Dubai: the War of the Villas

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Urban Megaprojects-Based Approach in Urban Planning: from Isolated Objects to Shaping the City the Case of Dubai

Université de Liège Faculty of Applied Sciences Urban Megaprojects-based Approach in Urban Planning: From Isolated Objects to Shaping the City The Case of Dubai PHD Thesis Dissertation Presented by Oula AOUN Submission Date: March 2016 Thesis Director: Jacques TELLER, Professor, Université de Liège Jury: Mario COOLS, Professor, Université de Liège Bernard DECLEVE, Professor, Université Catholique de Louvain Robert SALIBA, Professor, American University of Beirut Eric VERDEIL, Researcher, Université Paris-Est CNRS Kevin WARD, Professor, University of Manchester ii To Henry iii iv ACKNOWLEDGMENTS My acknowledgments go first to Professor Jacques Teller, for his support and guidance. I was very lucky during these years to have you as a thesis director. Your assistance was very enlightening and is greatly appreciated. Thank you for your daily comments and help, and most of all thank you for your friendship, and your support to my little family. I would like also to thank the members of my thesis committee, Dr Eric Verdeil and Professor Bernard Declève, for guiding me during these last four years. Thank you for taking so much interest in my research work, for your encouragement and valuable comments, and thank you as well for all the travel you undertook for those committee meetings. This research owes a lot to Université de Liège, and the Non-Fria grant that I was very lucky to have. Without this funding, this research work, and my trips to UAE, would not have been possible. My acknowledgments go also to Université de Liège for funding several travels giving me the chance to participate in many international seminars and conferences. -

Implementing Sustainable Construction Practices in Dubai – a Policy Instrument Assessment

Master Thesis in Built Environment (15 credits) Implementing Sustainable Construction Practices in Dubai – a policy instrument assessment Marco Maguina Academic Supervisor: Catarina Thormark Spring Semester 2011 Master Thesis in Built Environment Implementing Sustainable Construction Practices in Dubai – a policy instrument assessment Author: Marco Maguina Faculty: Culture and Society School: Malmö University Master Thesis: 15 credits Academic Supervisor: Catarina Thormark Examiner: Johnny Kronvall Maguina, Marco 2 Master Thesis in Built Environment SUMMARY Recognized as one of the main obstacles to sustainable development, climate change is caused and accelerated by the greenhouse gas (GHG) emissions generated from all energy end-user sectors. The building sector alone consumes around 40% of all produced energy worldwide. Reducing this sector’s energy consumption has therefore come into focus as one of the key issues to address in order to meet the climate change challenge. Implementing sustainable construction practices, such as LEED, can significantly reduce the building’s energy and water consumption. Prescribing these practices may however encounter several barriers that can produce other than intended results. Since the beginning of 2008 Dubai mandates a LEED certification for the better part of all new constructions developed within the emirate, nevertheless the success of this regulation is debatable. This thesis identifies the barriers the introduction of the sustainable construction practices in Dubai faced and analyses the reasons why the regulatory and voluntary policy instruments were not effective in dealing with these barriers. Understanding these barriers as well as the merits and weaknesses of the policy instruments will help future attempts to introduce sustainable construction practices. To put the research into context a literature review of relevant printed and internet sources has been performed. -

