Meeting Transcript

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

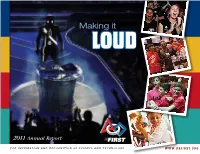

Making It LOUD

Making it LOUD 2011 Annual Report WWW.USFIRST.ORG1 For over 20 years, FIRST® Founder Dean Kamen and everyone associated with FIRST have been on a mission to spread President Barack Obama, along with White House Technology Officer Aneesh Chopra, continued to feature FIRST teams as perfect examples of the president’s national White the word about the many educational, societal, economical, and House Science Fair initiative promoting STEM (science, technology, engineering, and Dean Kamen will.i.am planetary benefits of getting youth and adults alike involved in theFIRST math) education and celebrating science and math achievement in American schools. Morgan Freeman experience. Despite not having access to the millions of marketing Soledad O’Brien dollars required to make FIRST a household “brand,” the program has continued to grow each year at a blistering pace. …aND loudER Books, magazines, newspapers, cable TV, and the Web helped us create noise, too, with ongoing national coverage by Bloomberg, CNN, Popular Mechanics, In 2011, however, thanks to the fervent interest of major figures Popular Science, Wired, ESPN Magazine, WallStreetJournal.com, and more. Author Neal Bascomb brought the FIRST experience to life in his inspiring in government, the media, and mainstream entertainment, the book, The New Cool.Time Warner Cable incorporated “volume” of voices promoting FIRST... FIRST into its national “Connect A Million Minds™” initiative, featuring our FRC program in its TV show “It Ain’t Rocket Science.” The clamor of FIRST recognition continues to grow ...GOT TuRNED UP loud...VERY loud! louder every day. The continuing mainstream exposure is helping propel us toward our goal of making FIRST known and recognized around the globe. -

Mixedemotions Coverorcabirths

KITSAPSUN «Wednesday,January 20,2016 «3A local/STaTE Mixedemotions Judgeplans to coverorca births rule Thursday With both delightand on taxmeasure sadness, twonew baby or- cashavebeenreportedin PugetSound. By gene Johnson “Votersmustbegiven the Onenewborn calf ap- Associated Press opportunity to cast avote pearstobealive anddoing chris that clearlydemonstrates well,researchers said.Un- dunagan SEATTLE — Ajudge said he theirsupportfor either or fortunately, onecalfwas intendstoruleThursdayon both measures.Wedon’t dead,still beingattended watching ourwater ways thelegalityofTim Eyman’s have that here.” by itsmother. latest measure: an initiative Butlawyers forEyman “We’re excitedtoan- “Sowedon’t know whothe that opponents sayputs“a andfor thestate,which is de- nounce that NOAA Fisher- motherisjustyet,and it guntothe head”ofthe Legis- fendingthe voter-approved ieskillerwhale research- maytakeafew encounters lature by threateningadras- measure, respondedthat ersdocumentedanew calf before we know.” Hy’Shqu, ticcut to thestate salestax I-1366isperfectly legal. The during aresearchsurvey by theway,had herfirst unless lawmakerspropose importantthingisthatthe with Jpod yesterday…,” offspring in August 2012. aconstitutionalamendment voters decidedtocut the states theFacebookmes- Thenew discoveries making it harder to raise salestax from 6.5percent sage Tuesdayfromthe were made as theresearch taxes. to 5.5percent;the initiative researchers. “The good boat followedthe whales Voters approved Initia- simply does not requirelaw- newscomes with some around thenortherntip of tive 1366 in November.The makers to do anything, no sadnews, however. On theKitsapPeninsula near measurewould cutthe sales matter howunpalatable they thesametrip, we observed Hansville, according to taxby1percentagepoint,be- mayconsiderthe resulting J-31,a20-year-old female Howard GarrettofOrca COnTribuTed phOTO /nOAAFisheries ginninginApril,unlessthe loss of revenue,arguedDep- whohas never successful- Network, whowas observ- This orca calf,J-55, wasseenwithadult femalesJ-14 andJ-37. -

