London Stock Exchange Group Response to CCP Resolution Guidance Consultation 2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LIBOR Transition Faqs ‘Big Bang’ CCP Switch Over

RED = Final File Size/Bleed Line BLACK = Page Size/Trim Line MAGENTA = Margin/Safe Art Boundary NOT A PRODUCT OF BARCLAYS RESEARCH LIBOR Transition FAQs ‘Big bang’ CCP switch over 1. When will CCPs switch their rates for discounting 2. €STR Switch Over to new risk-free rates (RFRs)? What is the ‘big bang’ 2a. What are the mechanics for the cash adjustment switch over? exchange? Why is this necessary? As part of global industry efforts around benchmark reform, Each CCP will perform a valuation using EONIA and then run most systemic Central Clearing Counterparties (CCPs) are the same valuation by switching to €STR. The switch to €STR expected to switch Price Aligned Interest (PAI) and discounting discounting will lead to a change in the net present value of EUR on all cleared EUR-denominated products to €STR in July 2020, denominated trades across all CCPs. As a result, a mandatory and for USD-denominated derivatives to SOFR in October 2020. cash compensation mechanism will be used by the CCPs to 1a. €STR switch over: weekend of 25/26 July 2020 counter this change in value so that individual participants will experience almost no ‘net’ changes, implemented through a one As the momentum of benchmark interest rate reform continues off payment. This requirement is due to the fact portfolios are in Europe, while EURIBOR has no clear end date, the publishing switching from EONIA to €STR flat (no spread), however there of EONIA will be discontinued from 3 January 2022. Its is a fixed spread between EONIA and €STR (i.e. -

Euronext Makes Irrevocable Cash Offer to Acquire Lch.Clearnet Sa

CONTACT - Media: CONTACT - Investor Relations: Amsterdam +31.20.721.4488 Brussels +32.2.620.15.50 +33.1.70.48.24.17 Lisbon +351.210.600.614 Paris +33.1.70.48.24.45 EURONEXT MAKES IRREVOCABLE CASH OFFER TO ACQUIRE LCH.CLEARNET SA Euronext has made an irrevocable all-cash offer to LCH.Clearnet Group Limited (“LCH.Clearnet Group”) and London Stock Exchange Group plc (“LSEG”) to acquire LCH.Clearnet SA (“Clearnet”), in relation to which terms and conditions have been agreed. Clearnet has commenced a period of consultation with its works council during which LSEG and LCH.Clearnet Group have granted exclusivity to Euronext Strategic combination to strengthen Euronext at the heart of the Eurozone capital markets: • Strengthening long-term control of clearing activities for Euronext’s markets, while enhancing our ability to innovate • Improving Euronext’s business diversification (post-trade revenue to represent approximately 30% of Euronext’s pro forma revenue) • Providing substantial growth opportunities in Fixed Income and CDS • Acquisition price of €510m (subject to a closing adjustment and including excess capital1) for 100% of Clearnet • Expected pre-tax operating cost synergies of €13m and additional opportunities for revenue synergies Completion of the contemplated transaction is subject to various conditions including: • Closing of the merger between Deutsche Börse AG (“DB”) and LSEG • Euronext shareholder approval • Customary regulatory and anti-trust approvals and other consents • Completion of the works council consultation process of Clearnet Irrespective of the completion of the contemplated transaction, Euronext remains committed to delivering the best long-term solution for its post-trade activities, in the interests of its clients and shareholders Amsterdam, Brussels, Lisbon, London and Paris – 3 January 2017 – Euronext, the leading pan-European exchange in the Eurozone, has signed a binding offer and been granted exclusivity to acquire 100% of the share capital and voting rights of Clearnet. -

