BUFFALO CITY METROPOLITAN MUNICIPALITY Audited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

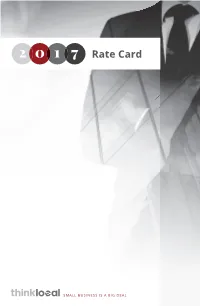

2017-10 A5 Rate Card

Rate Card SMALL BUSINESS IS A BIG DEAL print advert rates About Us Think Local is South Africa’s first and only community-level mass market publication aimed at entrepreneurs and SMMEs. Our content is geared towards empowering business owners with the knowledge, skills and opportunities needed to grow their businesses. Sizes Standard V.I.P. W x H Standard Advert Placements Premium 1/24 Page R 785 R 670 41 X 21 Platinum 1/12 Page R 1 120 R 950 41 X 44 Business Card 1/6 Page R 1 700 R 1 450 41 X 90 One Column 1/3 Page R 2 700 R 2 300 41 X 182 Two Columns 2/3 Page R 4 120 R 3 500 84 X 182 Full Page (Display) R 5 820 R 4 950 137 X 210 Full Page (Advertorial) R 6 650 R 5 650 137 X 210 Double Page (Display) R 9 295 R 7 900 274 X 210 Double Page (Advertorial) R 10 470 R 8 900 274 X 210 Special Advert Placements Map Feature R 1 560 R 1 325 41 X 44 Two Thirds Page 3 R 5 560 R 4 725 84 X 196 Full Page Inside Back R 6 760 R 5 745 137 X 210 Full Page Inside Front R 7 000 R 5 950 137 X 210 Back Cover R 7 960 R 6 765 137 X 210 Front Cover R 9 995 R 8 500 104 X 210 Wrapper R 15 995 R 13 600 274 X 210 Printed Ad Web Digital Edition Facebook Edition Email Newsletter A digital boost for SMMEs Did you know that Think Local offers Forever Free multi-tab websites to all small and micro businesses? In doing so, we give them access to new markets and help them achieve the efficiencies online business creates. -

DRAFT IDP Attached

BUFFALO CITY METROPOLITAN MUNICIPALITY 2019/20 DRAFT INTEGRATED DEVELOPMENT PLAN REVIEW “A City Hard at Work” Third (3rd) Review of the 2016-2021 Integrated Development Plan as prescribed by Section 34 of the Local Government Municipal Systems Act (2000), Act 32 of 2000 Buffalocity Metropolitan Municipality | Draft IDP Revision 2019/2020 _________________________________________________________________________________ Table of Content GLOSSARY OF ABBREVIATIONS 3 MAYOR’S FOREWORD 5 OVERVIEW BY THE CITY MANAGER 7 EXECUTIVE SUMMARY 9 SECTION A INTRODUCTION AND BACKGROUND 15 SECTION B SITUATION ANALYSIS PER MGDS PILLAR 35 SECTION C SPATIAL DEVELOPMENT FRAMEWORK 217 SECTION D OBJECTIVES, STRATEGIES, INDICATORS, 240 TARGETS AND PROJECTS SECTION E BUDGET, PROGRAMMES AND PROJECTS 269 SECTION F FINANCIAL PLAN 301 ANNEXURES ANNEXURE A OPERATIONAL PLAN 319 ANNEXURE B FRAMEWORK FOR PERFORMANCE 333 MANAGEMENT SYSTEM ANNEXURE C LIST OF SECTOR PLANS 334 ANNEXURE D IDP/BUDGET PROCESS PLAN FOLLOWED 337 ANNEXURE E WARD ISSUES/PRIORITIES RAISED 2018 360 ANNEXURE F PROJECTS/PROGRAMMES BY SECTOR 384 DEPARTMENTS 2 Buffalocity Metropolitan Municipality | Draft IDP Revision 2019/2020 _________________________________________________________________________________ Glossary of Abbreviations A.B.E.T. Adult Basic Education Training H.D.I Human Development Index A.D.M. Amathole District Municipality H.D.Is Historically Disadvantaged Individuals AIDS Acquired Immune Deficiency Syndrome H.R. Human Resources A.N.C₁ African National Congress H.I.V Human Immuno-deficiency Virus A.N.C₂ Antenatal Care I.C.D.L International Computer Drivers License A.R.T. Anti-Retroviral Therapy I.C.Z.M.P. Integrated Coastal Zone Management Plan A.S.G.I.S.A Accelerated Shared Growth Initiative of South Africa I.D.C. -

