Downtown Tampa Parking Study and Plan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Effective January 24, 2021 LIMITED EXPRESS ROUTES LOCAL

WESLEY CHAPELCHAPEL LOCAL ROUTES Calusa Tr ace BlBlv & HARTFLEX vdd.. Van Dyke RdRd.. St. Joseph’s Hospital - North ALL SERVICE MAPS LOCAL ONLY EXPRESS ONLY 33 WESLEY CHAPELCHAPEL NORTHDALE Lakeview D r . LUTZ SYSTEM MAP Gaither High TAMPA PALMS School Effective January 24, 2021 NNoorthda le B lv d. e. Sinclair Hills Rd. e. Av Av LEGEND LEGEND LEGEND Be . ars d s v l A Local Route Key Destinations Key Destinations B Ehrlich Rd. v s B 44 e n # and Route Number . w Route 33 does not 22nd St. 22nd St. Livingston Livingston ce BB. Do Hidden Local Route and Route Number Express Route Bru serve Hidden River 12 Calusa Skipper Rd.Rd. River Limited Express Route 20X20X Express routes marked by an X Tr Park-n-Ride on Park-n-Riderk-n-Ride ace BlvBl 44 AdventHealthventHealth Weekends # and Route Number Downtown to UATC CITRUS PARK vdd.. 1 42 400 Westeldsteld Fletcher Ave. 42 - Tampa 33 LX Limited Express routes See route schedule for details Limited Express Route Citrus Park @ Dale MabMabrryy Hwy. Stop P marked by an LX 75LX Mall Van Dyke RdRd.. 33 6 Fletcher Ave. Limited Express routes marked by an LX HARTFlex Zone St. Joseph’s Fletcher Ave. 33 400 FLEX e. HospitalCARROLLWOOCARROLLWOOD - North D e. 33 HARTFlex Route See route schedule for details 39 GunnGun H 48 Park-n-Ride Lots Av n Hwwy. 33 Av y. 131st Ave. University P B HARTFleHARTFlexx HARTFlex Route Vanpool Option Locations Walmart of South HARTFlex Zone See route schedule for details NORTHDALE Lakeview 45 Call TBARTA at (800) 998-RIDE (7433) e. -

West End Tampa Tampa, Florida

West End Tampa Tampa, Florida MORIN DEVELOPMENT GROUP 1510 West Cleveland Street, Tampa FL 33606 Telephone 813-258-2958 Fax 813-258-2959 1 The information above has been obtained from sources believed reliable. While we do not doubt its accuracy we have not verified it and make no guarantee, warranty or representation about it. It is your responsibility to independently confirm its accuracy and completeness. Table of Contents • Development Summary • Site Plans • Block A • Block B • Block C • Block D • Block E • Block F • Block G • North B Town Homes • Market Information • About Us 2 West End Tampa West End Tampa is a 20-acre master planned, family community comprised of apartments, town homes, condominiums and retail features. It is centrally located between the region’ s two largest business centers – Downtown Tampa (within 1 mile) and the West Shore Business District (within 3 miles). West End is encircled by major medical centers including Tampa General, Memorial and St. Joseph’s hospitals. It is situated within blocks of the nationally accredited University of Tampa. The West End community incorporates architectural sensitivity with ample, open public spaces to create a livinggyg environment that is distinctly different from the existing inventory of “Urban Lifestyle” product which is prevalent today. Contributing to the lifestyle balance of West End Tampa are parks, public art, recreational areas, pools, fitness centers and a convenient business center. Retail and Commercial…………………….25,000 Sq. Ft. of “neighborhood retail” spacece Office………………………………………...4, 500 Sq. Ft. of “Class A ” office space UNITS HEIGHT BEDROOMS SQ. FT. Condominiums 346 4-5 stories 2 & 3 630 – 1,600 Town Homes 79 3stories3 stories 2&32 & 3 16231,623 – 21132,113 Apartments 3 The Vintage Lofts 249 4 stories 1, 2 & 3 740 – 1,250 Logan Park 296 8 stories 1 & 2 737 – 1,204 West End Location West End Tampa is bordered to the south by Tampa’s charming Hyde Park neighborhood. -

