Embargoed Copy, Not Be Reported in Full, Or in Part, Before 00.01 24 August 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Copy of 2008122008-Cwells-Regulated

1 donation information continues on reverse Late reported donation by regulated donees 15 February 2001 - 31 January 2008 (where data is available) Regulated donee Donor organisation Donor forename Donor surname Donor status Address 1 Address 2 Jimmy Hood MP BAA Plc Company 130 Wilton Road Keith Simpson MP BAA Plc Company 130 Wilton Road Cheryl Gillan MP BAA Plc Company 130 Wilton Road Elfyn Llwyd MP BAA Plc Company 130 Wilton Road Ian Stewart MP BAA Plc Company 130 Wilton Road Ian Stewart MP Manchester Airport Plc Company PO Box 532 Town Hall John Gummer MP BAA Plc Company 130 Wilton Road Christopher Beazles BAA Plc Company 130 Wilton Road Chris Smith MP BAA Plc Company 130 Wilton Road Mike Weir MP BAA Plc Company 130 Wilton Road Tony Worthington MP BAA Plc Company 130 Wilton Road Ian Davidson MP BAA plc Company 130 Wilton Road Paul Tyler BAA Plc Company 130 Wilton Road Matthew Taylor MP BAA Plc Company 130 Wilton Road Menzies Campbell MP BAA Plc Company 130 Wilton Road Archy Kirkwood BAA Plc Company 130 Wilton Road David Hanson MP BAA Plc Company 130 Wilton Road Colin Breed MP BAA Plc Company 130 Wilton Road David Marshall MP BAA Plc Company 130 Wilton Road Mark Oaten MP BAA Plc Company 130 Wilton Road Diana Wallis MEP Manchester Airport Plc Company PO Box 532 Town Hall Christopher Ruane MP BAA Plc Company 130 Wilton Road Tim Loughton MP BAA Plc Company 130 Wilton Road Robert Wareing MP BAA Plc Company 130 Wilton Road Robert Wareing MP Manchester Airport Plc Company PO Box 532 Town Hall John McFall MP BAA Plc Company 130 Wilton Road -

Z675928x Margaret Hodge Mp 06/10/2011 Z9080283 Lorely

Z675928X MARGARET HODGE MP 06/10/2011 Z9080283 LORELY BURT MP 08/10/2011 Z5702798 PAUL FARRELLY MP 09/10/2011 Z5651644 NORMAN LAMB 09/10/2011 Z236177X ROBERT HALFON MP 11/10/2011 Z2326282 MARCUS JONES MP 11/10/2011 Z2409343 CHARLOTTE LESLIE 12/10/2011 Z2415104 CATHERINE MCKINNELL 14/10/2011 Z2416602 STEPHEN MOSLEY 18/10/2011 Z5957328 JOAN RUDDOCK MP 18/10/2011 Z2375838 ROBIN WALKER MP 19/10/2011 Z1907445 ANNE MCINTOSH MP 20/10/2011 Z2408027 IAN LAVERY MP 21/10/2011 Z1951398 ROGER WILLIAMS 21/10/2011 Z7209413 ALISTAIR CARMICHAEL 24/10/2011 Z2423448 NIGEL MILLS MP 24/10/2011 Z2423360 BEN GUMMER MP 25/10/2011 Z2423633 MIKE WEATHERLEY MP 25/10/2011 Z5092044 GERAINT DAVIES MP 26/10/2011 Z2425526 KARL TURNER MP 27/10/2011 Z242877X DAVID MORRIS MP 28/10/2011 Z2414680 JAMES MORRIS MP 28/10/2011 Z2428399 PHILLIP LEE MP 31/10/2011 Z2429528 IAN MEARNS MP 31/10/2011 Z2329673 DR EILIDH WHITEFORD MP 31/10/2011 Z9252691 MADELEINE MOON MP 01/11/2011 Z2431014 GAVIN WILLIAMSON MP 01/11/2011 Z2414601 DAVID MOWAT MP 02/11/2011 Z2384782 CHRISTOPHER LESLIE MP 04/11/2011 Z7322798 ANDREW SLAUGHTER 05/11/2011 Z9265248 IAN AUSTIN MP 08/11/2011 Z2424608 AMBER RUDD MP 09/11/2011 Z241465X SIMON KIRBY MP 10/11/2011 Z2422243 PAUL MAYNARD MP 10/11/2011 Z2261940 TESSA MUNT MP 10/11/2011 Z5928278 VERNON RODNEY COAKER MP 11/11/2011 Z5402015 STEPHEN TIMMS MP 11/11/2011 Z1889879 BRIAN BINLEY MP 12/11/2011 Z5564713 ANDY BURNHAM MP 12/11/2011 Z4665783 EDWARD GARNIER QC MP 12/11/2011 Z907501X DANIEL KAWCZYNSKI MP 12/11/2011 Z728149X JOHN ROBERTSON MP 12/11/2011 Z5611939 CHRIS -

