Starbucks Corporation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Executive Summary - November 2013

Executive Summary - November 2013 Project Café13 Europe – European Coffee Shop Market, November 2013© DISCLAIMER Copyright: Allegra Strategies Limited, November 2013 All rights reserved. No part of this publication may be reproduced or stored in a retrieval system, in any form or by any means, electrical, mechanical, photocopying or otherwise without the prior consent of the publishers. The views and forecasts presented in this report represent independent findings and conclusions drawn from a study of the European coffee shop market by Allegra Strategies. Main sources of information include published information, opinions and information shared by interviewees with Allegra Strategies during the period of study. This report has been produced under significant time constraints to ensure that the information contained is as up-to-date as possible. Great care has been taken to ensure that all information contained in this report is accurate, free from bias, and fully describes the latest developments in the European coffee shop market, as of October 2013. However, Allegra Strategies can accept no responsibility for any investment decision made on the basis of this information or for any omissions or inaccuracies that may be contained in this report. This report has been produced in good faith and independently of any operator or supplier to the industry. We trust that it will be of significant value to all readers. Allegra Strategies Limited Walkden House, 10 Melton Street, London, NW1 2EB Tel: +44(0)20 7691 8800 Fax: +44(0)20 7691 8810 Email: -

Chipotle Mexican Grill: Leavening Panera Bread's Sales? Downloaded from by IP Address 192.168.160.10 on 06/27/202

MORE INSIGHTS. MORE OFTEN. BETTER RETURNS. Richard Church [email protected] (203) 307-2581 Chipotle Mexican Grill: Leavening Panera Bread’s Sales? April 29th, 2016 DISCERN platform reveals: • Over 80% overlap between Chipotle and Panera in all regions within a 5-mile trade area • Other potential dining alternative beneficiaries from Chipotle challenges Chipotle Mexican Grill’s recent issues with food contamination and the resultant heavy losses of customers are widely known and do not appear to have ended judging by its first quarter earnings release. In its April 26 release Chipotle reported another significant decline in its same-store sales of 29.7%. Conversely, Panera reported a 6.2% increase for the same fiscal period. Key Takeaway As Chart 1 illustrates there appears to be a meaningful correlation between the trend of Chipotle’s same-store sales and Panera’s as Chipotle’s food contamination issues surfaced. This would largely be attributable to the high competition intensity between the chains as the illustrations below show. Chart 1. Chipotle & Panera Bread Comp-Store Sales Spread 30% 20% 10% CMG 0% PNRA -10% Spread -20% -30% 1Q15 2Q15 3Q15 4Q15 1Q16 Downloaded from www.hvst.com by IP address 192.168.160.10 on 09/26/2021 MORE INSIGHTS. MORE OFTEN. BETTER RETURNS. Illustration 1, which is from DISCERN’s database of retailer and restaurant locations, quantifies to what extent Chipotle and Panera overlap within their respective five mile trade area geographies. The data shows that Chipotle and Panera compete within the same five mile trade area in 86% of the total trade areas, a significant amount of restaurant overlap for 2 large competitors within the fast casual restaurant sector. -

When Fear Is Substituted for Reason: European and Western Government Policies Regarding National Security 1789-1919

WHEN FEAR IS SUBSTITUTED FOR REASON: EUROPEAN AND WESTERN GOVERNMENT POLICIES REGARDING NATIONAL SECURITY 1789-1919 Norma Lisa Flores A Dissertation Submitted to the Graduate College of Bowling Green State University in partial fulfillment of the requirements for the degree of DOCTOR OF PHILOSOPHY December 2012 Committee: Dr. Beth Griech-Polelle, Advisor Dr. Mark Simon Graduate Faculty Representative Dr. Michael Brooks Dr. Geoff Howes Dr. Michael Jakobson © 2012 Norma Lisa Flores All Rights Reserved iii ABSTRACT Dr. Beth Griech-Polelle, Advisor Although the twentieth century is perceived as the era of international wars and revolutions, the basis of these proceedings are actually rooted in the events of the nineteenth century. When anything that challenged the authority of the state – concepts based on enlightenment, immigration, or socialism – were deemed to be a threat to the status quo and immediately eliminated by way of legal restrictions. Once the façade of the Old World was completely severed following the Great War, nations in Europe and throughout the West started to revive various nineteenth century laws in an attempt to suppress the outbreak of radicalism that preceded the 1919 revolutions. What this dissertation offers is an extended understanding of how nineteenth century government policies toward radicalism fostered an environment of increased national security during Germany’s 1919 Spartacist Uprising and the 1919/1920 Palmer Raids in the United States. Using the French Revolution as a starting point, this study allows the reader the opportunity to put events like the 1848 revolutions, the rise of the First and Second Internationals, political fallouts, nineteenth century imperialism, nativism, Social Darwinism, and movements for self-government into a broader historical context. -