Rights in Principle – Rights in Practice, Revisiting the Role of International Law in Crafting Durable Solutions

Rights in Principle - Rights in Practice Revisiting the Role of International Law in Crafting Durable Solutions for Palestinian Refugees Terry Rempel, Editor BADIL Resource Center for Palestinian Residency & Refugee Rights, Bethlehem RIGHTS IN PRINCIPLE - RIGHTS IN PRACTICE REVISITING THE ROLE OF InternatiONAL LAW IN CRAFTING DURABLE SOLUTIONS FOR PALESTINIAN REFUGEES Editor: Terry Rempel xiv 482 pages. 24 cm ISBN 978-9950-339-23-1 1- Palestinian Refugees 2– Palestinian Internally Displaced Persons 3- International Law 4– Land and Property Restitution 5- International Protection 6- Rights Based Approach 7- Peace Making 8- Public Participation HV640.5.P36R53 2009 Cover Photo: Snapshots from «Go and See Visits», South Africa, Bosnia and Herzegovina, Cyprus and Palestine (© BADIL) Copy edit: Venetia Rainey Design: BADIL Printing: Safad Advertising All rights reserved © BADIL Resource Center for Palestinian Residency & Refugee Rights December 2009 P.O. Box 728 Bethlehem, Palestine Tel/Fax: +970 - 2 - 274 - 7346 Tel: +970 - 2 - 277 - 7086 Email: [email protected] Web: http://www.badil.org iii CONTENTS Abbreviations ....................................................................................vii Contributors ......................................................................................ix Foreword ..........................................................................................xi Foreword .........................................................................................xiv Introduction ......................................................................................1 -

Profile: Buffalo City

2 PROFILE: BUFFALO CITY PROFILE: BUFFALO CITY 3 CONTENT 1. Executive Summary…………………………………………………………………….3 2. Introduction: Brief Overview ............................................................................. 6 2.1 Location ..................................................................................................................................... 6 2.2 Historical Pesperctive ................................................................................................................ 6 2.3 Spatial Status ............................................................................................................................. 7 3. Social Development Profile ............................................................................... 8 3.1 Key Social Demographics ........................................................................................ 8 3.1.1 Population ............................................................................................................. 8 3.1.2 Race, Gender and Age ........................................................................................ 10 3.1.3 Households ......................................................................................................... 10 3.2 Health Profile .......................................................................................................... 11 3.3 COVID-19 .............................................................................................................. 11 3.4 Poverty Dimensions .............................................................................................. -

EPISCOPAL CHURCHPEOPLE for a FREE'southern AFRICA

E EPISCOPAL CHURCHPEOPLE for a FREE' SOUTHERN AFRICA C 339 Lafayette Street S , A Phone: (212) 477-0066 New York, N.Y. 10012 1 September 1987 FREE THE DETAINEES South Africa's State of Emergency is well into its second year. The apartheid state is steadily increasing its repression, and ~to attempt to mask the actions of the police, the military, vigilante squads and the enormous battery of implements it possesses - is pursuing an even greater censorship effort to prevent South Africans and the world popu lace from learning the extent of its depradations. Pretoria's tightening of the screws, far from giving the impression of 'stability', by its actions displays its fears and assures that the wide spread resistance is alive and still strong. Detentions are one Pretorian method. Herewith are some efforts we in the outside world can join in effecting our opposition to the repression in South Africa and in sustaining ~he resistance: Free South Africa's Children. Fill out, sign and send in the enclosed post card addressed to President P. W. Botha to the Lawyers Committee in Washington. Join the Africa Fund's Unlock Apartheid's Jails campaign by signing the enclosed form and sending in keys which will be deposited with the South African embassy in Washington. Attached is a list of names of persons detained under 'normal' Security legislation - as ascertained by the reliable Detainees' Parents Support Committee in Johannesburg. Not included are the thousands of South Africans of all ages held under the State of Emergency decree. Chose a name (or names) and send a letter demanding that person's (those persons') unconditional release to: State President P. -