Brief Amicus Curiae of the Senate of the United Mexican States, Et

No. 08-987 IN THE RUBEN CAMPA, RENE GONZALEZ, ANTONIO GUERRERO, GERARDO HERNANDEZ, AND LUIS MEDINA, Petitioners, v. UNITED STATES OF AMERICA, Respondent. On Petition for a Writ of Certiorari to the United States Court of Appeals for the Eleventh Circuit BRIEF IN SUPPORT OF PETITION FOR A WRIT OF CERTIORARI ON BEHALF OF THE SENATE OF THE UNITED MEXICAN STATES, THE NATIONAL ASSEMBLY OF PANAMA, MARY ROBINSON (UNITED NATIONS HIGH COMMISSIONER FOR HUMAN RIGHTS, 1997- 2002; PRESIDENT OF IRELAND, 1992-1997) AND LEGISLATORS FROM THE EUROPEAN PARLIAMENT AND THE COUNTRIES OF BRAZIL, BELGIUM, CHILE, GERMANY, IRELAND, JAPAN, MEXICO, SCOTLAND AND THE UNITED KINGDOM ______________ Michael Avery Counsel of Record Suffolk Law School 120 Tremont Street Boston, MA 02108 617-573-8551 ii AMICI CURIAE The Senate of the United Mexican States The National Assembly of Panama Mary Robinson (United Nations High Commissioner for Human Rights, 1997-2002; President of Ireland, 1992-1997) Legislators from the European Parliament Josep Borrell Fontelles, former President Enrique Barón Crespo, former President Miguel Ángel Martínez, Vice-President Rodi Kratsa-Tsagaropoulou, Vice-President Luisa Morgantini, Vice-President Mia De Vits, Quaestor Jo Leinen, Chair of the Committee on Constitutional Affairs Richard Howitt, Vice-Chair of the Subcommittee on Human Rights Guisto Catania, Vice-Chair of the Committee on Civil Liberties, Justice and Home Affairs Willy Meyer Pleite, Vice-Chair of the Delegation to the Euro-Latin American Parliamentary Assembly Edite Estrela, Vice-Chair -

Has Your MP Pledged to ACT On

January 2011 Issue 6 Providing information, support and access to established, new or innovative treatments for Atrial Fibrillation Nigel Mills MP Eric Illsley MP John Baron MP David Evennett MP Nick Smith MP Dennis Skinner MP Julie Hilling MP David Tredinnick MP Amber Valley Barnsley Central Basildon and BillericayHHasBexleyheath and CrayfordaBlaenau sGwent Bolsover Bolton West Bosworth Madeleine Moon MP Simon Kirby MP Jonathan Evans MP Alun Michael MP Tom Brake MP Mark Hunter MP Toby Perkins MP Martin Vickers MP Bridgend Brighton, Kemptown Cardiff North Cardiff South and Penarth Carshalton and Wallington Cheadle Chesterfield Cleethorpes Henry Smith MP Edward Timpson MP Grahame Morris MP Stephen Lloyd MP Jo Swinson MP Damian Hinds MP Andy Love MP Andrew Miller MP Crawley Creweyyour and Nantwich oEasington uEastbournerEast Dunbartonshire MMPEast Hampshire PEdmonton Ellesmere Port and Neston Nick de Bois MP David Burrowes MP Mark Durkan MP Willie Bain MP Richard Graham MP Andrew Jones MP Bob Blackman MP Jim Dobbin MP Enfield North Enfield Southgate Foyle Glasgow North East Gloucester Harrogate and Knaresborough Harrow East Heywood and Middleton Andrew Bingham MP Angela Watkinson MP Andrew Turner MP Jeremy Wright MP Joan Ruddock MP Philip Dunne MP Yvonne Fovargue MP John Whittingdale MP High Peak Hornchurchppledged and Upminster lIsle of eWight Kenilworthd and Southam Lewishamg Deptford eLudlow dMakerfield Maldon Annette Brooke MP Glyn Davies MP Andrew Bridgen MP Chloe Smith MP Gordon Banks MP Alistair Carmichael MP Douglas Alexander MP -

