Last Chance to TAP Into DLS! BLA Hires Two New Field Advisors

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Family Group Sheets Surname Index

PASSAIC COUNTY HISTORICAL SOCIETY FAMILY GROUP SHEETS SURNAME INDEX This collection of 660 folders contains over 50,000 family group sheets of families that resided in Passaic and Bergen Counties. These sheets were prepared by volunteers using the Societies various collections of church, ceme tery and bible records as well as city directo ries, county history books, newspaper abstracts and the Mattie Bowman manuscript collection. Example of a typical Family Group Sheet from the collection. PASSAIC COUNTY HISTORICAL SOCIETY FAMILY GROUP SHEETS — SURNAME INDEX A Aldous Anderson Arndt Aartse Aldrich Anderton Arnot Abbott Alenson Andolina Aronsohn Abeel Alesbrook Andreasen Arquhart Abel Alesso Andrews Arrayo Aber Alexander Andriesse (see Anderson) Arrowsmith Abers Alexandra Andruss Arthur Abildgaard Alfano Angell Arthurs Abraham Alje (see Alyea) Anger Aruesman Abrams Aljea (see Alyea) Angland Asbell Abrash Alji (see Alyea) Angle Ash Ack Allabough Anglehart Ashbee Acker Allee Anglin Ashbey Ackerman Allen Angotti Ashe Ackerson Allenan Angus Ashfield Ackert Aller Annan Ashley Acton Allerman Anners Ashman Adair Allibone Anness Ashton Adams Alliegro Annin Ashworth Adamson Allington Anson Asper Adcroft Alliot Anthony Aspinwall Addy Allison Anton Astin Adelman Allman Antoniou Astley Adolf Allmen Apel Astwood Adrian Allyton Appel Atchison Aesben Almgren Apple Ateroft Agar Almond Applebee Atha Ager Alois Applegate Atherly Agnew Alpart Appleton Atherson Ahnert Alper Apsley Atherton Aiken Alsheimer Arbuthnot Atkins Aikman Alterman Archbold Atkinson Aimone -

Surnames Beginning With

Card# MineName Operator Year Month Day Surname First and Middle Name Age Fatal/Nonfatal In/Outside Occupation Nationality Citizen/Alien Single/Married #Children Mine Experince Occupation Exp. Accident Cause or Remarks Fault County Mining Dist. Film# CoalType 14 Vesta No.4 Vesta Coal 1937 2 18 Babak Frank 28 nonfatal inside brakeman Slavic single thumb caught between car bumpers Washington 21st 3600 bituminous 32 Elma No.3 Baker Whitely Coal 1938 6 14 Babalanis William 18 nonfatal inside machine miner single rock broke & fell on foot heading Somerset 24th 3601 bituminous 7 Elma No.3 Baker Whitely Coal 1937 2 2 Babalonis Charles 29 nonfatal inside scraper Lithuanian citizen single foot caught under machine unloading Somerset 24th 3600 bituminous 117 Somers Pittsburgh Coal 1937 11 2 Babar Louis 35 nonfatal inside machine miner Hungarian married fall of slate in room Fayette 9th 3600 bituminous 12 Isabella Weirton Coal 1938 5 6 Babba Harry M 46 nonfatal inside married hernia lifting timber rail room Fayette 16th 3600 bituminous 33 Colonial No.3 H C Frick Coke 1939 6 24 Babchak John J 25 nonfatal inside brakeman married caught foot in clevices broke foot Fayette 9th 3601 bituminous 66 Heisley No.3 Heisley Coal 1937 9 22 Baber Louis 20 nonfatal inside machine miner Slavic single loose strand in hoist rope hit thumb Cambria 10th 3600 bituminous 91 Springfield No.1 Springfield Coal 1939 10 27 Babich Walter 57 nonfatal inside miner married caught car & roof broke hand Cambria 10th 3601 bituminous 5 Big Bend Big Bend Coal Mining 1942 9 28 Babinscak -