The Elliman Report: Q3-2020 Tampa Sales Prepared by Miller Samuel Real Estate Appraisers

Report South And Greater Q3-2020 Downtown Tampa, FL Sales Median Sales Price South Tampa Single Family Number of Sales $400K 400 $320K 320 South Tampa $240K 240 Single Family $160K 160 Dashboard $80K 80 YEAR-OVER-YEAR Median Sales Price South Tampa Single Family Number of Sales $0 0 $400K 400 + 11.2% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 $320KSouth Tampa Single Family Matrix Q3-2020 %∆ (QTR) Q2-2020 %∆ (YR) Q3-2019320 Prices Median Sales Price Average Sales Price $440,254 8.3% $406,697 13.7% $387,263 $240K 240 + 22.8% Average Price Per Sq Ft $224 1.4% $221 7.2% $209 $160KMedian Sales Price South Tampa Condo Number of Sales160 Sales Closed Sales Median Sales Price $358,750 10.6% $324,500 11.2% $322,500 $250KNumber$80K of Sales (Closed) 334 36.9% 244 22.8% 2728060 - 31.7% Days on Market (From Last List Date) 38 -20.8% 48 -29.6% 54 $200K$0 048 Inventory Tota l Inventor y Listing Discount (From Last List Price) 1.7% 2.4% 2.0% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 $150KListing Inventory 127 0.8% 126 -31.7% 18636 - 16 days $100KMonths of Supply 1.1 -26.7% 1.5 -47.6% 2.124 Marketing Time Average Square Feet 1,962 6.3% 1,845 5.9% 1,853 Days on Market $50K 12 Median Sales Price South Tampa Condo Number of Sales $0 0 $250K 60 South Tampa Condo 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Dashboard $200K 48 YEAR-OVER-YEAR $150K 36 + 34.1% $100K 24 Median Sales Price Number of Sales Prices Median Sales Price $50K South Tampa Luxury 12 $1.1M 50 + 10.6% $0 0 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 -

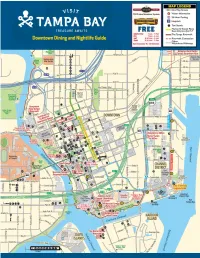

Downtown Dining Map 2019 List

To 13 51 136 137 118 138 114 17 157 123 25 23 41 154 91 10 101 98 76 45 61 83 18 149 143 2 76 86 16 26 55 105 94 14 103 56 128 109 80 48 111 8 2 77 96 104 78 74 93 28 46 99 141 53 40 1 38 7 32 97 5 153 3 146 21 39 95 134 4 66 47 106 21 90 9 59 79 102 44 72 92 58 121 120 87 70 151 127 135 69 60 82 122 124 114 115 68 100 85 120 41 125 43 117 84 88 119 71 73 140 73 12 35 64 75 20 42 34 To 27 15 29 33 24 17 156 126 19 To 52 63 158 159 37 129 152 30 81 6 147 107 155 89 To 133 11 22 139 50 132 148 131 To 130 31 36 49 62 65 110 112 AMERICAN 152 Publix Super Market on Bayshore Bakery- 87 Kahwa Café, Rivergate Tower - 17 Precinct Pizza - 813.228.6973 813.251.1173 813.225.2040 43 211 Restaurant at Hilton Tampa Downtown 96 Riverwalk Cafe at TMA - 813.421.8367 813.204.3000 BARBEQUE 66 Moxies Café - 813.221.4510 80 Tampa Pizza Co., SkyPoint - 813.463.1600 130 220 East - 813.259.1220 44 Holy Hog Barbecue - 813.223.4464 68 Nature’s Table, Park Tower - 813.223.2233 12 TamPiz - 813.252.3420 131 725 South Bistro at Westin Tampa 69 Oasis Deli - 813.223.3305 Waterside - 813.229.5000 CARIBBEAN 60 Toscanini NY Pizza and Pita - 813.500.7700 70 Ole Style Deli - 813.223-4282 97 1895 Kitchen Bar Market - 813.375.9995 34 Caribbean Cantina in Florida Aquarium - 813.273.4000 59 Pokeys - 813.223.6905 MEDITERRANEAN 132 American Social - 813.605.3333 40 Jerk Hut Downtown Café - 813.223.5375 152 Publix Deli - 813.251.1173 56 Falafel Inn Mediterranean Grill, SkyPoint - 124 Brightside Cafe - 813.241.9295 813.223.5800 84 Surf & Turf Cafe - 813.221.3354 98 Bistro at The -

