Tallinn Facts & Figures 09

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Matryca CNS&A Cover.Psd

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Varblane, Urmas; Mets, Tõnis; Andrijevskaja, Janita Research Report Knowledge-based entrepreneurship in Estonia CASE Network Studies & Analyses, No. 407 Provided in Cooperation with: Center for Social and Economic Research (CASE), Warsaw Suggested Citation: Varblane, Urmas; Mets, Tõnis; Andrijevskaja, Janita (2010) : Knowledge- based entrepreneurship in Estonia, CASE Network Studies & Analyses, No. 407, Center for Social and Economic Research (CASE), Warsaw This Version is available at: http://hdl.handle.net/10419/128204 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. www.econstor.eu CASE Network Studies & Analyses No.407 Knowledge-based entrepreneurship in Estonia Materials published here have a working paper character. They can be subject to further publication. -

Baltic Journal of Law & Politics Merger

BALTIC JOURNAL OF LAW & POLITICS VOLUME 6, NUMBER 1 (2013) ISSN 2029-0454 http://www.degruyter.com/view/j/bjlp Cit.: Baltic Journal of Law & Politics 6:1 (2013): 1-26 DOI: 10.2478/bjlp-2013-0001 MERGER REMEDIES IN A SMALL MARKET ECONOMY: EMPIRICAL EVIDENCE FROM THE BALTIC STATES Alexandr Svetlicinii Senior Researcher Tallinn University of Technology, Tallinn Law School (Estonia) Contact information Address: Akadeemia tee 3, 12618 Tallinn, Estonia Phone: +372 620 2422 E-mail address: [email protected] Külliki Lugenberg Adviser Estonian Competition Authority, Competition Division, Merger Control Department (Estonia) Contact information Address: Auna 6, 10317 Tallinn, Estonia Phone: +372 667 2483 E-mail address: [email protected] Received: February 4, 2013; reviews: 2; accepted: May 20, 2013. ABSTRACT The paper represents a comparative study of the merger remedies practices of the three Baltic states: Estonia, Latvia and Lithuania. Based on comprehensive merger control data (2004-2011) and a comparative assessment of merger remedies imposed by the NCAs in the selected economic sectors (telecoms, alcoholic beverages, construction materials, trade in pharmaceuticals) the study identifies trends and tendencies of merger control that are characteristic for small market economies. Despite harmonization of national competition laws and enforcement practices with the EU rules and standards, the study highlights an obvious divergence from the EU guidance expressed in increasing acceptance of behavioral commitments. The results of the assessment indicate the need to develop more specific BALTIC JOURNAL OF LAW & POLITICS ISSN 2029-0454 VOLUME 6, NUMBER 1 2013 guidance on behavioral remedies that would better reflect the merger control realities of small market economies. -

Voyager of the Seas® - 2022 Europe Adventures

Voyager of the Seas® - 2022 Europe Adventures Get your clients ready to dive deep into Europe in Summer 2022. They can explore iconic destinations onboard the new Odyssey of the Seas S M. Fall in love with the Med's greatest hits and discover its hidden gems onboard Voyager of the Seas® ITINERARY SAIL DATE PORT OF CALL 9-Night Best of Western April 15, 2022 Barcelona, Spain • Cartagena, Spain • Gibraltar, Europe United Kingdom • Cruising • Lisbon, Portugal • Cruising (2 nights) • Amsterdam, Netherlands Cruising • Copenhagen, Denmark 7-Night Best of Northern April 24, 2022 Copenhagen, Denmark • Oslo, Norway Europe August 28, 2022 (Overnight) • Kristiansand, Norway • Cruising • Skagen, Denmark • Gothenburg, Sweden • Copenhagen, Denmark 7-Night Scandinavia & May 1, 8, 15, 22, 2022 Copenhagen, Denmark • Cruising • Stockholm, Russia Sweden • Tallinn, Estonia • St. Petersburg, Russia • Helsinki, Finland • Cruising • Copenhagen, Denmark 7-Night Scandinavia & May 29, 2022 Copenhagen, Denmark • Cruising • Stockholm, Russia Sweden • Helsinki, Finland • St. Petersburg, Russia • Tallinn, Estonia • Copenhagen, Denmark 10-Night Scandinavia & June 5, 2022 Copenhagen, Denmark • Cruising • Stockholm, Russia Sweden • Tallinn, Estonia • St. Petersburg, Russia (Overnight) • Helsinki, Finland • Riga, Latvia • Visby, Sweden • Cruising • Copenhagen, Denmark Book your Europe adventures today! Features vary by ship. All itineraries are subject to change without notice. ©2020 Royal Caribbean Cruises Ltd. Ships’ registry: The Bahamas. 20074963 • 11/24/2020 ITINERARY SAIL DATE PORT OF CALL 11-Night Scandinavia & June 15, 2022 Copenhagen, Denmark • Ronne, Bornholm, Russia Denmark • Cruising • Tallinn, Estonia • St. Petersburg, Russia (Overnight) • Helsinki, Finland • Visby, Sweden • Riga, Latvia • Cruising (2-Nights) • Copenhagen, Denmark 7-Night Scandinavia & July 3, 2022 Stockholm, Sweden• Cruising • St. -

