Project Food Information Memorandum

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

1.Notice Inviting Tender (Nit)– E-Tender Tender No

Tender No.: INDIAN OIL CORPORATION LIMITED (Haldia Refinery) Page RHM19R2029 Procurement of Hand Tools / Cutting tools 1 of 2 1.NOTICE INVITING TENDER (NIT)– E-TENDER TENDER NO. :RHM19R2029 Indian Oil Corporation Limited, a Company incorporated in India and having its registered office at G- 9, Ali Yavar Jung Marg, “Western Express Highway”, Bandra (East), Mumbai-400 051 invites E- tender under TWO BID (PART-I: Techno-Commercial Bid and PART-II: Price Bid) from bonafide experienced Bidder of sound financial standing and reputation for the job(s) defined in this tender covering following items. The details of the tender are given below: Material Description Supply of Hand Tools/CUTTING TOOLS Quantity As per BOQ/Enquiry Cum Offer document Type of Tender National Open E-Tender EMD Amount ₹ 15,800/- (INR) (in INR) EMD exempted categories: Micro & Small Enterprises (MSE) as mentioned in “TENDER CONDITIONS FOR BENEFITS/PREFERENCE FOR MICRO & SMALL ENTERPRISES (MSEs)”, Startup recognized by DIPP, Central/State PSUs & Govt. Organizations and JVs of IOCL. Please refer “General Instruction to Bidders” for information on EMD submission. TENDER DOWNLOAD/ Please refer “Critical Dates table” in Tender Details at e-tender SALE PERIOD Portal BID SUBMISSION PERIOD Please refer “Critical Dates table” in Tender Details at e-tender Portal CLARIFICATION PERIOD 06.08.2019 5 PM IST to 09.08.2019 3 PM IST **Queries for clarification to be sent over email during the “Clarification Period”. Though IOCL may respond to clarifications sought after “Clarification Period”, IOCL will not be under obligation to extend the bid submission date or to respond to clarifications sought by the buyers after the scheduled “Clarification Period”. -

HALDIA REFINERY (A Govt

INDIAN OIL CORPORATION LIMITED (Refineries Division) HALDIA REFINERY (A Govt. of India Undertaking) Advertisement No. : APP-RECTT/01/2016 Notification for engagement of Apprentices Indian Oil Corporation Limited, the largest commercial undertaking in India and a Fortune “Global 500” Company, as a measure of Skill Building Initiative for the Nation, proposes to engage Apprentices at its Haldia Refinery ,West Bengal. Applications are invited from candidates meeting the following qualification and other parameters for engagement as Apprentices under Apprentices Act,1961/1973 (as amended from time to time) in the Trade/Discipline mentioned below: Educational Qualification, Provisional Number of seats in Apprentice category including likely reservation shall be as follows. The consolidated stipend payable shall be as mentioned below or as revised (under the Act )from time to time (whichever is higher). Reservation will be applicable as per the prescribed percentage for recruitment applicable to the state of West Bengal. S.No Trade/Discipline Qualification Period of Total UR SC ST OBC(NCL) Apprenticeship Nos. (months) 1 Trade 3 yrs. Full time 36 10 5 2 1 2 Apprentice(Boiler) B.Sc.(Phy,Maths,Chem,/Ind Discipline-Mechanical Chem) 2 Trade Matric with 2 year 12 5 3 1 0 1 Apprentice(Fitter) ITI(Fitter) course Discipline-Mechanical 3 Trade 3 yrs. Full time 18 Apprentice/Attendant B.Sc.(Phy,Maths,Chem,/Ind Operator(Chemical Chem) Plant) 39 20 9 1 9 Discipline-Chemical 4 Technician Apprentice 3 yrs. Full time Diploma in 12 Discipline-Chemical Chemical Engg./Refinery & petrochemicals Engg. 5 Technician Apprentice 3 yrs. Full time Diploma in 12 12 6 3 1 2 Discipline-Mechanical Mechanical Engg. -

