Tipping Points and the Local Housing Market

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

מכון ירושלים לחקר ישראל Jerusalem Institute for Israel Studies שנתון

מכון ירושלים לחקר ישראל Jerusalem Institute for Israel Studies שנתון סטטיסטי לירושלים Statistical Yearbook of Jerusalem 2016 2016 לוחות נוספים – אינטרנט Additional Tables - Internet לוח ג/19 - אוכלוסיית ירושלים לפי קבוצת אוכלוסייה, רמת הומוגניות חרדית1, רובע, תת-רובע ואזור סטטיסטי, 2014 Table III/19 - Population of Jerusalem by Population Group, Ultra-Orthodox Homogeneity Level1, Quarter, Sub-Quarter, and Statistical Area, 2014 % רמת הומוגניות חרדית )1-12( סך הכל יהודים ואחרים אזור סטטיסטי ערבים Statistical area Ultra-Orthodox Jews and Total homogeneity Arabs others level )1-12( ירושלים - סך הכל Jerusalem - Total 10 37 63 849,780 רובע Quarter 1 10 2 98 61,910 1 תת רובע 011 - נווה יעקב Sub-quarter 011 - 3 1 99 21,260 Neve Ya'akov א"ס .S.A 0111 נווה יעקב )מזרח( Neve Ya'akov (east) 1 0 100 2,940 0112 נווה יעקב - Neve Ya'akov - 1 0 100 2,860 קרית קמניץ Kiryat Kamenetz 0113 נווה יעקב )דרום( - Neve Ya'akov (south) - 6 1 99 3,710 רח' הרב פניז'ל, ,.Harav Fenigel St מתנ"ס community center 0114 נווה יעקב )מרכז( - Neve Ya'akov (center) - 6 1 99 3,450 מבוא אדמונד פלג .Edmond Fleg St 0115 נווה יעקב )צפון( - 3,480 99 1 6 Neve Ya'akov (north) - Meir Balaban St. רח' מאיר בלבן 0116 נווה יעקב )מערב( - 4,820 97 3 9 Neve Ya'akov (west) - Abba Ahimeir St., רח' אבא אחימאיר, Moshe Sneh St. רח' משה סנה תת רובע 012 - פסגת זאב צפון Sub-quarter 012 - - 4 96 18,500 Pisgat Ze'ev north א"ס .S.A 0121 פסגת זאב צפון )מערב( Pisgat Ze'ev north (west) - 6 94 4,770 0122 פסגת זאב צפון )מזרח( - Pisgat Ze'ev north (east) - - 1 99 3,120 רח' נתיב המזלות .Netiv Hamazalot St 0123 -

T S Form, 990-PF Return of Private Foundation

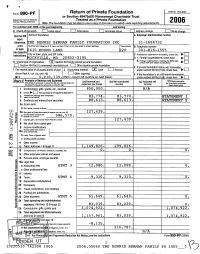

t s Form, 990-PF Return of Private Foundation OMB No 1545-0052 or Section 4947(a)(1) Nonexempt Charitable Trust Department of the Treasury Treated as a Private Foundation Internal Revenue service Note. The foundation may be able to use a copy of this return to satisfy state report! 2006 For calendar year 2006, or tax year beginning , and ending G Check all that a Initial return 0 Final return Amended return Name of identification Use the IRS foundation Employer number label. Otherwise , HE DENNIS BERMAN FAMILY FOUNDATION INC 31-1684732 print Number and street (or P O box number if mail is not delivered to street address) Room/suite Telephone number or type . 5410 EDSON LANE 220 301-816-1555 See Specific City or town, and ZIP code C If exemption application is pending , check here l_l Instructions . state, ► OCKVILLE , MD 20852-3195 D 1. Foreign organizations, check here Foreign organizations meeting 2. the 85% test, ► H Check type of organization MX Section 501(c)(3) exempt private foundation check here and attach computation = Section 4947(a)(1) nonexempt chartable trust 0 Other taxable private foundation E If private foundation status was terminated I Fair market value of all assets at end of year J Accounting method 0 Cash Accrual under section 507(b)(1)(A), check here (from Part ll, col (c), line 16) 0 Other (specify) F If the foundation is in a 60-month termination $ 5 010 7 3 9 . (Part 1, column (d) must be on cash basis) under section 507 (b)( 1 ► )( B ) , check here ► ad 1 Analysis of Revenue and Expenses ( a) Revenue and ( b) Net investment (c) Adjusted net ( d) Disbursements (The total of amounts in columns (b), (c), and (d) may not for chartable purposes necessary equal the amounts in column (a)) expenses per books income income (cash basis only) 1 Contributions , gifts, grants , etc , received 850,000 . -