View Adventure of the Seas 2021 European Sailings

Adventure of the Seas® Get ready to dive deeper into Old World adventures in Summer 2021. Rediscover the Med’s greatest hits onboard Harmony of the Seas® , sailing from Barcelona and Rome, or on returning favorites Vision® and Rhapsody of the Seas® . Head north for unforgettable sights in the Baltics and the British Isles onboard Jewel of the Seas® . Choose from fjord filled thrills in Norway to Mediterranean marvels and everywhere in between onboard Anthem of the Seas® , sailing from Southampton —all open to book now. ITINERARY SAIL DATE PORT OF CALL 18-Night Galveston to April 21, 2021 Galveston, Texas • Cruising (9 Nights) • Gran Canaria, Copenhagen Canary Islands • Cruising • Lisbon, Portugal • Cruising (2 Nights) • Paris (Le Havre), France • Rotterdam, Netherlands • Cruising • Copenhagen, Denmark 7-Night Scandinavia & May 16, 2021 Copenhagen, Denmark • Cruising • Stockholm, Sweden Russia • Tallinn, Estonia • St. Petersburg, Russia • Cruising (2 Nights) • Copenhagen, Denmark 8-Night Scandinavia & May 30, 2021 Copenhagen, Denmark • Cruising • Stockholm, Sweden Russia • Tallinn, Estonia • St. Petersburg, Russia • Helsinki, Finland • Cruising (2 Nights) • Copenhagen, Denmark 10-Night Scandinavia & June 7, 2021 Copenhagen, Denmark • Cruising • Riga, Latvia • Russia Tallinn, Estonia • St. Petersburg, Russia (Overnight) • Helsinki, Finland • Stockholm, Sweden • Cruising • Copenhagen, Denmark (Overnight) 10-Night Ultimate June 17, 2021 Copenhagen, Denmark • Berlin (Warnemunde), Scandinavia Adventure Germany • Cruising • Helsinki, Finland • St. Petersburg, Russia (Overnight) • Tallinn, Estonia • For deployment information and marketing resources, visit LoyalToYouAlways.com/Deployment Features vary by ship. All itineraries are subject to change without notice. ©2019 Royal Caribbean Cruises Ltd. Ships’ registry: The Bahamas. ITINERARY SAIL DATE PORT OF CALL Visby, Sweden • Riga, Latvia • Stockholm, Sweden (Overnight) 7-Night Scandinavia & June 27, 2021 Stockholm, Sweden • Cruising • St. -

