Clean Energy Investing: Global Comparison of Investment Returns

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Crystalline Silicon Photovoltaic Cells, Whether Or Not Assembled Into Modules, from the People's Republic of China

ACCESS C-570-980 Administrative Review POR: 01/01/2017-12/31/2017 Public Document E&C/OVII: GHC January 31, 2020 MEMORANDUM TO: Jeffrey I. Kessler Assistant Secretary for Enforcement and Compliance FROM: James Maeder Deputy Assistant Secretary for Antidumping and Countervailing Duty Operations SUBJECT: Decision Memorandum for the Preliminary Results of the Administrative Review of the Countervailing Duty Order on Crystalline Silicon Photovoltaic Cells, Whether or Not Assembled Into Modules, from the People’s Republic of China; 2017 ______________________________________________________________________________ I. SUMMARY The Department of Commerce is conducting an administrative review of the countervailing duty (CVD) order on crystalline silicon photovoltaic cells, whether or not assembled into modules (solar cells) from the People’s Republic of China (China), covering the period of review (POR) January 1, 2017 through December 31, 2017. The mandatory respondents are JA Solar Technology Yangzhou Co., Ltd. (JA Solar) and Risen Energy Co., Ltd. (Risen Energy). This is the sixth administrative review of the CVD order on solar cells from China. We preliminarily find that JA Solar and Risen Energy received countervailable subsidies during the POR. If these preliminary results are adopted in the final results of this review, we will instruct U.S. Customs and Border Protection (CBP) to assess countervailing duties on all appropriate entries of subject merchandise during the POR. Interested parties are invited to comment on these preliminary results. Unless the deadline is extended pursuant to section 751(a)(3)(A) of the Tariff Act of 1930, as amended (the Act), we will issue the final results of this review by no later than 120 days after the publication of these preliminary results in the Federal Register. -

Borderless, Boundless

Borderless, boundless. 2011 Greater China outbound M&A spotlight Chinese Services Group Contents 1 Foreword 2 Executive summary 4 Methodology 5 Greater China outbound M&A activity 12 Consumer Business & Transportation M&A activity 18 Energy & Resources M&A activity 25 Global Financial Services Industry M&A activity 30 Life Science & Health Care M&A activity 34 Manufacturing M&A activity 40 Technology, Media & Telecommunications M&A activity 46 Private equity M&A activity 54 A view from the other side - a target's perspective of a cross-border M&A deal 57 The impact of the 12th Five Year Plan on outbound M&A opportunities 60 The regulatory roundup 64 Introducing the Chinese Services Group 65 Expanding around the globe… 66 Deloitte's CSG network 67 Contacts 68 Notes Foreword Barclays, IBM, Sony, Tommy Hilfiger and Volvo - all renowned, market-leading champions in their particular fields - and all owned, or partly owned, by a business headquartered in Greater China. As the list goes on, individual names become unimportant. What is of importance is the irrefutable fact that cross-border acquisitions emanating from Greater China have grown of late, not only in stature, as the above can attest to, but also in scope and breadth. The stature of deal-making in this particular market has certainly increased over time. In 2005, less than one-out-of-five (19 percent) transactions were valued at more than US$250m. Over the first six months of 2011, this proportion rose to 27 percent, with the market's growing maturity also evident from a global standpoint. -

Countervailing Duty Administrative (NAICS 621) About Telemedicine Solar Cells from China

