LSEG Prospectus 9Dec2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Defenses to Customer Claims Against Stockbrokers

DEFENSES TO CUSTOMER CLAIMS AGAINST STOCKBROKERS Elizabeth Hoop Fay, Esquire Morgan, Lewis & Bockius LLP Philadelphia Foster S. Goldman, Jr., Esquire Markel Schafer & Goldman, PC Pittsburgh DEFENSES TO CUSTOMER CLAIMS AGAINST STOCKBROKERS I. DEFENSES TO CHURNING, SUITABILITY AND UNAUTHORIZED TRADING CLAIMS A. The Elements of Causes of Action for Churning, Unsuitable Recommendations and Unauthorized Trading 1. Churning of a brokerage account occurs when a broker who exercises control over the trading engages in an excessive number of transactions in order to generate commissions. See, e.g., Costello v. Oppenheimer & Co., Inc., 711 F.2d 1361, 1368-69 (7th Cir. 1983). To prevail on a churning claim, the customer must prove three elements: (1) control of the account by the broker; (2) trading activity that is excessive in light of the customer’s investment objectives; and (3) that the broker acted with scienter, i.e., intent to defraud or reckless disregard of the customer’s interests. Craighead v. E.F. Hutton & Co., 899 F.2d 485, 489 (6th Cir. 1990). 2. While a churning claim is a challenge to the quantity of transactions, a suitability claim challenges the quality of the investments recommended by the broker. To prevail on a suitability claim, the customer generally must prove: (1) that the broker recommended securities that are unsuitable in light of the customer’s investment objectives; and (2) that the broker did so with intent to defraud or with reckless disregard for the client’s interests. E.g., Brown v. E.F. Hutton Group Inc., 991 F.2d 1020, 1031 (2d Cir. 1991). 3. -

An Assessment of Valuation Methods of Stock Initial Public Offerings on Tehran Stock Exchange

International Journal of Academic Research in Business and Social Sciences 2017, Vol. 7, No. 4 ISSN: 2222-6990 An Assessment of Valuation Methods of Stock Initial Public offerings on Tehran Stock Exchange Mohammad Kheiry 1, Sima Golozar 2,*, Ali Amiri 3 1 Department of Economic, Accounting and Management, Payam Noor University, Tehran, Iran. Kheiry Email: [email protected] 2,* Postgraduate student of Financial Management, Qeshm Institute for Higher Education, Qeshm, Iran. Email: [email protected] 3 Department of Accounting, college of human science, Bandar Abbas, Islamic Azad University, Bandar Abbas, Iran. Email: [email protected] DOI: 10.6007/IJARBSS/v7-i4/2822 URL: http://dx.doi.org/10.6007/IJARBSS/v7-i4/2822 Abstract Every day hundreds of companies all over the world are entering capital market for the first time by issuing stocks. By doing so, they decide to invest capital necessary for continuing activity and expanding operations accordingly. For this reason, it is important to the companies that price specified for their stock demonstrate real value of assets and their growth and development opportunities in the future. The purpose of this research is to study valuation methods of stock initial public offerings at the Tehran Stock Exchange. Population and study sample consisted of firms publicly offered their stocks for the first time at Tehran Stock Exchange during 2009-2014, and experienced no trading halt, i.e. 45 companies of which seven companies were eliminated due to lack of trading on the stock exchange and 38 firms were chosen. The research method is correlational-descriptive and the research is an applied research by purpose. -

LIBOR Transition Faqs ‘Big Bang’ CCP Switch Over

RED = Final File Size/Bleed Line BLACK = Page Size/Trim Line MAGENTA = Margin/Safe Art Boundary NOT A PRODUCT OF BARCLAYS RESEARCH LIBOR Transition FAQs ‘Big bang’ CCP switch over 1. When will CCPs switch their rates for discounting 2. €STR Switch Over to new risk-free rates (RFRs)? What is the ‘big bang’ 2a. What are the mechanics for the cash adjustment switch over? exchange? Why is this necessary? As part of global industry efforts around benchmark reform, Each CCP will perform a valuation using EONIA and then run most systemic Central Clearing Counterparties (CCPs) are the same valuation by switching to €STR. The switch to €STR expected to switch Price Aligned Interest (PAI) and discounting discounting will lead to a change in the net present value of EUR on all cleared EUR-denominated products to €STR in July 2020, denominated trades across all CCPs. As a result, a mandatory and for USD-denominated derivatives to SOFR in October 2020. cash compensation mechanism will be used by the CCPs to 1a. €STR switch over: weekend of 25/26 July 2020 counter this change in value so that individual participants will experience almost no ‘net’ changes, implemented through a one As the momentum of benchmark interest rate reform continues off payment. This requirement is due to the fact portfolios are in Europe, while EURIBOR has no clear end date, the publishing switching from EONIA to €STR flat (no spread), however there of EONIA will be discontinued from 3 January 2022. Its is a fixed spread between EONIA and €STR (i.e. -