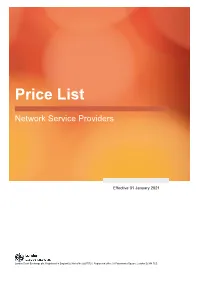

NSP Price List

Network Service Provider Price List For Network Service Providers providing customer access to London Stock Exchange Group Trading and Information Systems Price List Network Service Providers Effective 01 January 2021 London Stock Exchange plc. Registered in England & Wales No 02075721. Registered office 10 Paternoster Square, London EC4M 7LS. Network Service Provider Price List For Network Service Providers providing customer access to London Stock Exchange Group Trading and Information Systems Service Monthly cost per NSP per client per setup*/GBP London Stock Exchange Interactive Services1 1,995 London Stock Exchange Information Services 2,205 London Stock Exchange Testing Only Services2 645 London Stock Exchange Derivatives Market 260 Turquoise Interactive Services1 330 Turquoise Information Services 441 Borsa Italiana Equities 330 Borsa Italiana IDEM Derivatives 330 EuroTLX 330 Notes: 1Includes Trading, Drop-Copy and Post-Trade Gateways, and CDS. 2This service is included for free when ordered with London Stock Exchange Interactive Services or London Stock Exchange Information Services. If you are interested in taking FixHub services, please contact [email protected] for further information. Please note that all services are subject to a 90-day notice period for cancellation. All new services ordered are subject to a minimum 12-month service term. Orders *The ordering and cancellation of services is only supported by an NSP submitting a valid Technical Information Form to [email protected] For more information, please contact our Technology Business Development team on +44 (0)20 7797 3211 or email [email protected] London Stock Exchange plc. Registered in England & Wales No 02075721. Registered office 10 Paternoster Square, London EC4M 7LS. -

Clearing House Procedures Clearing Member and Dealer Status 1

Clearing House Procedures Clearing Member and Dealer Status SECTION 1 CONTENTS 1.1 APPLICATION PROCEDURE ................................................................ 2 1.2 CRITERIA FOR CLEARING MEMBER STATUS .................................... 4 1.3 DEALER STATUS CRITERIA ................................................................. 9 1.4 EQUITYCLEAR NON-CLEARING MEMBER STATUS ......................... 11 1.5 TURQUOISE DERIVATIVES NON-CLEARING MEMBER STATUS .... 12 1.6 PARTICIPATION IN CROSS-MARGINING AGREEMENTS ................. 12 1.7 EXTENSION OF CLEARING ACTIVITIES............................................ 12 1.8 TERMINATION OF CLEARING MEMBER STATUS ............................ 14 1.9 NET CAPITAL REQUIREMENTS ......................................................... 14 1.10 CALCULATION OF NET CAPITAL ....................................................... 18 1.11 FINANCIAL REPORTING ..................................................................... 19 1.12 ADDITIONAL REQUIREMENTS .......................................................... 21 1.13 OTHER CONDITIONS.......................................................................... 21 LCH.Clearnet Limited © 2012 1 MarchApril 2012 Clearing House Procedures Clearing Member and Dealer Status 1. CLEARING MEMBER, DEALER, EQUITYCLEAR AND TURQUOISE DERIVATIVES NCMs (NON-CLEARING MEMBERS) 1.1 APPLICATION PROCEDURE An application for Clearing Member status of the Clearing House, or for Dealer status (whether as a ForexClear Dealer, RepoClear Dealer or SwapClear Dealer, each -