Multi- Hazard District Disaster Management Plan

DISTRICT DISASTER MANAGEMENT PLAN 2019-20 DISTRICT DISASTER MANAGEMENT SECTION PURBA MEDINIPUR 1 Government of West Bengal Shri Partha Ghosh(WBCS Exe.) Office of the District Magistrate & Collector District Magistrate & Collector Tamralipta,Purba Medinipur,Pin-721236 Tamralipta,Purba Medinipur,Pin-721236 Ph. No.-03228-263329, Fax No.:– 03228–263728 Ph. No.-03228-263098, Fax No.:– 03228–263500 Email address: [email protected] Email address: [email protected] Foreword Purba Medinipur district is situated in the southern part of the state of West Bengal.Total geographical area covered by the district is 4713 sq Km.This district extended from 22031‘ North to 21038‘ North latitude and from 88012‘ East to 87027‘ East longitudes. This District has a Multi-Hazard geographical phenomenon having a large area falls under Bay of Bengal Coastal Zone. Digha,Mandarmoni,Shankarpur and Tajpur are the important tourist spots where a huge numbers of tourists come regularly.To ensure the safety and security of tourist involving all stakeholders is also a challenge of our District. The arrangement of Nulias for 24x7 have been made for safety of tourist.200 Disaster Management volunteers have been trained under ―Aapda Mitra Scheme‖ for eleven(11) Blocks,43 nos Multi-Purpose Cyclone Shelters(PMNRF-15,NCRMP-28) have also been constructed to provide shelter for people and cattle during any emergency need. Basic training for selected volunteers(@10 for each Block and @5 for Each GP) have also been started for strengthening the Disaster Management group at each level.A group of 20 nos of Disaster Management volunteers in our district have also been provided modern divers training at Kalyani. -

Appellate Jurisdiction

Appellate Jurisdiction Daily Supplementary List Of Cases For Hearing On Monday, 26th of July, 2021 CONTENT SL COURT PAGE BENCHES TIME NO. ROOM NO. NO. HON'BLE JUSTICE RAJESH BINDAL , CHIEF 1 On 26-07-2021 1 JUSTICE (ACTING) 1 DB-I At 11:00 AM HON'BLE JUSTICE RAJARSHI BHARADWAJ HON'BLE JUSTICE I. P. MUKERJI 3 On 26-07-2021 2 4 HON'BLE JUSTICE ANIRUDDHA ROY DB - II At 11:00 AM HON'BLE JUSTICE HARISH TANDON 28 On 26-07-2021 3 7 HON'BLE JUSTICE BIBEK CHAUDHURI DB-III At 11:00 AM HON'BLE JUSTICE SOUMEN SEN 16 On 26-07-2021 4 55 HON'BLE JUSTICE HIRANMAY BHATTACHARYYA DB - V At 11:00 AM HON'BLE JUSTICE SUBRATA TALUKDAR 11 On 26-07-2021 5 62 HON'BLE JUSTICE JAY SENGUPTA DB-VI At 11:00 AM HON'BLE JUSTICE TAPABRATA CHAKRABORTY 30 On 26-07-2021 6 71 HON'BLE JUSTICE SUBHASIS DASGUPTA DB-VII At 11:00 AM HON'BLE JUSTICE ARINDAM SINHA 4 On 26-07-2021 7 77 HON'BLE JUSTICE SAUGATA BHATTACHARYYA DB - VIII At 11:00 AM HON'BLE JUSTICE ARIJIT BANERJEE 32 On 26-07-2021 8 89 HON'BLE JUSTICE SUVRA GHOSH DB - IX At 11:00 AM 8 On 26-07-2021 9 HON'BLE JUSTICE DEBANGSU BASAK 119 SB II At 11:00 AM 42 On 26-07-2021 10 HON'BLE JUSTICE SHIVAKANT PRASAD 150 SB - III At 11:00 AM 13 On 26-07-2021 11 HON'BLE JUSTICE RAJASEKHAR MANTHA 154 SB - IV At 11:00 AM HON'BLE JUSTICE SABYASACHI 7 On 26-07-2021 12 188 BHATTACHARYYA SB - V At 11:00 AM 26 On 26-07-2021 13 HON'BLE JUSTICE SHEKHAR B. -

Name of the Hazardous Waste Reprocessing Units in West Bengal Registered by West Bengal Pollution Control Board (WBPCB)