Initial Public Offerings

November 2017 Initial Public Offerings An Issuer’s Guide (US Edition) Contents INTRODUCTION 1 What Are the Potential Benefits of Conducting an IPO? 1 What Are the Potential Costs and Other Potential Downsides of Conducting an IPO? 1 Is Your Company Ready for an IPO? 2 GETTING READY 3 Are Changes Needed in the Company’s Capital Structure or Relationships with Its Key Stockholders or Other Related Parties? 3 What Is the Right Corporate Governance Structure for the Company Post-IPO? 5 Are the Company’s Existing Financial Statements Suitable? 6 Are the Company’s Pre-IPO Equity Awards Problematic? 6 How Should Investor Relations Be Handled? 7 Which Securities Exchange to List On? 8 OFFER STRUCTURE 9 Offer Size 9 Primary vs. Secondary Shares 9 Allocation—Institutional vs. Retail 9 KEY DOCUMENTS 11 Registration Statement 11 Form 8-A – Exchange Act Registration Statement 19 Underwriting Agreement 20 Lock-Up Agreements 21 Legal Opinions and Negative Assurance Letters 22 Comfort Letters 22 Engagement Letter with the Underwriters 23 KEY PARTIES 24 Issuer 24 Selling Stockholders 24 Management of the Issuer 24 Auditors 24 Underwriters 24 Legal Advisers 25 Other Parties 25 i Initial Public Offerings THE IPO PROCESS 26 Organizational or “Kick-Off” Meeting 26 The Due Diligence Review 26 Drafting Responsibility and Drafting Sessions 27 Filing with the SEC, FINRA, a Securities Exchange and the State Securities Commissions 27 SEC Review 29 Book-Building and Roadshow 30 Price Determination 30 Allocation and Settlement or Closing 31 Publicity Considerations -

Euronext Makes Irrevocable Cash Offer to Acquire Lch.Clearnet Sa

CONTACT - Media: CONTACT - Investor Relations: Amsterdam +31.20.721.4488 Brussels +32.2.620.15.50 +33.1.70.48.24.17 Lisbon +351.210.600.614 Paris +33.1.70.48.24.45 EURONEXT MAKES IRREVOCABLE CASH OFFER TO ACQUIRE LCH.CLEARNET SA Euronext has made an irrevocable all-cash offer to LCH.Clearnet Group Limited (“LCH.Clearnet Group”) and London Stock Exchange Group plc (“LSEG”) to acquire LCH.Clearnet SA (“Clearnet”), in relation to which terms and conditions have been agreed. Clearnet has commenced a period of consultation with its works council during which LSEG and LCH.Clearnet Group have granted exclusivity to Euronext Strategic combination to strengthen Euronext at the heart of the Eurozone capital markets: • Strengthening long-term control of clearing activities for Euronext’s markets, while enhancing our ability to innovate • Improving Euronext’s business diversification (post-trade revenue to represent approximately 30% of Euronext’s pro forma revenue) • Providing substantial growth opportunities in Fixed Income and CDS • Acquisition price of €510m (subject to a closing adjustment and including excess capital1) for 100% of Clearnet • Expected pre-tax operating cost synergies of €13m and additional opportunities for revenue synergies Completion of the contemplated transaction is subject to various conditions including: • Closing of the merger between Deutsche Börse AG (“DB”) and LSEG • Euronext shareholder approval • Customary regulatory and anti-trust approvals and other consents • Completion of the works council consultation process of Clearnet Irrespective of the completion of the contemplated transaction, Euronext remains committed to delivering the best long-term solution for its post-trade activities, in the interests of its clients and shareholders Amsterdam, Brussels, Lisbon, London and Paris – 3 January 2017 – Euronext, the leading pan-European exchange in the Eurozone, has signed a binding offer and been granted exclusivity to acquire 100% of the share capital and voting rights of Clearnet. -