Political and Constitutional Reform Committee

Political and Constitutional Reform Committee Committee Office · House of Commons · 7 Millbank · London SW1P 3JA Tel 020 7219 6287 Fax 020 7219 2681 Email [email protected] Website www.parliament.uk/pcrc 7 September 2010 Written evidence published by the Committee to date for the inquiry into the government’s proposals for voting and parliamentary reform: Parliamentary Voting System and Constituencies Bill PVSCB 01 Lewis Baston, Democratic Audit PVSCB 02 David Allen PVSCB 03 Keep Cornwall Whole PVSCB 04 Secretaries to the Boundary Commissions PVSCB 05 Professor Robert Hazell and Mark Chalmers, Constitution Unit, University College London PVSCB 06 Dr Stuart Wilks-Heeg, Director, Democratic Audit PVSCB 07 Labour Campaign for Electoral Reform PVSCB 08 New Economics Foundation PVSCB 09 Rt Hon Denis MacShane MP PVSCB 10 Dr Graeme Orr and Prof K D Ewing PVSCB 11 Prof Michael Thrasher PVSCB 12 Dr Michael Pinto-Duschinsky PVSCB 13 Dr Matt Qvortrup, Cranfield University PVSCB 14 Professor Patrick Dunleavy, Chair, Public Policy Group, London School of Economics and Political Science PVSCB 15 Nicola Prigg PVSCB 16 Lord Lipsey PVSCB 17 Hugh Bayley MP PVSCB 18 Chris Ruane MP, Clive Betts MP, Andy Love MP and Russell Brown MP PVSCB 19 Rt Hon Peter Hain MP PVSCB 20 Paul Howley PVSCB 21 Rt Hon Paul Murphy MP PVSCB 22 Electoral Registration Office and Returning Officer, Weymouth and Portland Borough Council PVSCB 23 David A. G. Nowell PVSCB 24 Fawcett Society PVSCB 25 Ipsos MORI 2 Memorandum from Lewis Baston, Democratic Audit (PVSCB 01) I am currently senior research fellow with Democratic Audit and it is under the auspices of Democratic Audit that I offer these observations on the Parliamentary Voting Systems and Constituencies Bill. -

Parliamentary Debates (Hansard)

Monday Volume 583 23 June 2014 No. 11 HOUSE OF COMMONS OFFICIAL REPORT PARLIAMENTARY DEBATES (HANSARD) Monday 23 June 2014 £5·00 © Parliamentary Copyright House of Commons 2014 This publication may be reproduced under the terms of the Open Parliament licence, which is published at www.parliament.uk/site-information/copyright/. HER MAJESTY’S GOVERNMENT MEMBERS OF THE CABINET (FORMED BY THE RT HON.DAVID CAMERON,MP,MAY 2010) PRIME MINISTER,FIRST LORD OF THE TREASURY AND MINISTER FOR THE CIVIL SERVICE—The Rt Hon. David Cameron, MP DEPUTY PRIME MINISTER AND LORD PRESIDENT OF THE COUNCIL—The Rt Hon. Nick Clegg, MP FIRST SECRETARY OF STATE AND SECRETARY OF STATE FOR FOREIGN AND COMMONWEALTH AFFAIRS—The Rt Hon. William Hague, MP CHANCELLOR OF THE EXCHEQUER—The Rt Hon. George Osborne, MP CHIEF SECRETARY TO THE TREASURY—The Rt Hon. Danny Alexander, MP SECRETARY OF STATE FOR THE HOME DEPARTMENT—The Rt Hon. Theresa May, MP SECRETARY OF STATE FOR DEFENCE—The Rt Hon. Philip Hammond, MP SECRETARY OF STATE FOR BUSINESS,INNOVATION AND SKILLS—The Rt Hon. Vince Cable, MP SECRETARY OF STATE FOR WORK AND PENSIONS—The Rt Hon. Iain Duncan Smith, MP LORD CHANCELLOR AND SECRETARY OF STATE FOR JUSTICE—The Rt Hon. Chris Grayling, MP SECRETARY OF STATE FOR EDUCATION—The Rt Hon. Michael Gove, MP SECRETARY OF STATE FOR COMMUNITIES AND LOCAL GOVERNMENT—The Rt Hon. Eric Pickles, MP SECRETARY OF STATE FOR HEALTH—The Rt Hon. Jeremy Hunt, MP SECRETARY OF STATE FOR ENVIRONMENT,FOOD AND RURAL AFFAIRS—The Rt Hon. Owen Paterson, MP SECRETARY OF STATE FOR INTERNATIONAL DEVELOPMENT—The Rt Hon. -