Using 21St Century Science to Improve Risk-Related Evaluations (2017)

THE NATIONAL ACADEMIES PRESS This PDF is available at http://nap.edu/24635 SHARE Using 21st Century Science to Improve Risk-Related Evaluations (2017) DETAILS 200 pages | 8.5 x 11 | PAPERBACK ISBN 978-0-309-45348-6 | DOI 10.17226/24635 CONTRIBUTORS GET THIS BOOK Committee on Incorporating 21st Century Science into Risk-Based Evaluations; Board on Environmental Studies and Toxicology; Division on Earth and Life Studies; National Academies of Sciences, Engineering, and Medicine FIND RELATED TITLES SUGGESTED CITATION National Academies of Sciences, Engineering, and Medicine 2017. Using 21st Century Science to Improve Risk-Related Evaluations. Washington, DC: The National Academies Press. https://doi.org/10.17226/24635. Visit the National Academies Press at NAP.edu and login or register to get: – Access to free PDF downloads of thousands of scientific reports – 10% off the price of print titles – Email or social media notifications of new titles related to your interests – Special offers and discounts Distribution, posting, or copying of this PDF is strictly prohibited without written permission of the National Academies Press. (Request Permission) Unless otherwise indicated, all materials in this PDF are copyrighted by the National Academy of Sciences. Copyright © National Academy of Sciences. All rights reserved. Using 21st Century Science to Improve Risk-Related Evaluations USING 21ST CENTURY SCIENCE TO IMPROVE RISK-RELATED EVALUATIONS Committee on Incorporating 21st Century Science into Risk-Based Evaluations Board on Environmental Studies and Toxicology Division on Earth and Life Studies A Report of Copyright National Academy of Sciences. All rights reserved. Using 21st Century Science to Improve Risk-Related Evaluations THE NATIONAL ACADEMIES PRESS 500 Fifth Street, NW Washington, DC 20001 This activity was supported by Contract EP-C-14-005, TO#0002 between the National Academy of Sciences and the US Environmental Protection Agency. -

Brooklyn College Foundation ANNUAL REPORT 2015/2016 Brooklyn College Foundation 2015–2016 Annual Report

2015 –2016 Annual Report Brooklyn College Foundation ANNUAL REPORT 2015/2016 Brooklyn College Foundation 2015 –2016 Annual Report Dear Alumni and Friends, Dear Alumni and Friends, Welcome to the Brooklyn College Foundation’s FY16 Annual Report, covering the period from July 1, 2015, through June 30, 2016. This was a year of transition. We wrapped up our $200 million Foundation for Success Campaign, bid farewell to retiring President Karen Gould — who provided Brooklyn College with seven years of exceptional leadership — and welcomed our new president, Michelle Anderson. President Anderson comes to Brooklyn College from her previous position as dean of the CUNY School of Law, where she oversaw a period of great renewal and transformation in facilities, programs, and recognition. We on the foundation board are excited to work with her on our mutual mission to continue to provide affordable access to excellent higher education. This year’s report focuses on the impact of key donor gifts as well as the work of the foundation as we prepare for our next capital campaign. I am exceedingly proud that during FY16, the foundation provided more than $2 million to nearly 1,500 students in the form of scholarships, awards, travel grants, internships, fellowships, and emergency grants; and, for faculty, more than $450,000 in the form of professorships, chairs, travel awards, lectureships, and professional development support. All of us at the foundation are grateful to the more than 5,000 donors who share our steadfast commitment to Brooklyn College, its mission, and its students. Sincerely, Edwin H. Cohen ’62 Chair, Brooklyn College Foundation Brooklyn College Foundation 2 3 Brooklyn College Foundation 2015 –2016 Annual Report Dear Alumni and Friends of Brooklyn College, When he laid the cornerstone for the gymnasium building on our beautiful campus, President Franklin D. -