Name of the Hazardous Waste reprocessing units in West Bengal registered by West Bengal Pollution Control Board (WBPCB) Sl. Name & Address of the Nature of hazardous waste Registration No. Unit to be recycled valid upto 1 Abdul Salam & Co., Lead acid battery plates/ scrap Valid as per the Dharala, Panagarh, Budbud, - 1200 MTA terms & Dist-Burdwan, Pin-713 148 conditions specified in the regn. certificate 2 Adarsh Galai Udyog Lead Acid Batterry Plates / Valid as per the Dag No. 1250, Khatian No. Lead Scrap - 1380 MTA terms & 1819, 1862, Dhulagori conditions Industrial Park, Howrah. specified in the regn. certificate 3 Aleadco Batteries, Lead Acid Battery Plates and Valid as per the 49/2, T.N. Mukherjee Road, Lead Scrap - 150 MTA terms & Raghunathpur, Dist.- conditions Hooghly specified in the regn. certificate 4 Ambica Dhatu Pvt. Ltd., Zinc Dross - 1650 MTA 18.08.2010 to N.H.-VI, Jalan Industrial 17.08.2015 Complex, Vill. Biprannapara, Dist. Howrah- 711 411. 5 Ambica Dhatu Pvt. Ltd., Zinc ash & residue/zinc 18.08.2010 to N.H.-VI, Jalan Industrial dross/hot dip galvaniser slab 17.08.2015 Complex, Vill. & bottom dross/zinc Biprannapara, Dist. Howrah- ash/skimming : 4500 MTA 711 411. 6 Ambica Chemical & Zinc Ash/Skimming - 1600 Industrial Corporation, MTA, Zinc Dross/Zinc Scrap Valid as per the 68, Debendra Chandra Dey - 400 MTA terms & Road, P.O. & P.S.- Tangra, conditions Kolkata - 15 specified in the regn. certificate 7 Amit Metal Works, Mouza- Lead acid battery plates/lead Valid as per the Jala Dhulagori, J.L. no. 2, scraps/lead ash/lead dross : terms & Sl. -

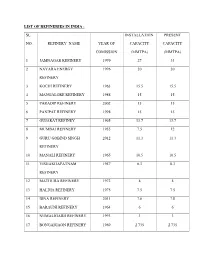

List of Refineries in India

LIST OF REFINERIES IN INDIA : SL INSTALLATION PRESENT NO. REFINERY NAME YEAR OF CAPACITY CAPACITY COMISSION (MMTPA) (MMTPA) 1 JAMNAGAR REFINERY 1999 27 33 2 NAYARA ENERGY 1996 20 20 REFINERY 3 KOCHI REFINERY 1963 15.5 15.5 4 MANGALORE REFINERY 1988 15 15 5 PARADIP REFINERY 2002 15 15 6 PANIPAT REFINERY 1998 15 15 7 GUJARAT REFINEY 1965 13.7 13.7 8 MUMBAI REFINERY 1955 7.5 12 9 GURU GOBIND SINGH 2012 11.3 11.3 REFINERY 10 MANALI REFINERY 1965 10.5 10.5 11 VISHAKHAPATNAM 1957 8.3 8.3 REFINERY 12 MATHURA REFINERY 1972 8 8 13 HALDIA REFINERY 1975 7.5 7.5 14 BINA REFINERY 2011 7.8 7.8 15 BARAUNI REFINERY 1964 6 6 16 NUMALIGARH REFINERY 1993 3 3 17 BONGAIGAON REFINERY 1969 2.735 2.735 18 GUWAHATI REFINERY 1962 1 1 19 NAGAPATTNAM 1993 0.5 1 REFINERY 20 DIGBOI REFINERY 1901 0.65 0.65 21 TATIPAKA REFINERY 2001 0.07 0.07 22 BARMER REFINERY 2013 9 9 Jamnagar Refinery: Jamnagar refinery is a private sector crude oil refinery owned by reliance. The refinery was commissioned in 14 July 1999 with an installed capacity of 27MMTPA. The present capacity of this refinery is 33MMTPA.It is currently the largest refinery in the world. Oil Field of Assam:- In Assam up to the cost of Myanmar, the presence of oil is very common .In the air 1825 itself seepage of oil was discovered in makum .In the year 1867 under the guidance of sir Madly Colt ,the first oil well was dug at makum .But after a very short production, it was abandoned as it was not economically viable. -

Indian Oil Corporation Limited (Refinery Division) P.O.: Haldia Oil Refinery, Dist