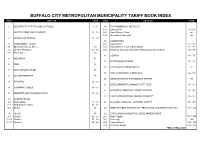

Buffalo City Metropolitan Municipality Tariff Book Index Item Service Page Item Service Page

BUFFALO CITY METROPOLITAN MUNICIPALITY TARIFF BOOK INDEX ITEM SERVICE PAGE ITEM SERVICE PAGE 1 ELECTRICITY TARIFFS AND CHARGES 1 - 11 14 ENVIRONMENTAL SERVICES 14.1 East London 63 - 65 2 WATER TARIFF AND CHARGES 11 - 20 14.2 King William's Town 66 14.3 Atmospheric Emission 66 3 SEWERAGE TARIFFS 21 - 29 15 CEMETERIES 4 ASSESSMENT RATES 15.1 East London 67 - 70 4.1 Municipal Property Rates 30 15.2 King William's Town and Breidbach 71 - 72 4.2 Uniform Flat Rates 31 - 33 15.3 Ginsberg, Dimbaza, Zwelitsha, Phakamisa & Ilitha & Bisho 72 - 73 4.3 Rates Other 33 16 LIBRARY 74 - 75 5 AQUARIUM 34 17 WASTE MANAGEMENT 76 - 80 6 ZOO 34 18 CITY HEALTH DEPARTMENT 81 7 BOAT REGISTRATION 35 19 FIRE & EMERGENCY SERVICES 82 - 84 8 NATURE RESERVE 35 20 ADMINISTRATION CHARGE-OUT TARIFFS 85 9 BEACHES 36 - 37 21 DEVELOPMENT PLANNING TARIFF FEES 85 - 91 10 SWIMMING POOLS 38 - 43 22 SCIENTIFIC SERVICES TARIFF CHARGES 92 - 95 11 RESORTS AND CARAVAN PARKS 44 - 46 23 EAST LONDON FRESH PRODUCE MARKET 96 - 97 12 SPORTSFIELDS 12.1 East London 47 - 50 24 ALL DIRECTORATES - GENERAL TARIFFS 98 - 100 12.2 King William's Town 41 - 52 12.3 Bhisho 52 25 FEES PAYABLE IN TERMS OF THE ACCESS TO INFORMATION ACT 101 - 102 13 HALLS 54 26 EAST LONDON INDUSTRIAL DEVELOPMENT ZONE 13.1 Group 1 55 - 57 26.1 Water Supply 103 - 105 13.1.4 Group 2 57 - 58 26.2 Sewerage 105 13.1.7 Group 3 59 - 62 26.3 Trade Effluent 106 - 108 26.4 Electricity Supply 108 - 109 FINAL 30 May 2018 2017/18 2017/18 2017/18 2018/19 2018/19 2018/19 Total VAT Total Total VAT Total Item Code Service R/cents R/cents R/cents R/cents R/cents R/cents Excl VAT 14% VAT Incl. -

A Situation Analysis of Water Quality in the Catchment of the Buffalo River, Eastern Cape, with Special Emphasis on the Impacts

A SITUATION ANALYSIS OF WATER QUALITY IN THE CATCHMENT OF THE BUFFALO RIVER, EASTERN CAPE, WITH SPECIAL EMPHASIS ON THE IMPACTS OF LOW COST, HIGH-DENSITY URBAN DEVELOPMENT ON WATER QUALITY VOLUME 2 (APPENDICES) FINAL REPORT to the Water Research Commission by Mrs C.E. van Ginkel Dr J. O'Keeffe Prof D.A.Hughes Dr J.R. Herald Institute Tor Water Research, Rhodes University and Dr P.J. Ashton Environmentek, CSIR WRC REPORT NO. 40S/2/96 ISBN NO. 1 86845 287 5 ISBN SET NO. 1 86845 288 3 Water Research. Commission Buffalo River Project EXECUTIVE SUMMARY 1. Introduction and aims of the project The Buffalo River provides water and a conduit for effluent disposal in one of the most populous areas on the East coast of southern Africa. The catchment supports a rapidly-growing population of 311 000 people, in which King William's Town, Zwelitsha, Mdantsane and East London are the mam towns, and they are all supplied with water from the river. The management of the river is complicated by the political division of the catchment between Ciskei and South Africa (figure 1.1), but a joint agreement makes provision for the formation of a Permanent Water Commission for coordinating the management of the river's resources. The river rises in the Amatole Mountains and flows South-East for 125 km to the sea at East London (figure 1.1). It can be divided into three reaches: The upper reaches to King William's Town, comprising the mountain stream in montane forest down to Maden Dam, and the foothill zone flowing through agricultural land downstream of Rooikrans Dam; the middle reaches, comprising the urban/industrial complex of King William's Town/Zwelitsha to Laing Dam, and an area of agricultural land downstream of Laing; and the lower reaches downstream of Bridle Drift Dam, comprising coastal forest and the estuary, which forms East London's harbour. -