People & Economic Activity

PEOPLE & ECONOMIC ACTIVITY STARBUCKS An economic enterpise at a local scale Dr Susan Bliss STAGE 6: Geographical investigation ‘Students will conduct a geographical study of an economic enterprise operating at a local scale. The business could be a firm or company such as a chain of restaurants. 1. Nature of the economic enterprise – chain of 5. Ecological dimension restaurants, Starbucks • Inputs: coffee, sugar, milk, food, energy, water, • Overview of coffee restaurants – types sizes and transport, buildings growth. Latte towns, coffee shops in gentrified inner • Outputs: carbon and water footprints; waste. suburbs and coffee sold in grocery stores, petrol stations and book stores. Drive through coffee places • Environmental goals: sustainability.‘Grounds for your and mobile coffee carts. Order via technology-on garden’, green power, reduce ecological footprints demand. Evolving coffee culture. and waste, recycling, corporate social responsibilities, farmer equity practices, Fairtrade, Ethos water, • Growth of coffee restaurant chains donations of leftover food 2. Locational factors 6. Environmental constraints: climate change, • Refer to website for store locations and Google Earth environmental laws (local, national). • Site, situation, latitude, longitude 7. Effects of global changes on enterprise: • Scale – global, national, local prices, trade agreements, tariffs, climate change, competition (e.g. McDonalds, soft drinks, tea, water), • Reasons for location – advantages changing consumer tastes. Growth of organic and • Growth in Asian countries https://www.starbucks. speciality coffees. Future trends – Waves of Coffee com/store- locator?map=40.743095,-95.625,5z Starbucks chain of restaurants 3. Flows Today Starbucks is the largest coffee chain in the world, • People: customers – ages as well as the premier roaster and retailer of specialty • Goods: coffee, milk, sugar, food coffee. -

Country Coffee Profile Italy Icc-120-6 1

INTERNATIONAL COFFEE ORGANIZATION COUNTRY COFFEE PROFILE ITALY ICC-120-6 1 COUNTRY COFFEE PROFILE ITALY ICO Coffee Profile Italy 2 ICC-120-6 CONTENTS Preface .................................................................................................................................... 3 Foreword ................................................................................................................................. 4 1. Background ................................................................................................................. 5 1.1 Geographical setting ....................................................................................... 5 1.2 Economic setting in Italy .................................................................................. 6 1.3 History of coffee in Italy .................................................................................. 6 2. Coffee imports from 2000 to 2016 ............................................................................. 8 2.1 Volume of imports .......................................................................................... 8 2.2 Value and unit value of imports ..................................................................... 14 2.3 Italian Customs – Import of green coffee ...................................................... 15 3. Re-exports from 2000 to 2016 ................................................................................... 16 3.1 Total volume of coffee re-exports by type and form ................................... -