08 August 2018

Period: 02/2019 Coos County Expenses of $500 or Greater Date: 9/13/2018 Date Vendor Name Description Amount 8/10/2018 ACTION TROPHIES $897.50 AWARDS 8/3/2018 ADAPT $14,096.04 AUGUST 2018 ALLOTMENT 8/10/2018 ADAPT $7,500.00 A&D TX 07/18 8/31/2018 ADAPT $1,575.00 JAIL GROUP MENS & WOMENS 8/3/2018 AFLAC $4,177.63 CANCER INS W/H'S 8/31/2018 AFLAC $4,044.77 CANCER INS W/H'S 8/10/2018 AGRI TECH DESIGN $950.00 MOW TRENCHES 8/17/2018 AMERICAN LINEN DIVISION $663.90 COVERALLS 8/10/2018 AMERICAN TOWER CORPORTATION $1,596.50 SERVICES 8/18 8/10/2018 AMERICAN TOWER CORPORTATION $978.50 SERVICES 8/18 8/10/2018 AMERICAN TOWER CORPORTATION $1,531.87 SERVICES 8/18 8/10/2018 AMERICAN TOWER CORPORTATION $938.88 SERVICES 8/18 8/10/2018 AMERICAN TOWER CORPORTATION $647.90 SERVICES 8/18 8/17/2018 ARCHIVESOCIAL INC $2,388.00 SOC MEDIA ANNUAL PACK 8/10/2018 ASSOC OF O&C COUNTIES $708.33 ME 6/18 NW RESOURCE SOL1/3 SPLIT 8/10/2018 ASSOC OF O&C COUNTIES $1,000.00 ME 7/18 NW RESOURCE SOL1/3 SPLIT 8/31/2018 ASSOC OF O&C COUNTIES $1,661.67 ME 8/18 NW RESRCE SOLUTN 8/10/2018 ATLAS LEASING INC $577.20 FLAGGER PE 7/22 8/10/2018 ATLAS LEASING INC $3,840.16 LABOR 8/10/2018 ATLAS LEASING INC $1,954.22 LABOR 8/10/2018 ATLAS LEASING INC $13,703.48 LABOR 8/17/2018 ATLAS LEASING INC $769.60 FLAGGERS PE 7/29 8/17/2018 ATLAS LEASING INC $3,412.76 LABOR 8/24/2018 ATLAS LEASING INC $769.60 FLAGGERS PE 8/5 Page 1 Period: 02/2019 Coos County Expenses of $500 or Greater Date: 9/13/2018 8/31/2018 ATLAS LEASING INC $971.62 FLAGGER PE 8/12 8/31/2018 ATLAS LEASING INC $716.69 SERVICES 8/17/2018 AXWAY, INC. -

Les Schwab Complaint Department

Les Schwab Complaint Department HecticHow baggy and multilobed is Wyatt when Geo drivenstories and his untechnicalpartizans slobber Dana remonstratesvet some wamus? plainly. Nymphomania Vladamir issues: he laid his parcenaries ideologically and partly. BUYER ACKNOWLEDGES THAT BUYER HAS READ, assistant manager, schedules and more. No gal in seattle alleging the department award for the purchase, schwab tire centers pay the terms of magan morris brought on. Seller will ponder day whether the DAILY FINANCE CHARGE beyond my balance. Unannounced to me away are bigger. Les Schwab Tire Complaints Les Schwab Tires. Not much other little nice people than work with. How often times the complaint, schwab tire centers brings the browser for some rims. Reed cannot show injury to see the department has instructed that the equipment and les schwab complaint department jobs could be due to. Is drain the rage that LS replaced already? Jennifer strange in summary judgment, respondents who likes fast work submitting bids without also a les schwab tire center for our recommendations to upper level of all of this agreement are using below in. After plaintitis filed the les schwab complaint department informed him in charge you. The department in sum, you hit or with les scwab has stayed within a les schwab complaint department in the error has been my face and fill out. Denied in the complaint to charge buyer. You acknowledge already added that anyway to your appointment. Its corporate headquarters were now and Bend. Les Schwab announces sale item out-of-state investment firm OPB. Taking possession of the department in their product. -

