Tampa's New Housing Wave

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

![Greenways Trails [EL08] 20110406 Copy.Eps](https://docslib.b-cdn.net/cover/8169/greenways-trails-el08-20110406-copy-eps-718169.webp)

Greenways Trails [EL08] 20110406 Copy.Eps

R 17 E R 18 E R 19 E R 20 E R 21 E R 22 E MULTI-USE, PAVED TRAILS Suncoast NAME MILES Air Cargo Road 1.4 G HILLSBOROUGH Al Lopez Park 3.3 BrookerBrooker CreekCreek un n CorridorCorridor Suncoast H Aldermans Ford Park 1.9 w y Trail Amberly Drive 2.8 l B LakeLake DanDan 39 Bayshore Boulevard Greenways 4.4 EquestrianEquestrian TrailTrail Lake s GREENWAYS SYSTEM F z e n Lut rn R P d w OakridgeOakridge Brandon Parkway 1.4 o EquestrianEquestrian TrailTrail HillsboroughHillsborough RRiveriver LLUTZUTZ LAKEAKE FERNF D Bruce B Downs Boulevard 4.8 BrookerBrooker CCreekreek ERN RDRD StateState ParkPark B HeadwatersHeadwaters 75 NNewew TTampaampa Y e Cheney Park 0.3 TrailTrail c A LutzLutz W u Commerce Park Boulevard 1.4 KeystoneKeystone K Tam r BlackwaterBlackwater Bruce B Downs Bl Downs B Bruce R ew pa B A N N Bl FloridaFlorida TrailTrail PPARKWAY L reek CreekCreek PreservePreserve Compton Drive 1.4 C D TrailTrail Bl E E ss Copeland Park 2.3 D K CypressCypress TATAR RRD N SUNSETSUNSET LNLN Cro O R Y P H ON GS T N A I I I O R V CreekCreek SP D G Cross County Greenway 0.8 S 275 G A R H W R H WAYNE RD A YS L R L C T 41 579 C CROOKED LN DairyDairy A O A A Cypress Point Park 1.0 N N L N KeystoneKeystone C P O D E D N LAK R FarmFarm C H D H T r Davis Island Park 0.5 U r O O R U Lake U S D SSUNCOAS 568 D A A Bo N G y S Desotto Park 0.3 co W Keystone T K u P N R I m D L E D BrookerBrooker CreekCreek t Rd 589 l RS EN R V d E VVanan DDykeyke RdRd a GRE DeadDead E Shell Point Road 1.2 Y I NNewew TampaTampa R ConeCone RanchRanch VVanan DDykeyke RRdd AV L LIVINGSTON -

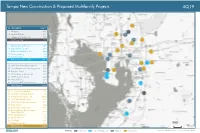

Tampa New Construction & Proposed Multifamily Projects

Tampa New Construction & Proposed Multifamily Projects 4Q19 ID PROPERTY UNITS 1 Wildgrass 321 3 Union on Fletcher 217 5 Harbour at Westshore, The 192 Total Lease Up 730 15 Bowery Bayside Phase II 589 16 Tapestry Town Center 287 17 Pointe on Westshore, The 444 28 Victory Landing 69 29 Belmont Glen 75 Total Under Construction 1,464 36 Westshore Plaza Redevelopment 500 37 Leisey Road Mixed Used Development 380 38 Progress Village 291 39 Grand Cypress Apartments 324 43 MetWest International 424 44 Waverly Terrace 214 45 University Mall Redevelopment 100 Total Planned 2,233 69 3011 West Gandy Blvd 80 74 Westshore Crossing Phase II 72 76 Village at Crosstown, The 3,000 83 3015 North Rocky Point 180 84 6370 North Nebraska Avenue 114 85 Kirby Street 100 86 Bowels Road Mixed-Use 101 87 Bruce B Downs Blvd & Tampa Palms Blvd West 252 88 Brandon Preserve 200 89 Lemon Avenue 88 90 City Edge 120 117 NoHo Residential 218 Total Prospective 4,525 2 mi Source: Yardi Matrix LEGEND Lease-Up Under Construction Planned Prospective Tampa New Construction & Proposed Multifamily Projects 4Q19 ID PROPERTY UNITS 4 Central on Orange Lake, The 85 6 Main Street Landing 80 13 Sawgrass Creek Phase II 143 Total Lease Up 308 20 Meres Crossing 236 21 Haven at Hunter's Lake, The 241 Total Under Construction 477 54 Bexley North - Parcel 5 Phase 1 208 55 Cypress Town Center 230 56 Enclave at Wesley Chapel 142 57 Trinity Pines Preserve Townhomes 60 58 Spring Center 750 Total Planned 1,390 108 Arbours at Saddle Oaks 264 109 Lexington Oaks Plaza 200 110 Trillium Blvd 160 111 -