National Retailer & Restaurant Expansion Guide Spring 2016

National Retailer & Restaurant Expansion Guide Spring 2016 Retailer Expansion Guide Spring 2016 National Retailer & Restaurant Expansion Guide Spring 2016 >> CLICK BELOW TO JUMP TO SECTION DISCOUNTER/ APPAREL BEAUTY SUPPLIES DOLLAR STORE OFFICE SUPPLIES SPORTING GOODS SUPERMARKET/ ACTIVE BEVERAGES DRUGSTORE PET/FARM GROCERY/ SPORTSWEAR HYPERMARKET CHILDREN’S BOOKS ENTERTAINMENT RESTAURANT BAKERY/BAGELS/ FINANCIAL FAMILY CARDS/GIFTS BREAKFAST/CAFE/ SERVICES DONUTS MEN’S CELLULAR HEALTH/ COFFEE/TEA FITNESS/NUTRITION SHOES CONSIGNMENT/ HOME RELATED FAST FOOD PAWN/THRIFT SPECIALTY CONSUMER FURNITURE/ FOOD/BEVERAGE ELECTRONICS FURNISHINGS SPECIALTY CONVENIENCE STORE/ FAMILY WOMEN’S GAS STATIONS HARDWARE CRAFTS/HOBBIES/ AUTOMOTIVE JEWELRY WITH LIQUOR TOYS BEAUTY SALONS/ DEPARTMENT MISCELLANEOUS SPAS STORE RETAIL 2 Retailer Expansion Guide Spring 2016 APPAREL: ACTIVE SPORTSWEAR 2016 2017 CURRENT PROJECTED PROJECTED MINMUM MAXIMUM RETAILER STORES STORES IN STORES IN SQUARE SQUARE SUMMARY OF EXPANSION 12 MONTHS 12 MONTHS FEET FEET Athleta 46 23 46 4,000 5,000 Nationally Bikini Village 51 2 4 1,400 1,600 Nationally Billabong 29 5 10 2,500 3,500 West Body & beach 10 1 2 1,300 1,800 Nationally Champs Sports 536 1 2 2,500 5,400 Nationally Change of Scandinavia 15 1 2 1,200 1,800 Nationally City Gear 130 15 15 4,000 5,000 Midwest, South D-TOX.com 7 2 4 1,200 1,700 Nationally Empire 8 2 4 8,000 10,000 Nationally Everything But Water 72 2 4 1,000 5,000 Nationally Free People 86 1 2 2,500 3,000 Nationally Fresh Produce Sportswear 37 5 10 2,000 3,000 CA -

Mary C. Egan and Drew Madsen Appointed to Noodles & Company

September 25, 2017 Mary C. Egan and Drew Madsen Appointed to Noodles & Company Board of Directors BROOMFIELD, Colo., Sept. 25, 2017 (GLOBE NEWSWIRE) -- Noodles & Company (NASDAQ:NDLS) today announced the appointment of Mary C. Egan and Drew Madsen as independent members of its Board of Directors effective September 22, 2017. Ms. Egan was also appointed to the Audit Committee of the Board of Directors. "We are pleased to announce the addition of two talented individuals to our Board of Directors," said Paul Murphy, Executive Chairman of Noodles & Company. "Both Mary and Drew are proven leaders, with significant strategic and operational experience in consumer-centric growth strategy and execution. We believe they will be invaluable resources to our entire organization as we focus on improving the performance and profitability of Noodles & Company." Ms. Egan co-founded and currently serves as CEO of Gatheredtable, a profitable consumer SaaS company offering customized meal planning. Prior to Gatheredtable, Ms. Egan served as Head of Global Strategy and Corporate Development at Starbucks, where she partnered with the senior leadership team to develop and execute corporate strategy, and led many successful strategic initiatives focusing on cost reduction, developing markets, digital, and food. Before joining Starbucks, Ms. Egan was a Managing Director at The Boston Consulting Group where she partnered with CEO's and boards of leading consumer brands to conceive and successfully drive aggressive growth strategies. While at BCG, she was a frequent global speaker on consumer-centric growth, and was featured in many news outlets, including The Wall Street Journal and The New York Times. -

A Chapter in the History of Coffee: a Critical Edition and Translation of Murtad}A> Az-Zabīdī's Epistle on Coffee

