City Office Market Watch February 2013

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Buses from Holborn Circus and Chancery Lane BRIXTON

HOLLOWAY ILFORD KENTISH HACKNEY TOWN ISLINGTON SHOREDITCH BETHNAL GREEN Buses from Holborn Circus and Chancery Lane BRIXTON 24 hour Northumberland Park 341 service 17 Tesco and IKEA Key continues to Maida Vale Archway Northumberland Park N8 Hall Road Hainault 8 Day buses in black The Lowe Lansdowne Road St JohnÕs Wood 24 hour N8 Night buses in blue Swiss Cottage Upper Holloway 25 service Wanstead Ilford Bruce Grove Hainault Street —O Connections with London Underground Warwick Avenue FitzjohnÕs Avenue HOLLOWAY o Connections with London Overground Holloway Tottenham Leytonstone Ilford Hampstead NagÕs Head Police Station Green Man 24 hour R Connections with National Rail West Green Road 242 service ILFORD Paddington Caledonian Road Homerton Hospital BishopÕs Bridge Road Philip Lane Leytonstone Manor Park DI Connections with Docklands Light Railway Harringay Green Lanes Broadway Clapton Park B Royal Free Hospital Caledonian Road & Barnsbury Connections with river boats Lancaster Gate Manor House Millfields Road Woodgrange 46 Leytonstone Park I Mondays to Fridays only Hackney Downs Hampstead Heath Green Lanes High Road South End Green Caledonian Road Forest Gate Copenhagen Street Lordship Park Newington Green Hackney Central Maryland Princess Alice Kentish Town West Caledonian Road Stratford Carnegie Street Newington Green Road Graham Road Balls Pond Road Bus Station KENTISH Kentish Town Road HACKNEY Essex Road Caledonian Road Stratford High Street Killick Street Dalston Junction TOWN Royal Camden Road Essex Road Old Ford College Pancras -

UC Riverside UC Riverside Electronic Theses and Dissertations

UC Riverside UC Riverside Electronic Theses and Dissertations Title Mobilizing the Metropolis: Politics, Plots and Propaganda in Civil War London, 1642-1644 Permalink https://escholarship.org/uc/item/3gh4h08w Author Downs, Jordan Publication Date 2015 Peer reviewed|Thesis/dissertation eScholarship.org Powered by the California Digital Library University of California UNIVERSITY OF CALIFORNIA RIVERSIDE Mobilizing the Metropolis: Politics, Plots and Propaganda in Civil War London, 1642-1644 A Dissertation submitted in partial satisfaction of the requirements for the degree of Doctor of Philosophy in History by Jordan Swan Downs December 2015 Dissertation Committee: Dr. Thomas Cogswell, Chairperson Dr. Jonathan Eacott Dr. Randolph Head Dr. J. Sears McGee Copyright by Jordan Swan Downs 2015 The Dissertation of Jordan Swan Downs is approved: ___________________________________ ___________________________________ ___________________________________ ___________________________________ Committee Chairperson University of California, Riverside Acknowledgements I wish to express my gratitude to all of the people who have helped me to complete this dissertation. This project was made possible due to generous financial support form the History Department at UC Riverside and the College of Humanities and Social Sciences. Other financial support came from the William Andrew’s Clark Memorial Library, the Huntington Library, the Institute of Historical Research in London, and the Santa Barbara Scholarship Foundation. Original material from this dissertation was published by Cambridge University Press in volume 57 of The Historical Journal as “The Curse of Meroz and the English Civil War” (June, 2014). Many librarians have helped me to navigate archives on both sides of the Atlantic. I am especially grateful to those from London’s livery companies, the London Metropolitan Archives, the Guildhall Library, the National Archives, and the British Library, the Bodleian, the Huntington and the William Andrews Clark Memorial Library. -