Transforming Tampa's Tomorrow

TRANSFORMING TAMPA’S TOMORROW Blueprint for Tampa’s Future Recommended Operating and Capital Budget Part 2 Fiscal Year 2020 October 1, 2019 through September 30, 2020 Recommended Operating and Capital Budget TRANSFORMING TAMPA’S TOMORROW Blueprint for Tampa’s Future Fiscal Year 2020 October 1, 2019 through September 30, 2020 Jane Castor, Mayor Sonya C. Little, Chief Financial Officer Michael D. Perry, Budget Officer ii Table of Contents Part 2 - FY2020 Recommended Operating and Capital Budget FY2020 – FY2024 Capital Improvement Overview . 1 FY2020–FY2024 Capital Improvement Overview . 2 Council District 4 Map . 14 Council District 5 Map . 17 Council District 6 Map . 20 Council District 7 Map . 23 Capital Improvement Program Summaries . 25 Capital Improvement Projects Funded Projects Summary . 26 Capital Improvement Projects Funding Source Summary . 31 Community Investment Tax FY2020-FY2024 . 32 Operational Impacts of Capital Improvement Projects . 33 Capital Improvements Section (CIS) Schedule . 38 Capital Project Detail . 47 Convention Center . 47 Facility Management . 49 Fire Rescue . 70 Golf Courses . 74 Non-Departmental . 78 Parking . 81 Parks and Recreation . 95 Solid Waste . 122 Technology & Innovation . 132 Tampa Police Department . 138 Transportation . 140 Stormwater . 216 Wastewater . 280 Water . 354 Debt . 409 Overview . 410 Summary of City-issued Debt . 410 Primary Types of Debt . 410 Bond Covenants . 411 Continuing Disclosure . 411 Total Principal Debt Composition of City Issued Debt . 412 Principal Outstanding Debt (Governmental & Enterprise) . 413 Rating Agency Analysis . 414 Principal Debt Composition . 416 Governmental Bonds . 416 Governmental Loans . 418 Enterprise Bonds . 419 Enterprise State Revolving Loans . 420 FY2020 Debt Service Schedule . 421 Governmental Debt Service . 421 Enterprise Debt Service . 422 Index . -

Unlocking Tampa Bay – Treasure Awaits

Media Contact: Kelly Prieto, APR Hayworth Public Relations (813) 318-9611 [email protected] Culinary Related media inquiries: Brooke Palmer Bern’s Steak House (727) 235-2389 Year 2017 [email protected] Unlocking Tampa Bay – Treasure Awaits TAMPA – The Epicurean Hotel rises from the heart of the vibrant city of Tampa, Fla., bringing a new level of contemporary comfort and style to the Hyde Park historic district. From the thrill of major league sports to the authentic charm of Tampa’s unique history, the Epicurean is the gateway to exploring one of Florida’s most beloved destinations. With distinctive vibes and cultures emanating from each of the city’s districts, Tampa always surprises visitors with something new to explore and experience. While staying at the Epicurean, guests can expect anything but a generic hotel experience. The hotel’s well-connected Epicurean Hosts give adventurous guests an inside track for finding the area’s genuine and enriching local experiences. From “locals-only” restaurants and hidden shopping gems, to the best bike routes and museum exhibitions, a chat with the Epicurean Hosts will leave guests feeling as if they own the city. Guests don’t have to travel far from the hotel to experience more of Tampa’s premier dining, nightlife and shopping. Directly across the street, the legendary Bern’s Steak House is a destination all its own, where diners can tour the kitchen and wine cellar and pay a visit to the famous Harry Waugh Dessert Room. Bern’s sister restaurant, Haven, thrills foodies with whimsical small plates, housemade charcuterie, cultured artisanal cheeses, crafted cocktails and cellared wine selections. -