A Chapter in the History of Coffee: A Critical Edition and Translation of Murtad}a> az-Zabīdī’s Epistle on Coffee Presented in Partial Fulfillment of the Requirements for the Degree Master of Arts in the Graduate School of The Ohio State University By Heather Marie Sweetser, B.A. Graduate Program in Near Eastern Languages and Cultures The Ohio State University 2012 Thesis Committee: Dr. Georges Tamer, Advisor Dr. Joseph Zeidan Copyright by Heather Marie Sweetser 2012 Abstract What follows is an edition and translation of an Arabic manuscript written by Murtad}a> az-Zabīdī in 1171/1758 in defense of coffee as per Islamic legality. He cites the main objections to coffee drinking and refutes them systematically using examples from Islamic jurisprudence to back up his points. The author also includes lines of poetry in his epistle in order to defend coffee’s legality. This particular manuscript is important due to its illustrious author as well as to its content, as few documents describing the legal issues surrounding coffee at such a late date have been properly explored by coffee historians. The dictionary Ta>j al-ʿAru>s, authored by Murtad}a> az-Zabīdī himself, as well as Edward Lane’s dictionary, were used to translate the manuscript, which was first edited. Unfortunately, I was only able to acquire one complete and one incomplete manuscript; other known manuscripts were unavailable. Arabic mistakes in the original have been corrected and the translation is annotated to provide appropriate background to the epistle’s commentary. A brief introduction to the history of coffee, a sample of the debate surrounding the legality of coffee in Islam, and a biography of the author is provided. -

Mcdonald's Targets Starbucks

BTS NRC MUC – NRC - TC McDonald's Targets Starbucks The fast-food company expects to add $1 billion in sales by offering specialty coffee drinks in all its U.S. restaurants. 10 January 2008 This is the VOA Special English Economics Report written by Mario Ritter McDonald's, the fast-food company, is heating up competition with the Starbucks Coffee Company. McDonald's plans to put coffee bars in its restaurants in the United States. McDonald's has enjoyed several years of strong growth. The company had almost twenty-two billion dollars in sales in two thousand six. Still, the move to compete against Starbucks carries some risk. Some experts say it could slow down service at McDonald's restaurants. And some people who are happy with McDonald's the way it is now may not like the changes. Starbucks, on the other hand, has faced slower growth and increasing competition. Starbucks has about ten thousand stores in the United States. Its high-priced coffee drinks have names like Iced Peppermint White Chocolate Mocha and Double Chocolate Chip Frappuccino. But a year ago he warned that its fast growth had led to what he called the watering down of the Starbucks experience. Some neighborhoods have a Starbucks on every block or two. Now, Starbucks will speed up its international growth while slowing its expansion in the United States. Millions of people have a taste for Starbucks. But testers from Consumer Reports thought Mc Donald’s coffee tasted better than Starbucks, and it cost less. . -

Espresso House Sweden Adds Caliente to Their Range

The growth of Caliente non-alcoholic drinks continues May 14, 2018 13:43 CEST Espresso House Sweden adds Caliente to their range “We’re thrilled that Caliente is part of the range at Espresso House, the leading coffee shop chain in the Nordic countries,” says Thomas Adners, the founder of Caliente. Espresso House is a Swedish coffee shop chain founded in Lund in 1996. Today Espresso House is present in all Nordic countries, with a total of 400 coffee shops and 3500 baristas. Espresso House only serve premium coffee, so called Specialty Coffee, roasted in their own coffee roastery in Länna. The cosy atmosphere and pastries from the own bakery are other important aspects of the Espresso House experience. Caliente has spread across Sweden, Europe and India since the launch in 2015. Their innovative idea is to create a drink based on the substance capsaicin – extracted chili heat. Caliente has been extremely well received both by the industry and consumers looking for a sophisticated and social drink without alcohol. One reason could be that young grown-ups demand more from social drinks without alcohol, and Caliente is one of few options offering a unique sensation – in this case taste and a light kick from chili. Caliente Blueberry Lemongrass Chili (chili heat level 3/5) and Ginger Lime Chili (chili heat level 4/5) are the two chosen flavors. Both contain low levels ofsugar and are bottled in Sweden from organic and natural ingredients. We want to make it easier to choose non-alcoholic. And realized that the same stuff that makes chilies hot – capsaicin – doesn’t just have the same lingering taste as alcohol. -