The Smithfield Gazette

THE SMITHFIELD GAZETTE EDITION 164 April 2018 REMEMBERING THE POULTRY MARKET FIRE Early on 23 January 1958 a fire broke out in the basement of the old Poultry Market building at Smithfield Market. It was to be one of the worst fires London had seen since the Blitz. The old Poultry Market was similar in style to the two remaining Victorian buildings – it was also designed by Sir Horace Jones and opened in 1875. In a moving ceremony held in Grand Avenue exactly sixty years after the fire started, the two firefighters who died were remembered by the unveiling of one of the Fire Brigades Union’s new red plaques. Wreaths were laid by Matt Wrack, General Secretary of the Fire Brigades Union, Greg Lawrence, Chairman of the Smithfield Market Tenants’ Association and Mark Sherlock, Superintendent of Smithfield Market. Serving and retired firefighters attended as well as Market tenants and representatives of the City of London. Two fire engines were also there. The fire burned for three days in the two and a half acre basement, which was full of crates of poultry as well as being lined with wooden match boarding which had become soaked with fat over a period of years – this meant that the fire spread exceptionally quickly. Reports of the time state that by dawn the stalls and market contents had been destroyed, the roof had collapsed and what was left was a blackened shell enclosing a twisted heap of ironwork and broken masonry. Flames 100 feet high lit the night sky. Firefighters from Clerkenwell fire station were the first to arrive on the scene, including Station Officer Jack Fourt-Wells, aged 46, and Firefighter Richard Stocking, 31, the two who lost their lives. -

1 Giltspur Street

1 GILTSPUR STREET LONDON EC1 1 GILTSPUR STREET 1 GILTSPUR STREET INVESTMENT HIGHLIGHTS • Occupies a prominent corner position in the heart of Midtown, where the City of London and West End markets converge. • Situated on the west side of Giltspur Street at its junction with West Smithfield and Hosier Lane to the north and Cock Lane to the south. • In close proximity to Smithfield Market and Farringdon Station to the north. • Excellent transport connectivity being only 200m from Farringdon Station which, upon delivery of the Elizabeth Line in autumn 2019, will be the only station in Central London to provide direct access to London Underground, the Elizabeth Line, Thameslink and National Rail services. • 23,805 sq. ft. (2,211.4 sq. m.) of refurbished Grade A office and ancillary accommodation arranged over lower ground, ground and four upper floors. • Held long leasehold from The Mayor and Commonalty of the City of London for a term of 150 years from 24 June 1991 expiring 23 June 2141 (approximately 123 years unexpired) at a head rent equating to 7.50% of rack rental value. • Vacant possession will be provided no later than 31st August 2019. Should completion of the transaction occur prior to this date the vendor will remain in occupation on terms to be agreed. We are instructed to seek offers in excess of£17 million (Seventeen Million Pounds), subject to contract and exclusive of VAT, for the long leasehold interest, reflecting a low capital value of £714 per sq. ft. 2 3 LOCATION & SITUATION 1 Giltspur Street is located in a core Central London location in the heart of Midtown where the City of London and West End markets converge. -

Trustees' Annual Report and Financial Statements 31 March 2016

THE FRANCIS CRICK INSTITUTE LIMITED A COMPANY LIMITED BY SHARES TRUSTEES’ ANNUAL REPORT AND FINANCIAL STATEMENTS 31 MARCH 2016 Charity registration number: 1140062 Company registration number: 6885462 The Francis Crick Institute Accounts 2016 CONTENTS INSIDE THIS REPORT Trustees’ report (incorporating the Strategic report and Directors’ report) 1 Independent auditor’s report 12 Consolidated statement of financial activities 13 Balance sheets 14 Cash flow statements 15 Notes to the financial statements 16 1 TRUSTEES’ REPORT (INCORPORATING THE STRATEGIC REPORT AND DIRECTORS’ REPORT) The trustees present their annual directors’ report together with the consolidated financial statements for the charity and its subsidiary (together, ‘the Group’) for the year ended 31 March 2016, which are prepared to meet the requirements for a directors’ report and financial statements for Companies Act purposes. The financial statements comply with the Charities Act 2011, the Companies Act 2006, and the Statement of Recommended Practice applicable to charities preparing their accounts in accordance with the Financial Reporting Standard applicable in the UK (FRS102) effective 1 January 2015 (Charity SORP). The trustees’ report includes the additional content required of larger charities. REFERENCE AND ADMINISTRATIVE DETAILS The Francis Crick Institute Limited (‘the charity’, ‘the Institute’ or ‘the Crick) is registered with the Charity Commission, charity number 1140062. The charity has operated and continues to operate under the name of the Francis Crick -