Sulphur Springs Stability Study Final Report 2017

Sulphur Springs Stability Study Final Report 2017 ANNUAL REPORT Department of Child & Family Studies College of Behavior & Community Sciences University of South Florida Tampa, Florida Copyright 2017 http://www.usf.edu/cbcs/cfs Acknowledgements We would like to thank the Sulphur Springs Leadership Council Key Partner And also we give thanks to SSNOP Research Advisory Committee Sheff Crowder, José Garcia, Chair SSNOP Leadership Council Executive Director, Rebuilding Together Tampa Bay Jacqueline Coffie Leeks, Curt L. McKay, SSNOP Executive Director Resident Engagement Director, Abundant Life Church Lettrice Blackman, Jeremy Twachtman, Community Facilitator, Devereux Kids Volunteer Coordinator, Rebuilding Together Tampa Bay Community Research Partners Linda Callejas - Lead Researcher Rene Anderson Amy Green Deb Mowery Angela Vatalaro Police Records Section, Tampa Police Department Suggested citation: Callejas, L., Mowery, D., and Vatalaro, A. (2017) Sulphur Springs stability study: Final report 2017. Tampa, FL: University of South Florida, Department of Child and Family Studies. 1 Sulphur Springs Stability Study Table of Contents Executive Summary ..................................................................................................................................4 Introduction ...................................................................................................................................................5 Sulphur Springs Stability Study .........................................................................................................6 -

Tampa Heights Historic District

'-~=------. i;f/~-: NPS Form 10-900 (Oct. 1990) ~-ECEIVE(?"IJ~''::'1 '• l UnlJedUnijted State,States D~rtmttntDea)artinent .of thethe.. lnJe(lorInferior . -, / ! National Park Seiylcfl , , National Park Secyicd , JJ. National Register of Historic Places _____6- __. ~ . National Register of Historic Places Registration Form INTERAGENCY RESOURCE;. :f This form is for use in nominating or requesting determinations for individualindividuai properties and tthliiiili■· ’ISSSE*' faaJnattuctionsNA~IONA~,fs~~~~te m"ftd>ftrBv66»tefe t~the I; National Register of Historic Places Registration Form (National Register Bulletin 16A). Complete each item by mariiidikliiy ing X lli<th»«pp(aB(iatgJox· x or by entering the information requested. If an item does not apply to the property bebeinging documented, enter "NIA"“N/A” for "not“not applicable."applicable.” For functions, architectural classification, materials, and areas of significance, enter only categories and subcategories from the instructions. Place additional entries and narrative items on continuation sheets (NPS Form 10-900a). Use a typewriter,typewriter, word processorprocessor,, or computer, to complete all items. 1. Name of Property .. , historic name __Tanpa='-'-"--C..C........CHei.~'-·Tampa Heightsgh.,__ts-'---_Hi_._s_to_r_i_c_D_i_s_tr_i_c_t Historic District____ _ ______________ other names/site number .__-'N'"'--A N/A____________________________ _ 2. Location Bounded by Adal6eAdalee St., I-275,1-275, 7th Ave. street & number and N. TairpaTampa Ave._____________________ N/lt:J not for -

Chicago Downtown Chicago Connections

Stone Scott Regional Transportation 1 2 3 4 5Sheridan 6 7 8 9 10 11 12 13 14 Dr 270 ter ss C en 619 421 Edens Plaza 213 Division Division ne 272 Lake Authority i ood s 422 Sk 422 u D 423 LaSalle B w 423 Clark/Division e Forest y okie Rd Central 151 a WILMETTE ville s amie 422 The Regional Transportation Authority r P GLENVIEW 800W 600W 200W nonstop between Michigan/Delaware 620 421 0 E/W eehan Preserve Wilmette C Union Pacific/North Line 3rd 143 l Forest Baha’i Temple F e La Elm ollw Green Bay a D vice 4th v Green Glenview Glenview to Waukegan, Kenosha and Stockton/Arlington (2500N) T i lo 210 626 Evanston Elm n (RTA) provides financial oversight, Preserve bard Linden nonstop between Michigan/Delaware e Dewes b 421 146 s Wilmette 221 Dear Milw Foster and Lake Shore/Belmont (3200N) funding, and regional transit planning R Glenview Rd 94 Hi 422 221 i i-State 270 Cedar nonstop between Delaware/Michigan Rand v r Emerson Chicago Downtown Central auk T 70 e Oakton National- Ryan Field & Welsh-Ryan Arena Map Legend Hill 147 r Cook Co 213 and Marine/Foster (5200N) for the three public transit operations Comm ee Louis Univ okie Central Courts k Central 213 93 Maple College 201 Sheridan nonstop between Delaware/Michigan Holy 422 S 148 Old Orchard Gross 206 C Northwestern Univ Hobbie and Marine/Irving Park (4000N) Dee Family yman 270 Point Central St/ CTA Trains Hooker Wendell 22 70 36 Bellevue L in Northeastern Illinois: The Chicago olf Cr Chicago A Harrison 54A 201 Evanston 206 A 8 A W Sheridan Medical 272 egan osby Maple th Central Ser 423 201 k Illinois Center 412 GOLF Westfield Noyes Blue Line Haines Transit Authority (CTA), Metra and Antioch Golf Glen Holocaust 37 208 au 234 D Golf Old Orchard Benson Between O’Hare Airport, Downtown Newberry Oak W Museum Nor to Golf Golf Golf Simpson EVANSTON Oak Research Sherman & Forest Park Oak Pace Suburban bus. -