Embracing Our Heritage and Values While Aiming Higher

Fiscal 2012 Financial Highlights Net Revenues (in Billions) Comparable Store Sales Growth $13.3 (Company-Operated Stores Open 13 Months or Longer) $11.7 $10.7 8% $10.4 7%* 7% $9.8 –3% 1971 Seattle –6% 2008 2009 2010 2011 2012 2008 2009 2010 2011 2012 Operating Income (in Millions) Operating Margin GAAP Non-GAAP GAAP Non-GAAP 14.8% 15.0% $1,997 14.5%** 13.3% 13.5%** $1,728 $1,698** The artwork on the cover is inspired by the Siren from $1,419 $1,414** 9.2%** our original store's logo in Seattle's Pike Place Market. Embracing our heritage and values 8.1%** ** $894** The second illustration comes from the interior of our $843 5.7% 4.9% $562 first store in Mumbai, India. These drawings evoke the while aiming higher than ever. $504 Starbucks Experience, treasured in Seattle since 1971 and now around the world. Starbucks Corporation Fiscal 2012 Annual Report 2008 2009 2010 2011 2012 2008 2009 2010 2011 2012 Earnings per Diluted Share Operating Cash Flow & Capital Expenditures (in Millions) GAAP EPS Non-GAAP EPS Cash from Operations Capital Expenditures $1.79 $1,705 $1,750 $1,612 $1.62 $1.52*** $1,389 $1,259 $1.24 $1.23** $985 $856 $0.80** 2012 Mumbai $0.71** $0.52 $532 $0.43 $446 $441 2008 2009 2010 2011 2012 2008 2009 2010 2011 2012 * 2010 comparable store sales growth was calculated excluding the additional week in September 2010. ** Non-GAAP measure. Excludes $339, $332 and $53 million in pretax restructuring and transformation charges in 2008, 2009 and 2010, respectively. -

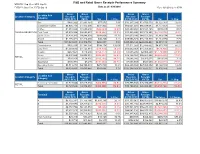

F&B and Retail Gross Receipts Performance Summary

F&B and Retail Gross Receipts Performance Summary MTD PFY: Sep 15 vs. MTD: Sep 16 FYTD PY: Sep 15 vs. FYTD: Sep 16 Data as of: 9/30/2016 Run: 12/1/2016 2:14:15 PM 12:00:00 AM Gross Gross Gross Gross Location Sub Location Category Receipts Receipts Receipts Receipts Category (MTD PFY) (MTD) Var % Chg (FYTD PFY) (FYTD) Var % Chg Bar $985,292 $1,063,164 $77,872 7.9% $10,237,209 $13,559,570 $3,322,361 32.5% Casual Dining/Bar $6,930,743 $7,472,696 $541,952 7.8% $83,051,037 $86,828,087 $3,777,051 4.5% Coffee $1,663,026 $1,620,456 ($42,569) (2.6%) $20,593,466 $21,123,745 $530,279 2.6% FOOD & BEVERAGE Fast Food $3,272,934 $2,653,679 ($619,254) (18.9%) $39,936,206 $37,772,391 ($2,163,816) (5.4%) Quick-Serve $3,439,385 $4,048,054 $608,669 17.7% $42,670,286 $44,553,560 $1,883,274 4.4% Snack $1,276,421 $1,316,689 $40,268 3.2% $15,056,923 $16,218,893 $1,161,970 7.7% Total $17,567,801 $18,174,738 $606,937 3.5% $211,545,128 $220,056,247 $8,511,119 4.0% Convenience $592,130 $1,341,304 $749,174 126.5% $7,511,263 $12,486,622 $4,975,359 66.2% Duty Free $1,203,685 $1,125,314 ($78,370) (6.5%) $15,632,363 $14,753,053 ($879,309) (5.6%) Kiosks $287,657 $118,240 ($169,417) (58.9%) $4,086,286 $2,906,298 ($1,179,988) (28.9%) News $2,597,882 $2,005,573 ($592,309) (22.8%) $32,124,769 $26,461,368 ($5,663,400) (17.6%) RETAIL News/Coffee $793,250 $678,050 ($115,199) (14.5%) $8,686,166 $9,305,677 $619,511 7.1% Spa/Salon $138,982 $7,429 ($131,553) (94.7%) $2,005,669 $541,657 ($1,464,012) (73.0%) Specialty Retail $3,711,278 $4,390,033 $678,755 18.3% $42,200,052 $47,368,052