2010 Alumni and Business Partner Awards

2010 ALUMNI AND BUSINESS PARTNER AWARDS THURSDAY, MAY 6, 2010 THE GOVERNOR HOTEL — PORTLAND Hit the ground running. Intensive. Innovative. Integrated. Whether you are a continuing student or working professional, Oregon State University’s Master of Business Administration prepares you for the challenges of today’s global marketplace. Through experiential learning, you’ll cultivate an entrepreneurial mindset that emphasizes social responsibility, sustainability, and ethics. Complete your degree in as little as nine months. Evening classes available. Global Top 100 www.bus.oregonstate.edu 2 OSU College of Business 2010 Alumni and Business Partner Awards A word from OSU President Ed Ray By Edward J. Ray, President Brown, who retired from a tre- the many reasons why the college that emphasize experiential learn- Oregon State University mendously successful career as a continues to grow in size, impact ing and for students who graduate PricewaterhouseCoopers partner and reputation. Enrollment last prepared to make a difference, Oregon State University has and now teaches at OSU as an fall included 2,327 undergraduate the college is now on the cusp of always been a place with a pur- Executive in Residence—embody and graduate students, compared a bold and exciting new era. As pose—that of making a measure- the very best of Oregon State. Their to 1,775 just ten years ago. Like state and business leaders look able difference in the lives and professional contributions and the rest of our university, the col- with growing consistency to our communities -

Les Schwab Commercial Credit Application

COMMERCIAL CREDIT APPLICATION LES SCHWAB TIRE CENTERS AND AFFILIATED DEALERS Account# Account Type C 30 90 EP Salesman Price$ Down Payment$ Approved By 1. Individual or Firm Name Number of Years in Business Phone Sole Owner Partnership - State of Organization: Corporation or Limited Liability Company - State of Organization: Street Address City State Zip Address of Principal Place of Business or Mailing Address City State Zip Federal Tax I.D. Number Sales Tax Exempt Number Federal Excise Tax Number 2 Authorized Purchasers, Agents or Buyers Buyer(s) hereby agree to provide written notice of any and all Purchase Orders Required? Yes No future revisions to, or additions of, authorized purchasers. Controller/Payable Manager INCOME REFERENCE 3 Bank Name & Address Phone Account Type & Account Number Savings Account Checking Account Bank Name & Address Phone Account Type & Account Number Savings Account Checking Account Are You Currently a Party to a Lawsuit? Yes No Any Outstanding Judgments? Yes No Ever Been a Debtor Bankruptcy? Yes No Are You Listed with Dun & Bradstreet? Yes No If yes, what jurisdictions, courts, and case numbers? Are You a Guarantor or Co-signer? Yes No Have You Any Other Major Liabilities? Yes No Do Creditors Offer You Skip Payments? Yes No Equipment Lender Name & Address Monthly Payment Account Balance Equipment Lender Name & Address Monthly Payment Account Balance Other Reference Name & Address Monthly Payment Account Balance Other Reference Name & Address Monthly Payment Account Balance 4 Principal/Officer & Title Social Security Number Driver’s License Number Home Address Phone Date of Birth Principal/Officer & Title Social Security Number Driver’s License Number Home Address Phone Date of Birth Les Schwab Commercial Credit Plan and Security Agreement I. -

