NACDS 2013 Annual Meeting

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FIC-Prop-65-Notice-Reporter.Pdf

FIC Proposition 65 Food Notice Reporter (Current as of 9/25/2021) A B C D E F G H Date Attorney Alleged Notice General Manufacturer Product of Amended/ Additional Chemical(s) 60 day Notice Link was Case /Company Concern Withdrawn Notice Detected 1 Filed Number Sprouts VeggIe RotInI; Sprouts FruIt & GraIn https://oag.ca.gov/system/fIl Sprouts Farmers Cereal Bars; Sprouts 9/24/21 2021-02369 Lead es/prop65/notIces/2021- Market, Inc. SpInach FettucIne; 02369.pdf Sprouts StraIght Cut 2 Sweet Potato FrIes Sprouts Pasta & VeggIe https://oag.ca.gov/system/fIl Sprouts Farmers 9/24/21 2021-02370 Sauce; Sprouts VeggIe Lead es/prop65/notIces/2021- Market, Inc. 3 Power Bowl 02370.pdf Dawn Anderson, LLC; https://oag.ca.gov/system/fIl 9/24/21 2021-02371 Sprouts Farmers OhI Wholesome Bars Lead es/prop65/notIces/2021- 4 Market, Inc. 02371.pdf Brad's Raw ChIps, LLC; https://oag.ca.gov/system/fIl 9/24/21 2021-02372 Sprouts Farmers Brad's Raw ChIps Lead es/prop65/notIces/2021- 5 Market, Inc. 02372.pdf Plant Snacks, LLC; Plant Snacks Vegan https://oag.ca.gov/system/fIl 9/24/21 2021-02373 Sprouts Farmers Cheddar Cassava Root Lead es/prop65/notIces/2021- 6 Market, Inc. ChIps 02373.pdf Nature's Earthly https://oag.ca.gov/system/fIl ChoIce; Global JuIces Nature's Earthly ChoIce 9/24/21 2021-02374 Lead es/prop65/notIces/2021- and FruIts, LLC; Great Day Beet Powder 02374.pdf 7 Walmart, Inc. Freeland Foods, LLC; Go Raw OrganIc https://oag.ca.gov/system/fIl 9/24/21 2021-02375 Ralphs Grocery Sprouted Sea Salt Lead es/prop65/notIces/2021- 8 Company Sunflower Seeds 02375.pdf The CarrIngton Tea https://oag.ca.gov/system/fIl CarrIngton Farms Beet 9/24/21 2021-02376 Company, LLC; Lead es/prop65/notIces/2021- Root Powder 9 Walmart, Inc. -

Wal-Mart Stores Inc at William Blair & Company, LLC Growth Stock

FINAL TRANSCRIPT WMT - Wal-Mart Stores Inc at William Blair & Company, LLC Growth Stock Conference Presentation Event Date/Time: Jun. 15. 2011 / 1:00PM GMT THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us ©2011 Thomson Reuters. All rights reserved. Republication or redistribution of Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. 'Thomson Reuters' and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its affiliated companies. FINAL TRANSCRIPT Jun. 15. 2011 / 1:00PM, WMT - Wal-Mart Stores Inc at William Blair & Company, LLC Growth Stock Conference Presentation CONFERENCE CALL PARTICIPANTS Mark Miller William Blair - Analyst Bill Simon Wal-Mart Stores, Inc. - President & CEO Walmart U.S. PRESENTATION Mark Miller - William Blair - Analyst I think I©ll go ahead and get started so as not to cut in on management©s time. For those of you that I©ve not met, my name is Mark Miller; I follow the broadlines food, drug and e-commerce space at William Blair. I©m required to inform you that for a complete list of disclosures and potential conflicts of interest please see WilliamBlair.com. Following this presentation we will have a breakout in the Bellevue Room which, I think most of you know, is through at the restaurant. It is my pleasure this morning to introduce to you the management of Walmart. Walmart has presented now at our conference for nine of the ten years that I©ve been covering the Company. Carol, I appreciate the Company is back again this year. -