Hatton Garden Bid Proposal

HATTON GARDEN BID PROPOSAL 2021 – 2026 Working together to showcase the best of Hatton Garden 1 Hatton Garden BID Proposal April 21 – March 26 2 to be welcomed, especially if we must learn to live with social distancing measures for the foreseeable Five years of delivery... and we’re just getting started. future. The commencement of Crossrail services is a significant opportunity for Hatton Garden and the BID It’s hard to believe that almost five years have passed since is determined to ensure the benefits are felt by the our first ballot and the Hatton Garden BID was established. whole of our business community. What a first term it’s been: three Prime Ministers, two royal This Business Plan sets out our ambitions plans for weddings, three General Elections, the 100th anniversary our second term. You will see that we are stretching since World War One and partial women’s suffrage, the Brexit ourselves to continue delivering the best for Hatton Garden. Across our core strategic themes we will Referendum and of course, one global pandemic. remain your business advocate, your helping hand, your advice giver as well as a place-maker, a good CONTENTS times creator, a warm welcome and a protector. Amid this fast changing political and social many creative, cultural and corporate We are proudly pushing the boundaries, looking at landscape, Hatton Garden has been industries who want to be part of this thriving Chairman Foreword from Gary Williams 1 changing too. I have worked in the Garden hub. And while much has been achieved all factors that need to combine to make a place for more than 45 years and I still passionately over the past five years, our work is not done. -

CAMDEN STREET NAMES and Their Origins

CAMDEN STREET NAMES and their origins © David A. Hayes and Camden History Society, 2020 Introduction Listed alphabetically are In 1853, in London as a whole, there were o all present-day street names in, or partly 25 Albert Streets, 25 Victoria, 37 King, 27 Queen, within, the London Borough of Camden 22 Princes, 17 Duke, 34 York and 23 Gloucester (created in 1965); Streets; not to mention the countless similarly named Places, Roads, Squares, Terraces, Lanes, o abolished names of streets, terraces, Walks, Courts, Alleys, Mews, Yards, Rents, Rows, alleyways, courts, yards and mews, which Gardens and Buildings. have existed since c.1800 in the former boroughs of Hampstead, Holborn and St Encouraged by the General Post Office, a street Pancras (formed in 1900) or the civil renaming scheme was started in 1857 by the parishes they replaced; newly-formed Metropolitan Board of Works o some named footpaths. (MBW), and administered by its ‘Street Nomenclature Office’. The project was continued Under each heading, extant street names are after 1889 under its successor body, the London itemised first, in bold face. These are followed, in County Council (LCC), with a final spate of name normal type, by names superseded through changes in 1936-39. renaming, and those of wholly vanished streets. Key to symbols used: The naming of streets → renamed as …, with the new name ← renamed from …, with the old Early street names would be chosen by the name and year of renaming if known developer or builder, or the owner of the land. Since the mid-19th century, names have required Many roads were initially lined by individually local-authority approval, initially from parish named Terraces, Rows or Places, with houses Vestries, and then from the Metropolitan Board of numbered within them. -