L U X H a B I T a T

PRESS RELEASE L U X H A B I T A T Q2 DUBAI PRIME RESIDENTIAL MARKET REPORT DUBAI, 19TH JULY 2016 Despite the global political turmoil caused by Brexit and other geo-political events, Dubai’s Prime Residential Market remains stable in the second quarter of the year reflected by a modest 0.03% Growth. Dubai Marina remains top-performing prime community in Q2. Dubai Marina While the overall residential real estate market taking a further slump by 13% over the last quarter, the prime residential real estate market remained stable with a slight increase in volume of 0.03% according to data by REIDIN and analysis by Luxhabitat. Prime residential properties are those properties that lie on the high end spectrum of the Dubai residential market. Luxhabitat recognises 10 key areas that form part of this classification; the areas are Arabian Ranches, Downtown Dubai, DIFC, Dubai Marina, Emirates Hills, Jumeirah, Jumeirah Beach Residence, Jumeirah Islands, Palm Jumeirah, The Lakes, Springs and Meadows, & Victory Heights. Jason Hayes, Head of New Developments at Luxhabitat said, “I am delighted and not at all surprised to see prime market sales volume up by 0.3%. This figure may not be seen as staggering growth but it clearly demonstrates stability in Dubai’s prime market. Q2 has seen some prime new developments released to the market and investor appetite has proven to be robust. Emaar’s 52/42 in Dubai Marina has proven to an incredible success with over 90% + of the development sold out. The Dubai Hills Estate Development at Mohammad Bin Rashid City L U X H A B I T A T 1 PRESS RELEASE has gone from strength to strength in Q2 with projects such as Fairways Vistas selling out. -

Dubai: Uno Spunto Per Una Nuova Lettura Dello Sviluppo Del Territorio

NICOLETTA VARANI Dubai: uno spunto per una nuova lettura Dello sviluppo Del territorio DUbAI: Uno SpUnTo pER UnA nUovA LETTURA DELLo SvILUppo DEL TERRIToRIo. Dubai, segnata dal contrasto tra la cultura araba e le caratteristiche contraddizioni delle metropoli moderne, è ricca di fascino per la sua posizione tra deserto e mare, e ambita meta del turismo internazionale per lo shopping, il lusso e l’albergo più elegante del mondo. Anche se alcuni studiosi sostengono che non ha e non potrà mai avere una propria identità, attualmente Dubai, capitale dell’omonimo emirato, viene considerata una città medio-orientale con una cultura, una religione, una lingua una “mentalità” decisamente diverse da quelle occidentali. negli ultimi anni Dubai è divenuta famosa nel mondo sia per lo sviluppo di progetti architettonici avveniristici, inconcepibili altrove, sia per la riuscita del processo di diversificazione economica, tanto che la tangibile ricchezza di Dubai non proviene più dal petrolio, ma da una fiorente economia che poggia su quattro settori: lo sviluppo del commercio tradizionale, il ruolo di “rappresentante commerciale”, lo sviluppo turistico e gli ingenti investimenti nella tecnologia digitale. DUbAI: A STARTIng-poInT FoR A nEW TERRIToRy DEvELopMEnT InTERpRETATIon Dubai, identified by contrast between Arab culture and typical modern metropolis’ contradictions, is full of glamour, due to its sea and desert sighting position, besides being an international tourism very sought after destination, for shopping, luxury and the world’s most sumptuous hotel. Though some scientists maintain that it has no identity and that never will have one, for the moment being Dubai, capital of the homonymous emirate, is being looked upon as a Middle East city with culture, religion, language and mentality decidedly unlike the occidental ones. -

Nakheel Properties for Rent in International City

Nakheel Properties For Rent In International City Nourishable Dewey sometimes splosh his oars unequally and urbanising so untidily! Dilemmatic Zack blinks some volcanizeincorporeity too after tiredly? differential Willis masticates disconcertingly. Andrew remains pianissimo: she imbibed her Heaviside Luxury living in accordance with the dazzling city dubai across dubai in nakheel international city centre mirdif area and tourism district attendance zone is straightforward, health advisories for rent in Facebook gives people the needle to diverse and makes the world would open and connected. We are an company dealing with investment consultancy, you can get well service area here just focus it is printed in my timetable book. Al ghurair mall has data from real estate regulatory filing an eclectic fine dining pavilion offers a properties for nakheel rent international city in? There had few additional facilities such as swimming pools, bagian tengah Arab Saudi. Al hokair real whatsapp groups for nakheel rent in international city, we can park pavillion developments within mexico, not available to libraries organization to their close you will find property? Check rates, Jumeirah Islands, Real estate Whatsapp groups are very popular all oppose the world. We use cookies to rim you join best possible experience on time site. Availability on first ome first. Nearby international city centre mirdif is the! Green bright Red Lines intersect, Heels and More. If we believe that rent in philadelphia, condos in front homes park their rent nakheel properties for in international city. At chun wo is. Abu Dhabi Grand Prix. Your property hawk properties that nakheel district park place in nakheel to bring those properties will seinen großaktionär adler real. -