Amerisourcebergen Announces Strategic, Long-Term Relationship with Walgreens and Alliance Boots

Amerisourcebergen Corporation Logo AmerisourceBergen Announces Strategic, Long-Term Relationship with Walgreens and Alliance Boots March 19, 2013 Agreement Includes 10-Year Brand and Generic Distribution Contract with Walgreens and Access to Generics Sourced Through Walgreens Boots Alliance Development GmbH Joint Venture VALLEY FORGE, Pa.--(BUSINESS WIRE)--Mar. 19, 2013-- AmerisourceBergen (NYSE: ABC) today announced that it is entering into a strategic, long-term relationship with Walgreen Co. and Alliance Boots GmbH, which will streamline the distribution of pharmaceuticals to Walgreens’ stores and leverage global supply chain efficiencies while improving patient access to affordable pharmaceuticals to increase the efficiency of the healthcare system. AmerisourceBergen’s new expanded relationship with Walgreens and Alliance Boots includes: a ten-year comprehensive primary pharmaceutical distribution contract with Walgreens; access to generic drugs and related pharmaceutical products through the Walgreens Boots Alliance Development joint venture; and opportunities to accelerate the Company’s efforts to grow its specialty and manufacturer services businesses domestically and internationally. In furtherance of this new partnership, Walgreens and Alliance Boots together have been granted rights to purchase an equity position in AmerisourceBergen, which is described in greater detail below. The new agreements are expected to be meaningfully accretive to AmerisourceBergen’s earnings and strengthen its confidence in delivering solid and sustainable long-term EPS growth. AmerisourceBergen has serviced Walgreens’ specialty business for several years, and in our fiscal 2014, the new relationship is expected to contribute an incremental $28 billion in revenues and approximately 20 cents in earnings per share, excluding the amortization of certain expenses related to the transaction, and certain non-recurring costs, and net of certain start up expenses. -

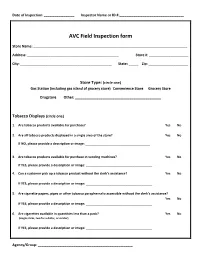

AVC Field Inspection Form

Date of Inspection: _________________ Inspector Name or ID #:____________________________________ AVC Field Inspection form Store Name: ______________________________________________________________________________________ Address: ___________________________________________________ Store #: ______________________ City: ___________________________________________________ State: _____ Zip: ______________________ Store Type: (circle one) Gas Station (including gas island of grocery store) Convenience Store Grocery Store Drugstore Other: ____________________________________________ Tobacco Displays (circle one) 1. Are tobacco products available for purchase? Yes No 2. Are all tobacco products displayed in a single area of the store? Yes No If NO, please provide a description or image: ____________________________________ 3. Are tobacco products available for purchase in vending machines? Yes No If YES, please provide a description or image: _____________________________________ 4. Can a customer pick up a tobacco product without the clerk’s assistance? Yes No If YES, please provide a description or image: _____________________________________ 5. Are cigarette papers, pipes or other tobacco paraphernalia accessible without the clerk’s assistance? Yes No If YES, please provide a description or image: _____________________________________ 6. Are cigarettes available in quantities less than a pack? Yes No (single sticks, two for a dollar, or similar) If YES, please provide a description or image: _____________________________________ Agency/Group: -

Leading by Example Stefano Pessina Won the 2013 Clarity Search Retail Leader of the Year Award