Zvi Hecker Press

About Distributors Online Issues Printed Issues Shoot the Breeze Store Video Rachel de Joode Various Qualities To Orbit The Mysterious Core, 2013 Interview by Whitney Mallett When I went to visit Rachel de Joode in her studio this Fall, she said we were going to try making a “squish.” This process consisted of filling a plastic tube with wet plaster and me hugging it likeuncube, a lover ,January leaving a 2016n imprint of my body, until it dried. About Distributors Online Issues Printed Issues Shoot the Breeze Store Video Rachel de Joode With the changes in Israeli society that followed the 1967 Six-Day War – during which Israel conquered the West Bank, Sinai Peninsula and Golan Heights, thus more than doubling its size – came massive urban expansion and architecture of a new kind. Rafi Segal traces how the design and construction of a single project, Zvi Hecker’s Ramot Polin housing complex on the outskirts of Jerusalem, came to embody and yet defy this nationwide change. The unification of Jerusalem under Israeli control in 1967 prompted a national building project of urban expansion through the construction of new neighbourhoods and settlements on Jerusalem’s surrounding hilltops. These aspired to echo the historic architecture of the old city of Jerusaem and thus establish a direct visual connection between the old and the new. The resulting architectural style of stone façades, arches and other “old Jerusalem” vernacular elements was so dominant that in some cases it led to the dressing of modernist pre-fabricated concrete slab buildings with local stone and arches. -

Jerusalem: Facts and Trends

JE R U S A L E M JERUSALEM INSTITUTE : F FOR ISRAEL STUDIES A C T Jerusalem: Facts and Trends oers a concise, up-to-date picture of the S A N current state of aairs in the city as well as trends in a wide range of D T R areas: population, employment, education, tourism, construction, E N D and more. S The primary source for the data presented here is The Statistical 2014 Yearbook of Jerusalem, which is published annually by the Jerusalem JERUSALEM: FACTS AND TRENDS Institute for Israel Studies and the Municipality of Jerusalem, with the support of the Jerusalem Development Authority (JDA) and the Leichtag Family Foundation (United States). Michal Choshen, Korach Maya The Jerusalem Institute for Israel Studies (JIIS), founded in 1978, Maya Choshen, Michal Korach is a non-prot institute for policy studies. The mission of JIIS is to create a database, analyze trends, explore alternatives, and present policy recommendations aimed at improving decision-making processes and inuencing policymaking for the benet of the general public. The main research areas of JIIS are the following: Jerusalem studies in the urban, demographic, social, economic, physical, and geopolitical elds of study; Policy studies on environmental issues and sustainability; Policy studies on growth and innovation; The study of ultra-orthodox society. Jerusalem Institute 2014 for Israel Studies The Hay Elyachar House 20 Radak St., Jerusalem 9218604 Tel.: +972-2-563-0175 Fax: +972-2-563-9814 Email: [email protected] Website: www.jiis.org 438 Board of Directors Jerusalem Institute for Israel Studies Dan Halperin, Chairman of the Board Avraham Asheri David Brodet Ruth Cheshin Prof. -

Jerusalem: Facts and Trends 2013

Jerusalem Institute for Israel Studies Founded by the Charles H. Revson Foundation Jerusalem: Facts and Trends 2013 Maya Choshen Michal Korach Inbal Doron Yael Israeli Yair Assaf-Shapira 2013 Publication Number 427 Jerusalem: Facts and Trends 2013 Maya Choshen, Michal Korach, Inbal Doron, Yael Israeli, Yair Assaf-Shapira © 2013, The Jerusalem Institute for Israel Studies The Hay Elyachar House 20 Radak St., 92186 Jerusalem http://www.jiis.org Table of Contents About the authors .......................................................................................................... 5 Preface ............................................................................................................................. 6 Area ................................................................................................................................. 7 Population ....................................................................................................................... 7 Population size .................................................................................................................. 7 Geographic distribution of the population ........................................................................ 9 Population growth ............................................................................................................. 9 Age of the population ...................................................................................................... 10 Sources of Population Growth ................................................................................... -

