Breakfast with Dave

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

(US PROGRAMMING) - JAN, 2019 (1/7/2019 - 1/13/2019) Date Updated:12/13/2018 6:40:14 PM

MONTHLY GRID (US PROGRAMMING) - JAN, 2019 (1/7/2019 - 1/13/2019) Date Updated:12/13/2018 6:40:14 PM MON (1/7/2019) TUE (1/8/2019) WED (1/9/2019) THU (1/10/2019) FRI (1/11/2019) SAT (1/12/2019) SUN (1/13/2019) 05:00A 05:00 AM WORLDWIDE EXCHANGE 05:00 AM WORLDWIDE EXCHANGE 05:00 AM WORLDWIDE EXCHANGE 05:00 AM WORLDWIDE EXCHANGE 05:00 AM WORLDWIDE EXCHANGE 05:00 AM AMERICAN GREED 43B - 05:00 AM THE PROFIT: HIGH 05:00A THE BLING RING CNAMG043B0KH STAKES (PRIME TIME BUG) 05:30A 05:30 AM ON THE MONEY 05:30A CNOTM01129H 06:00A 06:00 AM SQUAWK BOX 06:00 AM SQUAWK BOX 06:00 AM SQUAWK BOX 06:00 AM SQUAWK BOX 06:00 AM SQUAWK BOX 06:00 AM OPTIONS ACTION (2 LINE 06:00 AM OPTIONS ACTION (2 LINE 06:00A TICKER/NO BUGSTACK) TICKER/NO BUGSTACK) 06:30A 06:30 AM PAID PROGRAMMING 06:30 AM PAID PROGRAMMING 06:30A 07:00A 07:00 AM PAID PROGRAMMING 07:00 AM PAID PROGRAMMING 07:00A 07:30A 07:30 AM PAID PROGRAMMING 07:30 AM PAID PROGRAMMING 07:30A 08:00A 08:00 AM PAID PROGRAMMING 08:00 AM PAID PROGRAMMING 08:00A 08:30A 08:30 AM PAID PROGRAMMING 08:30 AM PAID PROGRAMMING 08:30A 09:00A 09:00 AM SQUAWK ON THE STREET 09:00 AM SQUAWK ON THE STREET 09:00 AM SQUAWK ON THE STREET 09:00 AM SQUAWK ON THE STREET 09:00 AM SQUAWK ON THE STREET 09:00 AM PAID PROGRAMMING 09:00 AM PAID PROGRAMMING 09:00A 09:30A 09:30 AM PAID PROGRAMMING 09:30 AM PAID PROGRAMMING 09:30A 10:00A 10:00 AM PAID PROGRAMMING 10:00 AM PAID PROGRAMMING 10:00A 10:30A 10:30 AM PAID PROGRAMMING 10:30 AM PAID PROGRAMMING 10:30A 11:00A 11:00 AM SQUAWK ALLEY (2 LINE 11:00 AM SQUAWK ALLEY (2 LINE 11:00 AM SQUAWK -