Russian Military Capability in a Ten-Year Perspective 2016

The Russian Armed Forces are developing from a force primarily designed for handling internal – 2016 Perspective Ten-Year in a Capability Military Russian disorder and conflicts in the area of the former Soviet Union towards a structure configured for large-scale operations also beyond that area. The Armed Forces can defend Russia from foreign aggression in 2016 better than they could in 2013. They are also a stronger instrument of coercion than before. This report analyses Russian military capability in a ten-year perspective. It is the eighth edition. A change in this report compared with the previous edition is that a basic assumption has been altered. In 2013, we assessed fighting power under the assumption that Russia was responding to an emerging threat with little or no time to prepare operations. In view of recent events, we now estimate available assets for military operations in situations when Russia initiates the use of armed force. The fighting power of the Russian Armed Forces is studied. Fighting power means the available military assets for three overall missions: operational-strategic joint inter-service combat operations (JISCOs), stand-off warfare and strategic deterrence. The potential order of battle is estimated for these three missions, i.e. what military forces Russia is able to generate and deploy in 2016. The fighting power of Russia’s Armed Forces has continued to increase – primarily west of the Urals. Russian military strategic theorists are devoting much thought not only to military force, but also to all kinds of other – non-military – means. The trend in security policy continues to be based on anti- Americanism, patriotism and authoritarianism at home. -

The List for Surnames by Towns in Bessarabia

Surnames in 19th century revision lists for towns in Bessarabia Compiled from data extracted by the Bessarabia Special Interest Group for the JewishGen Romania & Moldova Database www.http://www.jewishgen.org/Bessarabia http://www.jewishgen.org/databases/Romania How to use this document This list can be helpful in finding a surname that did not turn up in a search of the JewishGen database because the spelling differs significantly from what you entered in the search field, despite using "sounds like," phonetic, fuzzy and other search methods. It is organized by town. Numbers show how many times a given surname appears in in lists extracted for a given town. Data for this document came from lists for various years between 1824 and 1875, processed as of August 2015. Use the alphabetical links below to jump down. B C G I K L M P R S T V Abaklydzhaba village 6 Abaklydzhaba village 6 Abaklydzhaba village 6 Surname Entries Surname Entries Surname Entries KAUSHANSKIY 3 KOGAN 1 MELAMED/LUPU 2 Aleksandreny Colony 1748 Aleksandreny Colony 1748 Aleksandreny Colony 1748 Surname Entries Surname Entries Surname Entries ALEYVI 11 GERSHINKROYN 12 KREYMAR 9 ALTMAN 11 GERTS 13 KUSHNIR 5 ANBINDER 9 GINBERG 12 LANDER 32 AVERBUKH 16 GLEYZER 13 LANFIR 5 AYZIN 5 GLUZMAN 10 LEMLIKH 11 AZINBERG 4 GOFMAN 10 LERNER 3 BARDICHEVER 6 GOIKHMAN 4 LEVIV 4 BARG 7 GOLDBERG 13 LITVAK 5 BARIR 15 GOLDENBERG 15 LIVERANT 17 BATUSHANSKY 9 GOLDENER 12 LOBER 11 BEIN 7 GOLDFARB 9 LOYZGOLD 17 BENDERSKY 26 GOLDINBERG 13 MAGIDMAN 6 BENDIT 7 GOLDMAN 7 MALAMUD 10 BENIKHIS 5 GOLDYAK -