Israeli Archaeological Activity in the West Bank 1967–2007

ISRAELI ARCHAEOLOGICAL ACTIVITY IN THE WEST BANK 1967–2007 A SOURCEBOOK RAPHAEL GREENBERG ADI KEINAN THE WEST BANK AND EAST JERUSALEM ARCHAEOLOGICAL DATABASE PROJECT © 2009 Raphael Greenberg and Adi Keinan Cover: Surveying in western Samaria, early 1970s (courtesy of Esti Yadin) Layout: Dina Shalem Production: Ostracon Printed by Rahas Press, Bar-Lev Industrial Park, Israel Distributed by Emek Shaveh (CPB), El‘azar Hamoda‘i 13, Jerusalem [email protected] ISBN 978-965-91468-0-2 CONTENTS FOREWORD 1 PART 1. HISTORICAL BACKGROUND, ARCHAEOLOGICAL SURVEYS AND EXCAVATIONS IN THE WEST BANK SINCE 1967 Introduction 3 Israeli Archaeology in the West Bank 3 Note on Palestinian Archaeology in the West Bank 7 Israeli Archaeology in East Jerusalem 8 Conclusion 10 PART 2. CONSTRUCTING THE DATABASE A. Surveys 11 Survey Motivation and Design 12 Survey Method 12 Definition of Sites 13 Site Names 14 Dating 14 Survey Database Components 15 B. Excavations 18 Basic Data on Excavations 19 The Excavation Gazetteer 20 Excavated Site Types and Periods 21 C. GIS Linkage and Its Potential 22 Case No. 1: The Iron Age I Revisited 23 Case No. 2: Roman Neapolis 26 Case No. 3: An Inventory of Mosaic Floors 26 D. Database Limitations 28 Concluding Remarks 29 References (for Parts 1 and 2) 30 PART 3. GAZETTEER OF EXCAVATIONS, 1967–2007 33 PART 4. BIBLIOGRAPHY 151 PART 5. INDEX OF EXCAVATED SITES 173 PART 6. DATABASE FILES (on CD only) FOREWORD The authors will be the first to concede that modern been subsumed in a particular view of Jerusalem’s political boundaries—the Green Line, the Separation significance in history. -

Return of Private Foundation

l efile GRAPHIC p rint - DO NOT PROCESS As Filed Data - DLN: 93491225004093 Return of Private Foundation OMB No 1545-0052 Form 990 -PF or Section 4947( a)(1) Nonexempt Charitable Trust Treated as a Private Foundation Department of the Treasury 2012 Note . The foundation may be able to use a copy of this return to satisfy state reporting requirements Internal Revenue Service • . For calendar year 2012 , or tax year beginning 01-01-2012 , and ending 12-31-2012 Name of foundation A Employer identification number THE DENNIS BERMAN FAMILY FOUNDATION INC 31-1684732 ieiepnone number ( see instructions) Number and street ( or P 0 box number if mail is not delivered to street address ) Room/suite U 5410 EDSON LANE NO 220 (301) 816-1555 City or town, state, and ZIP code C If exemption application is pending, check here F ROCKVILLE, MD 208523195 G Check all that apply r'Initial return r'Initial return of a former public charity D 1. Foreign organizations , check here (- r-Final return r'Amended return 2. Foreign organizations meeting the 85% test, r Address change r'Name change check here and attach computation H Check type of organization FSection 501( c)(3) exempt private foundation r'Section 4947( a)(1) nonexempt charitable trust r'Other taxable private foundation J Accounting method F Cash F Accrual E If private foundation status was terminated I Fair market value of all assets at end und er section 507 ( b )( 1 )( A ), c hec k here F of y e a r (from Part 77, col. (c), Other ( specify) _ F If the foundation is in a 60-month termination line -