Sunday Morning Grid 8/22/21 Latimes.Com/Tv Times

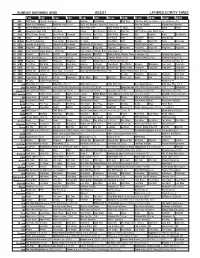

SUNDAY MORNING GRID 8/22/21 LATIMES.COM/TV TIMES 7 am 7:30 8 am 8:30 9 am 9:30 10 am 10:30 11 am 11:30 12 pm 12:30 2 CBS CBS News Face the Nation (N) News Graham Bull Riding PGA Tour PGA Tour Golf The Northern Trust, Final Round. (N) 4 NBC Today in LA Weekend Meet the Press (N) Å 2021 AIG Women’s Open Final Round. (N) Race and Sports Mecum Auto Auctions 5 CW KTLA 5 Morning News at 7 (N) Å KTLA News at 9 KTLA 5 News at 10am In Touch David Smile 7 ABC Eyewitness News 7AM This Week Ocean Sea Rescue Hearts of Free Ent. 2021 Little League World Series 9 KCAL KCAL 9 News Sunday Joel Osteen Jeremiah Joel Osteen Paid Prog. Mike Webb Harvest AAA Danette Icons The World’s 1 1 FOX Mercy Jack Hibbs Fox News Sunday The Issue News Sex Abuse PiYo Accident? Home Drag Racing 1 3 MyNet Bel Air Presbyterian Fred Jordan Freethought In Touch Jack Hibbs AAA NeuroQ Grow Hair News The Issue 1 8 KSCI Fashion for Real Life MacKenzie-Childs Home MacKenzie-Childs Home Quantum Vacuum Å COVID Delta Safety: Isomers Skincare Å 2 2 KWHY Programa Resultados Revitaliza Programa Programa Programa Programa Programa Programa Programa Programa Programa 2 4 KVCR Great Scenic Railway Journeys: 150 Years Suze Orman’s Ultimate Retirement Guide (TVG) Great Performances (TVG) Å 2 8 KCET Darwin’s Cat in the SciGirls Odd Squad Cyberchase Biz Kid$ Build a Better Memory Through Science (TVG) Country Pop Legends 3 0 ION NCIS: New Orleans Å NCIS: New Orleans Å Criminal Minds (TV14) Criminal Minds (TV14) Criminal Minds (TV14) Criminal Minds (TV14) 3 4 KMEX Programa MagBlue Programa Programa Fútbol Fútbol Mexicano Primera División (N) República deportiva (N) 4 0 KTBN R. -

Sunday Morning Grid 12/4/11 Latimes.Com/Tv Times

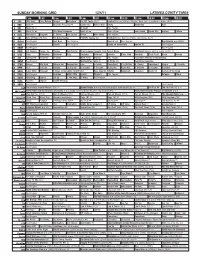

SUNDAY MORNING GRID 12/4/11 LATIMES.COM/TV TIMES 7 am 7:30 8 am 8:30 9 am 9:30 10 am 10:30 11 am 11:30 12 pm 12:30 2 CBS CBS News Face/Nation Danger Horseland The NFL Today (N) Å Football Raiders at Miami Dolphins. From Sun Life Stadium in Miami. (N) Å 4 NBC News Å Meet the Press (N) Å Conference Willa’s Wild Skiing Swimming Golf 5 CW News (N) Å In Touch Paid Program 7 ABC News (N) Å This Week-Amanpour News (N) Å News (N) Å Jack Hanna Ocean Mys. Explore Culture 9 KCAL Tomorrow’s Kingdom K. Shook Joel Osteen Prince Mike Webb Paid Program 11 FOX Hour of Power (N) (TVG) Fox News Sunday FOX NFL Sunday (N) Football Denver Broncos at Minnesota Vikings. (N) Å 13 MyNet Paid Program Best Buys Paid Program Best of L.A. Paid Program Bee Season ›› (2005) 18 KSCI Paid Program Church Paid Program Hecho en Guatemala Iranian TV Paid Program 22 KWHY Paid Program Paid Program 24 KVCR Sid Science Curios -ity Thomas Bob Builder Classic Gospel Special: Tent Revival Home Prohibition Groups push to outlaw alcohol. Å 28 KCET Cons. Wubbulous Busytown Peep Pancakes Pufnstuf Lidsville Place, Own Roadtrip Chefs Field Pépin Venetia 30 ION Turning Pnt. Discovery In Touch Mark Jeske Beyond Paid Program Inspiration Ministry Campmeeting 34 KMEX Paid Program Muchachitas Como Tu Al Punto (N) República Deportiva 40 KTBN Rhema Win Walk Miracle-You Redemption Love In Touch PowerPoint It Is Written B. Conley From Heart King Is J. -