Cameras Corner Crooks

Trans·vestite in pr stitution arrest I Community Newspaper Company allstonbrightontab.com Vol. 10, No. 44 44 Pages • 3 Sections 75¢ R EETMI CAUGHT Cameras corner crooks By Meghann Ackerman an accomplice allegedly held up STAFF WRITER the Market Street Gulf station, hanks to video surveil 195 North Beacon St., at knife lance and cooperating wit point and fled with about $100. Tnesses, police have arrest Working with a witness, police ed three suspects in three said they were able to identify different crimes committed Coleman as a suspect. around Allston and Brighton. Using video surveillance tape A warrant for the arrest of from Brooks Pharmacy, 181 Robert P. Coleman, 27, of 84A Brighton Ave., police were able Dunstable St., Charlestown, was to recover an image of an armed sought for his alleged involve robber who took two shopping ment in a robbery on Feb. 16. Ac bags of money and, according to STAFF PHOTO 8Y DAVID GORDON cording to police, Coleman and CAMERA, 4 Colleen DeRosa, 6, front, In green, a~d hoards of other children from the Our Lady of the Presentatlo School, release balloons during page their vlg11 on Friday. It was the one-year annlvers ry of the kids belni;; locked out of the school by the rchdlocese. The Presentation School Foundation has been trying t, buy the cloMKI bulldlng from ie archdiocese, but has encount red repeated roadblocks. Presentation ralli Fake cop school d ~al near guzzles vodka By Meghann Ackerman datJ n held three day told !he .crowd, gathered under a STAFF WRITER om· year anni\ ersaf) of students being tent to ape the impending ram, that they Drives-through Allston in MBTA cruiser Neither snow nor rain nor heat nor gloom loded out of OLP and to Jebrate 1t:> unity. -

LCH Limited CPMI – IOSCO Self-Assessment 2020

LCH Limited CPMI – IOSCO Self-Assessment 2020 Assessor In 2020, LCH Limited (LCH) performed a self-assessment of its observance with the CPMI-IOSCO Principles for Financial Market Infrastructures (PFMIs). Objective of the assessment LCH’s self-assessment was undertaken in accordance with the PFMIs of April 2012, and supplementary guidance published thereafter, in order to demonstrate compliance with them. Scope of the assessment This self-assessment was made against all PFMIs and supplementary guidance published thereafter which apply to CCPs and covers all the clearing services of LCH. Methodology of the assessment LCH followed the disclosure framework and applied the assessment methodology recommended by CPMI-IOSCO. Source of information in the assessment In making this assessment, LCH used a combination of public and non-public information, including LCH’s policies, procedures and management information. This was also supplemented with discussions with LCH staff responsible for critical activities of the central counterparty. Date of assessment LCH’s assessment was made using data available as of 31st March 2020. 1 Contents 1 Executive Summary .................................................................................................................................. 3 2 Overview of LCH ...................................................................................................................................... 4 3 Detailed assessment report ..................................................................................................................... -

Your Financial Events. Anytime. Anywhere

Your financial events. Anytime. Anywhere. Issuer Services lsegissuerservices.com Live corporate presentations, events and meetings Spark Live offers a unique opportunity to place your content on a trusted website with millions of visitors, so you can maximise the reach of every event in your corporate calendar. With Spark Live, you can offer live and on demand access to your financial results, capital markets days, analyst updates, AGMs and all the important moments in your corporate calendar. Our unique platform lets you integrate your broadcasts into your fully branded London Stock Exchange profile page and open your events to our network of millions. Embed your broadcasts simultaneously into your existing Investor Relations channels to maximise your reach. – Reach millions of investors: through your profile on our trusted portal, your broadcasts are made available to millions of visitors at londonstockexchange.com – Tell your story: enhance your profile page with branding, social media feeds, research and event calendars to support your corporate marketing strategy. – Maximise your content views: investors can view your events in real time or catch up on demand. Wherever and whenever works for them. – Build powerful communications: use our tools to add investor Q&As, slide synching, speaker bios, presentation downloads, transcripts and more. – Broadcast worldwide: broadcast your financial results, capital markets days or analyst updates from any location to increase the reach of every event. Drive visibility, liquidity and demand through -