Master Plan - Phase 1 0 10050 200 Other Logos Here Tampa, Florida February 12, 2019

Tampa’s next chapter Introducing Water Street Tampa, the city’s new downtown. A dynamic waterfront district, the neighborhood will enhance Tampa’s profile on the national stage, attracting professionals, residents, and tourists to explore and enjoy. Tampa, transforming No. 1 Top city for first time city for home buyers entrepreneurs Zillow, 2018 Forbes Magazine, 2017 th highest job and population growth in the nation 4 US Census Bureau, 2017 The Water Street Tampa impact It’s growing up 11 12 9 10 4 6 3,525* 13 3 7 Units Residential 2 13,700** 8 5 { 1 14 Residents 2,390,007* Square Feet Office { 45,000** Hotels Office Residential Future Phase Employees 1 727 Keys 4 564,883 SF Office 8 420 Units 11 Residential & Retail 122,650 SF Retail 52,848 SF Retail 2 519 Keys 12 Office & Retail 5 188,523 SF Office 3 37 Units 3 173 Keys 76,320 SF Retail 29,833 SF Retail 13 Entertainment & Retail Annual visitors 3,169,300** 6 354,306 SF Office 9 481 Units 14 Residential & Retail 10,568 SF Retail 29,833 SF Retail 7 2,000 Employees & Students 10 388 Units * Includes future phases 6,421 SF Retail 13,394 SF Retail ** Downtown, Channel District, Harbour Island Vibrant, spirited, and creative The Water Street Tampa who 25% 20% 13% 4,440 / 17,140 3,330 / 17,140 2,200 / 17,140 Established urbanites Bohemian mixers Digital natives Harbour Island / Davis Islands Channel District Downtown Tampa Wealthy city dwellers with Young, diverse, and mobile Tech-savvy, established advanced degrees, expensive urbanites with liberal millennials living in fashionable, cars, -

Tampa Convention Center Parking

E 7th Av 7th Av 7th Av Henderson Av Henderson Av DOWNTOWN TAMPA & CHANNEL DISTRICT 6th Av EstelleEstelle WATER WORKS StetsonStetson UUnivniv To Ybor City PARK t LawLaw CCenterenter s 5th5th AAvv Streetcar EXIT a E continues to 45A 4 Ybor City - I 1 14th St St 14th 1 14th o KayKay StSt 30 5 EXIT T 4th4th AvAv 4 ToTo StSt Petersburg,Petersburg, t t ay S 29 t 45A KayK St h ClearwaterClearwater & h Nebraska Av Av Nebraska N Nebraska ScottS Dr S Governor St St Governor G Governor c S e BeachesBeaches o t t o t b t v D 275 r r e a Maryla M Maryla Franklin St St Franklin F Franklin r ScottScott StSt s FloridaF Av Morgan M Morgan ScottScott SStt Tampa St St Tampa T Tampa Marion St Marion M Marion St Marion n r k l a a a o o o a D D a r m n r r y r r EXIT A o o i g k i y l d p 44 o a v y S k l a a SunP i - a ll ass nd St nd n nd S nd o n T o l ( n t n n w s ly) e e IndiaIndia StSt n A d OrangeO Av OrangeO Av S P a AdamoAdamo L Bush St B 60 S C S LaurelLaurel s t v o s r r S u t i e t r a a a c t t p Marion Transit Center s r n n c x l h u E t In-Town Trolleys g g Ct e o d NuccioN Pwkyl S e e e b connect to JoedJo Ct i n t s A A r FortuneFortune StSt HARTline Busses D t e S v v v r r l re 27 e u R LaurelLa St St PERRY HARVEY n d t o e S SENIOR PARK ris t son ar a rri HarrisonH St vva a e HarrisonH St l 618 ONT E 12th St St 12th 1 12th 2 HowardHoward St t h JohnsonJohnson ler CassCass StSt yyl 31 T S PlazaPlaza t t NebraskaN Av SunPass 60 S e e Only un b T rt HERMAN t r Fo S a MacInnesM Pl MASSEYK ss TwiggsTwiggs SStt PAR 26 CassCa St s a 58 k c -