Lisa Oake Freelance News Anchor Independent Media Consultant

Dec 19 Lisa Oake Freelance News Anchor Independent Media Consultant Moderator and Chairperson Professional Experience • Based in Singapore, Lisa is a former CNBC News Anchor with over 16 years broadcasting and hosting a range of financial markets and business programmes including Squawk Box, Worldwide Exchange and other CNBC programmes. • She is CEO & Founder of Oake Media - a boutique coaching firm that specialises in teaching executives and broadcast journalists how to deliver compelling, on-air performances as well as a Crisis Communications consultant who helps companies develop operating procedures for dealing with unexpected scenarios. • Lisa was named Best Media Trainer at the 2017 Asia Training and Development Excellence Awards. She is also a recipient of the Canadian Radio Television News Directors Foundation’s Eric Murray award for investigative journalism and CNBC’s special achievement award for journalistic excellence • Lisa was the first journalist to report live from the trading floor of the Singapore Exchange and to interview the President of Indonesia after the devastation of 2004 tsunami. • Lisa has interviewed numerous CEOs, central bank governors and heads of state including Indonesia’s Susilo Bambang Yudhoyono, Thailand’s Abhisit Vejjajiva, New Zealand’s Helen Clarke and Canada’s Kim Campbell. • Lisa has moderated discussions on everything from the global economy & finance to talent wars & women’s issues. Lisa has a very strong understanding of financial and investment topics but also has the skills, experience and personality to handle discussions across many economic, political, business and management topics. Sample assignments • Lisa has been involved in a number of CNBC events including moderating the Business Leaders’ Awards and other media events. -

Affidavit of Performance

OnMedia Advertising Sales 1037 Front Avenue Suite C Columbus , GA31901 Affidavit of Performance Client Name WARNOCK FOR GEORGIA/GA Contract ID 289621 Remarks 62849605-3646 Contract Type Political Bill Cycle 12/20 Bill Type Condensed EAI Broadcast Standard Date Weekday Network Zone Program Name Air Time Spot Name Spot Contract Billing Spot Length Line Status Cost 12/15/2020 Tuesday AEN_E Columbus-Valley-Auburn The First 48 2:50 AM RWTV2032H I WOULD 00:01:60 1 Charged 2.00 * 12/17/2020 Thursday AEN_E Columbus-Valley-AuburnWOW GA The First 48 5:42 PM RWTV2032H I WOULD 00:01:60 2 Charged 18.00 * 12/16/2020 Wednesday AEN_E Columbus-Valley-AuburnWOW GA Court Cam 11:20 PM RWTV2032H I WOULD 00:01:60 3 Charged 70.00 * 12/15/2020 Tuesday AMC_E Columbus-Valley-AuburnWOW GA Snow Day 1:52 AM RWTV2032H I WOULD 00:01:60 4 Charged 2.00 * 12/20/2020 Sunday AMC_E Columbus-Valley-AuburnWOW GA Fred Claus 4:20 PM RWTV2053H BUS 00:01:60 5 Charged 18.00 * 12/16/2020 Wednesday AMC_E Columbus-Valley-AuburnWOW GA Scrooged 6:23 PM RWTV2032H I WOULD 00:01:60 6 Charged 22.00 * 12/15/2020 Tuesday BET_E Columbus-Valley-AuburnWOW GA Martin 12:15 AM RWTV2032H I WOULD 00:01:60 7 Charged 2.00 * 12/17/2020 Thursday BET_E Columbus-Valley-AuburnWOW GA Deliver Us From Eva 3:45 PM RWTV2032H I WOULD 00:01:60 8 Charged 6.00 * 12/16/2020 Wednesday BET_E Columbus-Valley-AuburnWOW GA Tyler Perry's Sistas 11:38 PM RWTV2032H I WOULD 00:01:60 9 Charged 22.00 * 12/15/2020 Tuesday BRVO_E Columbus-Valley-AuburnWOW GA Monster-in-Law 2:49 AM RWTV2032H I WOULD 00:01:60 10 Charged 2.00 * 12/18/2020 -