ELITE Welcomes 20 New UK Companies

Press Release 08 November 2017 ELITE welcomes 20 new UK companies Brings total number of UK ELITE businesses to over 120 ELITE UK CEOs from across the country open London trading More than 660 international companies from across 25 countries make up growing ELITE community London Stock Exchange Group (LSEG) today welcomes 20 new UK companies to its unique business support and capital raising programme, ELITE. This brings the total number of UK companies in the ELITE community to over 120, which includes companies such as online investment management service provider, Nutmeg, British furniture brand, Swoon Editions, and developers of affordable credit card sized computers, Raspberry Pi. Robert Barnes, Global Head of Primary Markets and CEO Turquoise, LSEG, welcomed the new ELITE CEO’s and Kirsty Blackman MP, Aberdeen North and SNP Westminster Deputy Leader and Economy Spokesperson to open trading on London’s markets this morning. Joining the new ELITE cohort are 20 businesses from across the UK, from Oxford to Brighton, including three companies from Aberdeen. Businesses come from across a wide range sectors, from pharmaceuticals to software technology and music. Companies include Northumberland based, Tharsus, a robotics firm that designs the robots used by grocery delivery firm Ocado, life science business, Adaptix, specialised in medical imaging, and state51 Music Group, the first company from the creative music industry to join ELITE. Today the new UK ELITE group brings the total number of businesses in the community to over 660, from across 25 countries and 35 sectors, generating over £45 billion in combined revenues and accounting for over 180,000 jobs across Europe and beyond. -

British American Tobacco Plc (BATS:LN)

British American Tobacco Plc (BATS:LN) Consumer Staples/Tobacco Price: 2,670.50 GBX Report Date: September 23, 2021 Business Description and Key Statistics British American Tobacco is a holding company. Through its Current YTY % Chg subsidiaries, Co. is a multi-category consumer goods company that provides tobacco and nicotine products to consumers around the Revenue LFY (M) 25,776 -0.4 world. Co.'s non-combustible portfolio includes: Vuse and Vype, EPS Diluted LFY 2.79 12.0 glo™, Velo, and Grizzly and Camel Snus. Co.'s combustible portfolio includes: Newport, Natural American Spirit, Camel, Pall Market Value (M) 61,106 Mall, Lucky Strike, Kent, Dunhill Tobacco, and Rothmans. Co. also has a portfolio of international and local brands. These combustible Shares Outstanding LFY (000) 2,288,191 brands include Vogue, Viceroy, 555, Benson and Hedges, Peter Book Value Per Share 27.39 Stuyvesant, Double Happiness, Kool, and Craven A, while oral brands include Granit, Mocca, and Kodiak. EBITDA Margin % 44.30 Net Margin % 24.8 Website: www.bat.com Long-Term Debt / Capital % 36.5 ICB Industry: Consumer Staples Dividends and Yield TTM 2.16 - 7.93% ICB Subsector: Tobacco Payout Ratio TTM % 75.4 Address: Globe House;4 Temple Place London 60-Day Average Volume (000) 2,914 GBR 52-Week High & Low 2,924.00 - 2,448.00 Employees: 89,182 Price / 52-Week High & Low 0.91 - 1.09 Price, Moving Averages & Volume 3,017.2 3,017.2 British American Tobacco Plc is currently trading at 2,670.50 which is 1.1% below its 50 day 2,942.7 2,942.7 moving average price of 2,701.17 and 2.6% below its 2,868.1 2,868.1 200 day moving average price of 2,740.94. -

Kraken First Oil the Enclosed Announcem

FOR IMMEDIATE RELEASE 26 June 2017 CAIRN ENERGY PLC (“Cairn” or “the Company”) Kraken First Oil The enclosed announcement has been reported by EnQuest PLC (70.5% Operator) with regards to the Kraken development in which Cairn has a 29.5% working interest. Enquiries to: Analysts / Investors David Nisbet, Corporate Affairs Tel: 0131 475 3000 Media Linda Bain, Corporate Affairs Tel: 0131 475 3000 Cairn Energy PLC Patrick Handley, David Litterick Tel:0207 404 5959 Brunswick Group LLP NOTES TO EDITORS Cairn is one of Europe's leading independent oil and gas exploration and development companies and is listed on the London Stock Exchange. Cairn has discovered and developed oil and gas reserves in a variety of locations around the world. Cairn’s business operations are now focused on frontier exploration acreage in North West Europe, North West Africa and the North Atlantic, underpinned by interests in development assets in the North Sea. Cairn has its headquarters in Edinburgh, Scotland supported by operational offices in London, Norway and Senegal. Cairn and Corporate Responsibility Cairn is a signatory to the UN Global Compact and our core values of respect, responsibility, relationships and our commitments towards people, the environment and society are enshrined in our Business Principles, which are available on the Cairn website at http://www.cairnenergy.com/index.asp?pageid=282 Cairn became a participating company in the Extractive Industry Transparency Initiative (EITI) in September 2013. The EITI is a coalition of governments, companies and civil society, who have adopted a multi-stakeholder approach to applying the EITI global standard promoting transparency of payments in the oil, gas and mining sectors http://eiti.org/ For further information on Cairn please see: www.cairnenergy.com ENQUEST PLC. -