City of Tampa Walk–Bike Plan Phase VI West Tampa Multimodal Plan September 2018

City of Tampa Walk–Bike Plan Phase VI West Tampa Multimodal Plan September 2018 Completed For: In Cooperation with: Hillsborough County Metropolitan Planning Organization City of Tampa, Transportation Division 601 East Kennedy Boulevard, 18th Floor 306 East Jackson Street, 6th Floor East Tampa, FL 33601 Tampa, FL 33602 Task Authorization: TOA – 09 Prepared By: Tindale Oliver 1000 N Ashley Drive, Suite 400 Tampa, FL 33602 The preparation of this report has been financed in part through grants from the Federal Highway Administration and Federal Transit Administration, U.S. Department of Transportation, under the Metropolitan Planning Program, Section 104(f) of Title 23, U.S. Code. The contents of this report do not necessarily reflect the official views or policy of the U.S. Department of Transportation. The MPO does not discriminate in any of its programs or services. Public participation is solicited by the MPO without regard to race, color, national origin, sex, age, disability, family or religious status. Learn more about our commitment to nondiscrimination and diversity by contacting our Title VI/Nondiscrimination Coordinator, Johnny Wong at (813) 273‐3774 ext. 370 or [email protected]. WEST TAMPA MULTIMODAL PLAN Table of Contents Executive Summary ........................................................................................................................................................................................................ 1 Introduction and Purpose ......................................................................................................................................................................................... -

Tampa Bay History Published Through a Partnership Between the Tampa Bay History Center and the University of South Florida Libraries’ Florida Studies Center

Volume 23 2009 Tampa Bay History Published through a partnership between the Tampa Bay History Center and the University of South Florida Libraries’ Florida Studies Center Rodney Kite-Powell, Editor Saunders Foundation Curator of History, Tampa Bay History Center Andrew Huse, Assistant Editor Assistant Librarian, University of South Florida Libraries’ Special Collections Department and Florida Studies Center Mark I. Greenberg, Ph.D., Book Review Editor Director, University of South Florida Libraries’ Special Collections Department and Florida Studies Center Editorial Board Jack Davis, Ph.D. University of Florida James M. Denham, Ph.D. Florida Southern College Paul Dosal, Ph.D. University of South Florida Maxine Jones, Ph.D. Florida State University Robert Kerstein, Ph.D. University of Tampa Joe Knetsch, Ph.D. State of Florida, Department of Environmental Protection Jerald Milanich, Ph.D. Florida Museum of Natural History Gary R. Mormino, Ph.D. Florida Studies Program, University of South Florida Susan Parker, Ph.D. St. Augustine Historical Society Cheryl Rodriguez, Ph.D. University of South Florida Aaron Smith, Ph.D. University of South Florida Doris Weatherford Tampa, Florida Tampa Bay History (ISSN: 0272-1406) is published annually through a partnership between the Tampa Bay History Center and the Florida Studies Center at the University of South Florida Library. The journal is provided complimentarily to Tampa Bay History Center members who belong at or above the Supporter membership level. Copies of the current issue of Tampa Bay History may be purchased directly from the Tampa Bay History Center at a cost of $19.95, plus shipping. Back issues (beginning with the 2007 issue) will also be available for purchase. -