Document.Pdf

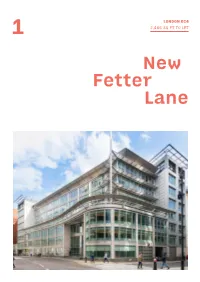

KI NG ’S C R OSS R D . FA R R IN GD O N R D. L RD LOCATION L NWE KE F LER AR C H A R T I NG TO Positioned between Holborn Circus and New Street Square GR N DO A G GRAY'S INN Y’ N BARBICAN RD AR 1 New Fetter Lane has unrivalled connectivity being within a ’S S FARRINGDON LD GARDENS RD OBA IN DE E N TH N short walk to Farringdon (Thameslink, Crossrail, Circle, RO ST SE AD U O ERH ART Metropolitan and Hammersmith & City lines) along with CH D AL FIEL GI TH DERS SMITHFIELDSMI MARKET Chancery Lane (Central Line) and Blackfriars HIGH HOLBORN HOLBORN T LT WES SPUR ST GA HOLBORN HO (Circle and District Lines and Thameslink). A TE ST ND L ST C CHANCERY BOR HANC E FA N K LANE RE VI IN N AD LINCOLN'S W RR U GS LA CT The building is also adjacent to the eclectic mix of retail, ER INN FIELDS ST IN WA ER CITY Y RE TT GDON Y LA THAMESLINK restaurants and bars of New Street Square and Clerkenwell. ET FE NE 1 W ST NE ST. PAUL’S STRAND STRAND FLEET ST LUDGATE HIL ST. PAULS NE L MIDD ES LA AR CATHEDRAL W SE NC UNDE BR X ST LE TE CITY AS ID THAMESLINK TE L ST GE MP R PL TUDOR ST ST LE LN QUEEN VICTORIA ST MANSION HOUSE BLACKFRIARS VICTORIA EMBANKMENT UPPER THAMES ST RIVER THAMES DESCRIPTION PART 3RD FLOOR PLAN 1 New Fetter Lane is a prominent headquarters building located 2,466 SQ FT (229.1 SQ M) in the heart of London’s Midtown. -

History of the River Fleet

The History of the River Fleet Compiled by The UCL River Fleet Restoration Team 27 th March 2009 All images within this document are subject to copyright restrictions and should not be used without permission from the River Fleet Restoration Team. 2 Contents 1 Overview .............................................................................................................. 5 1.1 Etymology ..................................................................................................... 5 1.2 The source of the River ................................................................................. 5 1.3 Uses of the River ........................................................................................... 5 1.4 Flooding ........................................................................................................ 6 1.5 Maintenance of the River .............................................................................. 7 1.6 Enclosure of the River ................................................................................... 8 2 Places of Historical interest along the River .................................................... 11 2.1 Hampstead Ponds ......................................................................................... 11 2.2 Highgate Ponds ............................................................................................ 11 2.3 Kentish Town .............................................................................................. 12 2.4 St Pancras Old Church ............................................................................... -

Trades Directory, 1910. Dia-Din

1527 TRADES DIRECTORY, 1910. DIA-DIN J'oseph Brothere, 28 Holborn viaduct E C t WarwickBenjamin,l6&18KingWilliam st E C Mead Joseph Ltn.. 102 Sonthwark street SE t§PearRon Oha~. & Son Lt-1.93 & 05 :Mansell st, Josephi Benj. Henry, 17 Hatton garden E: C tWatherston & Son,6 Vigo street,Regent et W PowellN. J. &Co.101 Whitech'lpel High&t E Ald:;ate E ; 53 Leadenhall st E C ; 34 ,\br 11: Kaufma.nn Jonas Bemard,96 Hatton gdnE C Weisz N. 73 Hatton garden E C Smith T. J. & J. Lt<l. 26 Ollarterltouse sq E C lane E C & 1 Bi'hop<gate chnrchya ·d E C t•Keller L. & Co. 88 Hatton garden E C tWellby Danl. &Jn. I...im. 18&20Garrick st'NC Speller Jamea & Co. (Oharterhouse series), §Phipps & Connor, 13 & 14 Tothill Rtrcct SW Kendal & Dent, 106 Oheapside E C Wernher.Beit &Co.29 &30Holborn viaduct E C 61 to 65 Golden lane E C Phamix Art Metal En~;n'lering O.l. Ltd. 27 A, •~King John William, 1 Albemarle street E C WheelerHaydenW.&Co.50Holborn viaoctE C Btraker Chas.& Sons Ltd. 38 King Willm.st E C & 40 Ooin street, Stamford street SE •tKlean Michael& Co. 70MyddeltonstreetE C Wnigtler E•l ward & Co. l1 Strand WC STRAKER & CRA.NES DIARY CO. LTD. §Pi card & Boyle, 259 St. John sti·ect E C Kmuss Brothers, 101 llatton garden E C WHITEHORN BRO-rHERS, 19, 20 & 21 "PettittR," " HlaekwoOlls," "Gossamer," t§Pinches John, 21 Alhcrt embank:mP.nt SE Krolik Lippm~nn (agent), 7 Warwick et WC Featherstone buildings WC "Crown,""Rensha ws," ''Cranes,""Pennys" Pratt Tl10B. -

