm Cinnamon Crunch 1 50 50 50 30 16 (tie) Cascadian Farm Honey Nut O’s 1 50 44 50 23 16 (tie) Cascadian Farm Fruitful O’s 1 50 - 50 29 16 (tie) Kellogg Corn Pops 1 50 33 50 31 Shredded Oats - 16 (tie) Barbara’s Bakery Cinnamon Crunch 1 50 50 50 27 22 General Mills Chex 7 49 45 44-56 7-33 Cheerios (except regular 23 General Mills and Honey Nut) 8 48 46 46-52 28-33 23 (tie) Kellogg Honey Smacks 1 48 46 48 56 25 General Mills -

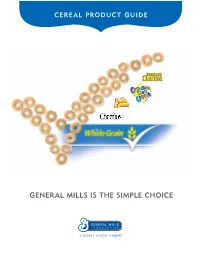

General Mills Is the Simple Choice

CEREAL PRODUCT GUIDE ® GENERAL MILLS IS THE SIMPLE CHOICE success made simple™ GEN-5501 GMFS_Cereal Prod Guide.indd 1 5/5/11 11:11 AM THE BRANDS PLUS THE WHOLE GRAIN YOUR PATRONS LOVE... THEY NEED 92% OF AMERICANS BELIEVE WHOLE GRAIN IS IMPORTANT3 • Whole Grain is the #1 ingredient consumers look for when they buy cereal4 • 2010 dietary guidelines call for at least three servings of Whole Grain foods daily GENERAL MILLS BIG G CEREALS ARE THE #1 SOURCE OF WHOLE GRAIN AT BREAKFAST • General Mills Big G cereals provide America with more Whole Grain at breakfast than any other breakfast food from any other manufacturer • General Mills is the only leading cereal company with Whole Grain in every cereal5 GENERAL MILLS HAS 4 OF THE TOP 5 BEST-SELLING BRANDS1 • We have 4 out of the 5 top brands, including Cheerios, Honey Nut Cheerios, Cinnamon Toast Crunch and Lucky Charms1 • General Mills cereals appeal to patrons of all ages2 • More than 40% of Lucky Charms and Cinnamon Toast Crunch consumption is from adults2 3 General Mills Whole Grain Survey October 2010. 4 Health Cereal Benefit/Ingredient Sort Study, 2008. 5 All Big G Cereals contain at least 8 grams of whole grain per standard serving. All Big G Cereal BowlPaks contain Whole Grain, but some contain less than 8 1 Nielsen, Dollar Share of TTL, 52wks ending 3/12/11. grams due to smaller serving sizes. At least 48 grams recommended daily. 2 National Eating Trends, 2009. GEN-5501 GMFS_Cereal Prod Guide.indd 2-3 5/5/11 11:11 AM ALL THE FORM ATS YOU WANT Singlepak® Tasty and convenient single-serve portions. -

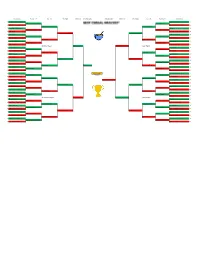

Cereal Bracket

Round of 64 Round of 32 Sweet 16 Elite Eight Final Four Championship Championship Final Four Elite Eight Sweet 16 Round of 32 Round of 64 1 Cinnamon Toast Crunch 51 Frosted Flakes 49 1 Cinnamon Toast Crunch 30 Frosted Flakes 40 16 Blueberry Cheerios 2 Dippin Dots Cereal 4 16 Cinnamon Toast Crunch 24 Frosted Flakes 24 8 Frosted Mini Wheats 42 Kix 34 8 Frosted Mini Wheats 16 Kix 6 9 Alpha-Bits 2 Chocolate Peanut Butter Cheerios 6 9 Cinnamon Toast Crunch 19 Frosted Flakes 33 5 Cheerios 47 Golden Grahams 47 5 Cheerios 23 Golden Grahams 24 12 Bran Flakes 6 Franken Berry 6 12 Cheerios 12 Golden Grahams 12 4 Cocoa Pebbles 35 Fruity Pebbles 39 4 Cocoa Pebbles 22 Fruity Pebbles 22 13 Honey Smacks 18 Kashi Go Lean 14 13 Cinnamon Region Froot Loops 31 Frosted Flakes 28 Sugar Region 6 Count Chocula 30 Corn Pops 41 6 Count Chocula 24 Corn Pops 18 11 Special K Red Berries 23 PB Chex 12 11 Count Chocula 3 Apple Jacks 21 3 Waffle Crisp 42 Apple Jacks 42 3 Waffle Crisp 21 Apple Jacks 27 14 Nilla Cereal 11 Krave 10 14 Froot Loops 27 Apple Jacks 13 7 Raisin Bran 37 Rice Crispy Treats 33 7 Raisin Bran 18 Rice Krispy Treats 26 10 Chocolate Chex 15 Captain Peanut Butter Crunch 20 10 Froot Loops 33 Froot Loops 24 Rice Krispy Treats 15 2 Froot Loops 50 Honey Comb 46 2 Froot Loops 28 Honey Combs 19 15 Twinkies Cereal 3 Donettes Cereal 7 15 1 Lucky Charms 49 Froot Loops Honey Nut Cheerios 48 1 Lucky Charms 37 Champion Honey Nut Cheerios 35 16 Sour Patch Kids Cereal 4 Grape-Nuts 5 16 Lucky Charms 34 Honey Nut Cheerios 23 8 Special K 25 Honey Nut Cheerios 22 Rice -