King Williams Town Education District I Z V IE I Tylden R MIDDLE XOLOBE JS JOJWENI 4 NTSELA Intsika Yethu Local Municipality ZWELIVUMILE SS

1 4 2 3 1 4 2 3 G 1 8 U 1 8 G U T LA O LU B 3 U O UPPER NQOLOSA JS ESIKOLWENI 3 NY Y 11 22 I NDLOVUKAZI JP TOBOYI K NQOLOSA W U MDANTSANE 22 33 IT B - A KE KWANANGCANGCAZELA 2 0 IR N 2 0 King Williams Town Education District I Z V IE I Tylden R MIDDLE XOLOBE JS JOJWENI 4 NTSELA Intsika Yethu Local Municipality ZWELIVUMILE SS R ESIXHOTYENI N E H MZAMOMHLE JP FAIRVIEW JP I G O O 1 6 V X 1 6 I W M H NOMZAMO SP CENU R I A O I T KWAJIM E S S R H A T K E - U I T R V I I E I W BABA ROAD R V NOLUSAPHO SP T NQOLOSA JS I A R Z I A MBHONGISENI O L E BORDERLINE/KOMKHULU L K P A - S BENGU JS NI O P I N T I W O UD OM L L R MPIKWANA JS A O UB H K G E A Q SI YA N JOJWENI 3 W S MKHANYENI KWAKHOZA SAJINI JS A X AN MADAM E AL E NK 11 55 B S O A L N R 11 66 E Lukanji Local Municipality O D A IN Whittlesea E 1 3 IN I 1 3 X NCIS V I R E 11 99 D E I IN N K K I - KWA JACK 2 T S U G I T CAMPBELL MNYHILA JP S C Z C O N O E I B M O A KWA JACK 1 A 11 33 O R S L G O G O MZAMOMHLEJOJO JS C L M I M B B A O U A A G LU L N N A LA 11 77 U E XOLOBA O K U 1 8 Q G NKALWENI BENGU M O AK 1 8 A R O P MTW W O X 22 00 O U T L - BLY NGCONGOLO JP K A E G N 11 77 IR R I O A V O Y I T LAMTHOLE E - KENSINGTON T R K E CULU E IR SONKOSI JS NG B I V E IE Nqamakwe Bacela R G N KHUZE NKQUBELA JS CENYU NGXALAWA KANYISA SP MATOLWENI TEMBENI JS MCHEWULA 2 A B MCHEWULA 1 A Mbulukweza Clinic C BE A E N FUBU BE-H MBULUKWEZA HE A K A GCIBHALA MAGWATYUZENI D A N B 11 33 H A E 1 5 C B 1 5 CABA JS LUXOMO E A DUBUKAZI - CABA COMPREHENSIVE NDEMA SS H N E A I B K T DUMEZWENI J S S KWAMFULA 1 A N A -