December 2019 Vladimir J. Konečni

December 2019 Vladimir J. Konečni CURRICULUM VITAE Birthplace: Belgrade, Yugoslavia Citizenship: Serbia and U.S.A. Address: Department of Psychology University of California, San Diego La Jolla, California 92093-0109, U.S.A. Office: tel (858) 534-3000; e-mail [email protected] Residence: tel (858) 481-9719 Web sites: http://www.vladimirkonecni.net/VJK_Publications http://psychology.ucsd.edu/people/profiles/vkonecni.html http://www.vladimirkonecni.net https://en.wikipedia.org/wiki/Vladimir_J._Konečni Education: 1959-1963 Second Belgrade Gymnasium, Belgrade, Yugoslavia 1964-1969 University of Belgrade, Belgrade, Yugoslavia; Diploma in Experimental and Clinical Psychology, 1969 1968 Behavior Modification Section, Academic Unit of Psychiatry, Middlesex Hospital, London, England 1970-1973 University of Toronto, Toronto, Canada; M.A., 1971; Ph.D., 1973 (Social and Experimental Psychology) Graduate Fellowships: 1970-1971 University of Toronto Open Fellowship; M. H. Beatty Graduate Fellowship 1971-1973 Canada Council Doctoral Fellowship 1972-1973 Junior Fellowship, Massey (Graduate) College, University of Toronto Research Fellowships: 1979-1980 John Simon Guggenheim Fellowship 1987 Deutscher Akademischer Austauschdienst (DAAD; September, December) Honors: 1994 Academician (Active Member, Section of Informatics in Culture) of the International Informatics Academy (Moscow/New York, an Affiliate of the Organization of United Nations); elected in September of 1994 in Moscow Academic Positions: 2 1973-1978 Assistant Professor, Department of Psychology, -

Legal Considerations

© 2010 Cooperative Cyber Defence Centre of Excellence (CCD COE) Contact: Cooperative Cyber Defence Centre of Excellence (CCD COE) 12 Filtri Rd. 10132 Tallinn, Estonia [email protected] www.ccdcoe.org All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without prior written permission of CCD COE. The views, opinions, and/or findings and recommendations contained in this analysis are those of the authors and should not be construed as an official position, policy, or decision of NATO or any NATO entity. Layout, design and illustrations: Marko Söönurm ISBN: 978-9949-9040-0-6 INTERNATIONAL CYBER INCIDENTS: LEGAL CONSIDERATIONS Eneken Tikk Kadri Kaska Liis Vihul 2010 4 Contents PREFACE ������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������6 INTRODUCTION TO CASE STUDIES..........................................................................................................................................................................................10 ESTONIA 2007 ����������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������14 -

White Book for the Future of Europe

White Book for the Future of Europe SPACE Street Participation for Active Citizenship in Europe Project Municipality of Tiggiano ITALY Index Introduction 3 Presentation of the SPACE project 4 Actors of the project 6 Presentation of Europe for Citizens - Strand Democratic engagement and civic participation 9 To debate in the street: the SPACE methodology 10 Citizen’s Voice: Street debate on “How important is Europe for you?” 15 Citizen’s Voice: Street debate on “What would you change in Europe?” 21 Citizen’s Voice: Street debate on “As citizens, how can I change Europe?” 27 Tiggiano (Italy), September 2019 This brochure had been realised in the frame of the project “Street Participation for Active Citizenship in Europe S.P.A.C.E” funded by the program “Europe for cit- izens” (Strand Democratic engagement and civic participation - Network of Town). The European Commission support for the production of this publication does Autors: not constitute an endorsement of the contents which reflects the views only of the Fillon Bastien (Officine Cittadine) authors, and the Commission cannot be held responsible for any use which may Leuzzi Evangelista (Fattoria Pugliese Diffusa) be made of the information contained therein. Actors of the project Introduction LEADING ORGANISATION After each European Elections, the statement is always the same: our European democracy is in crisis. Many European citizens do not partici- pate to the main democratic process of the European Union. To face this Municipality of Tiggiano fact and bring a positive answer to this challenge a Network of Towns ITALY decided in 2017 to create space in the street where citizens could ex- press, exchange and debate about the future of Europe: the SPACE PARTNERS OF THE PROJECT project. -