Federal Register / Vol. 85, No. 237 / Wednesday, December 9, 2020 / Notices 79163 service delivery for the healthcare DEPARTMENT OF COMMERCE days.2 On July 21, 2020, Commerce industry, and its importance has tolled the due date for these final results increased during the current pandemic. International Trade Administration an additional 60 days.3 On September 25, 2020, Commerce extended the Expanding the collection of data on [C–570–980] telemedicine use will support deadline for issuing the final results of measurement on changes in its adoption Crystalline Silicon Photovoltaic Cells, this review by 60 days, until November 4 during this unprecedented public health Whether or Not Assembled Into 27, 2020. emergency. SAS currently asks Modules, From the People’s Republic Scope of the Order of China: Final Results of ambulatory health care providers The products covered by the order are Countervailing Duty Administrative (NAICS 621) about telemedicine solar cells from China. A full Review; 2017 services in relation to patient visits. description of the scope of the order is This proposal will add a question about AGENCY: Enforcement and Compliance, contained in the Issues and Decision revenues from telemedicine services for International Trade Administration, Memorandum.5 hospitals (NAICS 622) and nursing Department of Commerce. homes (NAICS 623). Furthermore, to Analysis of Comments Received SUMMARY: The Department of Commerce standardize content across industries All issues raised in interested parties’ (Commerce) determines that and provide consistency for briefs are addressed in the Issues and countervailable subsidies are being respondents, the current telemedicine Decision Memorandum accompanying provided to producers/exporters of this notice. -

Q2/Q3 2020 Solar Industry Update

Q2/Q3 2020 Solar Industry Update David Feldman Robert Margolis December 8, 2020 NREL/PR-6A20-78625 Executive Summary Global Solar Deployment PV System and Component Pricing • The median estimate of 2020 global PV system deployment projects an • The median residential quote from EnergySage in H1 2020 fell 2.4%, y/y 8% y/y increase to approximately 132 GWDC. to $2.85/W—a slower rate of decline than observed in any previous 12- month period. U.S. PV Deployment • Even with supply-chain disruptions, BNEF reported global mono c-Si • Despite the impact of the pandemic on the overall economy, the United module pricing around $0.20/W and multi c-Si module pricing around States installed 9.0 GWAC (11.1 GWDC) of PV in the first 9 months of $0.17/W. 2020—its largest first 9-month total ever. • In Q2 2020, U.S. mono c-Si module prices fell, dropping to their lowest • At the end of September, there were 67.9 GWAC (87.1 GWDC) of solar PV recorded level, but they were still trading at a 77% premium over global systems in the United States. ASP. • Based on EIA data through September 2020, 49.4 GWAC of new electric Global Manufacturing generating capacity are planned to come online in 2020, 80% of which will be wind and solar; a significant portion is expected to come in Q4. • Despite tariffs, PV modules and cells are being imported into the United States at historically high levels—20.6 GWDC of PV modules and 1.7 • EIA estimates solar will install 17 GWAC in 2020 and 2021, with GWDC of PV cells in the first 9 months of 2020. -

Crystalline Silicon Photovoltaic Cells, Whether Or Not Assembled Into Modules, from the People’S Republic of China

A-570-979 Administrative Review POR: 12/1/2014 - 11/30/2015 Public Document E&C/IV: KH, JP, MK, EL DATE: June 20, 2017 MEMORANDUM TO: Ronald K. Lorentzen Acting Assistant Secretary for Enforcement and Compliance FROM: James Maeder Senior Director, Office I Antidumping and Countervailing Duty Operations Enforcement and Compliance SUBJECT: Issues and Decision Memorandum for the Final Results of the 2014-2015 Antidumping Duty Administrative Review of Crystalline Silicon Photovoltaic Cells, Whether or Not Assembled into Modules, From the People’s Republic of China SUMMARY On December 22, 2016, the Department of Commerce (the Department) published its Preliminary Results in the 2014-2015 administrative review of the antidumping duty order of crystalline silicon photovoltaic cells, whether or not assembled into modules (solar cells) from the People’s Republic of China (PRC).1 The period of review (POR) is December 1, 2014, through November 30, 2015. This administrative review covers two mandatory respondents: (1) Canadian Solar International Limited, which we have treated as a single entity with five affiliated additional companies (collectively, Canadian Solar);2 and (2) Trina Solar, consisting of 1 See Crystalline Silicon Photovoltaic Cells, Whether or Not Assembled Into Modules, From the People’s Republic of China: Preliminary Results of Antidumping Duty Administrative Review and Preliminary Determination of No Shipments; 2014–2015, 81 FR 93888 (December 22, 2016) (Preliminary Results), and accompanying Preliminary Decision Memorandum (PDM). 2 The Department has continued to treat the following six companies as a single entity: Canadian Solar International Limited/Canadian Solar Manufacturing (Changshu), Inc./Canadian Solar Manufacturing (Luoyang), Inc./CSI Cells Co., Ltd./CSI-GCL Solar Manufacturing (YanCheng) Co., Ltd./CSI Solar Power (China) Inc. -