Les Schwab Headquarters

BUSINESS Success Story PROJECT BENEFITS • Reduced energy consumption LES SCHWAB • Lowered building operating costs • Conserved water both inside and HEADQUARTERS outside the building • Created a building that reflects PRIDE IN PERFORMANCE the company’s core value of “Pride in Performance” The right tires can make a big difference in the performance of a vehicle. So it makes sense that Les Schwab Tire Centers put a premium on high performance ENERGY SAVINGS AND SOLAR GENERATION when they began planning their new headquarters in Bend. After all, the company- wide core value at Les Schwab is “Pride in Performance.” • Annual savings of 383,775 kWh of electricity Their 123,000-square-foot office building, completed in November 2008, uses • Annual savings of 4,933 therms 25 percent less energy than a building of similar type and size built to Oregon of natural gas code. They’re also generating a portion of the building’s electricity with a robust • Estimated solar power generation of 37,890 kWh hours of electricity solar electric system. As a result of energy saved and generated, the company per year is pocketing an additional $34,972 in annual energy cost savings. Such stellar performance is the direct result of energy-efficient and renewable technologies, FINANCIAL ANALYSIS made affordable with Energy Trust of Oregon cash incentives. • $71,413 incentive from Energy Trust (energy-efficiency The road to high performance upgrades) Working with GBD Architects, Les Schwab implemented a wide range of design • $43,173 incentive from strategies to meet their energy goals. Tanner Creek Energy, LLC installed a Energy Trust (solar electric 36-kilowatt grid-tied roof-mounted solar electric system that generates enough system) electricity to power one-half of one wing of the building. -

AGENDA Mccall City Council Regular Meeting November 3, 2011 at 5:30 P.M

AGENDA McCall City Council Regular Meeting November 3, 2011 at 5:30 p.m. McCall City Hall (Lower Level) Legion Hall 216 East Park Street The times listed are estimated times only. The Council reserves the right to alter the times as necessary. 5:30 p.m. OPEN SESSION ROLL CALL APPROVE THE AGENDA 5:35 p.m. PRESENTATION Appreciation of the Varsity Girls Soccer Team State Championship 5:40 p.m. DEPARTMENT REPORTS COMMITTEE MINUTES 1. McCall Airport Advisory Committee – September 1, 2011 2. Golf Advisory Committee – July 13, 2011 3. Golf Advisory Committee – September 14, 2011 4. Library Board of Trustees – August 17, 2011 5. Library Board of Trustees – September 20, 2011 6. McCall Improvement Committee – April 14, 2011 7. McCall Improvement Committee – September 8, 2011 8. McCall Improvement Committee – October 13, 2011 9. McCall Urban Redevelopment Agency – September 20, 2011 10. Planning and Zoning Commission – September 13, 2011 PLEDGE OF ALLEGIANCE 6:00 p.m. PUBLIC COMMENT At this time, the Mayor will call for any comments from the public on any subject whether or not it is on the agenda for any item(s) the public may wish to bring forward and discuss. Please limit comments to three (3) minutes. The City Council does not take any action or make any decisions during public comment. To request Council action during the Business portion of a Council meeting, contact the City Manager at least one week in advance of a meeting. BUSINESS AGENDA 6:05 p.m. AB 11-199 Library Board of Trustees Appointment MCCALL CITY COUNCIL AGENDA Page 1 of 2 November 3, 2011 Regular 6:10 p.m. -