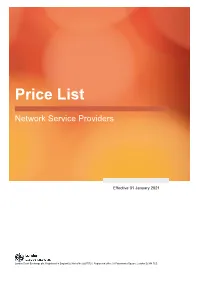

NSP Price List

Network Service Provider Price List For Network Service Providers providing customer access to London Stock Exchange Group Trading and Information Systems Price List Network Service Providers Effective 01 January 2021 London Stock Exchange plc. Registered in England & Wales No 02075721. Registered office 10 Paternoster Square, London EC4M 7LS. Network Service Provider Price List For Network Service Providers providing customer access to London Stock Exchange Group Trading and Information Systems Service Monthly cost per NSP per client per setup*/GBP London Stock Exchange Interactive Services1 1,995 London Stock Exchange Information Services 2,205 London Stock Exchange Testing Only Services2 645 London Stock Exchange Derivatives Market 260 Turquoise Interactive Services1 330 Turquoise Information Services 441 Borsa Italiana Equities 330 Borsa Italiana IDEM Derivatives 330 EuroTLX 330 Notes: 1Includes Trading, Drop-Copy and Post-Trade Gateways, and CDS. 2This service is included for free when ordered with London Stock Exchange Interactive Services or London Stock Exchange Information Services. If you are interested in taking FixHub services, please contact [email protected] for further information. Please note that all services are subject to a 90-day notice period for cancellation. All new services ordered are subject to a minimum 12-month service term. Orders *The ordering and cancellation of services is only supported by an NSP submitting a valid Technical Information Form to [email protected] For more information, please contact our Technology Business Development team on +44 (0)20 7797 3211 or email [email protected] London Stock Exchange plc. Registered in England & Wales No 02075721. Registered office 10 Paternoster Square, London EC4M 7LS. -

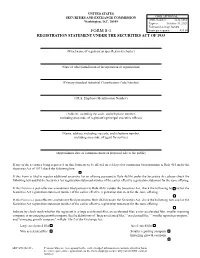

Registration Statement Under Securities Act of 1933

UNITED STATES SECURITIES AND EXCHANGE COMMISSION OMB APPROVAL OMB Number: 3235-0065 Washington, D.C. 20549 Expires: October 31, 2021 Estimated average burden FORM S-1 hours per response ............653.54 REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 (Exact name of registrant as specified in its charter) (State or other jurisdiction of incorporation or organization) (Primary Standard Industrial Classification Code Number) (I.R.S. Employer Identification Number) (Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) (Name, address, including zip code, and telephone number, including area code, of agent for service) (Approximate date of commencement of proposed sale to the public) If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. -

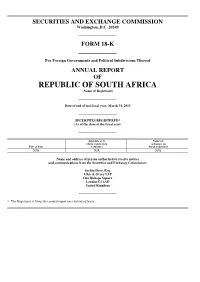

Printmgr File

SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 18-K For Foreign Governments and Political Subdivisions Thereof ANNUAL REPORT OF REPUBLIC OF SOUTH AFRICA (Name of Registrant) Date of end of last fiscal year: March 31, 2013 SECURITIES REGISTERED* (As of the close of the fiscal year) Amounts as to Names of which registration exchanges on Title of Issue is effective which registered N/A N/A N/A Name and address of person authorized to receive notices and communications from the Securities and Exchange Commission: Sachin Davé, Esq. Allen & Overy LLP One Bishops Square London E1 6AD United Kingdom * The Registrant is filing this annual report on a voluntary basis. (1) In respect of each issue of securities of the registrant, a brief statement as to: (a) The general effect of any material modifications, not previously reported, of the rights of the holders of such securities. There have been no such modifications. (b) The title and the material provisions of any law, decree or administrative action, not previously reported, by reason of which the security is not being serviced in accordance with the terms thereof. There has been no such law, decree or administrative action. (c) The circumstances of any other failure, not previously reported, to pay principal, interest or any sinking fund or amortization installment. There has been no such failure. (2) A statement as of the close of the last fiscal year, giving the total outstanding of: (a) Internal funded debt of the registrant. (Total to be stated in the currency of the registrant. If any internal funded debt is payable in a foreign currency, it should not be included under this paragraph (a), but under paragraph (b) of this item.) See “Tables and Supplementary Information,” pages 126-141 of Exhibit 99.D, which are hereby incorporated by reference herein. -

Thomson Completes Acquisition of Reuters; Thomson Reuters Shares Begin Trading Today

Thomson Completes Acquisition of Reuters; Thomson Reuters Shares Begin Trading Today April 17, 2008 << World's Leading Source of Intelligent Information for Businesses and Professionals US$500 Million Share Repurchase Program Announced >> The Thomson Corporation today announced that it has completed its acquisition of Reuters Group PLC, forming Thomson Reuters (NYSE: TRI; TSX: TRI; LSE: TRIL: Nasdaq: TRIN), the world's leading source of intelligent information for businesses and professionals in the financial, legal, tax and accounting, scientific, healthcare, and media markets. Thomson Reuters has more than 50,000 employees with operations in 93 countries on six continents and 2007 pro forma revenues of approximately US$12.4 billion. << (Logo: http://www.newscom.com/cgi-bin/prnh/20020227/NYW014LOGO ) >> Effective today, Thomson Reuters shares will begin trading on exchanges in Toronto, New York and London and are eligible for inclusion in S&P/TSX and FTSE 100 UK indices. Thomson Reuters Corporation's common shares are listed on the Toronto Stock Exchange and the New York Stock Exchange under the ticker symbol "TRI". Thomson Reuters PLC ordinary shares are listed on the London Stock Exchange under the symbol "TRIL" and its ADSs are listed on Nasdaq under the symbol "TRIN". Thomas H. Glocer, chief executive officer of Thomson Reuters, said, "This is a very exciting day for our shareholders, customers and employees. Thomson Reuters will deliver the intelligent information needed to give businesses and professionals the knowledge to act. We call our information "intelligent" because it is not only insightful, highly relevant and timely, but it is also made available in formats which applications can consume and to which they can add further value. -