114 12Th Street for SALE.Indd

114 S. 12TH STREET TAMPA, FL 33602 For Sale - Live/Work/Play Opportunity, Channel District Ultimate Party Pad- Luxury and Style Working For YOU! Property Details: • Sales Price: $3,400,000 (6,782 SF) Th e Heights/ • Also available For Lease Armature Works • Zoned: CD-1 (Channel Dist - Mixed Use) Ybor • View Virtual Tour of Open Space Here. • Renown Street Artist work within space. • Designed to include a roof top patio. • Perfect location for live/work/play, solid investment and endless possibilities. • Amidst the newest entertainment district of Water Street & Sparkman Wharf. Channel • Proposed uses: Residential, Offi ce, High End Car Storage, Downtown District Event Venue, B&B, Restaurant. • Blocks from SPP’s Water Street, Downtown, Convention Center, the Riverwalk, Florida Aquarium and the Streetcar Line. • Minutes from South Tampa, Armature Works, Ybor City, and the University of Tampa. A quick 15 minute drive to the airport and the BUCS stadium. FOR MORE INFORMATION, CONTACT: THE DOHRING GROUP ABBEY DOHRING AHERN 518 North Tampa Street, Suite 300 Principal, Brokerage Tampa, Florida 33602 Main (813) 223-9111 www.DohringGroup.com [email protected] 114 S. 12TH STREET TAMPA, FL 33602 For Sale - Live/Work/Play Opportunity, Channel District Commercial Photos FOR MORE INFORMATION, CONTACT: THE DOHRING GROUP ABBEY DOHRING AHERN 518 North Tampa Street, Suite 300 Principal, Brokerage Tampa, Florida 33602 Main (813) 223-9111 www.DohringGroup.com [email protected] 114 S. 12TH STREET TAMPA, FL 33602 For Sale - Live/Work/Play Opportunity, Channel District Commercial Photos FOR MORE INFORMATION, CONTACT: THE DOHRING GROUP ABBEY DOHRING AHERN 518 North Tampa Street, Suite 300 Principal, Brokerage Tampa, Florida 33602 Main (813) 223-9111 www.DohringGroup.com [email protected] 114 S. -

Fpid No. 258337-2 Downtown Tampa Interchange

DETAIL A MATCHLINE A DRAFT Grant Park SACRED HEART ACADEMY James Street James Street These maps are provided for informational and planning PROPOSED NOISE BARRIER TO BE CONSTRUCTED UNDER purposes only. All information is subject to change and WPI SEGMENT NO.44 3770-1 the user of this information should not rely on the data N 5 AUX Emily Street Emily Street ORANGE GROVE 1 Ybor Heights College Hill-Belmont Heights for any other purposes that may require guarantee of 0 60 300 AUX MIDDLE MAGNET 4 1 BORRELL SCHOOL accuracy, timeliness or completeness of information. Feet N PARK (NEBRASKA AVENUE 0 60 300 PARK) DATE: 2/19/2020 5 AUX Feet X 1 26th Avenue AU 4 ROBLES PARK 1 STAGED IMPLEMENTATION PROPOSED NEW AND PLAY GROUND FOR WPI 431746 NOISE BARRIER -1 INTERSTATE 4 (SELMON CONNECTOR TO EAST OF 50th STREET) T B N T e x Plymouth Street IS t S S e ec g ti m on e n 8 t 3 B Adalee Street Adalee Street 3 e 3 nu e v M A e lbou a Hugh Street k r Hugh Street n TE A s T KING'S KID e S R a E A T r CHRISTIAN ve IN b n PROPOSED NEW u e ACADEMY e NOISE BARRIER N Hillsborough Avenue N Highland Pines Hillsborough Avenue Floribraska Avenue INTERSTATE Floribraska Avenue 1 e 3 nu 3 e e v 21st Avenue e t A nu 1 t nu e ll INTERSTATE St. Clair Street ee e v r e ee t v r A h t S A c e S l l C it C h t a Robles Street r M CC t no i 50 e n FRANKLIN MIDDLE e m e 52nd nu MAGNET SCHOOL e C nu 20th Avenue e S Jackson Heights e v N v A N SALESIAN YOUTH CENTER A BO o YS & GIRLS CLUB l 41 rr a OF TAMPA BAY r e t f n a e li a C T 18th Avenue Florence N e Bryant Avenue nu e North Ybor Villa / D.W.W ATER CAREER CENTER v EXISTING NOISE V.M. -