IndianOil INDIAN OIL CORPORATION LIMITED (REFINERY DIVISION) P.O.: HALDIA OIL REFINERY, DIST. : PURBA MEDINIPUR, PIN - 721 606 NOTICE INVITING TENDER NIT NO : IS/PR/631 Indian oil Corporation Limited, Haldia Refinery, invites sealed tenders (Petty Job; Estimated Amount Less than Rs.02.50 Lac) in prescribed tender form under Two Bid System from bonafide, experienced contractors with sound technical and financial capabilities and reputation, fulfilling the qualifying requirements stated hereunder :- TENDER NO. ISPR631 NAME OF WORK Supply of 1000 nos. printed Mouse Pad. COST OF TENDER DOCUMENT : NIL EARNEST MONEY DEPOSIT NIL PERIOD OF SALE OF TENDERS : 10.04.2019 TO 28.04.2019 DURING 10.00AM TO 3:00PM (EXCLUDING SUNDAY & HOLIDAY). DATE & TIME OF RECEIPT / : 29.04.2019 @ 3:00 PM OPENING OF TENDER DOCUMENT CONTACT PERSON Shri. Sanjib Hansda / Shri. Supriyo Dutta PHONE, FAX, MAIL ADDRESS Phone : 03224 - 223413 / 223409 E-mail : [email protected] E-mail : duttasupriyo@IndianOiLin TENDER TO BE SUBMITTED TO : Chief Manager (IS), IS Department Indian Oil Corporation Ltd., Haldia Refinery, P.O. Haldia Oil Refinery, Dist. Purba Medinipur West Bengal , PIN - 721 606. Special condition for the bidders :- a) Vendor to produce a sample mouse pad of desired quality and content printed on it as per attached specimen for taking EIC's consent before bulk production. b) Tender Papers shall be collected from IS Department. Haldia Refinery or can be downloaded from CPP site. (https://eprocure.gov.in/epublish/app) Mere issue of Bid Document does not entitle a bidder to pre-qualify without furnishing requisite documentary evidence in support of pre-qualification. -

Annexure I Sampling and Analysis Charges of the Wbpcb Laboratories

Annexure I Annual Report 2006-2007 145 ANNEXURE I SAMPLING AND ANALYSIS CHARGES OF THE WBPCB LABORATORIES ITEM Charge Sampling Charge (including personnel and cost of hired car) Rs. 500 Cost of determination of five basic parameters Rs. 400 (pH, TSS, COD, BOD and O&G) Rate for routine industrial waste-water monitoring Rs. 900 Rate for additional parameters for industrial waste-water monitoring As prescribed below Processing charge for samples deposited for analysis by outside agencies. Rs. 100 CHARGE FOR ANALYSIS pH Rs.50 Temperature Rs.20 Conductivity Rs.50 DO Rs.50 BOD Rs.250 Oil & Grease Rs.200 Nitrate-Nitrogen Rs.100 Nitrite Nitrogen Rs.100 Anionic detergent Rs.150 Fecal Coliform (Fermentation Tube method) Rs.200 Total Coliform (Fermentation Tube method) Rs.200 Turbidity Rs.50 Phenolphthalein Alkalinity Rs.100 Total Alkalinity Rs.100 Chloride Rs.100 Free Chlorine Rs.100 COD Rs.200 Total Kjeldal Nitrogen Rs.300 Ammoniacal Nitrogen Rs.300 Hardness as CaCO3 Rs.100 Calcium as CaCO3 Rs.100 Sulphate Rs.100 Sulphide Rs.100 Sodium Rs.200 Total Dissolved Solid Rs.200 146 SAMPLING AND ANALYSIS CHARGES Annexure I ITEM Charge Total Fixed Solids Rs.200 Total Suspended Solids Rs.200 Phosphate Rs.100 Boron Rs.150 Magnesium Rs.150 Potassium Rs.150 Fluoride Rs.150 Field Observation (Physical observation only) Rs.200 Biomonitoring Rs.400 Arsenic Rs.200 Cadmium Rs.150 Copper Rs.150 Lead Rs.150 Total Chromium Rs.150 Nickel Rs.150 Zinc Rs.150 Mercury Rs.200 Iron (Total) Rs.150 Any other metal involving AAS Rs.150 Hexavalent Chromium Rs.100 Phenol Rs.300 -