ATHENS the Resumption in Development Will Help Athens’ Letting Market

GREECE ATHENS The resumption in development will help Athens’ letting market TAKE-UP 90 OFFICE € RENT RATE % 80 255 11.0 thousands 70 PRIME RENT +5% of sqm 60 & VACANCY 250 9.0 IMPROVED BUSINESS ACTIVITY IS The improvement in the Greek econo- 50 +14% 40 RATE 245 7.0 CREATING DEMAND FOR MODERN SPACE my (GDP 2.0%) in 2019, political stabil- 30 -300 bp 20 240 5.0 The demand for quality office space ity and ongoing employment gains will 10 (grade A) in the major business districts support the demand side of commercial 0 of the city remained intense over 2019 real estate market. With the low vacan- 2016 2017 2018 2019 2016 2017 2018 2019 and led to take-up of 80,000 sqm over cy rate, rental prices are increasing and % BOND YIELD PRIME YIELD % the year. Demand came from relocation of now stand at €252/sqm/year. 550 OFFICE OFFICE existing tenants and new business activ- 10 8.0 INVESTMENT PRIME 7 7.50 ities from start-ups. Relocation is taking THE ATHENS INVESTMENT MARKET IS -100 bp € million +400% YIELD advantage of the new buildings that exist IMPROVING CREATING A REDUCTION 4 7.0 & BOND in Athens. The office sector lacks modern IN YIELDS 110 48 56 YIELD 1 6.50 units and undersupply means that the Stability also helped improve the in- vacancy rate is low at 5.7% in 2019. vestment market in Athens that posted 2016 2017 2018 2019 2016 2017 2018 2019 Development is improving gradually. a total investment volume of €550m Prodea REIC commenced construction in 2019. -

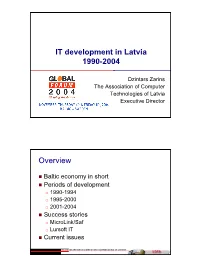

IT Development in Latvia 1990-2004 Overview

IT development in Latvia 1990-2004 Dzintars Zarins The Association of Computer Technologies of Latvia Executive Director Overview Baltic economy in short Periods of development 1990-1994 1995-2000 2001-2004 Success stories MicroLink/Saf Lursoft IT Current issues 1 Baltic economies 7.2 m inhabitants Bigger than Finland, Norway or Denmark GDP 36.2 m USD (2003) 22% of Finnish GDP GDP per capita 2-2.5 lower than in Nordic countries GDP growth 5-9% p.a. Set to continue over coming years The fastest-growing region in EU Tight integration with Nordic region Foreign trade equals to GDP Nordic countries are the main trade partners Whole branches of economy are owned by and integrated with Nordic companies Liberal economic policies Piracy level in the Baltic states Source: BSA 100% 90% 80% 70% 60% Latvia 50% Lithuania 40% Estonia 30% 20% 10% 0% 1999 2000 2001 2002 2003 2 Years 1990 - 1994 A lot of companies that distribute IT products and service were established; there was a great margin of hardware products. Equipment delivery to governmental and private sector Great “Black” market share Small distribution of legal software Missing of the greatest international whole sellers, great proportion of OEM computers. Direct company contact with USA, Taiwan and China Telecomunications monopoly, small internet capacity, expensive service Years 1990 - 1994 Software and data base development for governmental and private sector Small proportion of international business and accounting software Many local accounting programmes Beginning of international projects and success of a/s SWH Riga in software development; development of: SWH technology, today known as A/S "Exigen Latvia" DATI group 3 Years 1995 - 2000 International whole sellers start work Soft-tronik (Elko group) 1992 Elko Group 1993 Scribona (ex. -

Berlin to the Baltics: Germany, Czech Republic, Poland, Estonia, Latvia, Lithuania and Finland

FIND OUT MORE! www.ecetravelsptpi.com 2017 TRAVEL BERLIN TO THE BALTICS: GERMANY, CZECH REPUBLIC, POLAND, ESTONIA, LATVIA, LITHUANIA AND FINLAND Your key destinations: Berlin, Prague, ADVENTURE Challenge yourself and experience Krakow, Warsaw, Vilnius, Riga, personal growth as you: Tallinn and Helsinki. • Navigate the challenges of Tallinn’s premier ‘Rope Garden’ Explore a wealth of Eastern • Explore Helsinki by bike during an exclusive People to People moment European history, stretching • Explore Finland’s thrilling amusement park, Linnanmaki from the Medieval castles of the Baltics to war torn Berlin. EDUCATION Learn about different cultures and Discover how WW2 and the traditions as you: • Pay your respects at Auschwitz Cold War have shaped the • Attend an insightful, specially arranged meeting with a witness to the fall of the Berlin Wall region, as well as the ancient • Challenge the body and mind with sporting competitions and classical music performances traditions of the countries that make up this beautiful part of CULTURE Connect with locals as you: the world. • Immerse yourself in the glorious architecture of the region, particularly the much heralded city of Dresden All-inclusive Program Price: $6,290 • Meet like-minded peers and create long-lasting international relationships • With the help of experts, examine the progression of European society during the Cold *Supplements may apply. War and beyond 2017 TRAVEL BERLIN TO THE BALTICS: ITINERARY Helsinki GERMANY, CZECH REPUBLIC, POLAND, ESTONIA, LATVIA, LITHUANIA AND FINLAND Tallinn Day 7 Riga Day 1 Explore the sights of Krakow Depart the USA Join a guided visit of the Wawel Castle, a Vilnius Board your overnight flight to Europe. -