SEIA BOARD FACEBOOK *Updated March 2016

SEIA BOARD FACEBOOK *Updated March 2016 8MINUTENERGY RENEWABLES, LLC 8minutenergy Renewables, LLC is one of the country's leading developers of ground- mounted solar PV projects, with a portfolio of more than 2,000 megawatts (MW) of solar PV power plant projects. Martin Hermann Board At-Large CEO & Founder Serial entrepreneur with 24 years of experience in the solar, clean-tech and high- tech industries, Developed a 100MW solar PV module manufacturing plant as Chief Strategy Officer with Advent Solar. Arthur Haubenstock Board Alternate General Counsel and Vice President, Government & Regulatory ALLEARTH RENEWABLES, INC. AllEarth Renewables – an Inc. 500 recognized company -- is the designer and manufacturer of the AllSun Tracker, a complete grid-tied, dual-axis solar electric system that uses GPS technology to follow the sun, producing up to 45% more energy than fixed rooftop systems. Made in the U.S.A, the ground-mounted solar tracker has a 120 mph wind rating, 10-year warranty, and is designed for residential and commercial-scale installations. Andrew Savage Elected Director Chief Strategy Officer Served as deputy chief of staff, legislative director and communications director for Vermont Congressman Peter Welch. Chief Strategy Officer at AllEarth Renewables, manufacturer of the AllSun Tracker. Part of President Barack Obama’s successful 2008 presidential primary campaign team Andrew received his bachelor’s degree in political science and environmental studies from Middlebury College graduating summa cum laude. AZTEC SOLAR INC. Aztec Solar is a full-service solar energy provider, including Solar Thermal, Solar AC and Solar Photovoltaic systems for both residential sites and commercial businesses. Aztec offers in-house solar water heating, solar pool heating and solar electric power. -

FTSE Publications

2 FTSE Russell Publications FTSE Developed Asia Pacific ex 19 August 2021 Japan ex Controversies ex CW Index Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) a2 Milk 0.1 NEW CJ Cheiljedang 0.1 KOREA GPT Group 0.22 AUSTRALIA ZEALAND CJ CheilJedang Pfd. 0.01 KOREA Green Cross 0.05 KOREA AAC Technologies Holdings 0.16 HONG KONG CJ Corp 0.04 KOREA GS Engineering & Construction 0.07 KOREA ADBRI 0.04 AUSTRALIA CJ ENM 0.05 KOREA GS Holdings 0.06 KOREA Afterpay Touch Group 0.61 AUSTRALIA CJ Logistics 0.04 KOREA GS Retail 0.04 KOREA AGL Energy 0.12 AUSTRALIA CK Asset Holdings 0.5 HONG KONG Guotai Junan International Holdings 0.01 HONG KONG AIA Group Ltd. 4.6 HONG KONG CK Hutchison Holdings 0.64 HONG KONG Haitong International Securities Group 0.02 HONG KONG Air New Zealand 0.02 NEW CK Infrastructure Holdings 0.11 HONG KONG Hana Financial Group 0.36 KOREA ZEALAND Cleanaway Waste Management 0.08 AUSTRALIA Hang Lung Group 0.07 HONG KONG ALS 0.14 AUSTRALIA CLP Holdings 0.5 HONG KONG Hang Lung Properties 0.15 HONG KONG Alteogen 0.06 KOREA Cochlear 0.37 AUSTRALIA Hang Seng Bank 0.44 HONG KONG Altium 0.09 AUSTRALIA Coles Group 0.5 AUSTRALIA Hanjin KAL 0.04 KOREA Alumina 0.1 AUSTRALIA ComfortDelGro 0.08 SINGAPORE Hankook Technology Group 0.1 KOREA Amcor CDI 0.54 AUSTRALIA Commonwealth Bank of Australia 4.07 AUSTRALIA Hanmi Pharmaceutical 0.06 KOREA AmoreG 0.05 KOREA Computershare 0.21 AUSTRALIA Hanmi Science 0.03 KOREA Amorepacific Corp 0.21 KOREA Contact Energy 0.14 NEW Hanon Systems 0.07 KOREA Amorepacific Pfd. -