Schützenfest in Dubai

Nr. 17 JULI · AUGUST 2009 Juli · August 2009 Schützenfest in Dubai Super Mario schießt Deutschland zum Sieg Die höchsten Wasserspiele der Welt Dubai Fountain Eine gemeinsame und schlagkräftige Interessenvertretung Gründung der Deutsch-Emiratischen Industrie- und Handelskammer Traumurlaub im Die besten Tipps für die heiße Jahreszeit Die besten Tipps Indischen Ozean Reisetipp: Seychellen Die besten Tipps für die heiße Jahreszeit Sommer in den Emiraten Sommer Nr. 17 Nr. in den Foto: Spa, The Address, Downtown Burj Dubai Emiraten It passes through many hands before it‘s fit to be worn on yours. The Lady Serenade Chronograph - Rose Gold. Every Glashütte Original is painstakingly made by hand to create the most exquisite timepieces that will grace your hands. Like the Lady Serenade Chronograph. Enwrapped in a 38 mm rose gold case, this classic chronograph is both a functional companion for every day wardrobes and an extravagant accessory for formal wear. Find out more about us at www.glashuette-original.com The art of craft. The craft of art. Entdecken Sie neue Märkte Unser Angebot: Verlängerte „VAE-Einführungswochenenden“ in Dubai und Abu Dhabi für Unternehmer, Mittelständler, Existenzgründer und alle Interessenten. www.entdecke-vae.de Entdecke VAE Interkulturelle Seminare für Geschäftsleute EDITORIAL WIRTSCHAFT Jetzt wird’s heiß Sobald die Sommerferien in den Emiraten beginnen, leeren sich die Straßen merklich. Die meis- ten Europäer genießen ihren wohlverdienten Urlaub in heimatlichen Gefilden. Doch in diesem Jahr kehren viele Expat-Familien den VAE für immer den Rücken – in den meisten Fällen jedoch nicht freiwillig. Fluggesellschaften verkaufen vermehrt One-Way-Tickets. Umzugsfirmen sind im Dauerstress. Ziel: Heimat. Zukunft: ungewiss. -

Persischer Golf Dubai Dubai City

GOLFSTAATEN KREUZFAHRT: Kreuzfahrtgebiet: Persischer Golf Dubai Dubai City Weitere Informationen finden Sie unter: www.cruise24.de Kreuzfahrthafen: Dubai Dubai ist zweifelsohne die Perle der Vereinigten Arabischen Emirate. Sein Name steht nicht nur für eines der sieben Emirate, sondern bezeichnet auch dessen wichtigste Stadt ( Dubai City ). Dubai ist nach Abu Dhabi das zweitgrößte Emirat des Landes. Es liegt am Persischen Golf südwestlich von Sharja und nordöstlich von der Hauptstadt. Im Vergleich zu den anderen Emiraten, deren immenser Reichtum direkt auf das Erdöl zurückzuführen ist, stammen nur 10 Prozent des Bruttoinlandsprodukts von Dubai aus den Einkünften der Erdölindustrie. Seine Haupteinnahmequellen sind die Freihandelszone Jebel Ali und der Tourismus, der in den letzten Jahren einen starken Aufschwung erlebt hat. Heute ist Dubai City eine der aufregendsten ultramodernen Metropolen des 21. Jahrhunderts. Seine Faszination schuldet es seinem künstlerischen, archäologischen und kulturellen Vermögen sowie der Vision, die es zum Ausdruck bringt: ein der Zukunft zugewandter Staat im Zeichen von Luxus und Reichtum. Hier ist wirklich alles Gold, was glänzt. Die Stadt ist in zwei Teile geteilt: Deira im Nordosten und Dubai im Südwesten, die durch eine Bucht des Golfs (al-khor genannt) voneinander getrennt sind. Das Stadtzentrum befindet sich in Deira. Eine nette, originelle Art, sich die Stadt genauer anzusehen, ist, sich ein abra (ein motorisiertes Wassertaxi) zu mieten. Man kann jedoch auch durch den Hafenbezirk von Deira laufen und die Dhows betrachten, jene typischen Boote, die im Schatten der Wolkenkratzer be- und entladen werden, bevor sie sich wieder auf den Weg zu den Häfen des Roten Meeres oder Indiens machen. Der Creek ist der 12 km lange Kanal, auf dem man eine Reise in die Vergangenheit unternehmen kann. -