The Estonian ICT Manufacturing and Software Industry: Current State and Future Outlook

TECHNICAL REPORT SERIES The Estonian ICT Manufacturing and Software Industry: Current State and Future Outlook EUR 21193 EN Institute for Prospective Technological Studies THE ESTONIAN ICT MANUFACTURING AND SOFTWARE INDUSTRY: Current State and Future Outlook TARMO KALVET The author of this report is solely responsible for the content, style, language and editorial control. The views expressed do not necessarily reflect those of the European Commission APRIL 2004 Technical Report EUR 21193 EN European Commission Joint Research Centre (DG JRC) Institute for Prospective Technological Studies http://www.jrc.es Legal notice Neither the European Commission nor any person acting on behalf of the Commission is responsible for the use which might be made of the following information. Techncial Report EUR 21193 EN © European Communities, 2004 Reproduction is authorised provided the source is acknowledged. Printed in Spain Acknowledgments ACKNOWLEDGMENTS The author would like to express his gratitude to the ICT Unit at the Institute for Prospective Technological Studies (part of the Directorate General Joint Research Centre) for initiating this research project. Several most interesting round-table discussions led by Bernard Clements (Head of the ICT Unit), Jean-Claude Burgelman and Marc Bogdanowicz, took place from 2002 to 2004. I would particularly like to thank Marc Bogdanowicz for these professional and stimulating debates. I would also like to acknowledge the help of my colleagues, Wolfgang Drechsler and Rainer Kattel at the Innovation Program at the PRAXIS Centre for Policy Studies, and the foreign experts at PRAXIS – most notably Carlota Perez and Erik S. Reinert – for thought provoking and inspiring discussions. Special thanks for discussing related issues over the years go to Marek Tiits and Tarmo Pihl. -

The Tallinn Declaration on the Future of Smr Licensing

THE TALLINN DECLARATION ON THE FUTURE OF SMR LICENSING We, gathered in Tallinn, Estonia, NOTING the formation of the European SMR Alliance in January 2020 with the goal of facilitating wide-spread Small Modular Reactor (“SMR”) deployment in Europe by the 2030s; RECOGNISING the urgent response needed to meet the European Union’s commitment to achieving carbon neutrality by 2050; BELIEVING that SMRs can make a significant contribution to low-carbon energy mixes in the European Union and globally; RESPECTFUL of the role of nuclear regulatory bodies in ensuring safe, secure and peaceful uses of nuclear energy; COGNISANT of the impact of nuclear licensing processes and regulatory matters on the business case for SMRs, design criteria, development of supply chains and overall viability of SMR deployment; CONSCIOUS that effective and efficient utilisation of experienced global human resources in reactor licensing is necessary; and CONVINCED that SMR vendors and future SMR licensees must proactively engage with regulators in their own countries and in key jurisdictions around the world to promote the optimal way forward for SMR licensing, Hereby support and will promote the following principles of SMR licensing: 1. A pragmatic approach to SMR licensing must be employed to overcome licensing and regulatory challenges and reduce SMR project risk relating to nuclear regulation and the licensing process. 2. SMR design standardisation must be facilitated to the greatest extent possible. 3. In developing or updating the regulatory framework applicable to SMRs, host country nuclear regulatory bodies should seek to facilitate regulatory harmonisation. Regulatory frameworks should be based on the International Atomic Energy Agency (“IAEA”) Safety Standards (as applicable to the relevant SMR(s)) and implement European Union Nuclear Safety Directives, as well as give due consideration to compatibility with relevant vendor/reference plant country-of-origin or other experienced nuclear country’s regulatory regimes.