Hillsborough County Water Atlas

Hillsborough County C OUNTY SEAT: Tampa \, P OPULATION : 355,500 } 11>"" ! ~ I • 'III> • I NCOIIPOIIAT ED CITIES: Plant '""'~''' ~~ I City, ,-~" + MULL~ r- ~Yl7l -, - .- -- Port Tampa City, Tampa, IDC. ./ K ~yD- · Temple Terrace. ' EGMONT ,/ '0lIl".",1Clt..,r ", ,*,'" ILLSBOROUGH COUNTY is situated eggplant, tomatoes, beans, squash, potatoes, H on the western coast of Florida near cabbage, cucumbers, spinach, and water the center of the State's length. Its 679,680 melons. Native grass hays are grown in con acres are bordered by Pasco, Pinellas, Polk, siderable quantity. In 1954 th ere were 4,492 and Manatee counties; Tampa Bay and Hills farms in the county comprising 863,243 borou gh Bay form a deep indentation in its acres. Winter truck crops are a specialty of shoreline, giving the county an extended the county. Plant City is considered the "win water frontage.Tampa , the county seat an d ter strawberry capital of the world:' pro principal city, is 20 miles from St. Peters ducing an average of 20,000,000 pints of burg, 33 miles from Lakeland, 97 miles from strawberries per season. Ruskin is noted as Orlando, and 98 miles from Ocala. the center of tomato production. One of the largest mechanized farms in the coun try is Annual average temp erature is 72.42 de located here. In 1955-56 there were 19,850 grees; average high 81.5 degrees in August, acres planted to vegetables and small fruits. average low 60.4 degrees in January. Aver Th e State Farmers' Market in Plant City is age annual rainfall is 48.48 inches, the heavi the largest market of its kind in the nation; est in June, July, August, and September. -

Tampa New Construction & Proposed Multifamily Projects 3Q20

Tampa New Construction & Proposed Multifamily Projects 3Q20 138 ID PROPERTY UNITS 65 142 4 Thrive by Watermark 328 64 143 5 Springs at Posner Park 288 4 137 11 The Lakeland Grand 268 5 12 Serenity at Lake Wales 335 139 140 Total Lease Up 1,219 141 24 Mirrorton 305 144 47 Twin Lakes Estates Phase II 132 Total Under Construction 437 105 58 Westwood at Winter Haven 280 64 The Addison Lake Wilson 309 65 Reunion Village 280 Total Planned 869 75 Parc at Lake Wales Phase II 240 98 97 4th Street & Kathleen 264 97 98 Griffin Lofts 60 100 99 Hawthorne Mills 180 24 104 100 Jersey Road Workforce Housing 304 47 101 Lakeland Logistics Park 300 101 58 102 Lakeside Village 240 106 109 103 One College Place 310 102 103 104 Twin Lakes Estates Phase III 86 108 107 105 Williams DRI 1,700 99 75 106 14th Street SW & Lake Howard 190 11 136 107 Cypress Landings 210 12 108 Parc at Lake Wales 240 109 RainDance 105 135 Palms at Kyle Terrace 87 136 The Preserve at Lake Ashton 512 141 Reserves at Citrus Ridge 250 137 Crystal Bay 365 142 Retreat at Lake Wilson 360 135 138 Jacks Road & US Route 27 426 143 Retreat at Lake Wilson Phase II 350 139 Posner Village Eastwind 163 144 The Tuttle 432 140 Posner Village in Four Corners 315 Total Prospective 7,689 2 mi Source: Yardi Matrix LEGEND Lease-Up Under Construction Planned Prospective Tampa New Construction & Proposed Multifamily Projects 3Q20 ID PROPERTY UNITS 1 Gables at Gulf View 312 2 The Beck 204 159 7 The Addison at Sunlake 307 158 160 9 Altis Grand at The Preserve 350 14 Icaria on Pinellas 236 Total Lease Up 1,409 -