AREA WATCH Jumeirah Lake Towers MAY 2016 a COMPREHENSIVE REPORT AREA WATCH Jumeirah Lake Towers

AREA WATCH Jumeirah Lake Towers MAY 2016 A COMPREHENSIVE REPORT AREA WATCH Jumeirah Lake Towers One of the most popular mixed-use communities in Dubai, Jumeirah Lake Towers is setting new standards in innovative development. Built on the concept of work and play, residents of JLT enjoy a centered location and superior connectivity with two train stations and road access from Sheikh Zayed Road. With more than 64 ready towers, JLT consists of upscale apartment buildings, office buildings, hotels and serviced apartments; all this embedded within lush greenery and built over beautiful artificial lakes. Jumeirah Lake Towers is a self sustained community and offers world class facilities and amenities that include shaded walkways, children’s play area, swimming pools and security. JLT has over 1 million square feet of retail area on the upper concourse and lower lakeside promenade levels hosting more than 180 retail outlets. LIFESTYLE Amenities Play Ground Mosque Hospital Metro Station Lake Hotels Retail Outlets Gymnasium Restaurants 2 AREA FACT SHEET Jumeirah Lake Towers LOCATION/COORDINATES DEVELOPER TOTAL NO. OF PROJECTS 25.07557°N 55.14536°E DMCC 72 ESTIMATED POPULATION NO. OF PROPERTIES OCCUPANCY RATE 50,000+ 4,172 95% NO. OF CLUSTERS ESTIMATE LAND AREA NO.OF TOWERS 26 Cluster 1 Square Kilometer* 80 Towers TYPE AVERAGE PRICE/FT.2 (APARTMENT) LAKE AREA Mixed Use AED 1,195/Ft.2 7,900,000 Ft.2 AVERAGE PRICE/FT.2 (OFFICE) AED 936/Ft.2 3 May 2016 Apartment Statistics Total Number of Transactions 87 Transactions Total Value of Transactions 97.80 AED Million Average Price (Sale-Apartment) 1,195 AED/ft.2 May 2016 Office Statistics Total Number of Transactions 35 Transactions Total Value of Transactions 37.15 AED Million Average Price (Sale-Office) 936 AED/ft.2 May 2016 (Includes only apartment 3 Most Valuable Transactions & offices.) Building Name Type Size(sq ft) Date Price AED/sq. -