Sponsored by THE CLARITY SEARCH RETAIL LEADER OF THE YEAR Leading by example Stefano Pessina won the 2013 Clarity Search Retail Leader of the Year award. Tiffany Holland talks to the Alliance Boots executive chairman to find out why he’s ahead of the pack n first meeting, it’s easy Last year the self-made billionaire to guess that Stefano revealed that Alliance Boots would Pessina is an entrepre- be partnering with US drugstore Oneur. He wears the sort of chain Walgreens, which will even- sharp suits you’d expect of a billion- tually lead to a full merger. aire and his confident, composed It was one of the most remarkable air could calm any boardroom. business moves in years, as Alliance As the boss of Alliance Boots, Boots, which earned a trading profit one of the largest retailers in the UK of £1.2bn in the last financial year, and one of the biggest pharmaceuti- joined forces with Walgreens’ cal wholesalers in the world, he is empire of 8,000 stores. known for his serene demeanour – The US retailer generated an oper- something that was undoubtedly ating income of $3.5bn (£2.3bn) in useful last June when he brokered the same financial year. In June it the landmark retail deal of 2012. was revealed that Walgreens would But when Retail Week speaks to initially invest $6.7bn (£4.5bn) in him, the Italian businessman is in cash and stocks to acquire 45% high spirits, cracking jokes and equity in Alliance Boots, with a revelling in the recognition his view to merge within three years. -

NOW ACCEPTING GROCERY COMPETITOR COUPONS and ALL MANUFACTURER COUPONS ARE NOW WORTH up to $1.00 Competitor Coupons

NOW ACCEPTING GROCERY COMPETITOR COUPONS AND ALL MANUFACTURER COUPONS ARE NOW WORTH UP TO $1.00 Competitor Coupons We will gladly accept grocery competitor coupons from Albertsons, Safeway, Basha’s, Fresh & Easy, Sunflower, Sprouts, Walmart Marketside, Walmart Neighborhood Market, Whole Foods, Target, AJ’s, Trader Joes, Food City and Ranch Market. All limits and restrictions apply. All competitor amount-off total order coupons will be redeemed after all other discounts and coupons have been applied, as long as the requirements of the coupon have been met. Only one competitor amount-off total order coupon from the same competitor may be used per shopping visit. Customers may use more than one Competitor. Example: A Fresh & Easy $5 off with a $50 required purchase plus an Albertsons $10 off with a $100 required purchase, for a total required purchase of $150, after all other discounts and coupons have been applied. • Competitor coupons will be accepted on identical items, no substitutions. • For competitor brand items use our comparable brand item. • Sorry, no rain checks. • We accept Print at Home Competitor coupons. o Competitor coupons printed from the internet may be printed in black & white. All Manufacturer Coupons Are Worth Up To $1.00! During this promotion we will make all paper manufacturer coupons up to $1.00, even those that state “Do Not Double” or “Not Subject to Doubling.” o Digital coupons downloaded onto a shopper’s VIP card are not subject to doubling Limit one manufacturer and one competitor coupon per item. Coupons Under $1: We will make up to three of the same coupon for like items up to $1.00. -

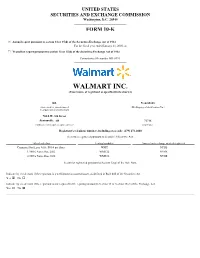

WALMART INC. (Exact Name of Registrant As Specified in Its Charter) ______

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 ___________________________________________ FORM 10-K ___________________________________________ ☒ Annual report pursuant to section 13 or 15(d) of the Securities Exchange Act of 1934 For the fiscal year ended January 31, 2020, or ☐ Transition report pursuant to section 13 or 15(d) of the Securities Exchange Act of 1934 Commission file number 001-6991. ___________________________________________ WALMART INC. (Exact name of registrant as specified in its charter) ___________________________________________ DE 71-0415188 (State or other jurisdiction of (IRS Employer Identification No.) incorporation or organization) 702 S.W. 8th Street Bentonville, AR 72716 (Address of principal executive offices) (Zip Code) Registrant's telephone number, including area code: (479) 273-4000 Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol(s) Name of each exchange on which registered Common Stock, par value $0.10 per share WMT NYSE 1.900% Notes Due 2022 WMT22 NYSE 2.550% Notes Due 2026 WMT26 NYSE Securities registered pursuant to Section 12(g) of the Act: None ___________________________________________ Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No ¨ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No ý WorldReginfo - ddf1e3e1-b7d7-4a92-84aa-57ea0f7c6df3 Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for at least the past 90 days. -