Download Move Magzter App from Android & Apple Store

INTERVIEW INDIA'S LOGISTICS COSTS DEDICATED FREIGHT LOGISTICS Raj Chopra Container Logistics Cost: CORRIDORS Data You Can Director, Freya Shipping Myth VS Facts Bringing the Modal Shift Bank On! south asia’s premier mariti me business magazine R100 APRIL 2020 WWW.MARITIMEGATEWAY.COM RNI NO: TELENG/2009/30633 POSTAL REGISTRATION NO: HD/1137/2019-2021 DATE OF PUBLICATION: 25/03/2020 DATE OF POSTING: 28/03/2020 IMO 2020 AND THE COVID-19 CURSE MARITIME TRADE QUARANTINED China is gradually recovering from the pandemic which is spreading to other parts of the globe bringing them under quarantine, once again highlighting the vulnerability of the global supply chain APRIL 2020 | MARITIME GATEWAY 3 FROM THE EDITOR PANDEMIC TEACHES RESILIENCE hile the actual impact of COVID-19 digital technology to organize and collaborate to the global economy is still with suppliers, thereby ensuring supplies reach Wunknown, but the very basic measure the people who needed the most. to prevent from getting bitten by the virus - In China’s major cities, home delivery of social distancing will surely give more pain to the Indian economy already reeling under items purchased online can be made within 20 slowdown. Prime Minister Narendra Modi minutes. This is largely down to the deployment appealed to citizens to stay at and work from of digital technology. Alibaba’s Cainiao network, home to curb the coronavirus outbreak. The for example, supports the supply chains of the People services sector, which accounts for about 55 per merchants it serves via an AI-enabled digital leveraged cent of India’s GDP is poised to be the worst hit. -

Haldia Refinery Ref. No. : HR/Medical/2018

Indian Oil Corporation Limited (A Govt. of India Undertaking) (Refineries Division) Haldia Refinery Ref. no. : HR/Medical/2018 Walk-in-interview for Contingent Duty Medical Officer (CDMO) & Specialists/ Paramedics at Haldia Refinery Hospital Indian Oil Corporation Limited, Haldia Refinery invites interested candidates for engagement as Contingent Duty Medical Officers (CDMO) and Psychiatrist, Pediatrician, Physiotherapist & Psychological Counselor at IOCL Haldia Refinery Hospital on contractual basis. (A) CDMO: Tenure of Engagement: Initially for 01 year which may be extended or reduced based on performance. Minimum Minimum Nos. to be Scope of work Consolidated Qualification/ Experience engaged monthly Med. emolument Registration MBBS Completed 6 days working in a week, duties Rs 70,000/- and internship and 03 would be in shifts of 48 hrs per week suitable registration schedule in the Refinery Hospital accommodation with Medical including Emergencies, First Aid will be provided Council of India Center, OHC, Immunization, OT etc. subject to availability. (B) Psychiatrist, Pediatrician, Physiotherapist & Psychological Counselor: Tenure of Engagement: Initially for a period of 1 year which may be extended or reduced based on visiting pattern of the patients. Specialization Qualification/ Med. Min. Nos. Scop Duty Hours Remuneration Registration Exp to be e of (Monthly) * enga work Rs. ged Psychiatrist MD (Psychiatry) 3 yrs 01 On 3 days/ week and 4 40,000/- Cont hours/ day ract Psychological Minimum graduate in 3 yrs 01 on 4 days/ week and 4 17,000/- Counselor any stream with Part hours/ day Diploma in Time Psychoanalysis/ Clinical basis psychology/ Medical counseling Pediatrician MD (Pediatrics) 2 yrs 01 3 days/ week and 4 40,000/- hours/ day Physiotherapist Bachelor in 2 yrs 01 6 days/ week and 4 25,000/- Physiotherapy hours/ day (8AM – 12 PM) Note: * Remuneration cost is inclusive of any transportation charges. -