View the Latest Issue of Yakha

ISSUE 14 2021 STANDING UP HAVE YOUR YOUTH SAY TOGETHER RELATIONSHIPS FASHION OUT BUMB'INGOMSO WORKLINK PRESENTS: dreamXchange is a WEB PORTAL that connects people with other people by offering simple, user-friendly functionality through which ANYONE can share work opportunities, training and tools of the trade, to help EVERYONE become economically active. Visit www.dreamxchange.co.za and be a part of the wave. WHAT’S INSIDE FEATURES THE TEAM COVER STORY Relationships 06 EDITOR Spokazi Tyiwani #BEMORE Generous in Spirit 09 EDITOR-IN-CHIEF Angela Stewart-Buchanan FEATURE Standing up 10 YAKHA is produced by EDITORIAL TEAM Aphiwe Ntlemeza, IKHWELOLETHU Friends 14 Bumb’INGOMSO, a multi- Libhongo Ntoyam, Lindokuhle Msele, EMPLOYMENT Job Journey 22 faceted project that supports Unolali, Siseko Maposa and Xolelwa Pona WORK Remote work 23 and empowers young women ENTREPRENEUR Bizzy Acwesh 24 to fulfil their potential. CONTRIBUTORS HEALTH Safe Sex 28 Bumb’INGOMSO, is a Xhosa CREATIVE OPENFORM.co.za LEADERSHIP 30 phrase that means “mould the PRINTERS Novus Print CHANGEMAKER Yonela Mpetsheni 32 future”. WRITERS Kay Lani, Portia Jonas and FINANCE Informal Lending 33 Yonela Mpetsheni We envision a Buffalo City where young people are connected to key resources, COVER + COVER FEATURE support and networks to help STAR Phelisa Gcanga them thrive academically, in PHOTOGRAPHER 0077 Multi-Media their health and economically. STYLIST Unolali MAKEUP Nuvo Ink PTY LTD Bumb’INGOMSO is a development project of the National Department of Health ADVERTISING co-financed by the Federal To advertise in YAKHA call Republic of Germany through SPOKAZI TYIWANI KfW and DGMT, which is also (043) 721 0055 the executing agent. -

Accredited COVID-19 Vaccination Sites Eastern Cape

Accredited COVID-19 Vaccination Sites Eastern Cape Permit Primary Name Address Number 202103960 Fonteine Park Apteek 115 Da Gama Rd, Ferreira Town, Jeffreys Bay Sarah Baartman DM Eastern Cape 202103949 Mqhele Clinic Mpakama, Mqhele Location Elliotdale Amathole DM Eastern Cape 202103754 Masincedane Clinic Lukhanyisweni Location Amathole DM Eastern Cape 202103840 ISUZU STRUANWAY OCCUPATIONAL N Mandela Bay MM CLINIC Eastern Cape 202103753 Glenmore Clinic Glenmore Clinic Glenmore Location Peddie Amathole DM Eastern Cape 202103725 Pricesdale Clinic Mbekweni Village Whittlesea C Hani DM Eastern Cape 202103724 Lubisi Clinic Po Southeville A/A Lubisi C Hani DM Eastern Cape 202103721 Eureka Clinic 1228 Angelier Street 9744 Joe Gqabi DM Eastern Cape 202103586 Bengu Clinic Bengu Lady Frere (Emalahleni) C Hani DM Eastern Cape 202103588 ISUZU PENSIONERS KEMPSTON ROAD N Mandela Bay MM Eastern Cape 202103584 Mhlanga Clinic Mlhaya Cliwe St Augustine Jss C Hani DM Eastern Cape 202103658 Westering Medicross 541 Cape Road, Linton Grange, Port Elizabeth N Mandela Bay MM Eastern Cape Updated: 30/06/2021 202103581 Tsengiwe Clinic Next To Tsengiwe J.P.S C Hani DM Eastern Cape 202103571 Askeaton Clinic Next To B.B. Mdledle J.S.School Askeaton C Hani DM Eastern Cape 202103433 Qitsi Clinic Mdibaniso Aa, Qitsi Cofimvaba C Hani DM Eastern Cape 202103227 Punzana Clinic Tildin Lp School Tildin Location Peddie Amathole DM Eastern Cape 202103186 Nkanga Clinic Nkanga Clinic Nkanga Aa Libode O Tambo DM Eastern Cape 202103214 Lotana Clinic Next To Lotana Clinic Lotana -