Return of Private Foundation Form 990-PF I

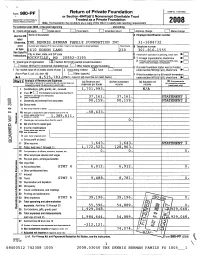

Return of Private Foundation OMB No 1545-0052 Form 990-PF I • or Section 4947(a)(1) Nonexempt Charitable Trust Department of the Treasury Treated as a Private Foundation Internal Revenue Service Note. The foundation may be able to use a copy of this return to satisfy state reporting requirements 2 00 8 For calendar year 2008 , or tax year beginning , and ending R ('hark au that annh, F__l Ind,sl return F__] 9:m2l rahirn I-1 e,nonnorl ratnrn 1 1 Adrlrocc nhanno hI,mn ,.h^nno Name of Use the IRS foundation A Employer identification number label Otherwise , HE DENNIS BERMAN FAMILY FOUNDATION INC 31-1684732 print Number and street (or P 0 box number if mail is not delivered to street address) Room/suite B Telephone number or type . 5410 EDSON LANE 220 301-816-1555 See Specific City or town, state , and ZIP code Instructions . C If exemption application is pending , check here OCKVILLE , MD 20852-319 5 D 1- Foreign organizations , check here ► 2. Foreignrganrzatac meetingthe85%test, H Check tYPtype oorganization 0X Section 501 (c)( 3 ) exempt Pprivate foundation check heere and atttach computation Section 4947(a )( 1 nonexempt charitable trust 0 Other taxable p rivate foundation E If private foun dation status was termina ted I Fair market value of all assets at end of year J Accounting method OX Cash Accrual under section 507(b)(1)(A), check here (from Part Il, col (c), line 16) = Other (specify ) F If the foundation is in a 60-month termination (Part I, column (d) must be on cash basis) ► $ 4 , 515 , 783 . -

Israel Als Laboratorium Moderner Architektur Rhz-Architekturreise Israel Vom 29

Israel als Laboratorium moderner Architektur rhz-Architekturreise Israel vom 29. März. bis 06. April 2014 Die Entstehung und Entwicklung des Staates Israel stellt eines der effizientesten und umfassendsten architektonischen Projekte der Moderne dar - ein Experiment, das die Anlage einer künstlichen Landschaft ebenso umfasste wie den Bau Dutzender neuer Städte und Siedlungen. Israel zeigt die Entstehungsbedingungen der Nachkriegsarchitektur auf: die Beziehung zwischen Ideologie und architektonischer Form, die räumlichen Organisation des Wohlfahrtsstaats, das Verhältnis von militärischer und ziviler Gesellschaft und schliesslich die typologischen Paradigmata der Architektur. Sonnenaufgang 05.45, Sonnenuntergang 17.45 1. Samstag 29. März Anreise und und erster Spaziergang zum Kennenlernen Hinreise Zürich Flughafen nach Tel Aviv Treffpunkt 08.25 Zürich Flughafen vor dem Abflug Gate 09.45 ZHR LX 254 Y 14.40 TLV 15:30 Transfer mit Bus nach Tel Aviv (Anfahrt 0.5 h) 16.00 Check-In Cinema Hotel, Tel Aviv http://www.atlas.co.il/deutsch/cinema-hotel-tel-aviv/ Das Cinema Hotel, nur ein kurzer Spaziergang vom Strand entfernt ist ein Originalbau im Tel Aviv: Jaffa Bauhaus-Stil, eines der ersten Kinos im Herzen von Tel Aviv. Das Cinema Hotel verfügt über eine wunderschöne Dachterrasse mit Blick über den Dizengoff-Platz. 16.30 Nachmittag/Abend: Jaffa, einer der ältesten Hafen der Welt (zu Fuss) Der erste Stadtspaziergang führt Sie zum Hafen von Jaffa. Die Altstadt, ein Kleinod mittelalterlicher Stadtbaukunst, war Ende des 19. Jahrhunderts ein Problem für die vielen jüdischen Einwanderer, da sie keine Möglichkeit zur baulichen Expansion bot und die Bevölkerung auf immer engerem Raum unterkommen musste, was zum Beginn der jüdischen Besiedlungen ausserhalb der Städte führte Abendessen 20.00 gemeinsam Restaurant Abrage in Jaffo Übernachtung Cinema Hotel, Tel Aviv (1) 2. -

Hot Pants in Hollywood Will Entertain with Stories of Life As a Jewish, Female Comedy Writer in Hollywood