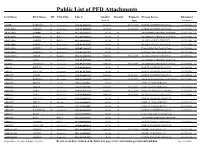

Public List of PFD Attachments

Public List of PFD Attachments Last Name First Name MI Court Site Case # Amount Reason* Payment Process Server Document Seized Date Locator # ABAIR BARBARA J Anchorage 3AN-15-07567CI $880.00 09/23/2017 NORTH COUNTRY PROCESS 2017042963 2 ABALAMA AMBER R Anchorage 3AN-10-00200SC $819.50 09/23/2017 NORTH COUNTRY PROCESS 2017011036 4 ABALAMA AMBER R Palmer 3PA-10-02623CI $0.00 B ATTORNEYS PROCESS SERVICE 2017011036 4 ABALAMA AMBER R Palmer 3PA-10-02623CI $0.00 B ATTORNEYS PROCESS SERVICE 2017011036 4 ABALAMA AMBER R Palmer 3PA-10-00783SC $0.00 B ALASKA COURT SERVICES 2017011036 4 ABALAMA SHIRELL F Anchorage 3AN-02-02749SC $0.00 B ALASKA COURT SERVICES 2017058060 0 ABALAMA SHIRELL F Anchorage 3AN-05-11010CI $0.00 B Certified Mail By Clerk Of Court 2017058060 0 ABALAMA SHIRELL F Anchorage 3AN-01-06487CI $0.00 B INQUEST PROCESS SERVICE 2017058060 0 ABALANZA JOMER T Kodiak 3KO-15-00018SC $880.00 09/23/2017 ALASKA COURT SERVICES 2017054462 8 ABANG TERA Anchorage 3AN-05-01894SC $0.00 A ATTORNEYS PROCESS SERVICE ABARO CHANELLE M Anchorage 3AN-09-02177SC $880.00 09/23/2017 ATTORNEYS PROCESS SERVICE 2017049038 9 ABBAS PHYLLIS A Anchorage 3AN-08-05753CI $0.00 B NORTH COUNTRY PROCESS 2017066584 3 ABBAS PHYLLIS A Anchorage 3AN-06-03730SC $0.00 B NORTH COUNTRY PROCESS 2017066584 3 ABBOTT ANGEL Anchorage 3AN-17-00537SC $506.04 09/23/2017 NORTH COUNTRY PROCESS 2017047984 4 ABBOTT BRENNA N Ketchikan 1KE-13-00007SC $880.00 10/20/2017 SEAK PROFESSIONAL SERVICES LLC2017012534 2 ABBOTT BRIAN L Juneau 1JU-12-00027SC $0.00 A CIVIL CLAIMS SERVICE ABBOTT CHLOE Juneau -

AKRON BEACON JOURNAL Index to Obituaries

AKRON BEACON JOURNAL Index to Obituaries 1985-1989 I Akron-Summit County Public Library Compiled by the the staff of the Language, Literature and History Division NAME DATE Abbott, Elizabeth K. 3-21 -88 Abbott, Franz D. 3-1 5-89 Abbott, John L. 2-1 6-88 Abbott, Madeline A. 7-18-86 Abbott, Nellie 2-1 3-85 Abbot , William F. 11-5-87 Abbuh , Robert Lee 12-6-86 Abbuh , Steven N. 1-7-89 Abdoo Florence C. 9-3-85 Abel, Glenn R. 11-27-86 Abel, Robert A. 9-29-87 Abele Beulah 9-1 3-86 Abell, James 2-1 -85 Abell, Mary A. 8-24-85 Abell, Ruth D. 2-8-87 Abell, Virgie M. 2-20-85 Abell, William I. 5-10-86 Abels, Ruth 10-29-86 Abercrombie, Dorothy A. 6-25-86 Aberegg, Paul 9-1 4-89 Abernathy, Elmo B. 3-29-89 Abernathy, John H. 3-1 4-88 Abernathy, Minnie I. 9-8-87 Abernathy, Myrtle L. 7-31~~ -86~~ Abicht, Jean 10-1 3-87 Ablett, Edith M. 6-30-87 Abmyer, Mary 4-2-85 Abraham, Daniel M. 6-1 5-86 Abraham, Flossie 10-31-87 Abraham, Louis 10-30-88 Abraham, Ruth 8-1 5-86 Abram, John R. 3-29-88 Abramchuk, Rose 11-1 3-86 Abrams, Ida M. 9-21 -85 Abrams, Mary E. 7-19-86 Abrams, W. J. 5-1 8-89 Abreu, Arnaldo J. 4-1 9-88 Abshire, Donald L. 11-4-86 Abshire, Gertrude G. -