15Th May 2015

Weekly e Briefing: 15 May 2015 Welcome to the Commissioner’s weekly horizon scanning brief: 1. Legislation (Legislation, Home Office, APCC, press comments, reports and campaigns relating to strategy, policy and programmes) 2. Strategic policing and crime news (relevant crime and criminal justice information and partners’ policy/reports/campaigns) 3. Developments and reports (covering research across political, economic, social, technological, environmental and organisations) 4. Consultations (police and crime bulletins, research, consultations and press releases) 5. Reviews and Inspections (covering various reviews, inspections and audits across policing) Contact Officer: [email protected] 1. Legislation General Election 2015 Completed update on the new MPs. Immigration Act 2014: appeals 'Legal highs' to be banned under temporary power Historic law to end Modern Slavery passed The Counter-Terrorism and Security Act 2015 (Risk of Being Drawn into Terrorism) (Amendment and Guidance) Regulations 2015 Serious Crime Bill: overarching documents New rules to crackdown on violent prisoners comes into force Bill on PCC recall Anti-Social Behaviour, Crime and Policing Act 2014 2. Strategic policing and crime news Her Majesty's Government: May 2015 The government appointments have been confirmed as at 14 May 2015. Counter-Extremism Bill - National Security Council meeting 15 May 2015 Weekly e Briefing: At the first meeting of the new National Security Council (NSC) plans for a new Counter- Extremism Bill will be discussed. -

Bacton, Cotton, Wyverstone Yearbook 2013 Bacton, Cotton, Wyverstone Yearbook 2014

Bacton, Cotton, Wyverstone Yearbook 2013 Bacton, Cotton, Wyverstone Yearbook 2014 2 Bacton, Cotton, Wyverstone Yearbook 2014 Local Clubs and Organisations Bacton Bowls Club........................23 Safer Neighbourhood Team.........35 Bacton & Cotton Local History Schools - Community, Primary & Society..............................................37 Middle....................................18 & 19 Bacton & Wyverstone Scout Group....................................13 Mothers Union...............................30 SNAP..................................................7 Bacton Play Centre/ Stowmarket Swimming Club........12 Bacton Under Fives.......................18 The Company of Friends.............30 Bacton United FC..........................17 Travel Information.........................25 Bacton & Wyverstone Village Halls....................................36 Horticultural Society......................21 Waste and Recycling.......................44 Butcher...............................................3 WI.....................................................21 Carter‘s Meadow Trust....................6 Winters School of Dance.............12 Churches..................................26 - 29 Work Club.........................................5 Church Friends.....................30 & 31 Wyverstone Carpet Bowls Club...22 Community Cafes...........................41 Wyverstone Over 60s.....................22 Cotton & District VPA.................20 Wyverstone Town Est. Charity.....30 District & County Councillors.....32 Doctors‘ Surgeries................38 -

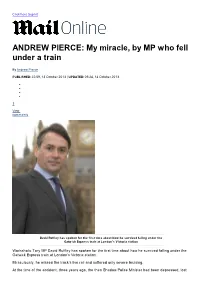

ANDREW PIERCE: My Miracle, by MP Who Fell Under a Train

Click here to print ANDREW PIERCE: My miracle, by MP who fell under a train By Andrew Pierce PUBLISHED: 22:59, 13 October 2013 | UPDATED: 09:24, 14 October 2013 3 View comments David Ruffley has spoken for the first time about how he survived falling under the Gatw ick Express train at London's Victoria station Workaholic Tory MP David Ruffley has spoken for the first time about how he survived falling under the Gatwick Express train at London’s Victoria station. Miraculously, he missed the track’s live rail and suffered only severe bruising. At the time of the accident, three years ago, the then Shadow Police Minister had been depressed, lost weight and was smoking and drinking too much. The incident was described as a failed suicide attempt because he was downcast, having becoming embroiled in the MPs’ expenses scandal. (He had claimed £1,674 for a sofa, £2,175 for a 46in high- definition television and a further £6,765 on furnishings, including a bed for his second home in London.) But now 52-year-old Ruffley’s life has turned around. Instead of being only a rare attender of Commons debates, he has one of the best records among all MPs and has been readopted to fight his Suffolk seat again at the 2015 election. Recalling the events at Victoria station, he tells me: ‘It was an accident. I certainly had a bout of depression, but it’s not something I’ve had since. It was a psychological imbalance. ‘I was incredibly lucky, to say the least. -