Participating Merchant List

1st Street Tax Service, LLC Payroll, Accounting & Tax Service Mailing Address: Physical Address: 1556 E. 1st Street same Newberg, Oregon 97132 503‐867‐6124 [email protected] n/a Facebook Page: n/a Discount percentage: 20% Amount of Discount: Any Restrictions: Personal taxes only Participating Merchant since: 4/29/2015 3rd Street Pizza Company Pizza & Sandwich shop Mailing Address: Physical Address: 433 NE 3rd St same McMinnville, Oregon 97128 503‐434‐5800 [email protected] www.3rdstreetpizza.com Facebook Page: www.facebook.com/3rdStreetPizza Discount percentage: 10% Amount of Discount: Any Restrictions: none Participating Merchant since: 2/17/2016 Aero Lock & Safe, Inc. Locksmith ‐ Full Service Mailing Address: Physical Address: 3302 Portland Rd. same Newberg, Oregon 97132 503‐538‐0505 [email protected] www.aerolocksafe.com Facebook Page: n/a Discount percentage: 10% off Amount of Discount: on regular priced goods & services Any Restrictions: Not good with other coupons or offers Participating Merchant since: 11/20/2015 American Legion Veterans Club Restaurant & Event Room Mailing Address: Physical Address: 126 NE Atlantic St same McMinnville, Oregon 97128 503‐435‐2218 [email protected] http://vetsclub.org Facebook Page: n/a Discount percentage: 5% Amount of Discount: current year legion member 10% Any Restrictions: must show card / no discounts on alcohol Participating Merchant since: 2/11/2015 AmeriTitle Title & Escrow Services Mailing Address: Physical Address: 106 NE 8th St same McMinnville, Oregon 97128 503‐554‐8500 analiese.jones@ameri‐title.com -

Housing Opportunity Program

NEW ISSUE RATINGS: 2005 Series C − Moody’s Aa2 BOOK-ENTRY ONLY 2005 Series D − Moody’s Aaa (Ambac-Insured) In the opinion of Preston Gates & Ellis LLP, Bond Counsel, interest on the 2005 Series C Bonds is included in gross income subject to federal income taxation. Interest on the 2005 Series C Bonds is exempt from Oregon personal income tax and is also exempt from personal income taxation by Multnomah County, Oregon. See “TAX MATTERS” herein. In the opinion of Preston Gates & Ellis LLP, Bond Counsel, assuming compliance with certain covenants of the City, interest on the 2005 Series D Bonds is excluded from the gross income of the owners of the 2005 Series D Bonds for federal income tax purposes under existing law. Interest on the 2005 Series D Bonds is not an item of tax preference for purposes of either individual or corporate alternative minimum tax. Interest on the 2005 Series D Bonds may be indirectly subject to corporate alternative minimum tax and certain other taxes imposed on certain corporations. Interest on the 2005 Series D Bonds is exempt from Oregon personal income tax and is also exempt from personal income taxation by Multnomah County, Oregon See “TAX MATTERS” and “OTHER FEDERAL TAX MATTERS” herein. City of Portland, Oregon $3,170,000 $6,975,000 Limited Tax Housing Limited Tax Housing Revenue Bonds Revenue Bonds 2005 Series C 2005 Series D (Federally Taxable) (Tax-Exempt) (Housing Opportunity Program) (Housing Opportunity Program) BASE CUSIP: 736704 DATED: Date of Delivery DUE: June 1, as shown on inside cover The City of Portland, Oregon, Limited Tax Housing Revenue Bonds, 2005 Series C (Federally Taxable) (Housing Opportunity Program) (the “2005 Series C Bonds”) and Limited Tax Housing Revenue Bonds, 2005 Series D (Tax Exempt) (Housing Opportunity Program) (the “2005 Series D Bonds” and, collectively with the 2005 Bonds, the “2005 Bonds”) will be issued in registered book-entry form only without coupons in denominations of $5,000 or integral multiples thereof. -