www.JewishFederationLCC.org Vol. 40, No. 7 n March 2018 / 5778 “Covenant With Israel” celebration mindfulness. bers and leaders of other FROM THE Now, one doesn’t Christian churches from EXECUTIVE need to react in these ways Lee, Charlotte and Col- in order to love Israel. lier counties. Also at- DIRECTOR These reflexive actions tending was the Deputy n Alan Isaacs are probably attributable Consul General of Israel to growing up in a certain from the Miami consul- elebrating Israel, her mean- environment where Israel and, more ate as well as other lu- ing and accomplishments, has importantly, when Israel mattered in minaries from Israel and Cchanged over the years – just very different ways than it does today. the U.S. “Covenant With Israel” celebration at Word of Life Ministries as Israel has changed. And just as ev- Many who love Israel have come This annual event, erything seems more complex today, to do so through study of the Bible and now in its 10th year, un- so does Israel and how to celebrate her the teachings of their spiritual leaders; derscores the commit- existence. in some cases as a revelation. Their ment that this evangeli- To some of us, Israel is with us, commitment to Israel and her people, cal Christian community in our consciousness, routinely. We indeed, all Jewish people, emanates feels toward Israel and skim articles online or on paper, and from a devotion to their faith. the support that they are if we skim the word “Israel” we in- On January 29, I spent the evening ready to give, and al- stinctively stop skimming, to read. -

Veolia Fact File

Urban District Haaglanden: Veolia-transport undesirable and unacceptable in city of peace and justice From: - United Civilians for Peace (Cooperation between Cordaid, ICCO, IKV Pax Christi, Oxfam Novib) - Another Jewish Voice To: - Urban District Haaglanden Re: - Fact file Veolia Date: - April 19, 2012 1. Introduction The French multinational Veolia Environment1 („Veolia‟) is possibly contributing to violation of international law including the Geneva Conventions and discriminates Palestinians concerning its activities in Israel / the occupied Palestinian territories as shown in the fact file presented below and the accompanying legal opinion.2 Based on these facts, Veolia has to be excluded from participation in the tender procedure for the concession „public transport bus Haaglanden-city‟. 2. Veolia: The facts 2.1 Jerusalem Light Rail project (JLR) The Jerusalem Light Rail project connects West-Jerusalem with a number of Jewish settlements in and around occupied (and illegally annexed) Palestinian East-Jerusalem. The establishment of settlements is illegal under international law. The JLR is part of the „Jerusalem Transportation Master Plan‟, drawn up by the Israeli Government in March 1996.3 The City Pass Consortium consists of Veolia (Veolia Transport Israel), Alstom, two Israeli companies and the Israeli banks Hapaolim and Leumi. In 2002, this Consortium won the tender of the Israeli Government for the construction, maintenance and exploitation of the JLR as well as the 1Veolia Environment is the name of the parent company and consists of 4 divisions: Transport, Water, Energy and Environmental Services. In March 2011, Veolia Transport merged with Transdev in VeoliaTransdev, still a division of Veolia Environment. 2 See Annex 1: Legal opinion. -

Return of Private Foundation 14 2, 6

Return of Private Foundation OMB NO 1545-0052 Form 990 -PF, or Section 4947(a)(1) Trust Treated as Private Foundation Do not enter social security numbers on this form as it may be made public. Department of the Treasury ► 2014 instructions is Internal Revenue Service ► Information about Form 990-PF and Its separate at For calendar year 2014 or tax year beginning JUL 1, 20 14 , and ending JUN 3 0, 20 1 5 Name of foundation A Employer identification number THE IMR CHARITY FOUNDATION, INC. 26 -0490086 Number and street (or P 0 box number if mail is not delivered to street address ) Room/swte B Telephone number 235 NORTH MAIN ST. 7 845-573-9100 C City or town, state or province, country, and ZIP or foreign postal code If exemption application is pending , check here ► SPRING VALLEY, NY 10977 G Check all that apply: L_J Initial return L_J Initial return of a former public charity D 1. Foreign organizations , check here Q Final return Amended return 2. Foreign organizations meeting the 85% test, Address c h an g e 0 N ame c h ange check here and attach computation ► H Check type of organization : TTr Section 501 (c)(3) exempt private foundation E If private foundation status was terminated 0 Section 4947(a)(1) nonexempt charitable trust = Other taxable private foundation under section 507(b)(1)(A), check here I Fair market value of all assets at end of year J Accounting method : Cash L_J Accrual F If the foundation is in a 60-month termination (from Part //, col (c), line 16) 0 Other ( specify) under section 507(b)(1)(B), check here ► ► $ 0 , (Part 1, column (d) must be on cash basis) Part I Ana lysis of Revenue and Expenses ( a) Revenue and (b) Net investment (c) Adjusted net (d) Disbursements (The total of amounts in columns ( b), (c), and ( d) may not for charitable purposes necessarily equal the amounts in column (a)) expenses per books income income ( cash basis only) 1 Contributions , gifts, grants, etc., received 141 , 000.