East London Education District

MKHONJANI NYABAVU MAZOTSHWENI XHOBANI QOBOQOBO SOMANA NKUKWANE GODIDI KWATHYAU NXAXHA KWANOBUSWANA GOJELA 2 4 MMANGWENI A GQUNQE QORA1 6 11 55 HECKEL KWABINASE EBHITYOLO 2 4 QIN GOBE MANUBE MANUBI 1 6 K LU MQAMBILE 11 00 SIZI LUSIZI GQUNQE Mbhashe Local Municipality ENGQANDA W S ANE A I TSIM K H A MANTETYENI N DIKHOHLONG N L WARTBURG I U LUSIZI GCINA O SEMENI NXAXHO B G O 1 4 L C GQUNQE Q N GCINA LUKHOLWENI 1 4 L HLANGANI GOBE NTILINI W A Qina Clinic G 44 O KWAMANQULU A T N R L RAWINI W I A Mgwali Clinic GOBE Z POTHLO W G 2 3 NTSHONGWENI E R Springs Clinic 2 3 NXQXHO M HLANGANI N E MGWALI GQUNQE I N V G G GCINA E I R GOBE NXAXHO B O EMAHLUBINI MAFUSINI SIGANGENI O E R O KOBODI INDUSTRIAL VIKA LE E T D CEBE CHEBE L T - LUSIZI MATEYISI GCINA E S I GQUNQE O K NCIBA GOBE I E MPHUMLANI DYOSINI KOBODI THEMBANI D I O I GODIDI R I S I T V A NJINGINI E I ER KOBODI A L 2 2 MANZAMA A R 2 2 NTINDE G I TOL E M V NI NDUVENI N E NXAXHO A N LA NDUBUNGE LUSIZI R N G Y Y X MATSHONA I LUSIZI A A O S S X T N KEI BRIDGE 66 GCINA GCINA I W A NTSANGANE H 11 R A A A Macibe Clinic ZIBUNU GQUNQE GCINA E R N S L IV ENTLEKISENI K M DLEPHU A E H KWA NGWANE COLUMBA MISSION O R U I U I MACIBE LUSIZI LU N E L B Q M SI GQ S A K Z U T I I I NQ O W U KOBODI B MACIBE E G O L MAZZEPA BAY T S G D A E M B C CI M W I Q E A B CHEBE M I KWATHALA MACIBE SINTSANA A N E U B O U NKENTE B O N N L X O N E B C E I K A K 7 Q G G MNYAMENI 7 Ngqusi Clinic U MNYAMA M U X Q KOBODI D 99 R A B MACIBE O O GQUNQE O O B U EDRAYINI BO KOMKHULU MB D L I O AZELA A O S DLEPHU B T N BUSY VILLAGE N -

Draft Integrated Development Plan Review 2009-2010

DRAFT INTEGRATED DEVELOPMENT PLAN REVIEW 2009-2010 The Executive Mayor Amathole District Municipality P O Box 320 East London Tel: 043 701 4000 Fax: 043 743 9050 Website: www.amathole.gov.za TABLE OF CONTENTS PAGE EXECUTIVE SUMMARY Background to the document 3 ADM Cluster approach 3 Report outline 4 SECTION A: THE PLANNING PROCESS 1.0 IDP Review process 5 1.1 Organizational arrangements 6 1.2 Schedule of meetings 7 1.3 Relevant documents 10 SECTION B: THE SITUATIONAL ANALYSIS 2.0 Introduction 12 2.1 Analysis overview 12 2.1.1 Introduction 12 2.1.2 Demographic overview 13 2.1.3 Economic overview 23 2.1.4 Cluster overview 26 2.1.4.1 LED & Environment overview 26 2.1.4.2 Infrastructure overview 44 2.1.4.3 Institution & Finance overview 73 2.1.4.4 Social Needs overview 104 SECTION C: CLUSTER OBJECTIVES, STRATEGIES & PROJECTS 3.0 The Municipal Vision, Mission and Values 126 3.1 Institution & Finance cluster 127 3.1.1 Good governance and public participation objectives and strategies 127 3.1.2 Good governance and public participation projects and programs 131 3.1.3 Municipal transformation and organizational development 132 objectives and strategies 3.1.4 Municipal transformation and organizational development 136 projects and programs 3.1.5 Financial viability and management objectives and strategies 137 3.1.6 Financial viability and management projects and programs 138 3.2 Infrastructure cluster 139 3.2.1 Water services objectives and strategies 139 3.2.2 MIG Projects 140 3.2.3 Solid waste objectives and strategies 144 3.2.4 Roads and transport