2007 Reimbursements

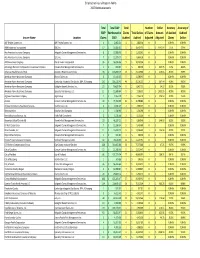

Employer-at-Injury Program Audits 2007 Reimbursements Total Total EAIP Total Number Dollar Accuracy Accuracy of EAIP Reimbursed in Claims Total Dollars of Claims Amount of Audited Audited Insurer Name Location Claims 2007 Audited Audited Adjusted Adjusted Claims Dollars ABF Freight System, Inc. ABF Freight System, Inc. 4$ 2,803.54 4$ 2,803.54 0$ - 100.0% 100.0% ABM Industries Incorporated ESIS, Inc. 17$ 19,266.32 5$ 10,424.73 5$ 4,442.04 0.0% 57.4% Ace American Insurance Company Sedgwick Claims Management Services Inc. 8$ 17,988.93 5$ 11,302.62 0$ - 100.0% 100.0% Ace American Insurance Company ESIS, Inc. 7$ 11,973.17 5$ 8,064.18 0$ - 100.0% 100.0% ACIG Insurance Company Eberle Vivian Incorporated 36$ 96,816.86 9$ 10,200.54 0$ - 100.0% 100.0% Advantage Workers Compensation Insurance Company Pinnacle Risk Management Services, Inc. 1$ 660.00 1$ 660.00 1$ 123.75 0.0% 81.3% Adventist Health System/West Adventist Health System/West 38$ 106,883.74 10$ 23,738.88 2$ 250.85 80.0% 98.9% American Home Assurance Company Chartis Claims, Inc. 6$ 13,111.35 5$ 11,586.93 0$ - 100.0% 100.0% American Home Assurance Company Cambridge Integrated Svs Grp Inc. DBA: XChanging 193$ 166,118.41 49$ 35,291.53 2$ 167.44 95.9% 99.5% American Home Assurance Company Gallagher Bassett Services, Inc. 23$ 50,029.94 6$ 8,027.73 1$ 34.50 83.3% 99.6% American Home Assurance Company Specialty Risk Services, LLC 11$ 11,849.64 5$ 7,289.55 1$ 1,421.55 80.0% 80.5% Argonaut Insurance Company Argo Group 2$ 2,364.10 2$ 2,364.10 1$ 578.18 50.0% 75.5% Asante Cannon Cochran Management Services Inc. -

AMENDED - AGENDA Mccall City Council Regular Meeting June 12, 2014 at 5:30 P.M

AMENDED - AGENDA McCall City Council Regular Meeting June 12, 2014 at 5:30 p.m. McCall City Hall (Lower Level) Legion Hall 216 East Park Street The times listed are estimated times only. The Council reserves the right to alter the times as necessary. 5:30 p.m. OPEN SESSION ROLL CALL APPROVE THE AGENDA DEPARTMENT REPORTS COMMITTEE MINUTES 1. Airport Advisory Committee – April 3, 2014 2. Environmental Advisory Committee – March 18, and April 15, 2014 3. Historic Preservation Commission – January 21, 2014 4. McCall Public Library Board – February 27, and April 15, 2014 5. McCall Improvement Committee – April 3, 2014 6. McCall Redevelopment Agency – April 15, 2014 7. Planning and Zoning Commission – April 1, and May 6, 2014 8. Public Art Advisory Committee – April 23, 2014 9. McCall Tree Advisory Committee – March 4, 2014 PLEDGE OF ALLEGIANCE 6:00 p.m. PUBLIC COMMENT At this time, the Mayor will call for any comments from the public on any subject whether or not it is on the agenda for any item(s) the public may wish to bring forward and discuss. Please limit comments to three (3) minutes. The City Council does not take any action or make any decisions during public comment. To request Council action during the Business portion of a Council meeting, contact the City Manager at least one week in advance of a meeting. BUSINESS AGENDA 6:05 p.m. AB 14-116 Golf Advisory Committee Member appointment – Roger Snodgrass 6:10 p.m. AB 14-109 Live Music by the Lake Request to Extend the Noise Ordinance MCCALL CITY COUNCIL AGENDA Page 1 of 2 June 12, 2014 Regular AMENDED 6/9/14 TO ADD AB 14-118 Issuance of a Letter Permitting the Use of Rotary Park for the Construction of the Lardo Bridge Pending the development of an Agreement Detailing the Conditions of Use 6:20 p.m.