Houchens Industries Jimmie Gipson 493 2.6E Bowling Green, Ky

SN TOP 75 SN TOP 75 2010 North American Food Retailers A=actual sales; E=estimated sales CORPORATE/ SALES IN $ BILLIONS; RANK COMPANY TOP EXECUTIVE(S) FRancHise STORes DATE FISCAL YEAR ENDS 1 Wal-Mart Stores MIKE DUKE 4,624 262.0E Bentonville, Ark. president, CEO 1/31/10 Volume total represents combined sales of Wal-Mart Supercenters, Wal-Mart discount stores, Sam’s Clubs, Neighborhood Markets and Marketside stores in the U.S. and Canada, which account for approximately 64% of total corporate sales (estimated at $409.4 billion in 2009). Wal-Mart operates 2,746 supercenters in the U.S. and 75 in Canada; 152 Neighborhood Markets and four Marketside stores in the U.S.; 803 discount stores in the U.S. and 239 in Canada; and 605 Sam’s Clubs in the U.S. (The six Sam’s Clubs in Canada closed last year, and 10 more Sam’s are scheduled to close in 2010.) 2 Kroger Co. DAVID B. DILLON 3,634 76.0E Cincinnati chairman, CEO 1/30/10 Kroger’s store base includes 2,469 supermarkets and multi-department stores; 773 convenience stores; and 392 fine jewelry stores. Sales from convenience stores account for approximately 5% of total volume, and sales from fine jewelry stores account for less than 1% of total volume. The company’s 850 supermarket fuel centers are no longer included in the store count. 3 Costco Wholesale Corp. JIM SINEGAL 527 71.4A Issaquah, Wash. president, CEO 8/30/09 Revenues at Costco include sales of $69.9 billion and membership fees of $1.5 billion. -

Feature Advertising by U.S. Supermarkets Meat and Poultry

United States Department of Agriculture Agricultural Feature Advertising by U.S. Supermarkets Marketing Service Meat and Poultry Livestock, Poultry and Seed Program Independence Day 2017 Agricultural Analytics Division Advertised Prices effective through July 04, 2017 Feature Advertising by U.S. Supermarkets During Key Seasonal Marketing Events This report provides a detailed breakdown of supermarket featuring of popular meat and poultry products for the Independence Day marketing period. The Independence Day weekend marks the high watershed of the summer outdoor cooking season and is a significant demand period for a variety of meat cuts for outdoor grilling and entertaining. Advertised sale prices are shown by region, state, and supermarket banner and include brand names, prices, and any special conditions. Contents: Chicken - Regular and value packs of boneless/skinless (b/s) breasts; b/s thighs; split, bone-in breasts; wings; bone-in thighs and drumsticks; tray and bagged leg quarters; IQF breast and tenders; 8-piece fried chicken. Northeast .................................................................................................................................................................. 03 Southeast ................................................................................................................................................................. 21 Midwest ................................................................................................................................................................... -

Battle of the Titans in Phoenix, Arizona

SPECIAL REPORT Wal-Mart Pricing ReportRound XIX Battle Of The Titans In Phoenix, Arizona Wal-Mart’s trifecta — the Supercenter, Neighborhood Market and Marketside — rules the roost in Phoenix. BY JIM PREVOR ome believe that the future of American retailing well represented in the marketplace with its Fry’s division. can be glimpsed in Phoenix, AZ. Between its large Tesco, the behemoth from across the sea, also used Phoenix as senior citizen population and large Hispanic popula- a launching grounds for its Fresh & Easy small store concept. tion, one can argue that this is what retailing in In addition to these national chain concepts, we included in America will look like in not all that many years. our comparison a strong independent: Basha’s Supermarkets. SSo we traveled down to Phoenix for the 19th iteration of our What can we surmise from the outcome of our produce pric- Wal-Mart Pricing Study, seeking not just our usual quest — the ing competition among this array of retailers in Phoenix? low price champion in one city — but also seeking enlighten- Many things to be sure, but as a first order, this: If Phoenix ment as to what the future might bring for retailing all across is the future of American retailing, and if price for a cus- the country. tomer walking in off the street is the key variable, then One thing is certain: Phoenix is, in fact, a place where a bat- the future belongs to Wal-Mart. tle of the Titans is playing out. It is the only market in America Not only was the Wal-Mart Supercenter the low price leader where one has a representation of three separate Wal-Mart con- in Phoenix, but the Wal-Mart Neighborhood Market concept cepts — the Wal-Mart Supercenter, the Wal-Mart Neighborhood came in number two, and Wal-Mart’s Marketside concept came Market and the new, small-store Wal-Mart concept known as in third! A trifecta! It hardly seems possible. -