Using 21St Century Science to Improve Risk-Related Evaluations

THE NATIONAL ACADEMIES PRESS This PDF is available at http://www.nap.edu/24635 SHARE Using 21st Century Science to Improve Risk-Related Evaluations DETAILS 260 pages | 6 x 9 | PAPERBACK ISBN 978-0-309-45348-6 | DOI: 10.17226/24635 AUTHORS BUY THIS BOOK Committee on Incorporating 21st Century Science into Risk-Based Evaluations; Board on Environmental Studies and Toxicology; Division on Earth and Life Studies; National Academies of Sciences, FIND RELATED TITLES Engineering, and Medicine Visit the National Academies Press at NAP.edu and login or register to get: – Access to free PDF downloads of thousands of scientific reports – 10% off the price of print titles – Email or social media notifications of new titles related to your interests – Special offers and discounts Distribution, posting, or copying of this PDF is strictly prohibited without written permission of the National Academies Press. (Request Permission) Unless otherwise indicated, all materials in this PDF are copyrighted by the National Academy of Sciences. Copyright © National Academy of Sciences. All rights reserved. Using 21st Century Science to Improve Risk-Related Evaluations PREPUBLICATION COPY Using 21st Century Science to Improve Risk-Related Evaluations ADVANCE COPY NOT FOR PUBLIC RELEASE BEFORE Thursday, January 5, 2017 11 a.m. EDT This prepublication version has been provided to the public to facilitate timely access to the committee’s findings. Although the substance of the report is final, editorial changes will be made throughout the text, and citations will be checked prior to publication. Copyright © National Academy of Sciences. All rights reserved. Using 21st Century Science to Improve Risk-Related Evaluations Copyright © National Academy of Sciences. -

Noms De Famille Issus De L'artisanat En France Et En Pologne

ROCZNIKI HUMANISTYCZNE Tom LXVII, zeszyt 8 – 2019 DOI: http://dx.doi.org/10.18290/rh.2019.67.8-5 IWONA PIECHNIK1 NOMS DE FAMILLE ISSUS DE L’ARTISANAT EN FRANCE ET EN POLOGNE SURNAMES FROM ARTISAN NAMES IN FRANCE AND IN POLAND Abstract The article analyses surnames originating from artisan names in France and in Poland. It presents their origins (including foreign influences), types and word formation. We can see, among other things, that the French surnames are shorter, but have many dialectal variants, while the Polish surnames are longer and have a richer derivation. The article also focuses on demographic statis- tics of such surnames in both countries: the blacksmith as an etymon is the most popular. In the top 50, there are also in France: baker, miller and mason; while in Poland: tailor and shoemaker. Key words: family names; surnames; patronyms; handicraft; artisan. Les plus anciens noms de famille issus des domaines de l’artisanat en France et en Pologne remontent au Moyen Âge, donc à l’époque où le sys- tème féodal se renforçait et les villes commençaient à se développer, en nourrissant surtout les ambitions des nobles de construire leurs demeures seigneuriales, et des gens de petits métiers venaient s’installer tout autour naturellement. Dans des bourgs, c’est-à-dire dans de gros villages où se te- naient ordinairement des marchés, les bourgeois bénéficiaient d’un statut privilégié et développaient le commerce et la conjoncture de la manufacture, donc il y avait aussi beaucoup de travail pour différents métiers. C’est juste- ment dans les bourgs et les villes que l’artisanat se développait le mieux, en 1 Dr hab. -