Curriculum Vitae

Curriculum Vitae Dr. Chiranjib Bhattacharjee Dean, Faculty of Engineering & Technology (FET) & Former Registrar, JU Professor & Former Head Dept of Chemical Engineering Jadavpur University, Calcutta – 700 032, India. Phone: +91 98364 02118 (Mobile), +91 33 24572669 (Office) Email: [email protected], [email protected], [email protected] Personal Information: Date of Birth: September 30, 1966 Nationality: Indian Marital Status: Married Education: Secondary (1983) Passed 10-level examination of West Bengal Board of Secondary Education (W.B.B.S.E.) with first division and 77.8% marks. Higher Secondary (1985) Passed Higher Secondary Examination (10+2 level) of West Bengal Council for Higher Secondary Examination (W.B.C.H.S.E.) with first division and 77.2% mark. B.Ch.E. Hons.(1989) Chemical Engineering Department, Jadavpur University, Calcutta. Obtained first class honors with 81.4% marks. M.Tech. (1991) Chemical Engineering Department, Indian Institute of Technology (IIT), Kanpur. CPI: 9.33 out of 10 points. Ph.D. Engineering (1998) Chemical Engineering Department, Jadavpur University. Present Employment: Joined Jadavpur University in 24th June1991 as Lecturer Promoted to Reader in 2000 and Professor in 2005. Served as Head of the Department for two years (as per Jadavpur University rule) from July 2010 to July 2012. Professor & former Head, Department of Chemical Engineering, Jadavpur University, Kolkata - 700 032, INDIA. Presently Dean, Faculty of Engineering & Technology (FET), Jadavpur University. Also served as Registrar, Jadavpur University during March – November, 2018 along with Dean, FET Professional Affiliation: . Life Member of Indian Institute of Chemical Engineers (I.I.Ch.E.): LM-10551 . Life Member of Institution of Engineers (India): M130793-7 . -

HALDIA REFINERY Haldia,West Bengal

HALDIA REFINERY Haldia,West Bengal S. N Name Designation Contact details 01 Mr. E Panthya Chief Manager Lead Presenter [email protected] Mob: 9996140617 02 Ms. Lalitha Rani Assistant Manager Member [email protected] Mob: 9679833427 03 Mr. Amit Kalyan Chandra Assistant Manager Member [email protected] Mob: 9432946618 YEAR OF DIGITALISATION Accelerating Efficiency, Empowering Growth 1.Brief Introduction on company/unit YEAR OF DIGITALISATION Accelerating Efficiency, Empowering Growth HALDIA REFINERY OVERVIEW SN Attribute Remarks 1 Foundation Stone by Late Prof. Triguna Sen, Hon’ble Petroleum Minister on 6th Dec 1969. laid 2 Area 583 Acres 3 Commissioned in January 1975 4 Located at Haldia, Medinipur (E) District of West Bengal, 130 km from Kolkata. 5 Employees 1529 6 Crude capacity 8.0 MMTPA crude capacity (Capacity revamp for 8 MMTPA done in Jan’20) 7 Crude imported Saudi Arabia, Iran, Iraq, UAE, Nigeria, Angola, Malaysia, Kuwait, America and from Indigenous crudes YEAR OF DIGITALISATION Accelerating Efficiency, Empowering Growth HALDIA REFINERY OVERVIEW SN Attribute Remarks Arab mix, iran mix, basrah, Kuwait, das, mars, Ural, Maya, Girasol, Clov, Bonny Lt, 8 Crude Basket Labuan AkPO, Bonga, Kissanje, Miri, Agbami, Seria Lt, Murban-LS,WTI midland, Egina, Escravos, Mondo. 34 Nos (CDU1/2,VDU1/2,DCU,OHCU,FPU,RFFCU,DHDS, MHC, CGOT, HGU-1/2, No of process 9 CRU,KHDS, MSQ-ISOM,PRIME-G, LHFU, CIDWU,FEU,PDA,VBU, SRU2/3/4/5, SWSs, plants ARUs ETPs1/2 etc..) 4 STGs:48 MWh 4 Boilers : 525 TPH 10 CPP capacity 3 GTs:60 MWh 3 HRSGs : 360 TPH Total Power :108 MWh Total Steam : 885 TPH Total storage 198Nos 11 tanks Despatch PPL, Rail, Road, Coastal (Barge, tanker), Bitumen bulk loading and drum filling 12 facilities MS, HSD, Kero, ATF, MTO, JBO, Naphtha, Bitumen, Bitumen emulsion, 5 grades of 13 Products LOBS YEAR OF DIGITALISATION Accelerating Efficiency, Empowering Growth HALDIA REFINERY-Block Flow Diagram ->Stream sharing among the process plants for manufacturing final products like LPG, MS, HSD, Kero, ATF, Bitumen etc.