When Information Is Abundant, a Good Filter Is Prized

WHEN INFORMATION IS ABUNDANT, A GOOD FILTER IS PRIZED In the internet age, the abundance of free information creates its own problems. This is the opportunity for the big business information groups. Tom Glocer, CEO of Thomson Reuters, argues that a path to relevant information is what people need s Stewart Brand, an early technology That statement is as true now as it was then, guru, wrote in The Media Lab nearly despite the information revolution that has A a quarter century ago, “Information occurred in the intervening years. So much wants to be free. Information also wants to information has become freely available as the be expensive. Information wants to be free internet has evolved. But businesses still need because it has become so cheap to distribute, information that helps them do commerce copy, and recombine – too cheap to meter. and are willing to pay for it. The challenge It wants to be expensive because it can be now lies in providing the most useful and immeasurably valuable to the recipient. relevant information – and in creating an That tension will not go away.” efficient path to it. 12 Brunswick Issue four Review Summer 2011 1851 Paul Julius Reuter opens an office to transmit stock market quotations and news between London 1965 and Paris over the new Thomson Newspapers Dover-Calais submarine becomes a publicly quoted telegraph cable. company on the Toronto 1934 Stock Exchange. Roy Thomson acquires his first newspaper, purchasing the Timmins Daily Press in Ontario. Since the invention of Gutenberg’s press in the were sent via the internet in 2010 alone, and the 15th century, each successive generation has been volume of information continues to grow. -

Ladies of the Ticker

By George Robb During the late 19th century, a growing number of women were finding employ- ment in banking and insurance, but not on Wall Street. Probably no area of Amer- ican finance offered fewer job opportuni- ties to women than stock broking. In her 1863 survey, The Employments of Women, Virginia Penny, who was usually eager to promote new fields of employment for women, noted with approval that there were no women stockbrokers in the United States. Penny argued that “women could not very well conduct the busi- ness without having to mix promiscuously with men on the street, and stop and talk to them in the most public places; and the delicacy of woman would forbid that.” The radical feminist Victoria Woodhull did not let delicacy stand in her way when she and her sister opened a brokerage house near Wall Street in 1870, but she paid a heavy price for her audacity. The scandals which eventually drove Wood- hull out of business and out of the country cast a long shadow over other women’s careers as brokers. Histories of Wall Street rarely mention women brokers at all. They might note Victoria Woodhull’s distinction as the nation’s first female stockbroker, but they don’t discuss the subject again until they reach the 1960s. This neglect is unfortu- nate, as it has left generations of pioneering Wall Street women hidden from history. These extraordinary women struggled to establish themselves professionally and to overcome chauvinistic prejudice that a career in finance was unfeminine. Ladies When Mrs. M.E. -

Clearing House Procedures Clearing Member and Dealer Status 1

Clearing House Procedures Clearing Member and Dealer Status SECTION 1 CONTENTS 1.1 APPLICATION PROCEDURE ................................................................ 2 1.2 CRITERIA FOR CLEARING MEMBER STATUS .................................... 4 1.3 DEALER STATUS CRITERIA ................................................................. 9 1.4 EQUITYCLEAR NON-CLEARING MEMBER STATUS ......................... 11 1.5 TURQUOISE DERIVATIVES NON-CLEARING MEMBER STATUS .... 12 1.6 PARTICIPATION IN CROSS-MARGINING AGREEMENTS ................. 12 1.7 EXTENSION OF CLEARING ACTIVITIES............................................ 12 1.8 TERMINATION OF CLEARING MEMBER STATUS ............................ 14 1.9 NET CAPITAL REQUIREMENTS ......................................................... 14 1.10 CALCULATION OF NET CAPITAL ....................................................... 18 1.11 FINANCIAL REPORTING ..................................................................... 19 1.12 ADDITIONAL REQUIREMENTS .......................................................... 21 1.13 OTHER CONDITIONS.......................................................................... 21 LCH.Clearnet Limited © 2012 1 MarchApril 2012 Clearing House Procedures Clearing Member and Dealer Status 1. CLEARING MEMBER, DEALER, EQUITYCLEAR AND TURQUOISE DERIVATIVES NCMs (NON-CLEARING MEMBERS) 1.1 APPLICATION PROCEDURE An application for Clearing Member status of the Clearing House, or for Dealer status (whether as a ForexClear Dealer, RepoClear Dealer or SwapClear Dealer, each