Family History Index

Family History Index Alternate First Spouse's Alternate Spouse's Surname Surname First Name Name(s) First Name First Surname Book Title Page # 3R's Gray R. Trails to Mannville 477 Aabak Ole Astrid Voices of Yesteryears: Vilna 225 Aarbo G. Trails to Mannville 304 Aaserud Berger Joy Gray Along Victoria Trail: Lamont 230 Abbott W. History of Greater Vegreville 118 Abbott Jack Memories of Mundare 173 Abbs R. A. M. Trails to Mannville 304 Abramic John Anne Slevinsky Down Memory Trails: Two Hills 675 Achtem Sam Anne Pride in Progress: Chipman, St. Michael, Edna/Star 244 Achtemichuk Andrew A Voice From the Wilderness 14, 18 Achtemichuk Peter Elaine Between River and Lake: Warspite 115 Achtemichuk Dymetro Jim By River and Trail: Waskatenau 548 Achtemichuk Mike By River and Trail: Waskatenau 548 Achtemichuk Paul Brenda By River and Trail: Waskatenau 548 Achtemichuk William By River and Trail: Waskatenau 548 Achtemichuk Alex Memories of Mundare 174 Achtemichuk Dan Anastasia Pride in Progress: Chipman, St. Michael, Edna/Star 242 Achtemichuk Harry Annie Pride in Progress: Chipman, St. Michael, Edna/Star 244 Achtemichuk John Verna Pride in Progress: Chipman, St. Michael, Edna/Star 241 Achtemichuk John Annie Pride in Progress: Chipman, St. Michael, Edna/Star 243 Achtemichuk Mike Mary Pride in Progress: Chipman, St. Michael, Edna/Star 243 Achtemichuk Paul Cassie Pride in Progress: Chipman, St. Michael, Edna/Star 244 Achtemichuk Tom Anna Pride in Progress: Chipman, St. Michael, Edna/Star 239 Achtemichuk Wasyl Pride in Progress: Chipman, St. Michael, Edna/Star 245 Achtemichuk Achtymijczuk, Andrew Andrij Maria Marcischuk Ukrainian Canadian Biography 21 Achtemichuk Achtymijczuk, Anton Irena Ukrainian Canadian Biography 22 Achtemichuk Achtymijczuk, Wasyl Basil Maria Achtemichuk Ukrainian Canadian Biography 24 Achtemichuk T. -

To St. Louis, Missouri Naturalization Records Created After Sept. 27, 1906

Index to St. Louis, Missouri Naturalization Records Created after Sept. 27, 1906 Alphabetical surname index A–D History & Genealogy Department St. Louis County Library 1640 S. Lindbergh Blvd. St. Louis, Missouri 63131 314-994-3300, ext. 2070 [email protected] Index to St. Louis, Missouri Naturalization Records Created after Sept. 27, 1906 This index covers St. Louis, Missouri naturalization records created between October 1, 1906 and December 1928 and is based on the following sources: • Naturalizations, U.S. District Court—Eastern Division, Eastern Judicial District of Missouri, Vols. 1 – 82 • Naturalizations, U.S. Circuit Court— Eastern Division, Eastern Judicial District of Missouri, Vols. 5 – 21 Entries are listed alphabetically by surname, then by given name, and then numerically by volume number. Abbreviations and Notations SLCL = History and Genealogy Department microfilm number (St. Louis County Library) FHL = Family History Library microfilm number * = spelling taken from the signature which differed from name in index. How to obtain copies Photocopies of indexed articles may be requested by sending an email to the History and Genealogy Department at [email protected]. A limit of three searches per request applies. Please review the library's lookup policy at https://www.slcl.org/genealogy-and-local- history/services. A declaration of intention may lead to further records. For more information, contact the National Archives at the address below. Include all information listed on the declaration of intention. National Archives, Central Plains Region 400 W. Pershing Rd. Kansas City, MO 64108 (816) 268-8000 [email protected] History Genealogy Dept. Index to St. Louis, Missouri Naturalization Records St.