Carolin Roth

WORLDWIDE SPEAKERS GROUP LLC YOUR GLOBAL PARTNER IN THOUGHT LEADERSHIP CAROLIN ROTH Carolin Roth has 13 years of experience of Live TV as an international finance and business journalist at CNBC International. Fluent in both German and English, she has been with CNBC since 2007, reporting on air full- time since 2009 and is now a freelance presenter. Carolin has hosted all of CNBC International’s flagship shows, including Worldwide Exchange, European Closing Bell, and co-anchored Squawk Box (Europe) from CNBC's London studios, and contributed to CNBC and MSNBC programming in the US on a regular basis. Covering breaking news and getting instant analysis from top guests is where she feels at home, while she also thoroughly enjoys and excels at in depth discussions on bigger topics, ranging from innovations in technology and how they shape the future to politics and beyond. During her time in London, Carolin also moderated CNBC's “Marketing|Media|Money”, a series that navigates the global advertising industry through the eyes of the senior marketers, as well as CNBC’s “Business Class”, a start-up show focusing on innovative business ideas. She also contributed to the channel’s technology-minded show called “The Edge”. Carolin has covered key events for CNBC including the World Economic Forum, G7 summits, the European financial crisis out of Zurich and Frankfurt, the European debt crisis live out of Greece, Italy, Spain, Hungary, and Cyprus. She has also been at the forefront of political events as a reporter on the ground for several key elections, such as the German, UK, French, Greek and Dutch elections. -

Star Channels, Oct. 18

OCTOBER 18 - 24, 2020 staradvertiser.com SONGS FROM AFAR Country star Blake Shelton, singer-songwriter John Legend, pop star Gwen Stefani and the original “American Idol,” Kelly Clarkson return as judges in the Season 19 premiere of The Voice. Hosted by Carson Daly, NBC has given no hints to this year’s mentors, but you can be sure this season will feature just as many powerhouse musicians as previous seasons. Airing Monday, Oct. 19, on NBC. || ON THE COVER | THE VOICE Not to be silenced NBC brings back ‘The Voice’ up all over social media. The judges returning ing tight to that list and has given no hints for to the show are country star Blake Shelton, whom it plans to bring on. What we do know singer-songwriter John Legend, pop star Gwen is that the network always goes big when it By Rachel Jones Stefani and the original “American Idol,” Kelly comes to getting the stars. Last season fea- TV Media Clarkson. Back for her fifth season in the red tured singers Ella Mai, Dua Lipa, Bebe Rexha, chair, Stefani has been a sporadic judge over the Jonas Brothers and even powerhouse icon eason 19 of “The Voice” is finally set to the past several years. Last seen in Season 17, James Taylor. air Monday, Oct. 19, on NBC. The show she took a two-season break and was replaced As with most television series, reality TV was originally meant to begin in the S with musician and actor Nick Jonas (“Jumanji: spring but was pushed back, like many oth- was severely impacted by the coronavirus Welcome to the Jungle,” 2017). -

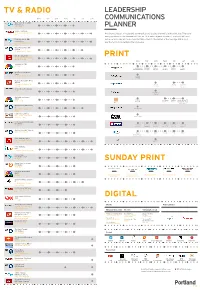

Print Digital Tv & Radio Sunday Print

TV & RADIO LEADERSHIP MON TUE WED THUR FRI SAT SUN COMMUNICATIONS Wake Up to Money, BBC Radio 5 Live 5:15 - 6 am PLANNER Sunrise, Sky News 6 - 9 am; Sat & Sun: 6 - 10 One important part of leadership communications is using the media in the right way. There are am many opportunities to communicate live on TV or radio, in print or online. Each has a different 5 Live Breakfast, BBC audience and some will be more suited than others to the leader or the message. But a good Radio 5 Live 6 - 10 am; Sat & Sun 6 - 9 way to start is to understand the landscape. am Today Programme, BBC Radio 4 6 - 9 am; Sat: 7 - 9 am BBC Breakfast, BBC 1 PRINT 6 - 9:15 am ; Sat: 6 - 10 am, Sun: 6 - 7:40 am MON TUE WED THUR FRI SAT SUN Squawkbox, CNBC 6 - 9 am Monday Manifesto; Business Business Business Business Business Business Big Shot Big Shot Big Shot Big Shot Big Shot Big Shot Nick Ferrari Show, LBC Radio 7 - 10 am; Sat: 5 - 7 am Monday Interview Business Daily, BBC World Service 7:32 am; 14.06 pm & Fri Society Friday Saturday 7.32 am Interview Interview Interview (varies) On the Move, Bloomberg 9 am The Business Interview Worldwide Exchange, CNBC Monday 9 am - 11 pm Recruitment Business Lunch with the FT; Interview Interview Speak Person in the News; My Weekend Woman’s Hour, BBC Radio 4 Mon - Fri: 10 - 11 am; Sat: Monday View 4-5pm Daily Politics, BBC 2 Mon - Fri: 12 - 1 pm; Wed: Growth Capital 11:30 am - 1 pm In The Loop with Betty Liu, Bloomberg 1 - 3pm 60 Second 60 Second 60 Second 60 Second 60 Second 60 Second Interview Interview Interview Interview Interview -