Wyverstone Cotton Bacton YEARBOOK 2012

Golden (Wyverstone) by Audrey Erbany Wyverstone Cotton Bacton YEARBOOK 2012 This Yearbook is delivered FREE every year to 1,000 homes and businesses in Bacton, Cotton & Wyverstone. Page Please support our loyal advertisers INCES Hunters from £25 Men’s & Sherwood Ladies’ Now Outdoor in Stock Wear 25 Ipswich Street Stowmarket, Suffolk T 01449 612664 IP14 1AH Page 2 A Letter from the Editor The Wyverstone, Cotton & Bacton Yearbook is an annual publication containing advertisements from local businesses (mainly on the yellow pages) and information about all our local organisations, churches, local politicians and so on (on the white pages) as well as bus timetables and doctors’ surgery hours (on the green centre pages). A large number of people deserve thanks for giving their time to the Yearbook. Amanda Hagger managed to find willing advertisers, Brian Manley has managed the accounts, Audrey Erbany has contributed her fabulous paintings and a huge number of volunteers have delivered this magazine to your door. Without such dedicated volunteers this Yearbook would never be produced. Last year we raised about £800 which is being used to support the various Community Projects centred on the new facilities in St Mary’s Church. These will include a work club, a club for older teenagers, a drop in café and a club for carers. This year, even though we have more advertisers, we should raise about £650 which will also go to these projects. Our decline in profit this year is due to increased printing costs. And if you would like to produce next year’s Yearbook, please get in touch. -

Private Finance 2

House of Commons Treasury Committee Private Finance 2 Tenth Report of Session 2013–14 Volume I: Report, together with formal minutes, and oral evidence Written evidence is contained in Volume II, available on the Committee website at www.parliament.uk/treascom. Ordered by the House of Commons to be printed 12 March 2014 HC 97 [Incorporating HC 990, Session 2012–13] Published June 2014 by authority of the House of Commons London: The Stationery Office Limited £14.50 The Treasury Committee The Treasury Committee is appointed by the House of Commons to examine the expenditure, administration, and policy of HM Treasury, HM Revenue and Customs and associated public bodies. All publications of the Committee (including press notices) and further details can be found on the Committee’s web pages at www.parliament.uk/treascom. Membership at time of the report Mr Andrew Tyrie MP (Conservative, Chichester) (Chairman) Mark Garnier MP (Conservative, Wyre Forest) Stewart Hosie MP (Scottish National Party, Dundee East) Andrea Leadsom MP (Conservative, South Northamptonshire) Mr Andy Love MP (Labour, Edmonton) John Mann MP (Labour, Bassetlaw) Mr Pat McFadden MP (Labour, Wolverhampton South West) Mr George Mudie MP (Labour, Leeds East) Mr Brooks Newmark MP (Conservative, Braintree) Jesse Norman MP (Conservative, Hereford and South Herefordshire) Teresa Pearce MP (Labour, Erith and Thamesmead) David Ruffley MP (Conservative, Bury St Edmunds) John Thurso MP (Liberal Democrat, Caithness, Sutherland, and Easter Ross) Powers The Committee is one of the departmental select committees, the powers of which are set out in House of Commons Standing Orders, principally in SO No 152. These are available on the Internet via www.parliament.uk. -

Do Actions Speak Louder Than Words? Nonverbal Communication in Parliamentary Oversight Committee Hearings

Do Actions Speak Louder than Words? Nonverbal Communication in Parliamentary Oversight Committee Hearings by Cheryl Schonhardt-Bailey, FBA Government Department London School of Economics and Political Science [email protected] http://personal.lse.ac.uk/schonhar/ Prepared for the Political Persuasion Conference Laguna Beach January 2016 1 “To me, public accountability is a moral corollary of central bank independence. In a democratic society, the central bank’s freedom to act implies an obligation to explain itself to the public. … While central banks are not in the public relations business, public education ought to be part of their brief.” (Alan Blinder, Princeton University professor and former vice chairman, Federal Reserve Board; (Blinder 1998: 69) ) “We made clear as a committee that we were going to look at the distributional impact of the budget in unprecedented detail. As a result, George Osborne responded by giving a lot more detail not only in the budget but also when he came before us. And there were some pretty vigorous and detailed exchanges about the distributional impact of the budget in that hearing. I think everybody gained from that experience. It certainly enabled a wider public to find out exactly what was going on in the budget and the Government was forced to explain its actions.” (Andrew Tyrie MP, Chairman Treasury Select Committee, commenting on Chancellor Osborne’s first budget (UK-Parliament 2011). 1. Introduction Public officials in modern democracies are conscious that their decisions and actions should be and are subject to scrutiny in the public domain. In the United Kingdom, this scrutiny is a statutory requirement and is conducted in formal parliamentary committee hearings.