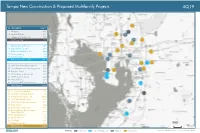

Tampa New Construction & Proposed Multifamily Projects

Tampa New Construction & Proposed Multifamily Projects 4Q19 ID PROPERTY UNITS 1 Wildgrass 321 3 Union on Fletcher 217 5 Harbour at Westshore, The 192 Total Lease Up 730 15 Bowery Bayside Phase II 589 16 Tapestry Town Center 287 17 Pointe on Westshore, The 444 28 Victory Landing 69 29 Belmont Glen 75 Total Under Construction 1,464 36 Westshore Plaza Redevelopment 500 37 Leisey Road Mixed Used Development 380 38 Progress Village 291 39 Grand Cypress Apartments 324 43 MetWest International 424 44 Waverly Terrace 214 45 University Mall Redevelopment 100 Total Planned 2,233 69 3011 West Gandy Blvd 80 74 Westshore Crossing Phase II 72 76 Village at Crosstown, The 3,000 83 3015 North Rocky Point 180 84 6370 North Nebraska Avenue 114 85 Kirby Street 100 86 Bowels Road Mixed-Use 101 87 Bruce B Downs Blvd & Tampa Palms Blvd West 252 88 Brandon Preserve 200 89 Lemon Avenue 88 90 City Edge 120 117 NoHo Residential 218 Total Prospective 4,525 2 mi Source: Yardi Matrix LEGEND Lease-Up Under Construction Planned Prospective Tampa New Construction & Proposed Multifamily Projects 4Q19 ID PROPERTY UNITS 4 Central on Orange Lake, The 85 6 Main Street Landing 80 13 Sawgrass Creek Phase II 143 Total Lease Up 308 20 Meres Crossing 236 21 Haven at Hunter's Lake, The 241 Total Under Construction 477 54 Bexley North - Parcel 5 Phase 1 208 55 Cypress Town Center 230 56 Enclave at Wesley Chapel 142 57 Trinity Pines Preserve Townhomes 60 58 Spring Center 750 Total Planned 1,390 108 Arbours at Saddle Oaks 264 109 Lexington Oaks Plaza 200 110 Trillium Blvd 160 111 -

Transforming Tampa's Tomorrow

TRANSFORMING TAMPA’S TOMORROW Blueprint for Tampa’s Future Recommended Operating and Capital Budget Part 2 Fiscal Year 2020 October 1, 2019 through September 30, 2020 Recommended Operating and Capital Budget TRANSFORMING TAMPA’S TOMORROW Blueprint for Tampa’s Future Fiscal Year 2020 October 1, 2019 through September 30, 2020 Jane Castor, Mayor Sonya C. Little, Chief Financial Officer Michael D. Perry, Budget Officer ii Table of Contents Part 2 - FY2020 Recommended Operating and Capital Budget FY2020 – FY2024 Capital Improvement Overview . 1 FY2020–FY2024 Capital Improvement Overview . 2 Council District 4 Map . 14 Council District 5 Map . 17 Council District 6 Map . 20 Council District 7 Map . 23 Capital Improvement Program Summaries . 25 Capital Improvement Projects Funded Projects Summary . 26 Capital Improvement Projects Funding Source Summary . 31 Community Investment Tax FY2020-FY2024 . 32 Operational Impacts of Capital Improvement Projects . 33 Capital Improvements Section (CIS) Schedule . 38 Capital Project Detail . 47 Convention Center . 47 Facility Management . 49 Fire Rescue . 70 Golf Courses . 74 Non-Departmental . 78 Parking . 81 Parks and Recreation . 95 Solid Waste . 122 Technology & Innovation . 132 Tampa Police Department . 138 Transportation . 140 Stormwater . 216 Wastewater . 280 Water . 354 Debt . 409 Overview . 410 Summary of City-issued Debt . 410 Primary Types of Debt . 410 Bond Covenants . 411 Continuing Disclosure . 411 Total Principal Debt Composition of City Issued Debt . 412 Principal Outstanding Debt (Governmental & Enterprise) . 413 Rating Agency Analysis . 414 Principal Debt Composition . 416 Governmental Bonds . 416 Governmental Loans . 418 Enterprise Bonds . 419 Enterprise State Revolving Loans . 420 FY2020 Debt Service Schedule . 421 Governmental Debt Service . 421 Enterprise Debt Service . 422 Index .