The Organisation and Structure of Central Banks. Dissertation

The Organisation and Structure of Central Banks Dissertation Approved as fulfilling the requirements for the degree of Doctor rerum politicarum (Dr. rer. pol.) at the Department of Law and Economics of Technische Universität Darmstadt by Jan Weidner, M.Sc. (born in Darmstadt) First supervisor: Prof. Dr. Volker Nitsch Second supervisor: Prof. Dr. Michael Neugart Date of submission: April 20, 2017 Date of defense: July 13, 2017 Place of publication: Darmstadt Year of publication: 2017 D17 Acknowledgments At this point, I would like to take a moment to thank those who have supported and guided me over the course of writing this dissertation. First and foremost, I owe my doctoral advisor Prof. Dr. Volker Nitsch a huge debt of gratitude for a number of reasons. Firstly, for agreeing to supervise my thesis and, secondly, for offering me a position at his chair. Above all however, I must thank him for the expertise he has shared with me and the moral support he provided me throughout this process. His knowledge, opinions, and advice have always been of great assistance and value to me. I thank Prof. Dr. Michael Neugart greatly for being my second supervisor and for his guidance and advice on many issues. Additionally, my great experience of a Winter School in Shanghai is thanks to him and I will remember this always. Finally, it would be remiss of me not to thank him for the happy hours spent on the football pitch. I wish to express my gratitude to the chairman of my examination committee, Prof. Dr. Jens Krüger, and to the other members of the committee, Prof. -

National TV Advertising Schedule September 2014 - August 2015

National TV Advertising Schedule September 2014 - August 2015 9/8-9/14 2/2-2/8 5/18-5/24 FOX News CNBC CNBC Fox & Friends, Fox News Live, Your World Worldwide Exchange, Squawk Box, Worldwide Exchange, Squawk Box, w/Neil Cavuto, The Five, Special Report, Squawk on the Street, Closing Bell, CNBC Squawk on the Street, CNBC Power O’Reilly Factor, Fox News Special, Geraldo Prime, On The Money Lunch, Closing Bell, CNBC Fast Money, at Large, Hannity, Fox Weekend Morning, CNBC Prime, CNBC Shark Tank Weekend Afternoon 2/23-3/1 CNBC 6/1-6/7 9/22-9/28 Worldwide Exchange, Squawk Box, CNN FOX News Squawk on the Street, CNBC Power Early Start, New Day, CNN Newsroom, Fox & Friends, Fox News Live, Your World Lunch, Street Signs, Closing Bell, CNBC CNN News Daytime, The Situation Room, w/Neil Cavuto, Special Report, O’Reilly Fast Money, Mad Money, CNBC Prime, On Anderson Cooper 360, Original Series/ Factor, Fox News Special, Geraldo at The Money Specials, New Day Sunday, Fareed Large, Hannity, Fox Weekend Morning, Zakaria GPS , Crossfire Weekend Afternoon 3/9-3/15 FOX News 6/15-6/21 10/6-10/12 Fox & Friends, Fox News Live, The Five, CNBC MSNBC Special Report, Huckabee, O’Reilly Factor, Squawk Box, CNBC Power Lunch, Closing Morning Joe, MSNBC Live (Daytime) Geraldo at Large, Hannity, Fox Weekend Bell, CNBC Fast Money, CNBC Prime, Morning, Weekend Afternoon CNBC Shark Tank 10/27-11/2 CNN 3/23-3/29 6/29-7/5 Early Start, CNN News Daytime, The CNBC FOX News Situation Room, Crossfire, Erin Burnett Worldwide Exchange, Squawk Box, CNBC Fox & Friends, Fox News -