City of Tampa Tree Canopy and Urban Forest Analysis 2016

City of Tampa Tree Canopy and Urban Forest Analysis 2016 City of Tampa Tree Canopy and Urban Forest Analysis 2016 Final Report to the City of Tampa March 2018 Authors Dr. Shawn M. Landry, University of South Florida Dr. Andrew K. Koeser, University of Florida Robert J. Northrop, UF/IFAS Extension, Hillsborough County Drew McLean, University of Florida Dr. Geoffrey Donovan, U.S. Forest Service Dr. Michael G. Andreu, University of Florida Deborah Hilbert, University of Florida Project Contributors Jan Allyn, University of South Florida Kathy Beck, City of Tampa Catherine Coyle, City of Tampa Rich Hammond, University of South Florida Eric Muecke, City of Tampa Jarlath O’Neil-Dunne, University of Vermont Dr. Ruiliang Pu, University of South Florida Cody Winter, University of South Florida Quiyan Yu, University of South Florida Special Thanks Fredrick Hartless, Hillsborough County Landowners and residents of the City of Tampa City of Tampa Urban Forest Management Internal Technical Working Group City of Tampa Natural Resources Advisory Committee Citation for this report: Landry S., Koeser, A., Northrop, R., McLean, D., Donovan, G., Andreu, M. & Hilbert, D. (2018). City of Tampa Tree Canopy and Urban Forest Analysis 2016. Tampa, FL: City of Tampa, Florida. Contents Executive Summary �������������������������������������������������������������������������������������� 9 The Benefits of Trees ................................................................................. 14 Project Methods Study Area ��������������������������������������������������������������������������������������������������������������17 -

South Tampa Neighborhoods

SOUTH TAMPA: South Tampa is a 4 mile x 8 mile peninsula that protrudes into the Tampa Bay / Hillsborough Bay. South Tampa is home to MacDill Air Force Base, which is encompasses the entire southern point of the peninsula. There’s a diversity of neighborhoods, ranging from mansions to historic homes to smaller, modest homes. Western side of the peninsula has hundreds of waterfront homes with direct access to the Tampa Bay. Each neighborhood is unique with homogeneous appeal and construction quality. Due to the desirability of South Tampa, and lack of vacant, buildable land, homes of less quality are being razed to make room for new, larger homes with significant appeal. This trend is obvious while driving the streets of south Tampa by both the mixture of new and old, and ongoing construction. Bayshore Boulevard overlooks the Hillsborough Bay, and sports the longest sidewalk in the world. Bayshore Boulevard is home to Tampa Bay’s largest and most popular festival, the Gasparilla Parade. This tradition started in 1904 as the mythical Jose Gaspar, a pirate, had a buried treasure in Tampa. Jose Gaspar and his krewe of 900, Ye Mystic Krewe of Gasparilla, invades the city by pirate ship every February, bringing nearly ½ million spectators to the invasion. SOUTH TAMPA NEIGHBORHOODS: BALLAST POINT Gandy Boulevard to the north; MacDill Air Force Base to the south; Hillsborough Bay to the east; MacDill Avenue to the west Driving through Ballast Point, you will see a wide variety of housing types, ranging from modest ranches to large estate homes. 1940’s vintage homes are average quality ranch design. -

National Register Off Historic Places Inventory—Nomination Form 1

NPS Form 10-900 OHB Ho. 1024-0018 Expires 10-31-87 United States Department of the Interior National Park Service For NPS UM only National Register off Historic Places received M- ^ 1 1987 Inventory—Nomination Form date entered See instructions in How to Complete National Register Forms Type all entries—complete applicable sections_______________ 1. Name historic William E. Curtis House and or common John F. Durack House 2. Location street & number 808 East Curtis Street not for publication city, town Tampa vicinity of state Florida code 012 county Hillsborough code 057 3. Classification \ Category Ownership Status Present Use district public X occupied __ agriculture __ museum _JL_ building(s) JL_ private unoccupied commercial __ park structure both work in progress educational X private residence site Public Acquisition Accessible entertainment religious __ object N/A in process __ yes: restricted __ government __ scientific N /A being considered .. yes: unrestricted industrial transportation JL_no __ military __ other: 4. Owner off Property name John F. Durack street & number 808 East Curtis Street city, town Tampa vicinity of state Florida 5. Location off Legal Description courthouse, registry of deeds, etc. Hillsborough County Courthouse street & number 419 Pierce Street Florida city, town Tampa state The Man-made Environment in Tampa title and Hillsborough County has this property been determined eligible? __ yes X no date 1979 (Revised 1983) federal state x county local depository for survey records Florida Master Site File, Bureau