1 Combined Policy Outcomes of the 7Th China-UK Economic and Financial Dialogue 21 September, 2015 Part I

Combined Policy Outcomes of the 7th China-U.K. Economic and Financial Dialogue 21 September, 2015 Part I: Policy Outcomes Chinese Vice Premier Ma Kai and the UK's Chancellor of the Exchequer George Osborne concluded the meeting of the Seventh China-UK Economic and Financial Dialogue on 21 September, 2015, in Beijing.The UK and China welcome the continued strengthening of bilateral relations. They look forward to a successful State Visit by President Xi Jinping to the UK. The visit will usher in a golden era in relations and provide a platform for the strongest possible political, economic, financial, trade and investment relations and people-to-people exchanges in the decade ahead. I.MacroeconomicSituation and Policies 1. Both sides will continue to strengthen macroeconomic policy coordination, and take appropriate policy measures in line with the development and change of the economic and financial situation at home and abroad, promote strong, balanced and sustainable growth of both countries and global economy. 2. Both sides agree to strengthen cooperation in the G20 and to support G20 as the premier forum for international economic cooperation, and will work together to make G20 Antalya Summit successful. The UK looks forward to and actively supports China successfully hosting the 2016 G20 summit. The two sides commit to fulfilling the commitments made in the previous Summits and meetings of Finance Ministers and Central Bank Governors, working closely together with other G20 members to enhance cooperation in macroeconomic policy to achieve strong, sustainable and balanced growth. 3. China and the UK commit to strengthening their cooperation in the IMF. -

Submission Cover Sheet

SUBMISSION COVER SHEET Confidential Treatment has not been requested Organization Name: Javelin SEF, LLC Organization Type: SEF Registered Entity Identifier: 14-12 Submission Number: 1407-2416-2008-59 Submission Date: 07/24/14 04:20:08 PM Submission Type: Product - 40.2(a) Product Certification Submission Description: July 24, 2014 VIA Electronic Submission Office of the Secretariat Commodity Futures Trading Commission Three Lafayette Centre 1155 21st Street, N.W. Washington, DC 20581 Re: Javelin SEF, LLC Submission No. 14-12 To Whom It May Concern, Javelin SEF, LLC (“Javelin SEF”) hereby notifies the Commodity Futures Trading Commission (the “Commission”), pursuant to Commission Regulation 40.2, of its revised product listing of Javelin SEF interest rate swap products (“LCH IRS Products”) on Javelin SEF beginning July 28, 2014(the “Submission”). Specifically, Javelin SEF is amending its LCH IRS Products to include Package Trades as a new Trade Type1. The Submission contains the following: 1. A summary of the terms of the LCH IRS Products specifications 2. An explanation and analysis of the LCH IRS Products’ compliance with the relevant Core Principles for Swap Execution Facilities (“SEF Core Principles”) as set forth by section 5h of the Commodity Exchange Act; 3. A certification that, concurrent with the filing of the Submission, Javelin SEF posted on its website a notice of pending certification of the LCH IRS Products with the Commission. 1. Summary of Terms of the LCH IRS Products Contract An agreement to exchange one stream of cash flows for another where one stream Overview is based on a floating rate, for a given notional amount over a specified term, and the other stream is based upon either another floating interest rate or a fixed interest rate for the same notional and a given term.