Star Channels, August 29

AUGUST 29 - SEPTEMBER 4, 2021 staradvertiser.com MAMA DRAMA While the cast fi gure out their uncomfortable love triangles, we get to watch from a much more comfortable distance when Season 2 of I Love a Mama’s Boy. The show follows couples navigating the relationship between the “boys” and their mothers who just can’t let go. Premiering Sunday, Aug. 29, on TLC. CAMERA & LIGHTING FOR BEGINNERS Learn how to properly set up, light and shoot in the second of three courses taught by ¶Ōlelo’s in-house experts. To sign up, visit olelo.org/training olelo.org Video Production | Camera, Audio & Lighting | Video Editing $75 per class | Just $50 per class if you commit to and complete all 3 classes 590255_TrainingAds_2021_2in_F.indd 2 4/30/21 4:17 PM ON THE COVER | I LOVE A MAMA’S BOY Mommy dearest TLC launches Season 2 relationship — not always accompanied by room relationship, but it didn’t work out that smothering mothers; something the Season way. of “I Love a Mama’s Boy” 2 trailer does a great job of showing. Complete Trying to help in that department, mommy with awkward professions of mother-son love, dearest accompanied Kim to the lingerie sour looks from partners, mothers feeding store to pick out something special for Matt. By Rachel Jones their sons scrambled eggs and mothers insist- Needless to say, shortly thereafter, Matt and TV Media ing on being “honeymoon buddies,” even view- Kim moved out of Kelly’s house and into their ers will want to tell these moms to butt out. -

Affidavit of Performance

OnMedia Advertising Sales 1037 Front Avenue Suite C Columbus , GA31901 Affidavit of Performance Client Name WARNOCK FOR GEORGIA/GA Contract ID 293083 Remarks 62853334-3646 Contract Type Political Bill Cycle 1/21 Bill Type Condensed EAI Broadcast Standard Date Weekday Network Zone Program Name Air Time Spot Name Spot Contract Billing Spot Length Line Status Cost 12/29/2020 Tuesday CNBC_E Columbus-Valley-Auburn Worldwide Exchange 5:10 AM RW-TV20-60H THE CH 00:01:60 1 Charged 48.00 * 12/30/2020 Wednesday CNBC_E Columbus-Valley-AuburnWOW GA Worldwide Exchange 5:12 AM RW-TV20-60H THE CH 00:01:60 1 Charged 48.00 * 01/01/2021 Friday CNBC_E Columbus-Valley-AuburnWOW GA The Profit 8:16 AM RW-TV20-63H SHOES 00:01:60 1 Charged 48.00 * 12/30/2020 Wednesday CNBC_E Columbus-Valley-AuburnWOW GA Fast Money Halftime 12:46 PM RW-TV20-60H THE CH 00:01:60 2 Charged 26.00 * 12/30/2020 Wednesday CNBC_E Columbus-Valley-AuburnWOW GA The Exchange 1:17 PM RW-TV20-60H THE CH 00:01:60 2 Charged 26.00 * 01/01/2021 Friday CNBC_E Columbus-Valley-AuburnWOW GA Jay Leno's Garage 11:14 AM RW-TV20-63H SHOES 00:01:60 2 Charged 26.00 * 01/01/2021 Friday CNBC_E Columbus-Valley-AuburnWOW GA Jay Leno's Garage 11:54 AM RW-TV20-63H SHOES 00:01:60 2 Charged 26.00 * 01/05/2021 Tuesday CNBC_E Columbus-Valley-AuburnWOW GA Squawk on the Street 10:51 AM RW-TV20-63H SHOES 00:01:60 3 Charged 26.00 * 12/30/2020 Wednesday CNBC_E Columbus-Valley-AuburnWOW GA Fast Money 5:38 PM RW-TV20-60H THE CH 00:01:60 4 Charged 38.00 * 12/31/2020 Thursday CNBC_E Columbus-Valley-AuburnWOW GA Fast Money