Nutrition and Marketing Ratings of Children's Cereals

Nutrition and Marketing Ratings of Children’s Cereals Jennifer L. Harris, Ph.D., M.B.A. Marlene B. Schwartz, Ph.D. Kelly D. Brownell, Ph.D. EXECUTIVE SUMMARY The Bad News: There is no ambiguity in the results of this report. The least healthy cereals are the ones most marketed to children, and The Better News: It need not be this way. Most cereals overall, children are exposed to a vast amount of marketed to children are high in sugar, high in sodium, and low in marketing for highly-sugared cereals, more than for fiber. Many are highly colorful because of artificial dyes, making any other category of packaged food. healthier cereals, very literally, pale in comparison. Yet, every cereal company does have products that earn good nutrition scores, but What was once a simple marketing landscape— these are marketed to adults, not children. television advertising during cartoons—has morphed into a complex web of persuasive messages even Reinforcing the myth that children will not eat low-sugar cereals, adults may not perceive as marketing. Internet the industry has funded a number of studies that find that highly- games and marketing through social media such as sweetened cereal is good for children, especially when compared to Facebook are just the beginning and do not capture having no breakfast at all. Breakfast is good—make no mistake—but digital advances that will occur in the future. a breakfast with less sugar, more fiber, and less sodium will be better for children. The cereals marketed to children fail every reasonable nutrition test, yet according to the food A new study delivers good news. -

ON NOVEMBER 30, 1928, a New Company Was Listed on the New York Stock Exchange

ON NOVEMBER 30, 1928, a new company was listed on the New York Stock Exchange. Formed through the merger of several regional milling companies, General Mills would grow to become one of the largest food companies in the world. To mark that 75th anniversary, this book celebrates 75 years of innovation, invention, food and fun – both inside and outside the kitchen – in America and around the world. PROLOGUE 1 PROLOGUE It would be difficult to capture our rich history in a thousand pages. There are simply too many stories to tell. But this opportunity only comes once – and we couldn’t let it pass. On the 75th anniversary of the creation of General Mills – in our 137th year as a company – we wanted to pause to commemorate at least some of the historical highlights of a great American company. But where to start? With the creation of General Mills in 1928? Or at the beginning, on the banks of the Mississippi River in 1866? And what of the many companies with which General Mills has been intertwined? What of Pillsbury and Green Giant? What of Kenner and Parker Brothers, Red Lobster and Burger King? What of the products we invented together and the brands we built together? It was simple really. Pillsbury’s history is our history. Green Giant, Old El Paso, Colombo and Häagen-Dazs are here – alive within General Mills. Of the rest we chose to include a little of each, because they too are a part of us. And while we take no credit for the success they enjoy today, we are proud to have shared the same path for at least part of our shared history. -

Sugar in Children's Cereals

NOV 20, 2011 DRAFT EMBARGOED & CONFIDENTIAL SUGAR IN CHILDREN’S CEREALS: POPULAR BRANDS PACK MORE SUGAR THAN SNACK CAKES AND COOKIES by Paul Pestano, M.S., Research Analyst, Etan Yeshua, J.D., Stabile Law Fellow, and Jane Houlihan, M.S.C.E., Senior Vice President for Research Most parents say no to dessert for breakfast, but many children’s cereals have just as much sugar as a dessert!!"!or more. ENVIRONMENTAL WORKING GROUP NOV 20, 2011 DRAFT EMBARGOED & CONFIDENTIAL Acknowledgements For reviewing the ! ndings of this study, we thank Andrew Weil, MD, founder and director of the integrative medicine program at the University of Arizona College of Medicine and Professor of Medicine and Public Health; and Center for Science in the Public Interest’s Margo Wootan, D.Sc., Director, Nutrition Policy, and Bethany Pokress, M.S., Nutrition Policy Associate. Contributors to the study included EWG’s Sonya Lunder, M.P.H, Senior Scientist; Dawn Undurraga, R.D., Nutritionist; and David Andrews, Ph.D., Senior Scientist. The report was designed by Aman Anderson, and the accompanying website was designed by Tylan Yalniz, EWG Web Designers. Special thanks to EWG’s Elaine Shannon, Editor-in-Chief and Publisher, and Nils Bruzelius, Executive Editor and Vice President of Publications. EWG’s Sugar in Children’s Cereal report was made possible through the generosity of many private charitable foundations and EWG’s community of online supporters and individual donors (http://www.ewg.org/ about/funding). The opinions expressed in this report are those of EWG and do not necessarily re" ect the views of reviewers and supporters listed above. -