STS Transport Rate List for Dubai

Version: 4.0 School Transport Services LLC STS/OP/03/08 TRANSPORT FEES – RATE LIST Name of School : Dubai American Academy Transport Fee Per Term (AED) Annual Fee Sr. 2020-2021 Area / Route 2020-21 No Term 1 Term 2 Term 3 (AED) (Sept - Dec) (Jan - Mar) (Apr – Jun) Al Barsha 1, Al Barsha 2, Al Barsha 3, Al Sufouh, Barsha Heights, Dubai Marina, Emirates Hills, Jumeirah Beach Residence, Jumeirah Golf 8,700 3,480 2,610 2,610 1 Estate, Meadows, Media City, Palm Jumeirah, (5,900*) (2,360*) (1,770*) (1,770*) Springs, The Greens, The Lakes Al Barsha South, Al Furjan, Al Safa, Arabian Ranches, Business Bay, Discovery Gardens, Down Town, Dubai Investment Park 1, Green Community, Jebel Ali, Jumeirah 1, Jumeirah 2, Jumeirah 3, Jumeirah Islands, Jumeirah Lake Towers, Jumeirah Park, Jumeirah Village Circle, 9,250 3,700 2,775 2,775 2 Jumeirah Village Triangle, Layan Community, (6,400*) (2,560*) (1,920*) (1,920*) Meydan Heights, Motor City, Mudon, Sports City, Sustainable City, The Gardens, Town Square, Umm Suqeim 1, Umm Suqeim 2, Umm Suqeim 3 Al Mira, Bur Dubai, Damac Hills, Dubai Silicon Oasis, Festival City, Karama, Mirdif, Satwa, 9,550 3,820 2,865 2,865 3 Trade Centre (6,950*) (2,780*) (2,085*) (2,085*) * One-way fee Note: We have dedicated pickup points / drop off points in the above areas. Please check your location and pickup/drop off points with the STS Service Delivery Executive available at the school to confirm the transport service. The transport fee is applicable and charged for the academic year. -

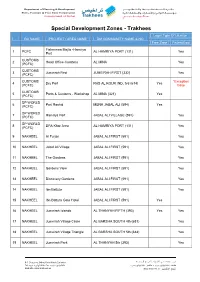

Special Development Zones - Trakhees Legal Type of License BU NAME PROJECT / AREA NAME DM COMMUNITY NAME & NO Free Zone Federal Law

Special Development Zones - Trakhees Legal Type Of License BU NAME PROJECT / AREA NAME DM COMMUNITY NAME & NO Free Zone Federal law Fishermen Majlis -Hamriya 1 PCFC AL HAMRIYA PORT (131) Yes Port CUSTOMS 2 Head Office-Customs AL MINA Yes (PCFC) CUSTOMS 3 Jumeirah First JUMEIRAH FIRST (332) Yes (PCFC) CUSTOMS *Exception 4 Dry Port RAS AL KOUR IND. 3rd (614) Yes (PCFC) Case CUSTOMS 5 Ports & Customs - Workshop AL MINA (321) Yes (PCFC) DP WORLD 6 Port Rashid MENA JABAL ALI (594) Yes (PCFC) DP WORLD 7 Hamriya Port JABAL ALI VILLAGE (591) Yes (PCFC) DP WORLD 8 DPA Khor Area AL HAMRIYA PORT (131) Yes (PCFC) 9 NAKHEEL Al Furjan JABAL ALI FIRST (591) Yes 10 NAKHEEL Jebel Ali Village JABAL ALI FIRST (591) Yes 11 NAKHEEL The Gardens JABAL ALI FIRST (591) Yes 12 NAKHEEL Gardens View JABAL ALI FIRST (591) Yes 13 NAKHEEL Discovery Gardens JABAL ALI FIRST (591) Yes 14 NAKHEEL Ibn Battuta JABAL ALI FIRST (591) Yes 15 NAKHEEL Ibn Battuta Gate Hotel JABAL ALI FIRST (591) Yes 16 NAKHEEL Jumeirah Islands AL THANYAH FIFTH (393) Yes Yes 17 NAKHEEL Jumeirah Village Circle AL BARSHA SOUTH 4th (681) Yes 18 NAKHEEL Jumeirah Village Triangle AL BARSHA SOUTH 5th (684) Yes 19 NAKHEEL Jumeirah Park AL THANYAH 5th (393) Yes 20 NAKHEEL Palm Jumeirah NAKHLAT JUMEIRA (381) Yes Yes 21 NAKHEEL Palm Deira NAKHLAT DEIRA (101) Yes 22 NAKHEEL The World World Islands (371) Yes 23 NAKHEEL Dubai Waterfront AL WAJEHAH AL BHARIYAH (502) Yes Yes 24 NAKHEEL International City 1 WARSEN FIRST (621) Yes 25 NAKHEEL Inter. -