Q4 2018 / Q1 2019 Solar Industry Update

Q4 2018/Q1 2019 Solar Industry Update David Feldman Robert Margolis May 2019 NREL/PR-6A20-73992 Executive Summary • At the end of 2018, global PV installations reached 509 GW-DC, • The United States installed 10.7 GW-DC of PV in 2018 (8.3 GW- an annual increase of 102 GW-DC from 2017. AC), with 4.2 GW-DC coming in Q4—cumulative capacity reached 62.5 GW-DC (49.7 GW-AC). – In 2018, the leading markets in terms of annual deployment were China (44 GW-DC), the United States (11 GW-DC), and – Analysts also expect U.S. PV capacity to double by 2022. India (8 GW-DC). • In 2018, global PV shipments were approximately 89 GW—a Analysts expect cumulative PV capacity to double by 2022. – decrease of 5% from 2017. More than 96% of those PV shipments used c-Si technology and were shipped from Asian • At the end of 2018, cumulative global CSP installations reached countries. 6.2 GW, up 710 MW from 2017. • In 2018, the United States produced approximately 1 GW of c-Si • Solar installations represented 22% of all new U.S. electric modules and 0.4 GW of thin film. generation capacity in 2018—second to natural gas (58%). – The United States expanded its PV manufacturing capacity • In 2018, solar represented 4.6% of net summer capacity and to 6 GW in Q1 2019 (up from 2.5 GW in 2017), and it is 2.3% of annual net generation. expected to add another 3 GW in the near future. -

Solar Photovoltaic Manufacturing: Industry Trends, Global Competition, Federal Support

U.S. Solar Photovoltaic Manufacturing: Industry Trends, Global Competition, Federal Support Michaela D. Platzer Specialist in Industrial Organization and Business January 27, 2015 Congressional Research Service 7-5700 www.crs.gov R42509 U.S. Solar PV Manufacturing: Industry Trends, Global Competition, Federal Support Summary Every President since Richard Nixon has sought to increase U.S. energy supply diversity. Job creation and the development of a domestic renewable energy manufacturing base have joined national security and environmental concerns as reasons for promoting the manufacturing of solar power equipment in the United States. The federal government maintains a variety of tax credits and targeted research and development programs to encourage the solar manufacturing sector, and state-level mandates that utilities obtain specified percentages of their electricity from renewable sources have bolstered demand for large solar projects. The most widely used solar technology involves photovoltaic (PV) solar modules, which draw on semiconducting materials to convert sunlight into electricity. By year-end 2013, the total number of grid-connected PV systems nationwide reached more than 445,000. Domestic demand is met both by imports and by about 75 U.S. manufacturing facilities employing upwards of 30,000 U.S. workers in 2014. Production is clustered in a few states including California, Ohio, Oregon, Texas, and Washington. Domestic PV manufacturers operate in a dynamic, volatile, and highly competitive global market now dominated by Chinese and Taiwanese companies. China alone accounted for nearly 70% of total solar module production in 2013. Some PV manufacturers have expanded their operations beyond China to places like Malaysia, the Philippines, and Mexico. -