Participating Products and Every Valid Box Tops Clip Is Worth 10¢

LOOK FOR BOX TOPS ON THE ALL-NEW BOX TOPS IS HERE! HUNDREDS OF PRODUCTS! DOWNLOAD THE APP: CLIP: Traditional Box Tops clips are NO MORE CLIPPING SCAN: If you see this label, do not send it to school. Use being phased out of production, but you YOURSCAN RECEIPT the new Box Tops app to scan your store receipt within 14 can still send unexpired clips to school. SEE HOW AT days of purchase. The app will find participating products and Every valid Box Tops clip is worth 10¢. BTFE.COM instantly add Box Tops to your school’s earnings online. BEVERAGES CEREAL & BREAKFAST FROZEN • Nestle Pure Life Water .5-Liter 24, 28, • Ancient Grains Cheerios™ • Annie's® Bagel Pizzas 32,35-Packs • Annie's® Cereal • Annie's® Pizza Bagels • Nestle Pure Life Water 8 oz. 6, 12, 24 & 56-Packs • Annie's® Toaster Pastries • Annie's® Pizza Poppers • Nestle Pure Life Water 11.15 oz 6-Pack • Apple Cinnamon Cheerios™ • Cinnamon Toast Crunch™ Bites • Apple Cinnamon Toast Crunch™ • Pillsbury™ Mini Cinnis • Banana Nut Cheerios™ • Pillsbury™ Pancakes HOUSEHOLD • Basic 4™ Cereal • Pillsbury™ Toaster Scambles CLEANING • Big G Cereal Breakfast Pack (8 Pouches) • Pillsbury™ Toaster Strudel • Berry Berry Kix™ • Totino's™ Party Pizza • Lysol® Disenfectant Spray • Birthday Cake Cookie Crisp™ • Totino's™ Pizza Rolls • Lysol® Disenfecting Wipes • Blueberry Cheerios™ • Lysol® Toilet Bowl Cleaner • Blueberry Chex™ • Blueberry Toast Crunch™ REFRIGERATED • Boo Berry™ & DAIRY • Cascadian Farm Cereal™ MEALS & SIDES • Cheerios™ • Annie's® Biscuits • Cheerios™ Oat Crunch Cinnamon • Annie's® -

84 Children's Cereals Assessed Against Government And

84 Children’s Cereals Assessed Against Government and Industry Nutrition Guidelines Legend: 6 - Fails industry guidelines** 6 - Fails federal guidelines to take effect in 2016* 6 - Fails final federal sodium guideline to take effect in 2021 (but meets the guidelines to take effect in 2016) 4 - Meets federal guidelines to take effect in 2016 44 - Meets stricter federal guidelines to take effect in 2021 (stricter sodium limit) Labeled Serving Sodium (mil- Saturated Fat Size First (Predominant) Ingre- Sugar (grams Sugar (percent ligrams per (grams per serv- Children’s Cereal Products (grams) dient1 per serving)2 by weight) serving)3 ing)4,5 General Mills 1 Boo Berry 33 Whole Grain Corn 10 6 30.3 190 6 0 Cheerios 2 Cheerios Original 4 28 Whole Grain Oats 1 3.6 160 6 0 3 Apple Cinnamon Cheerios 30 Whole Grain Oats 10 6 33.3 115 6 0 4 Banana Nut Cheerios 28 Whole Grain Corn 9 6 32.1 160 6 0 5 Chocolate Cheerios 27 Whole Grain Corn 9 6 33.3 170 6 0 6 Cinnamon Burst Cheerios 33 Whole Grain Corn 9 6 27.3 130 6 0 7 Frosted Cheerios 28 Whole Grain Oats 9 6 32.1 170 6 0 8 Fruity Cheerios 27 Whole Grain Corn 9 6 33.3 135 6 0 9 Honey Nut Cheerios 28 Whole Grain Oats 9 6 32.1 160 6 0 10 Multi-Grain Cheerios 4 29 Whole Grain Corn 6 20.7 120 6 0 11 Oat Cluster Cheerios Crunch 27 Whole Grain Oats 8 6 29.6 130 6 0 12 Yogurt Burst Cheerios Strawberry 30 Whole Grain Oats 9 6 30.0 170 6 0.5 Chex 13 Chex Wheat 47 Whole Grain Wheat 5 10.6 270 6 0 14 Chocolate Chex 32 Whole Grain Rice 8 25.0 240 6 0 15 Cinnamon Chex 30 Whole Grain Rice 8 6 26.7 180 6 0 16 Corn