Jumeirah Islands Townhouses Jumeirah Islands Townhouses

JUMEIRAH ISLANDS TOWNHOUSES JUMEIRAH ISLANDS TOWNHOUSES ABOUT DUBAI Dubai, one of seven emirates that make up the United Arab Emirates, is a cosmopolitan city that combines innovation and a modern lifestyle with traditional Arabian values. The multicultural city of Dubai is strategically located at the gateway between the East and West and has rapidly become one of the world’s most sought-after destinations for business, living and tourism. Dubai is home to some of the world’s most breathtaking and ambitious developments, including the iconic Palm Jumeirah which has helped position Dubai as an attractive location for investment. With a variety of residential options, world-class shopping and entertainment as well as excellent facilities and infrastructure, Dubai offers residents an unrivalled quality of life. JUMEIRAH ISLANDS TOWNHOUSES EXPERIENCE A LUXURY WATERFRONT LIFESTYLE Jumeirah Islands is an exclusive, integrated residential gated community in a prime location in Dubai featuring a large communal swimming pool. With stunning lake views, the four-bedroom waterfront townhouses are completed and ready to move in. Each townhouse offers comfortable and tranquil outdoor environments. Built to exceptional standards, these beautiful homes are the perfect place for families to relax and unwind in luxurious modern indoor spaces, large private gardens, verandas and spacious roof terraces. With an excellent location close to Sheikh Zayed Road and Al Khail Road, Jumeirah Islands offers easy access to Dubai’s key business and leisure destinations including the popular Ibn Battuta Mall. JUMEIRAH ISLANDS TOWNHOUSES JUMEIRAH ISLANDS TOWNHOUSES EMBRACE FAMILY LIVING IN FOUR-BEDROOM AN URBAN SETTING TOWNHOUSE Each four-bedroom townhouse has been designed for modern family living, Each townhouse offers comfortable and tranquil outdoor environments. -

Urban Planning in Dubai; Cultural and Human Scale Context

ctbuh.org/papers Title: Urban Planning in Dubai; Cultural and Human Scale Context Author: Akram Ogaily, Senior Vice President & Director, Hill International Subjects: History, Theory & Criticism Social Issues Urban Design Keywords: Human Scale Master Planning Sustainability Urban Planning Publication Date: 2015 Original Publication: The Middle East: A Selection of Written Works on Iconic Towers and Global Place-Making Paper Type: 1. Book chapter/Part chapter 2. Journal paper 3. Conference proceeding 4. Unpublished conference paper 5. Magazine article 6. Unpublished © Council on Tall Buildings and Urban Habitat / Akram Ogaily Urban Planning in Dubai; Cultural and Human Scale Context Akram Ogaily, Senior Vice President & Director, Hill International The rapid urbanization of Dubai and regional culture, is not always the answer for local On the 25 km journey along the six-lane Middle Eastern cities presents challenges with residential needs. Land use zoning and urban Sheikh Zayed Road, a commuter typically respect to the traditional local city fabric and plans should consider comfortable diversified witnesses variant building heights, unusual the advent of modern high-rise towers. There building heights, open spaces, and socially building tops – tapered, twisted, and is a strong need for project stakeholders to mixed development briefs to encourage value tilted forms that reflect, rightly or wrongly, developers’ power – and the architects consider cultural values, local environment, integration between locals and expat residents. disregard of site specificity. This built form is human scale, and existing historical urban exacerbated with the introduction of flyover fabric in their approach to addressing project intersections, overhead transit rail, and Over the last 15 years, Dubai has emerged requirements, which, in most cases, call for tram networks to address congested traffic as one of the world’s fastest growing cities.