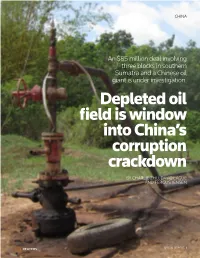

Depleted Oil Field Is Window Into China's Corruption Crackdown

CHINA An $85 million deal involving three blocks in southern Sumatra and a Chinese oil giant is under investigation. Depleted oil field is window into China’s corruption crackdown BY CHARLIE ZHU, DAVID LAGUE AND FERGUS JENSEN SPECIAL REPORT 1 CHINA CORRUPTION CRACKDOWN LIMAU, INDONESIA, DECEMBER 19, 2014 n a muddy clearing in southern Sumatra, a portable diesel power plant hammers Iaway alongside a wellhead, struggling to extract crude from a depleted reservoir that lies below farmland and rubber plantations. It was much easier to extract cash from a state-owned Chinese oil giant. A subsidiary of China National Petroleum Corporation (CNPC), PetroChina Daqing Oilfield, paid $85 million to pump from three blocks in the ageing Limau field un- der a 2013 contract with Indonesia’s state- owned oil company, Pertamina, according to senior Chinese oil industry officials with knowledge of the transaction. Today, the three Limau blocks squeeze PETRO PURGE: At least a dozen former top managers at China National Petroleum Corporation have out less than three percent of the oil been arrested as part of President Xi Jinping’s anti-corruption drive. Zhou Yongkang (below), a former pumped when output peaked in the 1960s. CNPC boss and rival to Xi, faces charges of corruption and leaking state secrets. A wellhead atop the When PetroChina Daqing announced the depleted Limau field in Indonesia (cover). REUTERS/BOGDAN CRISTEL/JASON LEE/FERGUS JENSEN deal, it didn’t disclose the seller, the price or any other financial details. “We all know it is a ridiculous invest- ment, but I have no idea where the mon- ey has actually ended up,” says a senior billion Chinese oil industry official who has seen $25 The amount that CNPC spent on budget figures for the Limau wells. -

Greater China Oil & Gas M&A and Greenfield FDI Investment Spotlight

Greater China Oil & Gas M&A and greenfield FDI investment spotlight 2013 edition M&A Services 1 Contents Introduction .............................................................................................................................................................. 3 Methodology ............................................................................................................................................................. 4 Global Oil & Gas M&A and greenfield investment activity .................................................................................. 5 Greenfield Oil & Gas investment increasingly giving way to M&A activity across the globe ................................... 6 Where is this investment going? .............................................................................................................................. 6 The Greater China angle .......................................................................................................................................... 8 Foreign investments into China's Oil & Gas sector ................................................................................................. 9 Domestic investment activity in China's Oil & Gas sector ..................................................................................... 11 Greater China's Oil & Gas investments overseas ................................................................................................. 13 Looking forward – Potential deal opportunities and investment themes ....................................................... -

Asia Infrastructure, Energy and Natural Resources (IEN)

Asia Infrastructure, Energy and Natural Resources (IEN) Slaughter and May is a leading international firm with a worldwide corporate, commercial and financing practice. We provide clients with a professional service of the highest quality combining technical excellence and commercial awareness and a practical, constructive approach to legal services. We advise on the full range of matters for infrastructure, energy and natural resources clients in Asia, including projects, mergers and acquisitions, all forms of financing, competition and regulatory, tax, commercial, trading, construction, operation and maintenance contracts as well as general commercial and corporate advice. Our practice is divided into three key practice areas: – Infrastructure – rail and road; ports and airports; logistics; water and waste management. – Energy – power and renewables; oil and gas. – Mining and Minerals – coal, metals and minerals. For each regional project we draw on long‑standing relationships with leading independent law firms in Asia. This brings together individuals from the relevant countries to provide the optimum legal expertise for that particular transaction. This allows us to deliver a first class pan‑Asian and global seamless legal service of the highest quality. Recommended by clients for project agreements and ‘interfacing with government bodies’, Slaughter and May’s team is best-known for its longstanding advice to MTR on some of Hong Kong’s key infrastructure mandates. Projects and Energy – Legal 500 Asia Pacific Infrastructure – rail MTR Corporation Limited – we have advised the • Tseung Kwan O Line: The 11.9‑kilometre MTR Corporation Limited (MTR), a long‑standing Tseung Kwan O Line has 8 stations and links client of the firm and one of the Hong Kong office’s the eastern part of Hong Kong Island with the first clients, on many of its infrastructure and eastern part of Kowloon other projects, some of which are considered to be amongst the most significant projects to be • Disney Resort Line: The 3.3‑kilometre Disney undertaken in Hong Kong.