Two Waterhouse Square Midtown Fourth Floor Two Waterhouse Square Midtown

TWO WATERHOUSE SQUARE MIDTOWN FOURTH FLOOR TWO WATERHOUSE SQUARE MIDTOWN 183,286 sq ft of new Category ‘A’ offices. A DEVELOPMENT BY The modern offices of Two Waterhouse Square sit behind gothic façades of vibrant red brick. Dramatic arches and tranquil squares combine to make Two Waterhouse Square one of London’s most distinguished landmark buildings. ...a stunning courtyard provides access to Two Waterhouse Square. ...a magnificent lobby area bridges the old with the new. ...the majestic lobby leads in to an inspirational atrium. At its centre is a modern reception ‘pod’, above which are suspended two vast rings of highly polished steel. ...two banks of four passenger lifts provide fast access to the floors above. All of these floors ‘grip’ the central atrium. There are two other atria within the building. ...expansive 30,000 square feet floorplates with excellent natural light, enable efficient and effective occupation. E U N E V A Y R R ST GEORGE’S E T B GARDENS E E E S R O T R S E P 5 R M I O N U H T T L 4 E A S C W ...midtown is central London. A F A L R Midway between the City and the West End, R K I N 6 11 G D 5 O N 7 Two Waterhouse Square is located at R O A D 6 4 CLERKENWELL 5 its epicentre - perfectly situated for North, South, A D R O RUSSELL GREAT ORMOND 2 E L L E N W SQUARE STREET HOSPITAL L E R K G C East and West travel within the capital. -

London Metropolitan Archives Saint

LONDON METROPOLITAN ARCHIVES Page 1 SAINT ANDREW, HOLBORN: HOLBORN CIRCUS, CITY OF LONDON P82/AND Reference Description Dates PARISH RECORDS - LMA holdings Parish Records P82/AND/001 Minutes of Trustees Apr 1726-Mar Indexed 1745/6 P82/AND/002 Minutes of Trustees May 1746-Mar Indexed 1785 P82/AND/003 Minutes of General Committee Jan 1801-Aug 1816 P82/AND/004 Minutes of General Committee Aug 1816-Dec 1828 P82/AND/005 Minutes of General Committee Jan 1829-Jul 1843 P82/AND/006 Rough Minutes of General Committee Dec 1827-Aug 1837 P82/AND/007 Rough Minutes of General Committee Sep 1837-Mar 1854 P82/AND/008 Rough Minutes of General Committee Apr 1854-Aug 1866 P82/AND/009 Rough Minutes of General Committee Aug 1862-Dec Indexed. Includes, at front, Copy conveyances 1898 of school by bishop of Ely to school Lessees and school Lessees to rector and churchwardens P82/AND/010 Rough Minutes of General Committee Sep 1866-Jan In-letters pasted in 1899 P82/AND/011 Minutes of various Committees, mainly Jan 1828-Jan Education and Finance 1861 Includes number of audited accounts P82/AND/012 Audited accounts approved by Finance Apr 1861-May Committee 1901 LONDON METROPOLITAN ARCHIVES Page 2 SAINT ANDREW, HOLBORN: HOLBORN CIRCUS, CITY OF LONDON P82/AND Reference Description Dates P82/AND/013 Treasurers' account book, with statements re 1828-1891 capital and receipts for annuity from consols at end P82/AND/014 Cash Book Jul 1895-Oct Gives expenditure on teachers' salaries, 1899 monitors, books, stationery, fuel, lighting, furniture replacements, books, etc.