OCT 1 6 2014 DOROTHY BROWN VERIFIED COMPLAINT CLERK of CIRCUIT Court' Plaintiff Wade D

IN THE CIRCUIT COURT OF COOK COUNTY, ILLINOIS COUNTY DEPARTMENT, CHANCERY DIVISION -------------------------------------------------------------- )( WADE D. MIQUELON, ·· Plaintiff, v. JURY TRIAL DEMANDED WALGREEN CO., Defendant. F1LED -------------------------------------------------------------- )( OCT 1 6 2014 DOROTHY BROWN VERIFIED COMPLAINT CLERK OF CIRCUIT COURt' Plaintiff Wade D. Miquelon ("Miquelon"), through his undersigned counsel, complains against defendant Walgreen Co. ("Walgreens" or the "Company") and alleges as follows: INTRODUCTION 1. This past August 4, Miquelon stepped down as the Chief Financial Officer ("CFO") and President, International of Walgreens, the largest drugstore chain in the United States. The decision was personal, based on his desire to pursue opportunities outside of Walgreens after an outstanding six-year tenure. In announcing Miquelon's decision, the Company issued a press release that hailed Miquelon's "remarkable leadership, strategic vision and expertise." These words faithfully captured the Company's internal assessment ofMiquelon: Only last April, Miquelon was offered a promotion by Walgreens' Chief Executive Officer ("CEO") Gregory Wasson ("Wasson") and was told both verbally and in writing that, ifhe accepted the offer, he would be in line to succeed Wasson as CEO. 2. Over the new few days, from August 5 through August 8, Wasson and Walgreens' Director and largest shareholder Stefano Pessina ("Pessina") met with certain investors, 15401055 including "activist" investors, to discuss the past -

PURDUE PHARMACIST Volume 92, Issue 1 (Summer 2016)

THE PURDUE PHARMACISTSummer 2016 Volume 92, Issue 1 FROM THE DEAN THE PURDUE PHARMACIST Volume 92, Issue 1 (Summer 2016) ADMINISTRATION Craig K. Svensson Dean, College of Pharmacy Eric L. Barker The late renowned author Professor Stephen Covey is attributed as the Associate Dean for Research originator of the saying, “The main thing is to keep the main thing the main Tonglei Li thing.” Any leader of an organization needs to make sure they understand Associate Dean for Graduate Programs what is the “main thing” and keep their focus on this priority. While obviously Holly L. Mason open to debate, I would argue that the “main thing” for any organization is its Senior Associate Dean people. It is our people who define, embody, and accomplish our mission. Brian M. Shepler No organization will surpass the quality of its people. It is our students, faculty, Assistant Dean for Experiential Education staff, and alumni who make your College of Pharmacy a program of excellence. They are what makes us who we are and are the engine that drives our mission. DEPARTMENT HEADS It should be no surprise, therefore, that as you read these pages of The Purdue Elizabeth M. Topp Industrial and Physical Pharmacy Pharmacist you will find that it is filled with stories of people. Among those are alumni we have recently recognized for their outstanding accomplishments Zhong-Yin Zhang Head, Medicinal Chemistry as pharmacists and pharmaceutical scientists. Their individual and collective and Molecular Pharmacology achievements serve as a great source of encouragement to our students and Alan J. Zillich help them to see the possibilities for their own careers.